Oil and gas carbon capture and storage Market Size by Technology, End User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

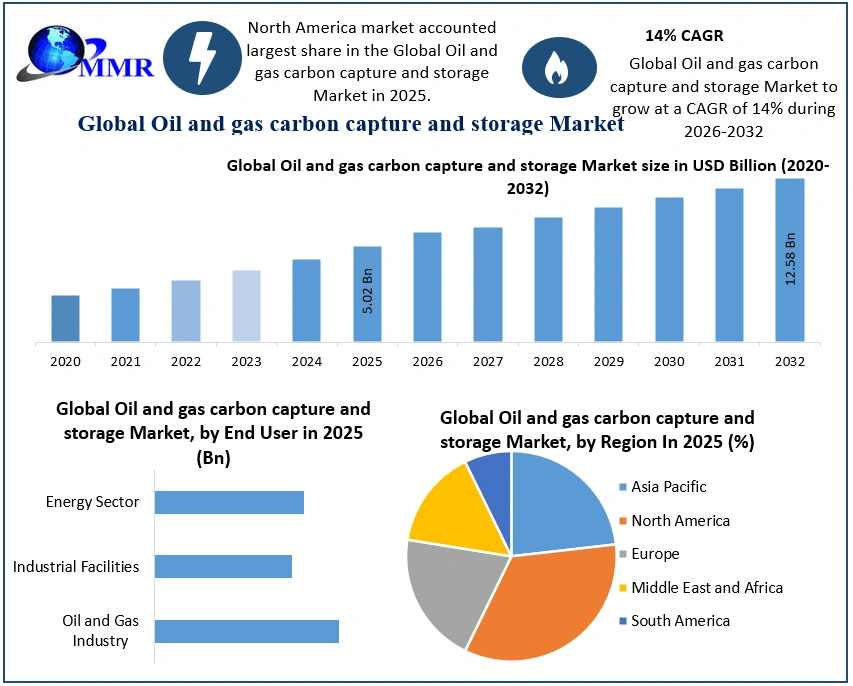

The Oil and gas carbon capture and storage Market size was valued at USD 5.02 Billion in 2025 and the total Oil and gas carbon capture and storage revenue is expected to grow at a CAGR of 14% from 2025 to 2032, reaching nearly USD 12.58 Billion by 2032.

Oil and gas carbon capture and storage market Overview

The oil and gas carbon capture and storage are a crucial component, it aimed to reduce the greenhouse gas emission from oil and gas industry. Governments and Companies are ambitions towards achieving targets and Carbon Capture and Storage (CCS) plays a significant role in Completing those goals. Governments and private projects are allocating significant funding to CCS projects. Investment is essential to scale up CCS and Make it economically viable on a larger scale. The oil and gas sector plays a pivotal role in driving the growth of the CCS market. The oil and gas carbon capture and storage recognizes the importance of CCS in addressing emissions reduction and sustainability goals. The oil and gas industry, as a major player in the Carbon Capture and Storage (CCS) arena, serves as an example of successful CCS implementation. Its experiences and success stories become models for other industries and sectors, encouraging wider adoption of CCS technologies.

To know about the Research Methodology :- Request Free Sample Report

Investment and innovation in the oil and gas industry are pivotal in driving the development and adoption of advanced Carbon Capture and Storage (CCS) technologies. CCS offers the oil and gas industry a unique opportunity to enhance hydrocarbon recovery from depleted reservoirs. Ongoing technological advancements in capture, transportation, and storage methods are a driver for the Carbon Capture and Storage (CCS) market. Innovations improve efficiency, reduce costs, and make oil and gas carbon capture and storage market more feasible for a wider range of applications. CCS projects, especially large-scale applications, require substantial financing. Securing investments and funding for these projects can be a significant challenge. Building public trust and acceptance of Carbon Capture and Storage (CCS) is crucial. Many concerns surround safety, environmental impact, and the long-term security of CO2 storage sites. The Oil and gas carbon capture and storage market is driven by the imperative to reduce emissions, economic benefits, regulatory support, and technological advancements.

