Next Generation Memory Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

The Next Generation Memory Market size was valued at USD 8.43 Billion in 2025, and the total Next Generation Memory revenue is expected to grow at a CAGR of 16.6% from 2026 to 2032, reaching nearly USD 24.7 Billion by 2032.

Next Generation Memory Market Overview:

To know about the Research Methodology :- Request Free Sample Report

Next Generation Memory Market Dynamics:

The Rise of MRAM and ReRAM in Battery-Powered Devices Drives the Next Generation Memory Market Growth

The rapid growth in data from various sources like cloud computing, IoT devices, AI, and big data analytics is a significant driver. For instance, the rise in data-intensive applications, such as autonomous vehicles and smart cities, demands memory solutions that handle large volumes of data with high speed and reliability. Companies like Intel and Micron have developed 3D XPoint memory technology, which provides non-volatile memory that is faster than traditional NAND flash, catering to these high-performance needs. Continuous advancements in semiconductor technology have propelled the development of Next Generation Memory Market. Technologies like MRAM (Magnetoresistive RAM), ReRAM (Resistive RAM), and PCRAM (Phase Change RAM) offer superior performance in terms of speed, endurance, and power consumption. For example, Everspin Technologies' MRAM is being used in automotive applications due to its robustness and speed, which are critical for advanced driver-assistance systems (ADAS).

The increasing awareness and regulatory pressure regarding energy consumption, there is a growing demand for energy-efficient memory solutions. Next-generation memories like MRAM and ReRAM consume less power compared to traditional DRAM and NAND flash, making them suitable for battery-powered devices like smartphones and wearables. Sony’s development of ReRAM is a notable example, where the focus is on creating memory solutions that offer high speed with low power consumption. New applications in AI, machine learning, and edge computing require memory solutions with higher performance and reliability. The adoption of next-generation memory in these applications is a critical driver. IBM's use of Phase Change Memory (PCM) in neuromorphic computing architectures showcases the potential of next-gen memory to revolutionize computing by mimicking human brain functions, thereby offering unprecedented processing power and efficiency which drives the Next Generation Memory Market.

Long-Term Reliability and Market Adoption of Emerging Memory Solutions Boost the Next Generation Memory Market

The high manufacturing costs associated with these advanced memory technologies. For instance, the production of 3D XPoint technology, developed by Intel and Micron, involves complex and expensive manufacturing processes, making it less economically viable for mass Next Generation Memory market applications. Additionally, technological complexities present substantial hurdles. These include issues related to material stability, device reliability, and achieving desired performance metrics, which slow down the development and commercialization of next-gen memory solutions. For example, while ReRAM holds promise due to its superior performance, its development has been hindered by difficulties in achieving consistent and reliable material properties. Moreover, market competition from established memory technologies like DRAM and NAND flash, which continue to improve in performance and cost-efficiency, poses a significant barrier.

Companies and consumers are often hesitant to adopt new technologies that have not yet proven their long-term reliability and cost-effectiveness. The issues related to scalability and integration into existing systems restrain the Next Generation Memory market. For instance, integrating new memory types into current computing architectures is challenging and costly, requiring significant changes to hardware and software. These combined factors create a challenging environment for the widespread adoption of next-generation memory technologies.

Next Generation Memory Market Segment Analysis:

Based on Technology, the market is divided into Non-volatile memory and Volatile memory. Non-volatile memory witnessed the highest Next Generation Memory Market share in 2025 and continued its dominance during the forecast period. The increasing demand for faster, more efficient, and reliable memory solutions. Key technologies in this market include Resistive RAM (ReRAM), Phase Change Memory (PCM), Magnetoresistive RAM (MRAM), and Ferroelectric RAM (FeRAM). ReRAM's high speed and low power consumption make it ideal for IoT devices and edge computing. PCM, with its scalability and durability, is suited for data centers and high-performance computing. MRAM, offering speed and endurance, targets automotive, aerospace, and industrial automation. FeRAM, known for low power use and fast write speeds, is used in smart cards and sensors. The need for fast data access is due to the exponential growth of data, energy efficiency demands, and the push for miniaturization and scalability in electronic devices. Applications span consumer electronics, automotive, and industrial automation drives Next Generation Memory market.

