Knee Replacement Devices Market by Procedure Type, Implant Type, End-User, and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2029

Overview

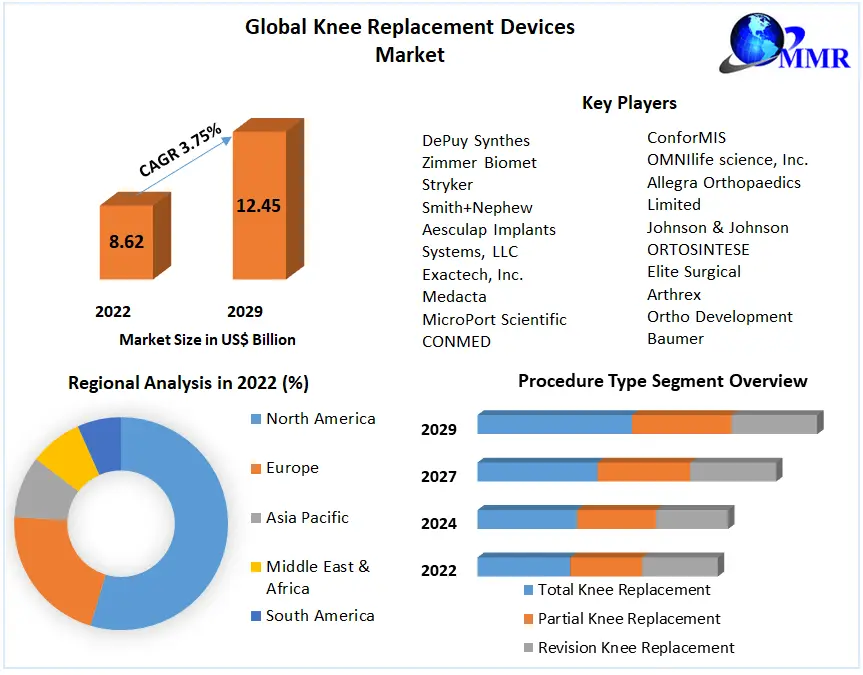

The Knee Replacement Devices Market size was valued at USD 9.62 Billion. in 2022 and the total Knee Replacement Devices revenue is expected to grow at a CAGR of 3.75% from 2023 to 2029, reaching nearly USD 12.45 Billion.

Knee Replacement Devices Market Overview:

Knee arthroplasty or knee replacement surgery involves removing damaged tissues and cartilage from the knee joint and replacing them with artificial knee devices/ implants. Knee joint replacements are often highly helpful in managing osteoarthritis symptoms. An artificial man-made joint, on the other hand, cannot match the performance of a naturally healthy joint. The result of a joint replacement, on the other hand, is typically much better than the patient's pre-operative state with osteoarthritis. Obesity and overweight have been established as major local risk factors for osteoarthritis, particularly in the case of knee osteoarthritis.

The growing global prevalence of osteoarthritis and other joint disorders such as psoriatic arthritis and rheumatoid arthritis is expected to drive the growth of the knee replacement devices market during the forecast period. Globally, more than 200 million women suffer from osteoporosis. In addition, the Arthritis Foundation stated that 16 million people in the United States had symptomatic knee osteoarthritis in 2020.

However, according to the European Journal of Rheumatology, 200 million individuals in the United States and Europe suffered from osteoporosis illness in 2020, with 30% of them being women. As a result, an increase in the number of individuals with osteoporosis disorders has resulted in an increase in demand for knee replacement surgery, eventually requiring knee replacement devices and which drives the knee replacement device market growth significantly during the forecast period.

In addition, the rapid growth in the prevalence rate of post-traumatic arthritis and the growing adoption of minimally invasive surgical procedures are expected to drive the growth of the knee replacement devices market during the forecast period. According to the Agency for Healthcare Research and Quality (AHRQ), more than 600,000 knee replacement procedures are performed in the United States each year.

Meanwhile, Zimmer Biomet, a global medical technology provider, and Canary Medical, a medical data firm, won FDA approval for Persona IQ, the world's first smart knee replacement device for complete knee replacement surgery, in August 2022. The major competitors' perspectives on unmet requirements for the effective treatment of severe knee osteoarthritis through a patient-centric development strategy are expected to increase the market growth.