Oil and gas carbon capture and storage market Dynamics:

Integration with Enhanced Oil Recovery (EOR)

The growing adoption of EOR techniques in the oil and gas industry is a positive trend for the (Carbon Captured and storage) CCS market. As more oil and gas companies use EOR to enhance hydrocarbon recovery, the demand for CO2 for injection into reservoirs increases. EOR's economic benefits make CCS more attractive. About 30 EOR projects were underway in the Asia-Pacific area as of 2019, with China leading the chemical injection market sector under study. Of these, about 58% fell under the category of CO2 miscible injection or chemical injection. EOR trends align with sustainability goals in the oil and gas industry. EOR allows companies to sustain or increase oil production while addressing emissions reduction objectives. Advances in EOR techniques can lead to more efficient and effective use of injected CO2. As EOR methods become more sophisticated, the efficiency of CO2 utilization increases, promoting the development and improvement of Carbon Captured and storage (CCS) technologies that capture and supply the required CO2. The trends in the Enhanced Oil Recovery (EOR) market, especially its integration with CCS, can have a positive impact on the Oil and Gas Carbon Capture and Storage (CCS) market.

Technological advancements

Technological advancements are a driving force in the Oil and Gas Carbon Capture and Storage (CCS) market. Continuous innovation in CCS technologies is improving efficiency and reducing costs. Innovations in capture methods, transportation infrastructure, and storage practices make CCS more accessible and economically viable. The use of advanced data analytics and machine learning in CCS operations optimizes processes and helps predict and prevent potential issues. Innovations in CCS allow for greater scalability, meaning that CCS technologies can be applied in a wider range of applications and industries. Technological advancements are often tested and validated through pilot projects and demonstrations. Successful projects provide valuable data and build confidence in CCS technologies, encouraging further investment and adoption. Technological advancements often lead to the development of hybrid solutions that combine CCS with other technologies, such as carbon utilization and hydrogen production. These advancements drive efficiency, cost reduction, scalability, and the overall viability of CCS technologies in the Oil and Gas Carbon Capture and Storage market.

Opportunities in Oil and Gas Carbon Capture and Storage (CCS) market

Opportunities in the Oil and Gas Carbon Capture and Storage (CCS) market have a significant impact on the industry's growth and development. Enhanced Oil Recovery (EOR) through CO2 injection offers economic benefits by increasing oil production. The economic viability of EOR combined with CCS presents a significant opportunity for the oil and gas sector to adopt CCS technologies, driving market growth. Increasing regulatory measures to reduce carbon emissions create opportunities for CCS adoption. Governments worldwide are implementing policies, incentives, and carbon pricing mechanisms to encourage CCS projects, further fueling market growth. The commitment of the oil and gas industry, along with public and private investors, to allocate substantial funding to CCS projects represents a major opportunity. Continuous technological advancements in CCS methods and materials open opportunities for improvement. The integration of CCS with other technologies, such as carbon capture and utilization (CCU) and utilization in hydrogen production, presents opportunities for market growth. opportunities in the Oil and Gas Carbon Capture and Storage market are instrumental in its growth and development.

Challenges of Oil and Gas Carbon Capture and Storage (CCS) market

One of the primary restraints is the high costs associated with implementing CCS technologies. The significant investment required for carbon capture, transportation, and storage can deter some companies from adopting CCS solutions, slowing down market growth. Beyond initial investment, operational expenses for maintaining and monitoring CCS facilities can be substantial. The CCS market heavily relies on the development of transportation infrastructure, including pipelines for CO2 transport. The absence of a well-established infrastructure network can limit the feasibility of CCS projects, particularly in regions with inadequate transportation systems. Public acceptance of CCS projects can be a significant challenge. Concerns about the environmental impact of CO2 storage and potential risks associated with leakage or site failure can lead to opposition and resistance to CCS initiatives. Securing financing for large-scale CCS projects can be a significant hurdle. Uncertainty about project viability and returns on investment can make it challenging to attract necessary funding from public or private sources. These restraints can impact the Oil and Gas Carbon Capture and Storage market by affecting project feasibility, costs, and the overall willingness of companies to invest in CCS technologies.

Oil and Gas Carbon Capture and Storage (CCS) market regional insights

North America, Carbon Capture and Storage (CCS) market benefits from a strong oil and gas industry, with the United States and Canada being key players. Support for CCUS is also growing in Canada, which has announced an investment tax credit for CCUS with the goal of reducing emissions by at least 15Mt/year, and CAD 319 million in funding to support CCUS RD&D. In the U.S., regulatory incentives such as the 45Q tax credit have encouraged CCS adoption. The 45Q tax credit provides a financial incentive for companies to capture and store carbon emissions.

