Next-Generation Sequencing Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

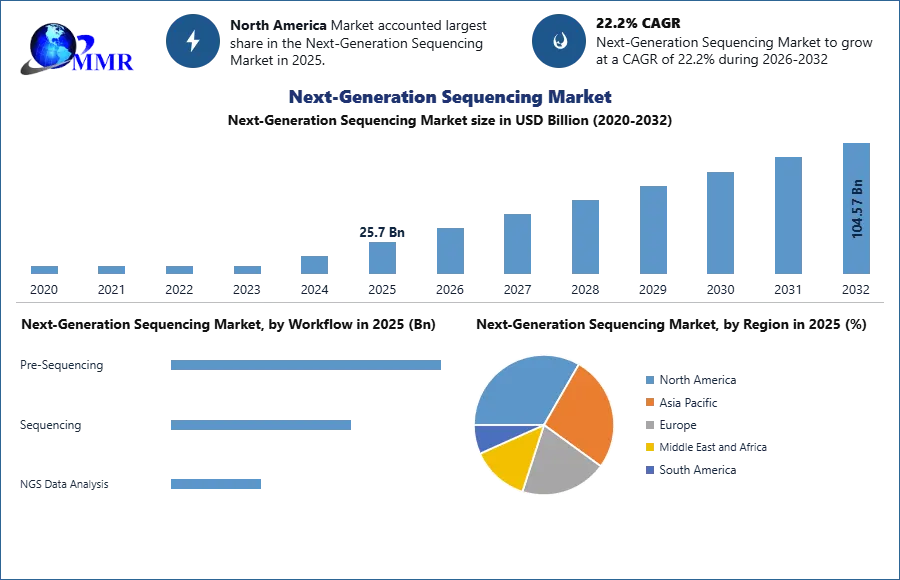

The Next-Generation Sequencing Market size was valued at USD 25.7 Billion in 2025 and the total Next-Generation Sequencing revenue is expected to grow at a CAGR of 22.2% from 2025 to 2032, reaching nearly USD 104.57 Billion.

Next-Generation Sequencing Market Overview

To know about the Research Methodology:- Request Free Sample Report

Global Next-Generation Sequencing Market Overview:

Next-generation sequencing is also known as high-throughput sequencing because it encompasses a variety of advanced sequencing technologies. These new technologies have changed the study of genomics and molecular biology by enabling DNA and RNA to be produced more cheaply, quickly, and without creating as much cost as conventional technologies. The sequential counting of nucleotides to immobilized and spatially arrayed RNA or DNA templates is screened using this next-generation sequencing (NGS) technology. However, there are significant differences between how these RNA or DNA templates are created and how they are interrogated to reveal their sequences. As a result, next-generation sequencing has filled in the holes to meet these higher-level understanding requirements and has become a popular analysis method. The scalability of next-generation sequencing allows for changing the level of precision to satisfy laboratory needs, making it a digital alternative to sequence-based gene expression.

Global Next-Generation Sequencing Market

Drivers:

One of the main factors driving the market's growth is the rising prevalence of chronic medical conditions such as cancer, as well as numerous technical advances in the field of medical sciences. There has been substantial growth in the use of NGS technology as a result of the widespread use of liquid biopsies in cancer diagnostics. Continuous technical advancements in sequencers have allowed the development of reliable, compact, and simple-to-use NGS platforms that can provide fast and accurate results while also reducing turnaround times. The launch of such products and the technology that underpins them gives players an instant competitive advantage; as a result, major corporations are continually relying on product research and development to improve their market positions and share.

Furthermore, the growing use of genome mapping programs to predict the onset of various diseases is fueling the market growth. Scientists use genetic maps to help them figure out which genes are linked to rising rates of diabetes, heart disease, obesity, cancer, and mental disorders. Moreover, numerous technology advances and convergence of cloud-computing platforms for better data processing are positively impacting the market growth. Other trends, such as falling NGS system costs and robust research and development (R&D) activities in the fields of sequencing chemistry, molecular biology, and technological engineering, are expected to fuel the global next-generation sequencing market even more. Other trends, such as falling NGS system costs and robust research and development (R&D) activities in the fields of sequencing chemistry, molecular biology, and technological engineering, are expected to fuel the global next-generation sequencing market even more.

Restraints:

Academic R&D in developed countries is largely reliant on outside finance. Despite government and private sector initiatives to provide funding for research around the world, numerous scientific and university institutes are experiencing budget pressures when it comes to the procurement and usage of sophisticated and high-priced equipment and technology. As a consequence, advanced research facility construction and extension in university and research institutes in developed countries are slowed. This is a major impediment to the implementation of innovations like NGS in developed countries in Africa and Asia.

Global Next-Generation Sequencing Market Segment Analysis:

Based on Technology, Whole Genome Sequencing (WGS) and Whole Exome Sequencing (WES) are the dominant technologies. WGS offers comprehensive analysis by sequencing the entire genome, making it invaluable for applications such as rare disease research, personalized medicine, and oncology. It allows for a deeper understanding of genetic variations that influence health outcomes. WES, while not as exhaustive as WGS, focuses on sequencing the exons, the protein-coding regions of the genome, which comprise about 1-2% of the genome but are known to harbor the majority of clinically relevant variants. WES is widely used in both clinical diagnostics and research due to its ability to identify key genetic mutations associated with diseases like cancer and inherited conditions, offering a cost-effective alternative to WGS.