However, a high focus of market participants in developing new implants/ devices is expected to increase the revenue growth of the market during the forecast period. For instance, Conformis Inc. one of the major competitors in the market, gained FDA certification for their Identity Imprint knee replacement system in May 2022. This device is available in both cruciate-retaining and posterior stabilized variants, giving orthopedic surgeons and patients more alternatives. Identity Imprint is tailored to each patient's specific size, shape, and curvature. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Knee Replacement Devices Market Dynamics:

High prevalence rate of knee osteoarthritis

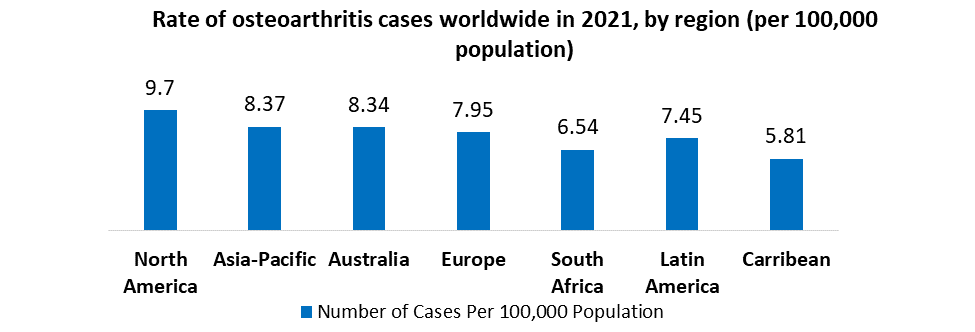

A high prevalence rate of knee osteoarthritis all across the world is expected to be one of the major factors increase the demand for bone surgeries in coming years. The rise in the adult population's diagnostic rate of knee arthritis is expected to increase demand for knee replacement devices/ implants during the forecast period. According to the Osteoarthritis Research Society International (OARSI), it has been stated that the prevalence rate of global knee osteoarthritis is expected to reach 5% and is expected to increase with the increase in the aging population by 2030. According to the Arthritis Foundation, the prevalence rate of knee osteoarthritis in the United States annually is highest between the age group 55 and 64 years old.

The rapid increase in the aging population and the increasing epidemics of overweight at a significant rate are expected to drive the demand for knee replacement surgeries during the forecast period. As a result, the rising knee replacement surgeries are expected to increase the demand for knee implants/ devices and benefit the knee replacement devices market growth.

Growing technological developments to improve treatment efficacy

Growing technological developments to improve treatment efficacy

Increasing awareness of technological developments, chemical and material innovations, and designs of knee implants, as well as robot-assisted knee operations, is currently an important trend influencing sales of the products/ devices utilized in replacement procedures. Robot-assisted technology is increasing procedure accuracy and decreasing reliance on surgeons for operative results. In addition, with the incorporation of robotic surgery into their portfolio, some significant manufacturers in the industry are delivering more complete knee implants.

Smith & Nephew, for example, bought Blue Belt Holdings, Inc. in 2016 to gain access to the Navio Surgical System, which provides robot help in partial knee operations using CT- a free navigation system and a portable robotic bone shaping device. Increased demand for customized knee implants, as well as the entry of new competitors offering novel knee implants with innovations, are expected to drive knee replacement devices market growth during the forecast period.

Stringent governmental regulations

Concerns with artificial knee replacement devices/ implants, such as adverse effects associated with metallic implants, post-surgery infectious diseases, implant displacements, hypersensitivity, wear debris, and toxicity issues, are leading to increased product recalls. As a result, regulatory organizations are implementing severe product approval procedures to ensure patient safety, pushing back product clearance timelines. As a result, the current stringent regulatory framework is expected to be a major restraint to the knee replacement devices/implants market growth over the forecast period.