Europe is a dominant region for the Carbon Capture and Storage (CCS) adoption, driven by the European union’s commitment to carbon neutrality. Norway, Netherlands, and UK are the leading countries in CSS projects. In Europe, Norway has committed USD 1.8 billion to the Longship project, which includes the Northern Lights offshore storage hub; the Netherlands has committed up to EUR 2 billion through its sustainable energy and climate fund to the Porthos CCUS hub at the Port of Rotterdam the United Kingdom has established a GBP 1 billion CCS Infrastructure Fund with a target of building four CCUS hubs by 2030; and four CCUS projects have been selected in the first funding call for the European Commission’s EUR 10 billion Innovation Fund.

The Asia-Pacific region, including China and Japan, is increasingly interested in CCS, primarily due to its growing industrial sector. China and Japan are focusing on the reducing emission and investments in hydrogen production and storage create opportunities for the CSS Projects. In Asia-Pacific area, there are more than 20 possible hubs and more than 1,300 emitter enterprises in the region. According to MMR analysis, the region is expected to provide over 60% of future CCUS abatement, which translates to more than three gigatons of annual abatement by 2050.

The MENA (Middle East and North Africa) region, with its significant oil and gas operations, sees potential in CCS adoption. The practice of utilizing CCS for Enhanced Oil Recovery (EOR) while reducing emissions aligns with regional economic interests. Countries such as Saudi Arabia are exploring CCS for emissions reduction. ADNOC to Invest in One of the Largest Integrated Carbon Capture Projects in MENA. The project will triple ADNOC's carbon capture capacity to 2.3 mtpa using best-in-class technology, which is the equivalent of taking more than 500,000 gasoline-powered automobiles off the road annually. The project will comprise pipeline infrastructure, a network of wells for CO2 injection, and carbon capture units at the Habshan gas processing plant. ADNOC Gas will build, run, and maintain the project on behalf of ADNOC.

Latin American countries are gradually exploring CCS opportunities. For example, Brazil has investigating in CCS applications in oil and gas sector. It is capture and store carbon dioxide emissions, preventing them from entering the atmosphere. The implementation of CCUS projects in Latin America can provide economic and environmental benefits. It allows countries to reduce carbon emissions while enhancing energy security and sustainability. Regional insights facilitate knowledge sharing and technological exchanges. Countries and regions with advanced CCS expertise collaborate with those looking to develop CCS capabilities, accelerating global CCS adoption. regional insights significantly impact the Oil and Gas Carbon Capture and Storage market by influencing factors such as industry focus, regulatory support, investment climate, and economic conditions.

Oil and gas carbon capture and storage market segments

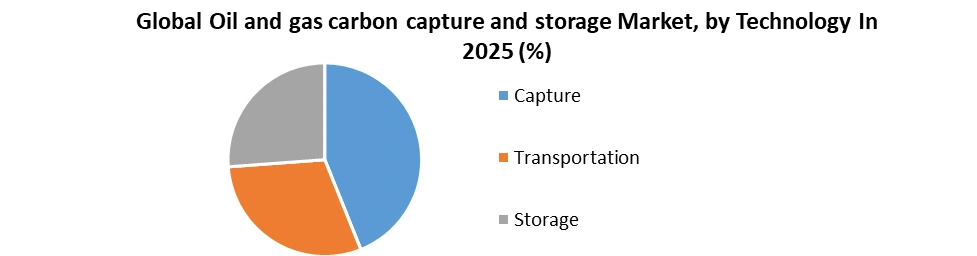

By Technology, Capture technologies are pivotal in the CCS process as they determine how effectively CO2 emissions are captured. There are three types of Combustion technologies such as, Pre-combustion, Post combustion, and Oxy fuel. The development and adoption of advanced capture technologies can significantly impact the market's growth. Innovations that enhance capture efficiency, reduce costs, and make capture feasible in a broader range of applications can drive market growth. Innovations in transportation methods and infrastructure extend the reach of CCS projects. By opening up new geographic markets, transportation technologies contribute to the global growth of CCS applications. Efficient and secure transportation of captured CO2 to storage sites is crucial. The development of cost-effective and environmentally friendly transportation technologies reduces the overall costs of CCS projects and make them more attractive to investors. The development of reliable storage technologies that minimize the risk of CO2 leakage or unintended release is essential for market growth. Innovations in monitoring and verification technologies for storage sites enhance the credibility and safety of CCS projects, influencing investor confidence.