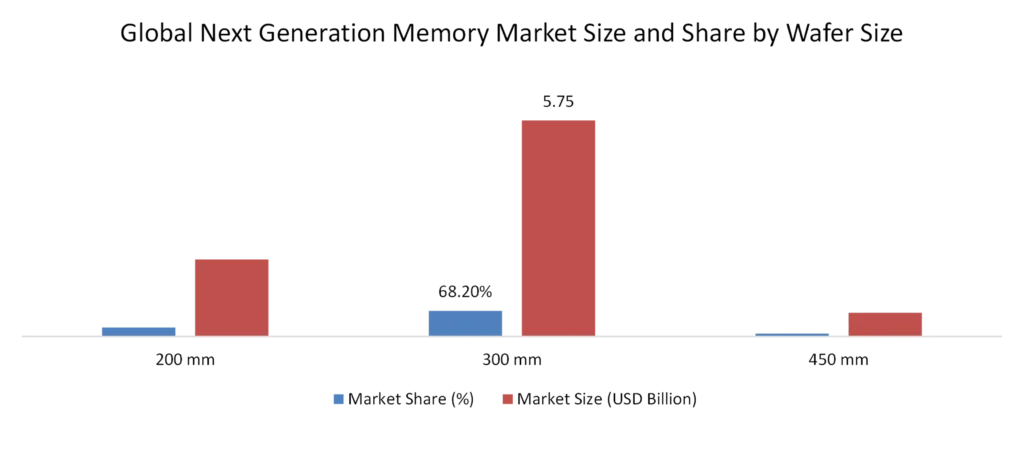

Based on Wafer Size, the Next Generation Memory Market is segmented into 200 mm, 300 mm and 450 mm. In this 300 mm dominated the market 2025 and is expected to dominate in the forecasted period. The 300 mm wafers offer higher yield per wafer, improved cost-efficiency, and are widely used in modern semiconductor fabs. They support advanced memory technologies like MRAM, ReRAM, and 3D XPoint, which require scaling and high-volume production.

Regional Analysis – Global Next Generation Memory Market

Asia-Pacific Dominated the Global Next Generation Memory Market

Asia-Pacific dominated the global Next Generation Memory Market in 2025 and is expected to maintain its leading position throughout the forecast period. The region's dominance is driven by the strong presence of semiconductor manufacturing hubs, increasing investments in memory fabrication facilities, and growing demand for advanced memory technologies across consumer electronics, data centers, automotive, and industrial applications. Countries such as China, South Korea, Japan, and Taiwan are home to leading semiconductor manufacturers and are continuously investing in research and development, advanced chip manufacturing, and next-generation memory technologies. Additionally, government initiatives supporting domestic semiconductor production, rising adoption of artificial intelligence (AI), 5G infrastructure, and high-performance computing are further strengthening the region's market position.

North America Holds a Significant Share of the Next Generation Memory Market

North America accounted for a substantial share of the global Next Generation Memory Market, driven by the presence of leading semiconductor companies, increasing investments in AI infrastructure, and rapid expansion of hyperscale data centers. The United States is witnessing significant demand for advanced memory solutions across cloud computing, enterprise storage, defense, automotive, and consumer electronics sectors. Furthermore, supportive government initiatives to strengthen domestic semiconductor manufacturing, increasing adoption of edge computing, and continuous innovation in non-volatile memory technologies are contributing to regional market growth.

Europe is Expected to Register Strong Growth in the Next Generation Memory Market

Europe is expected to witness strong growth during the forecast period, supported by increasing investments in semiconductor innovation, automotive electronics, and industrial automation. Countries including Germany, France, the Netherlands, and the United Kingdom are focusing on strengthening semiconductor manufacturing capabilities and expanding research in advanced memory technologies. Growing demand for next-generation memory in electric vehicles (EVs), Industry 4.0 applications, aerospace, and telecommunications, along with government-backed semiconductor initiatives, is expected to drive market expansion across the region.

Latin America and the Middle East & Africa are Emerging Markets

Latin America and the Middle East & Africa are expected to experience steady growth in the Next Generation Memory Market during the forecast period. Rising digital transformation, increasing investments in data centers, expanding telecommunications infrastructure, and growing adoption of cloud computing are supporting market growth across these regions. Countries such as Brazil, Mexico, the United Arab Emirates, Saudi Arabia, and South Africa are investing in digital infrastructure and smart technologies, creating new opportunities for advanced memory solutions. Additionally, increasing demand for consumer electronics and enterprise IT infrastructure is expected to contribute to long-term regional market expansion.

Recent Developments – Global Next Generation Memory Market

| Date | Recent Development | Strategic Impact |

| June 2026 | Samsung Electronics Co., Ltd. expanded production of next-generation high-bandwidth memory (HBM) solutions to address increasing demand from AI accelerators and hyperscale data centers. | Strengthened the company's leadership in AI memory solutions and increased manufacturing capacity for advanced memory products. |

| April 2026 | Micron Technology, Inc. introduced advanced HBM products designed to support AI training, high-performance computing, and next-generation server applications. | Enhanced product portfolio and reinforced competitiveness in the rapidly growing AI memory segment. |

| February 2026 | SK hynix Inc. expanded investments in advanced DRAM and HBM manufacturing facilities to support growing demand from AI and cloud computing applications. | Increased production capabilities and strengthened its position in the high-performance memory market. |

| November 2025 | Kioxia Holdings Corporation announced advancements in next-generation 3D flash memory technology with improved storage density and power efficiency for enterprise and data center applications. | Improved storage performance and strengthened the company's competitive advantage in next-generation memory technologies. |

| August 2025 | Everspin Technologies, Inc. expanded its MRAM product portfolio with new industrial and automotive-grade memory solutions targeting edge computing and embedded applications. | Broadened application areas for MRAM technology and strengthened its presence in industrial and automotive memory markets. |