High cost of knee replacement implant surgeries

Knee replacement surgery costs between USD 4500 to USD 8000 for one knee, with computer-aided treatments costing an additional 5-10%. Despite a CAGR of 16% in insurance coverage, less than 300 million individuals are now covered by health insurance through one of several sources: government-provided coverage, corporate group coverage, and private retail plans. The segment's potential as a significant out-of-pocket market is restricted by affordability limits for expensive orthopedic implant operations. The reduced frequency of hip replacements throughout the world is frequently linked to the affordability issue and the resulting proclivity to postpone or avoid the treatment. As a result, the high cost of surgeries is expected to restrain the trauma implants market growth.

Knee Replacement Devices Market Segment Analysis:

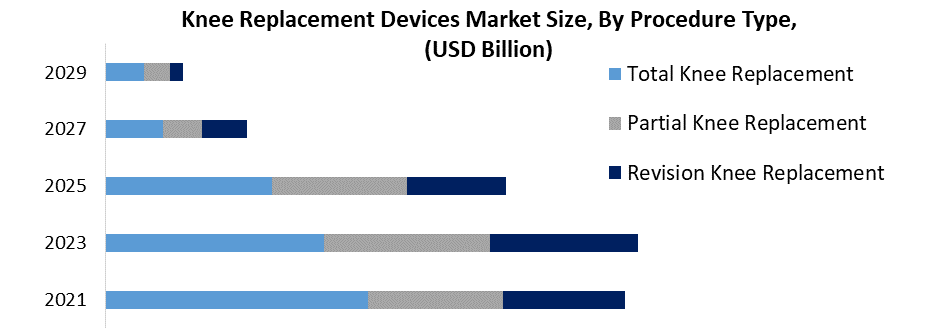

Based on Procedure Type, the total knee arthroplasty segment held the market share of 62% and dominated the knee replacement devices market in 2022. The segment is expected to grow at a CAGR of 3.68% during the forecast period. The ultimate therapy for symptomatic end-stage osteoarthritis of the knee is surgical replacement of the knee joint, commonly known as total knee arthroplasty (TKA) and total knee replacement. Of the 11 million adults in the United States who have been estimated to have this diagnosis, 4 million have undergone a knee replacement. A total of 700,000 main TKA treatments are expected to be done in 2018, representing an 86% increase over 2015.

Factors associated with the increased use and prevalence of knee replacements include developing lifestyles, aging population, and increasing longevity of the population; obesity; growing indications for the procedure; and younger age at implantation. Direct-to-consumer advertising may also have a role in raising demand. Although the entire cost of a TKA is comparable to that of a new car, several studies have shown that TKA is quite cost-effective. Imaging patients with knee replacements are now standard practice.

The revision arthroplasty segment is expected to be the fastest-growing segment during the forecast period. The increasing number of revision knee surgeries in total knee replacement procedures, technical advances in revision implants, and a change in knee surgery procedures among younger patients are expected to be major growth drivers for the segment.

The revision arthroplasty segment is expected to be the fastest-growing segment during the forecast period. The increasing number of revision knee surgeries in total knee replacement procedures, technical advances in revision implants, and a change in knee surgery procedures among younger patients are expected to be major growth drivers for the segment.

Because of the presence of major market participants involved in the development of revolutionary partial knee implants, the partial knee arthroplasty segment is expected to grow at a modest CAGR during the forecast period. Additionally, partial knee arthroplasty surgery entails replacing only the injured knee bone, which has increased patient demand for customized implants. This is expected to increase the preference for partial knee arthroplasty among healthcare professionals during the forecast period.

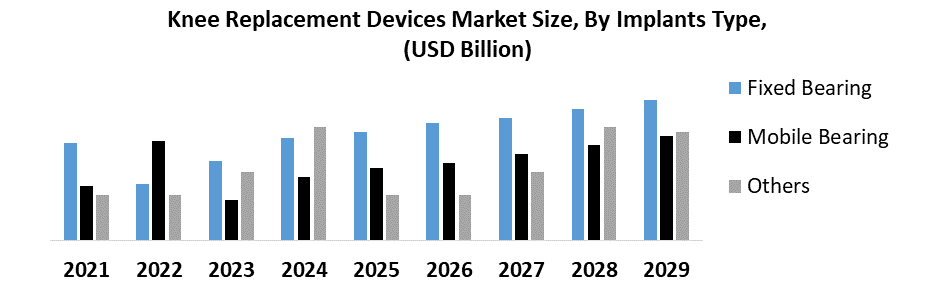

Based on Implants Types, the Fixed Bearing segment dominated the knee replacement devices market with the highest revenue share in 2022 and is expected to grow at the highest CAGR and maintain its dominance at the end of the forecast period. Fixed-bearing implants are a common type of implant because they are long-lasting and give excellent mobility. Polyethylene inserts are secured into a tibial tray in fixed-bearing implants. Although fixed-bearing knee prostheses have been clinically effective, there have been long-term failures because of loosening or polyethylene wear.

