Oil and Gas Electrification Market Size by Type, Application, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

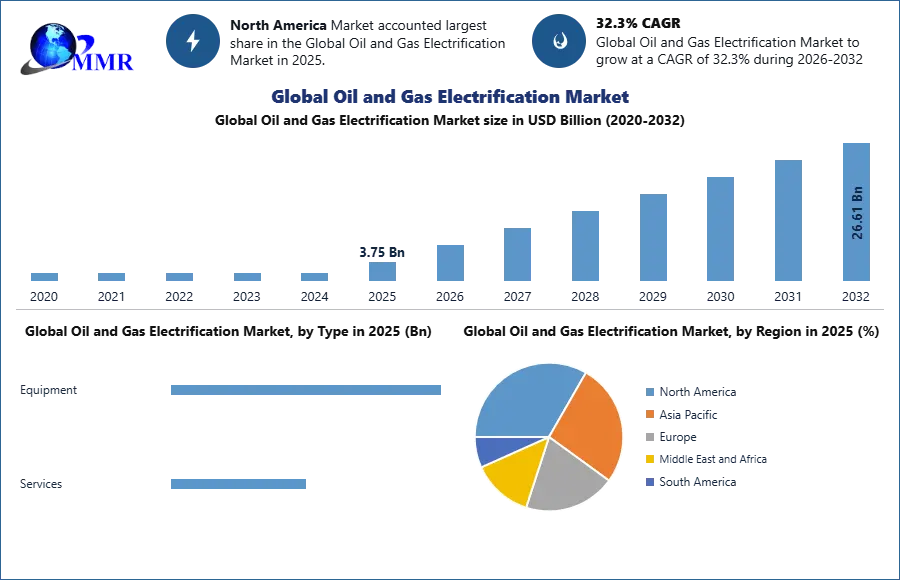

The Global Oil and Gas Electrification Market size was valued at USD 3.75 Billion in 2025 and the total Oil and Gas Electrification revenue is expected to grow at a CAGR of 32.3% from 2026 to 2032, reaching nearly USD 26.61 Billion.

Oil and gas electrification is a process of integrating electrical technologies into various aspects of the oil and gas industry to improve efficiency, reduce greenhouse gas emissions, and lower operational costs. Oil and gas electrification is part of the broader transition towards a more sustainable and environmentally responsible energy sector. It not only helps reduce the industry's impact on the environment but also positions it to adapt to changing energy landscapes and regulations. However, the degree of electrification in the oil and gas sector may vary depending on factors such as the availability of renewable energy sources, local regulations, and the specific operations of each facility.

The global energy landscape is undergoing a transformative shift with electrification emerging as a vital pathway to achieving net-zero emissions. This factor is expected to support the oil and gas electrification market growth. As the share of electricity in total final energy consumption continues to rise, several countries are making significant strides in this direction. China's remarkable adoption of electric vehicles and France and the United States witnessing heat pumps outselling fossil-fuel heating systems highlight this trend, further boosting the oil and gas electrification market revenue growth. The electrification of transportation, industry, and residential sectors is essential to reduce emissions, enhance energy efficiency, and integrate renewables effectively. Policymakers all across the world are taking steps to foster electrification through infrastructure development, subsidy schemes, and awareness campaigns, benefiting the oil and gas electrification market.

The oil and gas industry’s significant transformation in response to global energy transitions and the imperative to reduce greenhouse gas emissions is further expected to increase the oil and gas electrification market size during the forecast period. This shift is driven by both environmental pressures and the need to align with the goals of the Paris Agreement. While the focus is often on the major integrated oil and gas companies, they account for a fraction of global reserves and production. The majority of production and reserves are controlled by national oil companies (NOCs). The industry is exploring diversification into low-carbon sectors, with a portion of capital allocated to renewable energy, electric vehicle charging, and battery technologies.

Significantly, oil and gas companies are expected to contribute to emissions reduction by providing clean fuels and investing in low-carbon hydrogen, biomethane, and advanced biofuels. The deployment of technologies like carbon capture, utilization, and storage (CCUS), offshore wind, and advanced biofuels relies on the industry's engineering and project management capabilities. While transitioning towards cleaner energy sources is essential, oil and gas production remains necessary, albeit with a shift towards lower-cost and environmentally sustainable practices, thereby driving the oil and gas electrification market.