By End-Users, the oil and gas carbon capture and storage (CCS) market by end-users provides insights into how different industries and sectors influence the growth and development of CCS technologies. The commitment of the oil and gas industry to CCS often leads to substantial investments and innovative solutions. Companies in this sector are motivated to develop and implement advanced CCS technologies that enhance carbon capture efficiency and minimize operational costs. CSS is also relevant for heavy industries such as cement production, steel manufacturing, and power generation. The implementation of CSS in industrial settings leads to emissions reductions and improved environmental performance. The energy sector, particularly fossil fuel-based power generation, is another significant end-user of CCS. Government policies and carbon pricing mechanisms impact the market's growth within this sector. The amount to which these industries embrace CCS technologies significantly influences the market's growth and the scale of CCS deployment.

Competitive landscape of Oil and gas carbon capture and storage market

The oil and gas carbon capture and storage industry has observed many small and large products & services providers serve carbon capture methods and storage technology. The industry has observed many small and large products & services providers serve carbon capture methods and storage technology. Many companies have showed significant interests in entering into collaboration agreements to outline the competitive landscape. ExxonMobil has collaborated with various entities on CCS projects, including partnerships with universities and research institutions. For example, ExxonMobil has Collaborated with Global Thermostat, a Technology company focused on direct air capture of CO2. This collaboration aims to explore and advance the development of direct air capture technology, which can capture CO2 directly from the atmosphere. Chevron and Carbon Clean are seeking to develop a carbon capture pilot for Carbon Clean CycloneCC technology on a gas turbine in San Joaquin Valley, California. Chevron is targeting 25 million tonnes of CO₂ per year in equity storage by the end of this decade, with a focus on developing regional hubs that leverage its existing and emerging partnerships with customers, governments, and industry. Equinor Energy AS (Equinor) and Mitsubishi Heavy Industries, Ltd. (MHI) are pleased to announce the signing of a Memorandum of Understanding (MoU) for a low carbon technology collaboration. The non-exclusive cooperation agreement will see both companies develop and use technology to reduce the carbon footprint of oil & gas operations. This will drive the growth of the (Carbon capture utilization and storage) CCUS market, as more resources are allocated to develop and implement carbon capture and storage solutions across oil and gas operations.

Oil and gas carbon capture and storage Market Scope:Inquire Before Buying

| Global Oil and gas carbon capture and storage Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 5.02 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 14% | Market Size in 2032: | USD 12.58 Bn. |

| Segments Covered: | by Technology | Capture Transportation Storage |

|

| by End User | Oil and Gas Industry Industrial Facilities Energy Sector |

||

Oil and gas carbon capture and storage Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players of the Oil and gas carbon capture and storage Market

1. Fluro Corporation (US)

2. ExxonMobil Corporation (US)

3. Linde PLC (UK)

4. Royal Dutch Shell (Netherlands)

5. Mitsubishi Heavy Industries Ltd., (Japan)

6. JGC Holdings Corporation (Japan)

7. Schlumberger.

8. Royal Dutch Shell Plc

9. Jgc Holdings Corporation

Frequently Asked Questions:

1] What is the growth rate of the Oil and gas carbon capture and storage Market?

Ans. The Oil and gas carbon capture and storage Market is growing at a significant rate of over the forecast period.

2] Which region is expected to dominate the Oil and gas carbon capture and storage Market?

Ans. North America region is expected to dominate the Oil and gas carbon capture and storage Market over the forecast period.

3] What was the Global Oil and gas carbon capture and storage Market size in 2025?

Ans: The Global Oil and gas carbon capture and storage Market size was USD 5.02 Billion in 2025.

4] Who are the top players in the Oil and gas carbon capture and storage Industry?

Ans. The major key players in the Oil and gas carbon capture and storage Market are Fluor Corporation (US), ExxonMobil Corporation (US), Linde PLC (UK), Royal Dutch Shell (Netherlands), Mitsubishi Heavy Industries Ltd., (Japan), JGC Holdings Corporation (Japan), Schlumberger.

5] Which factors are expected to drive the Oil and gas carbon capture and storage Market growth by 2030?

Ans Climate Change Mitigation Goals and Energy Transition Strategies Increasing demand for carbon capture and storage (CCS) is expected to drive the Oil and gas carbon capture and storage Market growth over the forecast period (2026-2032).