Competitive Landscape – Global Next Generation Memory Market

The global Next Generation Memory Market is highly competitive, with leading semiconductor companies focusing on product innovation, advanced memory architectures, strategic partnerships, capacity expansion, and research and development to strengthen their market positions. Market participants are investing significantly in emerging memory technologies such as Magnetoresistive RAM (MRAM), Resistive RAM (ReRAM), Phase Change Memory (PCM), Ferroelectric RAM (FeRAM), and Compute Express Link (CXL)-enabled memory solutions to address the growing demand from artificial intelligence (AI), high-performance computing (HPC), cloud data centers, automotive electronics, and industrial automation. Companies are also expanding semiconductor fabrication facilities, adopting advanced packaging technologies, and collaborating with technology providers to accelerate commercialization and improve memory performance, endurance, and energy efficiency.

Major industry participants such as Samsung Electronics Co., Ltd., SK hynix Inc., Micron Technology, Inc., Kioxia Holdings Corporation, Western Digital Corporation, Winbond Electronics Corporation, Everspin Technologies, Inc., Infineon Technologies AG, NXP Semiconductors N.V., and Renesas Electronics Corporation are strengthening their competitive positions through continuous investments in advanced memory technologies, AI-enabled memory solutions, strategic acquisitions, and manufacturing capacity expansion. Companies are also focusing on developing high-bandwidth memory (HBM), automotive-grade memory, embedded non-volatile memory, and enterprise storage solutions to meet the evolving requirements of next-generation computing platforms.

Next Generation Memory Market Scope: Inquire before buying

| Next Generation Memory Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 8.43 USD Billion |

| Forecast Period 2026-2032 CAGR: | 16.6% | Market Size in 2032: | 24.7 USD Billion |

| Segments Covered: | By Technology | Non-volatile memory Magneto-Resistive Random-Access Memory (MRAM) Spin-Transfer MRAM (STT-MRAM) Toggle MRAM Ferroelectric RAM (FRAM) Resistive Random-Access Memory (ReRAM) 3D Xpoint Phase-Change Memory (PCM) Nano RAM Other Volatile Memory Hybrid Memory Cube (HMC) High-bandwidth Memory (HBM) Others |

|

| By Wafer Size | 200 mm 300 mm 450 mm |

||

| By Storage Type | Mass Storage Embedded Storage |

||

| By Interface | DDR PCIe / NVMe SATA Others |

||

| By End User | Consumer Electronics Enterprise Storage Automotive and Transportation Military and Aerospace Industrial Telecommunications Energy & Power Healthcare Agricultural Retail Others |

||

Next Generation Memory Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Next Generation Memory Market, Key Players

Major Contributors in the Next-Generation Memory Market in North America:

1. Intel Corporation (California, USA)

2. Micron Technology, Inc. (Idaho, USA)

3. Honeywell International Inc. (North Carolina, USA)

4. IBM Corporation (New York, USA)

5. Crossbar Inc. (California, USA)

6. Cypress Semiconductor Corporation (California, USA)

7. Avalanche Technology, Inc. (California, USA)

8. Adesto Technologies (California, USA)

9. Everspin Technologies Inc. (Arizona, USA)

10. Microchip Technology Inc. (Arizona, USA)

Major Contributors in the Next Generation Memory Market in Asia Pacific:

1. Samsung Electronics Co., Ltd. (Suwon, South Korea)

2. SK Hynix Inc. (Icheon, South Korea)

3. Toshiba Corporation (Tokyo, Japan)

4. Fujitsu Ltd (Tokyo, Japan)

5. Sony Corporation (Tokyo, Japan)

6. Taiwan Semiconductor Manufacturing Company Limited (TSMC) (Hsinchu, Taiwan)

7. Kioxia Holdings Corporation (Tokyo, Japan)

8. Winbond Electronics Corporation (Taichung, Taiwan)

9. Nanya Technology Corporation (Taoyuan, Taiwan)

FAQs:

1. What are the growth drivers for the Next Generation Memory Market?

Ans. The Next Generation Memory Market is driven by the increasing demand for faster and more efficient memory solutions, particularly for AI and Big Data application.

2. What are the major restraints for the Next Generation Memory Market growth?

Ans. The production of next-generation memory technologies involves advanced materials and complex manufacturing processes, leading to significantly higher costs compared to traditional memory solutions. This cost factor can be a barrier to widespread adoption.

3. Which region is expected to lead the global Next Generation Memory Market during the forecast period?

Ans. North America is expected to lead the global Next Generation Memory Market during the forecast period.

4. What is the projected market size and growth rate of the Next Generation Memory Market?

Ans. The Next Generation Memory Market size was valued at USD 8.43 Billion in 2025, and the total Next Generation Memory revenue is expected to grow at a CAGR of 16.6% from 2026 to 2032, reaching nearly USD 24.7 Billion by 2032.

5. What segments are covered in the Next Generation Memory Market report?

Ans. The Next Generation Memory report covers Technology, Wafer Size, Application, and Region.