To know about the Research Methodology :- Request Free Sample Report

Oil and Gas Electrification Market Dynamics:

Supportive Government Regulations

Supportive government regulations and policies are playing a critical role in the Oil and Gas Electrification Market. The global energy landscape is undergoing a profound transformation as governments all across the world are actively endorsing decarbonization and emission-reduction technologies, particularly in the upstream oil and gas sector. This profound shift is led by countries including Australia, Canada, Denmark, Norway, the Netherlands, the United Kingdom, and the United States, which have been at the forefront of establishing regulatory frameworks to facilitate the energy transition within the industry. Carbon capture, utilization, and storage (CCUS), a technology that has received substantial attention in the endeavor to reduce carbon emissions, is one of the primary areas of concentration within this regulatory framework. Governments are investing in CCUS research and development, pilot projects, and commercial-scale developments, often through financial participation or tax credits.

Additionally, blue hydrogen projects, closely linked to CCUS, are being incentivized, especially as carbon storage infrastructure expands. These supportive mechanisms are integral drivers of low-carbon investment and electrification efforts within the oil and gas sector. The emphasis on offshore wind and floating offshore wind, which are used to electrify oil and gas platforms is expected to be a significant aspect of this government support. This backing, notably in North Sea regions, opens new avenues for the decarbonization of producing platforms. Government engagement varies across regions, with North America and Australia adopting a policy of limited intervention in the oil and gas industry, emphasizing market mechanisms, budgetary funding for research, and tax incentives. In contrast, European governments take a more direct role in low-carbon projects aimed at reducing emissions, with state-owned enterprises actively participating in CCS projects and facilitating collaboration across the value chain. In January 2022, several of these oil and gas-producing countries reaffirmed their commitment to creating a conducive environment for decarbonization projects. These commitments range from budget allocations to tax credits and support for low-carbon energy sources, further bolstering the attractiveness of the Oil and Gas Electrification Market. This governmental support, marked by stable policies and transparent incentive schemes, is expected to be instrumental in expanding decarbonization projects within the oil and gas sector. As governments work in coordination with the private sector, research institutions, and civil society, the market for electrification in the oil and gas industry is poised for significant growth, facilitating a more sustainable and environmentally responsible future.

In January 2022, several of these oil and gas-producing countries reaffirmed their commitment to creating a conducive environment for decarbonization projects. These commitments range from budget allocations to tax credits and support for low-carbon energy sources, further bolstering the attractiveness of the Oil and Gas Electrification Market. This governmental support, marked by stable policies and transparent incentive schemes, is expected to be instrumental in expanding decarbonization projects within the oil and gas sector. As governments work in coordination with the private sector, research institutions, and civil society, the market for electrification in the oil and gas industry is poised for significant growth, facilitating a more sustainable and environmentally responsible future.

Recent announcements signal further support to come:

Several of these producers have put forth policy initiatives that underline their resolute dedication to enhancing the investment environment for decarbonization projects in the oil and gas sector in the first five months of 2022.

| Country | Policy Initiatives | Key Focus | Expected Impact |

| Australia | AUSD 300 million for low-emissions LNG, blue hydrogen, and CCUS in Darwin | Emissions reduction, green hydrogen, renewables, expanded carbon credits | Development of a potential low-carbon energy hub, ongoing support for initiatives introduced by the prior government |

| Canada | Tax credit for CCUS projects in the 2023 budget | Permanent storage of captured CO2, excluding EOR | Tax credit rate ranging from 37.5% to 60%, CUSD 2.2-billion recapitalization of Low Carbon Economy Fund |

| United States | USD 2.25-billion Carbon Storage Assurance Facility Enterprise (CarbonSAFE) Initiative | Commercial storage of 50 MMt of CO2 over 30 years, methane rule, oil and gas equipment upgrades | Balance short-term production growth with emission reduction, potential delay due to legal challenges and midterm elections |

| United Kingdom | Adoption of the Energy Security Bill | Formalizing business models for CCUS projects, risk mitigation arrangements | Strengthened carbon storage initiatives, regulatory enhancements, and expedited project reviews and approvals |

Increasing Demand for Low-Carbon Electricity

The increased demand for low-carbon electricity generation, driven mostly by solar and wind deployment, underscores the global commitment to mitigate climate change. Furthermore, policymakers are increasingly recognizing the merits of nuclear energy in this environment. This shift towards cleaner energy sources is challenging the traditional energy landscape. While power utilities have modernized their fossil fuel assets and improved resource efficiency, including the transition from coal to natural gas, the pace of this multifaceted transition remains insufficient to avert the most severe consequences of climate change. Despite revised policy ambitions, support for innovation, and heightened investments in low-carbon capacities, fossil fuels continue to meet a significant portion of global electricity needs, reflecting the persistent demand for more sustainable energy alternatives. The future of power systems is expected to be a significant integration of variable power generation sources, necessitating a more flexible operation of existing and new power capacities.