Low contact stress is provided by a fixed-bearing prosthesis with a high conformance surface (so-called round-on-round), but excessive torque at the bone-implant interface may induce loosening. A low-conformity surface (round-on-flat) generates less torque at the bone-implant interface, but high contact stress may result in polyethylene failure.

The Mobile Bearing segment is expected to grow at a significant CAGR during the forecast period. This component's qualities, such as superior wear characteristics and stability, are expected to increase product demand throughout the forecast period. Mobile-bearing knee prostheses were developed to reduce polyethylene wear and component loosening. Implant-bone interface stress and contact stress might be minimized concurrently by generating a dual-surface articulation and a high-conformity surface.

The Mobile Bearing segment is expected to grow at a significant CAGR during the forecast period. This component's qualities, such as superior wear characteristics and stability, are expected to increase product demand throughout the forecast period. Mobile-bearing knee prostheses were developed to reduce polyethylene wear and component loosening. Implant-bone interface stress and contact stress might be minimized concurrently by generating a dual-surface articulation and a high-conformity surface.

Although mobile-bearing designs have theoretical benefits over fixed-bearing designs, comparative studies found no difference in function, patient preference, or prosthesis-related problems. Mobile-bearing prostheses appear to offer no kinematic benefits over fixed-bearing prostheses, and they are also prone to bearing dislocation and fracture, soft-tissue impingement, problematic implantation, and volumetric degradation. For unicompartmental arthroplasty, mobile bearings are also available.

Knee Replacement Devices Market Regional Insights:

North American knee replacement devices market held the largest market share in terms of value and volume and dominated the market in 2022. The region is further expected to grow at a CAGR of 3.74% and maintain its dominance at the end of the forecast period. The primary factors expected to drive market growth in the North American region are an increase in the number of individuals diagnosed with osteoarthritis and an increase in the geriatric population. Additionally, the rising adoption of computer-aided implant designs, robot-assisted surgeries in North American countries, and advantageous reimbursement circumstances are expected to drive the knee replacement devices market during the forecast period.

North American knee replacement devices market held the largest market share in terms of value and volume and dominated the market in 2022. The region is further expected to grow at a CAGR of 3.74% and maintain its dominance at the end of the forecast period. The primary factors expected to drive market growth in the North American region are an increase in the number of individuals diagnosed with osteoarthritis and an increase in the geriatric population. Additionally, the rising adoption of computer-aided implant designs, robot-assisted surgeries in North American countries, and advantageous reimbursement circumstances are expected to drive the knee replacement devices market during the forecast period.

In addition, an increase in the number of product approvals by the U.S. FDA is expected to increase knee replacement devices market revenue during the forecast period. Likewise, an increase in the number of research initiatives aimed at developing cost-effective and unique implants in developed North American countries supported the market growth. In 2022, the United States owned the greatest market share of the North American knee replacement market. The increasing geriatric population, as well as the increased prevalence of arthritis and other joint abnormalities, are expected to drive market growth in the United States. Additionally, the availability of well-established healthcare infrastructure and access to technologically improved implant operations are expected to drive market growth during the forecast period.

Asia-Pacific region is expected to grow at a CAGR of 3.21% during the forecast period, offerings lucrative potentials for the key players operating in the knee replacement devices market. The rapidly rising geriatric population, increased awareness of orthopedic implants, increased demand for improved implants, growth of healthcare infrastructure, and increased need for minimally invasive treatments all contribute to the region's growth. Besides that, advancements in bone scan diagnostic tools for determining bone density among clinical laboratories, improved reimbursements by private and public institutions, and the improvement of healthcare infrastructure are all contributing to an increase in the number of patients receiving orthopedic treatments. This, together with favorable government regulations to encourage orthopedic procedures, is expected to increase the growth of the Asia-pacific knee replacement devices market.