Based on End User, Academic research institutions held the largest share for the Next-Generation Sequencing Market in 2025. The users of NGS technology are leveraging it for cutting-edge genomic studies, biomarker discovery, and disease pathogenesis understanding. Clinical research also plays a vital role, particularly in the development of precision medicine. Clinical applications, including genetic diagnostics and targeted therapies, are growing rapidly, making clinical research a significant contributor to the NGS market's expansion. Both sectors drive innovation and the adoption of NGS technology, influencing its continued evolution.

Global Next-Generation Sequencing Market Regional Insights:

The North American Next-Generation Sequencing (NGS) market is one of the largest and fastest-growing regions globally, driven by strong healthcare infrastructure, technological advancements, and significant investments in genomics research. The market in this region is primarily fueled by the increasing adoption of precision medicine, rising awareness of genetic diseases, and advancements in biotechnology. The United States holds a dominant position, with major players like Illumina, Thermo Fisher Scientific, and PacBio leading the development of sequencing technologies and platforms. The availability of government funding, along with collaborations between academic institutions, healthcare providers, and pharmaceutical companies, further strengthens the growth of the NGS market in North America.

In addition to its role in clinical diagnostics, NGS is widely used in research areas such as cancer genomics, infectious diseases, and rare genetic disorders, contributing to a surge in demand for sequencing services. The adoption of NGS by hospitals, clinics, and pharmaceutical entities for personalized medicine and drug discovery is expanding rapidly. Moreover, advancements in bioinformatics and data analytics are enhancing the interpretation of NGS data, making it more accessible for clinical and academic purposes. As North America continues to lead in genomic research, the NGS market is expected to maintain robust growth in the coming years.

Recent Developments:

In 2026, Agilent continued strengthening its NGS portfolio by enhancing its target enrichment and library preparation reagents, notably the SureSelect and Avida systems that improve genomic region capture and sequence quality for both research and clinical workflows. Their chemistry‑driven solutions aim to optimize sample preparation and integration with automation and QC platforms, helping laboratories improve accuracy and throughput in targeted sequencing applications. Agilent’s focus remains on seamless end‑to‑end NGS workflows by integrating advanced enrichment, sample‑to‑result solutions, and quality controls, supporting growing demand for high‑performance sequencing in oncology, rare disease research, and personalized medicine.

In 2025, Azenta Inc.: Azenta has been expanding its genomic services business, including NGS sample management, automation solutions, and sequencing services that cater to large‑scale studies. In recent updates, the company emphasized its enhanced biorepository and genomic storage capabilities, improving sample integrity and traceability for high‑volume genomics pipelines. Azenta’s systems are increasingly adopted by pharmaceutical and academic researchers aiming to scale sequencing projects with reliable sample workflows.

Global Next-Generation Sequencing Market Scope: Inquire before buying

| Next-Generation Sequencing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 25.7 USD Billion |

| Forecast Period 2026-2032 CAGR: | 22.2% | Market Size in 2032: | 104.57 USD Billion |

| Segments Covered: | by Technology | WGS (Whole Genome Sequencing) Whole Exome Sequencing Targeted Sequencing & Resequencing DNA-based RNA-based Others |

|

| by Product | Platform Sequencing Data Analysis Consumables Sample Preparation Target Enrichment Others |

||

| by Application | Oncology Diagnostics and Screening Oncology Screening Sporadic Cancer Inherited Cancer Companion Diagnostics Other Diagnostics Research Studies Clinical Investigation Infectious Diseases Inherited Diseases Idiopathic Diseases Non-Communicable/Other Diseases Reproductive Health NIPT Aneuploidy Microdeletions PGT Newborn Genetic Screening Single Gene Analysis HLA Typing/Immune System Monitoring Metagenomics, Epidemiology & Drug Development Agrigenomics & Forensics Consumer Genomics |

||

| by Workflow | Pre-Sequencing Nucleic Acid Extraction Library Preparation Sequencing NGS Data Analysis NGS Primary Data Analysis NGS Secondary Data Analysis NGS Tertiary Data Analysis |

||

| by End Use | Academic Research Clinical Research Hospitals & Clinics Pharma & Biotech Entities Other |

||

Global Next-Generation Sequencing Market, by Region

North America (United States, Canada, Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Poland, Belgium, Netherlands, Rest of Europe)

Asia Pacific (China, South Korea, India, Japan, Australia, Indonesia, Malaysia, Philippines, Thailand, Vietnam, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Rest of South America)

Key players/Competitors profiles covered in the Next-Generation Sequencing Market report in a strategic perspective

- Agilent Technologies Inc.

- Azenta Inc.

- BGI Genomics Co. Ltd.

- 10X Genomics Inc.

- Bio Rad Laboratories Inc.

- Element Biosciences Inc.

- Eurofins Scientific SE

- Hoffman-La Roche Ltd

- Fluidigm

- Fulgent Genetics Inc.

- Guardant Health Inc.

- Illumina Inc.

- Konica Minolta Inc.

- Laboratory Corp. of America Holdings

- Macrogen Inc.

- Merck KGaA

- MilliporeSigma

- Mission Bio, Inc.

- Nabsys Inc.

- NanoString Technologies

- New England Biolabs, Inc.

- OPKO Health Inc.

- PacBio

- PierianDx Inc.

- Promega Corporation

- Psomagen Inc.

- Qiagen N.V.

- Singular Genomics Systems Inc.

- Standard BioTools Inc.

- Takara Bio Inc.

- Thermo Fisher Scientific, Inc.

- Twist Bioscience Corp.