This transformation also relies on power interconnectors, demand-side management strategies, and energy storage solutions, including behind-the-meter devices. Operators within the oil and gas industry need to adapt their business models and value propositions to thrive in increasingly competitive environments characterized by demanding regulatory regimes. Strict policy enforcement by governments, in collaboration with the private sector, research institutions, and civil society, is essential to accelerate the transition toward low-carbon electricity. This collective effort is vital in achieving the ambitious 2050 objective of reducing the carbon intensity of electricity to under 50 gCO2 per kWh. Thus, the Oil and Gas Electrification Market stands to benefit significantly from the increasing demand for low-carbon electricity. As industries seek to reduce their carbon footprint and align with sustainability goals, the electrification of oil and gas operations becomes an attractive solution, further driving its market growth and reshaping the energy landscape.

Offshore Oil & Gas Companies Rapidly Electrifying Platforms

The rapid electrification of offshore platforms within the oil and gas industry is expected to offer lucrative growth opportunities, with profound implications for the Oil and Gas Electrification Market. Historically, offshore oil and gas operations have heavily relied on polluting fossil fuels, incurring substantial costs and environmental consequences. Each offshore platform typically utilized multiple diesel generators, resulting in investments as high as USD 25 million per year, coupled with substantial carbon emissions. To combat these challenges, the industry is increasingly transitioning to electricity generated through renewable energy sources, both onshore and offshore. Breakthroughs in renewable technology, including offshore wind turbines and advanced power storage, are making electrification a practical and economically viable choice. For instance,

Equinor's Johan Sverdrup Field, North Sea (Norway): Equinor's Johan Sverdrup Field represents a pivotal achievement in offshore electrification. In 2019, Equinor made a transformative move by establishing a connection between this offshore platform and the Norwegian power grid. This strategic shift marked a significant milestone as it substantially reduced the platform's reliance on traditional fossil fuel-based power generation methods. By integrating with the mainland power supply, Equinor demonstrated its commitment to embracing cleaner and more sustainable energy sources, contributing to reduced carbon emissions and greater operational efficiency.

Hywind Tampen Project, North Sea (Norway): Equinor's launch of the Hywind Tampen project in the North Sea in 2022 is emblematic of the industry's proactive approach to electrification. This pioneering project stands as the world's inaugural floating wind farm specifically designed to provide renewable power to offshore oil and gas installations. The innovative nature of this initiative showcases the oil and gas sector's dedication to cleaner energy solutions. By harnessing the power of offshore wind, the Hywind Tampen project exemplifies the drive to reduce carbon emissions, decrease operational costs, and contribute to a more sustainable offshore energy landscape.

Petrobras FPSO Maria Quitéria (Brazil): Petrobras is actively pursuing the electrification of its Floating Production Storage and Offloading (FPSO) vessel, Maria Quitéria, in a bid to curtail fuel consumption and emissions. While the exact implementation date remains unspecified, this endeavor underscores the broader industry trend toward adopting cleaner and more environmentally responsible power sources. The planned deployment of a combined-cycle power generation system reflects Petrobras' commitment to reducing its environmental footprint and enhancing operational efficiency, even in the context of complex offshore operations. This move aligns with the company's commitment to sustainability and aligning with global environmental goals.

Companies are benefiting from this shift in several ways:

1. Renewable Energy Integration: Incorporating wind and solar power into offshore platforms enables diversification of the energy portfolio, reduces carbon footprint, and lessens dependence on fossil fuels.

2. Cost Efficiency and Operational Benefits: Electrification eliminates the need for on-site fuel storage, transportation, and maintenance, resulting in substantial cost savings. For example, submarine power cables reduce operating costs by nearly USD 1,189,000 compared to gas turbines, while wind energy can save around USD 63 million annually.

3. International Climate Agreements: Offshore electrification aligns with global greenhouse gas reduction targets, as a significant portion of emissions emanates from oil and gas activities.