The European region is expected to grow at a modest rate throughout the forecast period, due to a rise in the prevalence of chronic conditions such as diabetes and bone disease. Innovations in implant material and design, the existence of prominent competitors with a robust distribution network, and rising demand for knee replacement surgeries are expected to further drive the EU5 knee replacement devices market by 2029. Latin America and the Middle East and Africa are expected to experience slow market growth due to a lack of orthopedic surgeons and poor income growth. However, a rising number of orthopedic injuries and disorders, as well as an increase in the acceptance of replacement procedures, are expected to drive the growth of the knee replacement market in Latin America, the Middle East, and Africa.

The European region is expected to grow at a modest rate throughout the forecast period, due to a rise in the prevalence of chronic conditions such as diabetes and bone disease. Innovations in implant material and design, the existence of prominent competitors with a robust distribution network, and rising demand for knee replacement surgeries are expected to further drive the EU5 knee replacement devices market by 2029. Latin America and the Middle East and Africa are expected to experience slow market growth due to a lack of orthopedic surgeons and poor income growth. However, a rising number of orthopedic injuries and disorders, as well as an increase in the acceptance of replacement procedures, are expected to drive the growth of the knee replacement market in Latin America, the Middle East, and Africa.

Knee Replacement Devices Market Scope: Inquiry Before Buying

| Knee Replacement Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2017 to 2022 | Market Size in 2022: | US $ 9.62 Billion. |

| Forecast Period 2023 to 2029 CAGR: | 3.75% | Market Size in 2029: | US $ 12.45 Billion. |

| Segments Covered: | by Procedure Type | 1. Total Knee Replacement 2. Partial Knee Replacement 3. Revision Knee Replacement |

|

| by Implant Type | 1. Fixed Bearing 2.Mobile Bearing 3. Others |

||

| by End-User | 1. Hospitals 2. Orthopedic Clinics 3. Ambulatory Surgery Centers |

||

Knee Replacement Devices Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Knee Replacement Devices Market, Key players are

1. DePuy Synthes

2. Zimmer Biomet

3. Stryker

4. Smith+Nephew

5. Aesculap Implants Systems, LLC

6. Exactech, Inc.

7. Medacta

8. MicroPort Scientific

9. CONMED

10. Kinamed, Inc.

11. ConforMIS

12. OMNIlife science, Inc.

13. Allegra Orthopaedics Limited

14. Johnson & Johnson

15. ORTOSINTESE

16. Elite Surgical

17. Arthrex

18. Ortho Development

19. Baumer

20. PETER BREHM

FAQs:

1. What are the growth drivers for the Knee Replacement Devices market?

Ans. The growing global prevalence of osteoarthritis and other joint disorders such as psoriatic arthritis and rheumatoid arthritis, an increase in the number of individuals with osteoporosis disorders, the rapid growth in the prevalence rate of post-traumatic arthritis and the growing adoption of minimally invasive surgical procedures, is expected to be the major driver for the Knee Replacement Devices market.

2. What is the major restraint for the Knee Replacement Devices market growth?

Ans. The Stringent Regulations on Knee Replacement Devices adoption, High cost of knee replacement implant surgeries are expected to be the major restraining factor for the Knee Replacement Devices market growth.

3. Which region is expected to lead the global Knee Replacement Devices market during the forecast period?

Ans. The North American market is expected to lead the global Knee Replacement Devices market during the forecast period due to an increase in the number of individuals diagnosed with osteoarthritis and an increase in the geriatric population.

4. What is the projected market size & growth rate of the Knee Replacement Devices Market?

Ans. The Knee Replacement Devices Market size was valued at USD 9.62 Billion. in 2022 and the total Knee Replacement Devices revenue is expected to grow at a CAGR of 3.75% from 2023 to 2029, reaching nearly USD 12.45 Billion.

5. What segments are covered in the Knee Replacement Devices Market report?

Ans. The segments covered in the Knee Replacement Devices market report are Procedure Type, Implant Type, End User, and Region.