Various methods are employed to achieve offshore platform electrification, including subsea cables for power transmission, offshore wind power integration, combined cycle power generation, and energy storage systems. These technologies ensure a consistent and sustainable power supply, reducing emissions and improving operational efficiency. As a result, the transition to electrification in the offshore sector is expected to be a significant factor, in fostering a cleaner, more cost-effective, and environmentally responsible future for the oil and gas industry. As the world's focus on sustainability intensifies, the Oil and Gas Electrification Market is poised for significant growth, driven by the imperative to reduce carbon emissions and enhance operational efficiency in offshore platforms.

Oil and Gas Electrification Market Trends:

Shift Toward Renewable Energy

The Oil and Gas Electrification Market is witnessing a prominent market trend driven by the broader energy transition sources and towards renewable electrification. This transition represents a global shift from fossil-based energy production and consumption to sustainable and environmentally conscious alternatives, emphasizing a fundamental change in the energy sector. The increasing penetration of renewable energy sources, such as wind and solar, into the energy supply mix, is expected to be the major factor for this shift. Technological advancements and declining costs have made renewable energy highly competitive, with wind power becoming cheaper than traditional high-carbon energy sources in some regions. This shift towards renewables offers substantial growth opportunities within the Oil and Gas Electrification Market, as companies seek cleaner and more sustainable energy sources.

Additionally, the onset of electrification and the growing adoption of electric transportation infrastructure are playing a pivotal role in driving this trend. The transition to electric vehicles (EVs) is one of the most significant areas for electrification, with the global EV adoption rate expected to reach 10%-12.5% by 2025. Electrification offers a cleaner and more efficient power transportation solution, aligning with the goals of the energy transition. Energy storage is another critical factor, with the potential to address the intermittent nature of renewable energy sources. As energy storage costs continue to fall, it is becoming increasingly viable for broader use. Energy storage solutions are integral to ensuring constant and reliable power supplies, enhancing the overall effectiveness of renewable energy technologies.

The energy transition's impact is not limited to the energy sector; it also aligns with broader environmental and sustainability goals, including commitments to reduce greenhouse gas emissions and achieve a carbon-neutral economy. Investors and companies are increasingly prioritizing environmental, social, and governance (ESG) factors, emphasizing the significance of this market trend. Although global regulatory structures related to the energy transition have been mixed, there is growing momentum towards lower greenhouse gas-emitting power generation and a clean energy economy in regions such as Europe, the U.S., and emerging economies like China. As a result, the energy transition towards renewable energy sources, electrification, and energy storage driving the Oil and Gas Electrification Market's growth by providing cleaner, more sustainable, and economically attractive energy solutions.

Oil and Gas Electrification Market Segment Analysis:

Based on the Type, the Electric vehicles segment held the largest market share of 32% and dominated the global oil and gas electrification market in 2025. The substantial reduction in emissions offered by EVs when compared to their conventional internal combustion engine (ICE) counterparts is expected to be the major factor driving the segment growth. As environmental awareness increases, oil and gas companies are increasingly cognizant of their carbon footprint and are actively incorporating EVs into their fleets to mitigate it. This move harmonizes with the global imperative to curtail greenhouse gas emissions and combat climate change. Moreover, the significant efficiency of the electric motors powering EVs, operating at efficiency rates typically ranging from 85% to 90%, presents a significant advantage. This efficiency substantially outpaces ICE vehicles, resulting in not only lowered emissions but also marked reductions in operating costs and enhanced energy conservation. The economic appeal of reduced fuel and maintenance expenses is a potent driver behind EV adoption, making it an attractive choice for businesses within the oil and gas sector. Government initiatives play a pivotal role in supporting this transition. Various governments worldwide are implementing policies and incentives, such as tax breaks, rebates, and infrastructure development, to encourage the widespread adoption of electric vehicles. Oil and gas companies are seizing these opportunities to expand their EV fleets, ultimately reducing their environmental impact and operational expenses. For instance,

Government initiatives play a pivotal role in supporting this transition. Various governments worldwide are implementing policies and incentives, such as tax breaks, rebates, and infrastructure development, to encourage the widespread adoption of electric vehicles. Oil and gas companies are seizing these opportunities to expand their EV fleets, ultimately reducing their environmental impact and operational expenses. For instance,

1. The U.S. federal government offers a federal income tax credit of up to USD 7,500 for the purchase of electric vehicles. Many states also provide additional incentives, such as rebates, reduced registration fees, and access to carpool lanes for EV owners.

2. China has been aggressively expanding its EV charging infrastructure. The government has set ambitious goals for the construction of public charging stations to support the growing EV market. This commitment to infrastructure development has encouraged the adoption of electric vehicles.

3. The EU has set stringent emissions targets for automakers, pushing them to produce more electric vehicles. It has also established emissions regulations and fines for automakers that do not meet these targets, further incentivizing the production and adoption of EVs.

Additionally, the expansion of charging infrastructure, which includes the proliferation of fast-charging stations, is critical to facilitating the widespread adoption of EVs. The growing accessibility of charging networks bolsters the confidence of oil and gas companies, assuring them that their vehicles are expected to be conveniently recharged at various work sites and facilities. Besides that, the mounting emphasis on environmental, social, and governance (ESG) factors is compelling oil and gas companies to align with sustainability objectives. The adoption of EVs emerges as a tangible way for these companies to demonstrate their commitment to reducing emissions and fostering cleaner transportation.

| EV Market Share in Global Light Vehicle Sales (%) | 2023 H1 | 2022 H1 | Change (Percentage Points) |

| Battery Electric Vehicles (BEVs) | 10% | - | +2.7% |

| Plug-in Hybrids (PHEVs) | 4.1% | - | +1.9% |

| Total EV Market Share (BEVs + PHEVs) | 14.1% | 11.3% | +2.8% |

| Top Countries with EV Market Share (%) | Norway | China | Europe | USA |

| EV Market Share (BEVs + PHEVs) in H1 2023 | 81% | 30.5% | 19.7% | 8.7% |

| Major BEV Sales Leader (H1 2023) | BYD | Tesla |

| Total Sales (including PHEVs for BYD) | 1.25 million | 633,000 |

| Total BEV Sales (Tesla) | - | 889,000 |

Oil and Gas Electrification Market Regional Insights:

The United States and Canada are the leaders in the oil and gas electrification market as these countries are increasingly adopting electrification technologies in the oil and gas industry. This is driven by regulatory pressure to reduce greenhouse gas emissions and operational cost savings. Electrification of end-use services in the oil and gas, transportation, buildings, and industrial sectors coupled with the decarbonization of electricity generation has been identified as one of the key pathways to achieving a low-carbon future in the United States. In addition, Canada is expected to be the potential market for oil and gas electrification market during the forecast period. Canada's commitment to achieving net-zero greenhouse gas (GHG) emissions by 2050 is underpinned by region-specific challenges and opportunities in the oil and gas sector. This transition to a low-carbon economy is a complex endeavor, requiring tailored strategies across the country's provinces and territories.

1. Western Canada: Provinces like Alberta and Saskatchewan, known for their oil and gas production, must navigate the shift from emissions-intensive oil sands to cleaner technologies. Investments in carbon capture and storage (CCS) are vital, with an emphasis on reducing emissions from these resource-rich regions.

2. British Columbia: BC has embraced renewable energy and electrification. Its thriving LNG sector showcases a commitment to cleaner energy in oil and gas operations, setting a regional standard for emissions reduction.

3. Newfoundland and Labrador: In the Atlantic region, offshore oil and gas operations play a pivotal role. Electrification of offshore platforms, such as the Hibernia and Hebron projects, demonstrates the potential for emissions reduction in this remote and challenging environment.

4. Quebec: With a diverse energy portfolio, Quebec leverages hydropower and supports carbon pricing initiatives, contributing to emissions reduction in the oil and gas sector.

5. Eastern Provinces: Provinces like Nova Scotia and New Brunswick, primarily consumers of oil and gas, can reduce emissions by promoting electric vehicles and renewable energy sources.

6. Northern Territories: The unique challenges of remote and harsh climates call for innovative electrification initiatives and indigenous knowledge to achieve emissions reduction.

The Canadian oil and gas sector is actively engaged in pioneering clean technologies and innovation, positioning itself at the forefront of sustainable energy practices. These initiatives align with Canada's ambitious goal of achieving net-zero emissions by 2050.

Clean Technology Investment: Over the past decade, the oil and gas sector has been a prominent contributor to energy research and development, investing approximately USD 1 billion annually, which amounts to 58% of all energy-related R&D investments in the country. Leading companies, such as Shell Canada, Whitecap Resources, Wolf Midstream, Enhance Energy, and Northwest Redwater Partnership, have taken significant strides in carbon capture, utilization, and storage (CCUS) technologies.

Decarbonization Projects: Several companies are committed to decarbonizing their operations. For instance, Pembina Pipeline is investing USD 195 million in wind power to fuel its operations, while Suncor Energy and ATCO are collaborating on a clean hydrogen project, offering a potential 60% emissions reduction at Suncor's Edmonton oil refinery. Tidewater Midstream and Imperial Oil are advancing renewable diesel projects, showcasing the industry's commitment to sustainable practices.

Pathways to Net-Zero: Many Canadian oil and gas companies, including members of the Pathways Alliance, have set net-zero-emissions targets and devised comprehensive decarbonization plans. The Pathways Initiative, comprising major industry players, aims to eliminate 68 million tonnes of emissions from oil sands operations by investing USD 75 billion in clean electrification, emerging technologies like low-emission hydrogen, carbon capture, and small modular nuclear, alongside operational efficiencies and offsets.

Economic Opportunities: The oil and gas sector's expertise positions it to excel in emerging industries. Clean fuels, such as hydrogen, and the production of value-added non-combustion products like asphalt, petrochemicals, zero-carbon fuels, or carbon fibers, present significant opportunities to reduce emissions, create jobs, and contribute to Canada's net-zero future. This industry's commitment to innovation underscores its pivotal role in shaping a sustainable and competitive energy landscape.

As the country grapples with the balance between economic interests and environmental goals, collaboration, innovation, and the effective implementation of cap-and-trade systems and carbon pricing are essential for a successful journey towards net-zero emissions, preserving energy security and economic competitiveness. The transition to a low-carbon future necessitates collective effort and regional adaptation, thereby supporting the oil and gas electrification market growth.

Companies’ Programs Concerning Energy Transition

| Company | Program | Description |

| BP | The energy transition | BP’s business strategy embraces a ‘reduce, improve, create’ framework, which means the reduction of GHG emissions, improvement of products to lower customers’ emissions, and creation of low-carbon businesses. |

| Chevron | Climate change resilience framework | Chevron supports energy transition, however frequently pointing out, that transitions “can take decades” and highlighting this particular low-carbon transition’s long-term nature. Primary focuses in sustainable activities are energy efficiency, CCS, renewables, flaring, and methane reduction. |

| Eni | Path to decarbonization | Eni has established a decarbonization strategy and has its goal to become a leader in energy transition with the priority target of reaching a net zero carbon footprint upstream in 2030. The strategy is based on energy efficiency and GHG reduction, a low-carbon portfolio, renewables, and circularity. |

| Equinor | From an oil company to a broad energy company | Equinor aims to be at the forefront of energy transition and has set a low-carbon approach as one of three sustainability priorities. Moreover, it was rated as the most prepared for energy transition among O&G companies by CDP. Three components of the company’s strategy are making the transition happen: GHG emissions reduction in O&G operations with “natural gas as a part of climate solution”, renewables, and portfolio resilience. |

| ExxonMobil | Environmental, social, and governance (ESG) concept | Exxon is employing mainly an ESG framework, thus contributing to many sides of sustainable development. The company’s position in terms of energy transition is that “Oil will continue to play a leading role in the world’s energy mix” as there will be growing energy demand from heavy-duty transportation. Therefore, Exxon works on making its current products more competitive and also enhances its activity in biofuels, CCS, and energy efficiency. |

| Shell | Shell Energy Transition Report | Shell’s business strategy is aligned with the energy transition challenge. The company works on preparation to become resilient through future shifts to lower-carbon energy systems. The main ambition is “to halve the Net Carbon Footprint of the energy products by 2050”. Key actions in terms of building resilience and enabling transition include reducing GHG, expanding in lower-emissions businesses – natural gas business and electricity, and developing new solutions – biofuels and CCS. |

| Sinopec | Energy transition | Sinopec is actively involved in China’s green and low-carbon transition and has a vision that “hydrogen is key to foster the energy transition”. The company’s actions also include improving energy efficiency, growth of natural gas share, development of alternative energy, and GHG emissions management. |

Recent Key Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 12 December 2025 | ONE-Dyas | The company successfully commissioned the N05-A gas platform as the first natural gas production facility in the Dutch and German North Sea to be powered entirely by offshore wind energy. | This breakthrough eliminates nearly all Scope 1 emissions from drilling and production, setting a new sustainability benchmark for offshore electrification in Europe. |

| 08 October 2025 | ABB | ABB signed a strategic agreement to supply advanced automation and electrification systems for a green ammonia FPSO vessel offshore Portugal. | The integration of a 300-MW electrolyzer on the vessel demonstrates the technical viability of using renewable power for offshore production of low-carbon marine fuels. |

| 22 September 2025 | Government of India | The Indian government implemented a GST reduction from 12% to 5% on solar energy devices and parts used for the electrification of energy infrastructure. | This fiscal policy accelerates the adoption of solar-integrated systems in the energy sector, lowering the cost of renewable transition projects across the region. |

| 15 August 2025 | BP (bpTT) | BP awarded a $19 million construction contract for major electrical infrastructure works at the Sangachal terminal in Azerbaijan as part of its full electrification roadmap. | The project involves phasing out seven gas turbines in favor of grid electricity, significantly reducing carbon intensity and freeing up fuel gas for export. |

| 16 January 2025 | Aker Solutions | Aker Solutions secured a contract to supply electromechanical equipment, including turbines and control systems, for a modernized power facility intended to support offshore grid stability. | The upgrades provide the flexible power solutions necessary to handle the intermittent nature of renewables in electrified oil and gas operations. |

| 10 February 2026 | U.S. EIA | The EIA released the Short-Term Energy Outlook confirming a 17% increase in solar and wind generation through 2026 to meet rising industrial electricity demand. | The rapid expansion of renewable capacity provides the critical power supply needed to support upstream electrification and carbon reduction targets in 2026. |

Oil and Gas Electrification Market Scope: Inquiry Before Buying

| Global Oil and Gas Electrification Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 3.75 USD Billion |

| Forecast Period 2026-2032 CAGR: | 32.3% | Market Size in 2032: | 26.61 USD Billion |

| Segments Covered: | by Type | Equipment

Services

|

|

| by Application | Upstream

Midstream

Downstream

|

||

| by End-User | Oil Companies (OCs) Oilfield Service Companies (OFSCs) Power Utilities Government Agencies Liquefied Natural Gas (LNG) And Floating LNG (FLNG) Facilities Others |

||

Oil and Gas Electrification Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players/Competitors Profiles covered in the Oil and Gas Electrification Market in Strategic Perspective

1. GE Oil & Gas

2. Schlumberger

3. Rockwell Automation

4. Schneider Electric

5. Siemens AG

6. ABB Group

7. General Electric (GE)

8. Emerson Electric Co.

9. Honeywell International Inc.

10. Baker Hughes, a GE company (BHGE)

11. Vestas Wind Systems

12. Nidec Corporation

13. Bosch Rexroth

14. Caterpillar Inc.

15. Wärtsilä

16. Eaton Corporation

17. Mitsubishi Electric Corporation

18. Parker Hannifin Corporation

19. Toshiba International Corporation

20. Yokogawa Electric Corporation

21. Voith Group

22. Altra Industrial Motion

23. Wood Group (now part of Wood PLC)

FAQs:

1. What are the growth drivers for the Oil and gas Electrification market?

Ans. The Increasing focus on reducing carbon emissions and mitigating climate change, coupled with Supportive policies, tax incentives, and infrastructure development by governments worldwide are expected to be the major driver for the Oil and gas Electrification market.

2. What are the major trends in the Oil and gas Electrification market growth?

Ans. The rise of Electric Vehicles (EVs), Charging Infrastructure Expansion, etc. are expected to be the major trends in the Oil and gas Electrification market.

3. Which region is expected to lead the Global Oil and gas Electrification market during the forecast period?

Ans. North America is expected to lead the global Oil and gas Electrification market during the forecast period thanks to increasingly adopting electrification technologies in the oil and gas industry.

4. What is the projected market size and growth rate of the Oil and gas Electrification Market?

Ans. The Global Oil and Gas Electrification Market size was valued at USD 3.75 Billion in 2025 and the total Oil and Gas Electrification revenue is expected to grow at a CAGR of 32.3% from 2026 to 2032, reaching nearly USD 26.61 Billion.

5. What segments are covered in the Oil and Gas Electrification Market report?

Ans. The segments covered in the Oil and Gas Electrification market report are Type, Applications End-user, and Region.