Jewelry Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

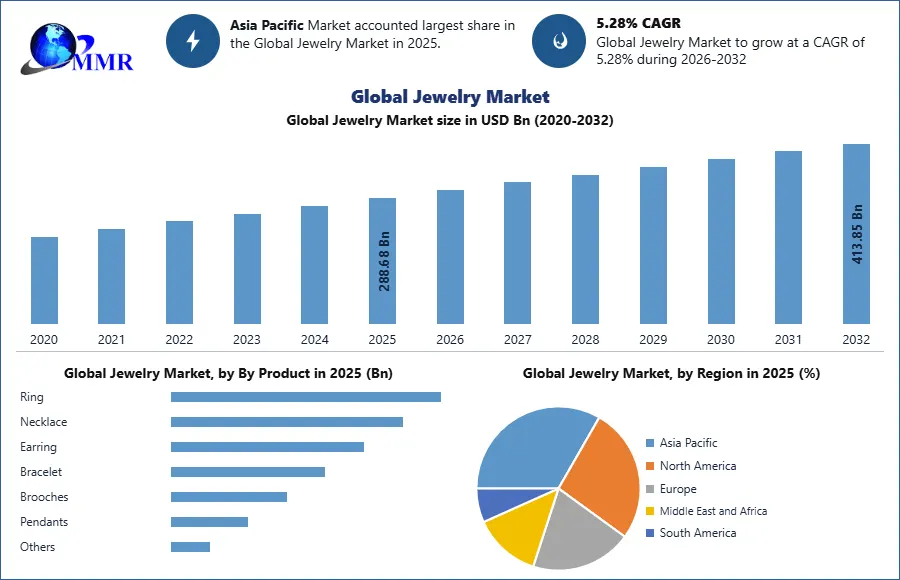

The Jewelry Market size was valued at USD 288.68 Billion in 2025 and the total Jewelry revenue is expected to grow at a CAGR of 5.28% from 2026 to 2032, reaching nearly USD 413.85 Billion by 2032.

Jewelry Market Overview

The global jewelry market is gleaming with creativity, sustainability, and individuality, marking a new era of conscious luxury. The jewelry industry is evolving through a seamless fusion of fine jewelry, fashion jewelry, and luxury jewelry, as designers adapt to rapidly shifting consumer values and aesthetics. The shoppers seek deeper meaning behind their adornments, preferring ethical jewelry and sustainable jewelry brands that emphasize responsible sourcing, recycled metals, and lab-grown diamonds. This alignment of sustainability with sophistication reflects a new definition of modern elegance—one that celebrates both artistry and accountability.

Style trends have grown bolder and more experimental. Oversized sculptural earrings, layered necklaces, chunky gold chains, and vivid gemstone accents dominate contemporary collections, signaling a move from minimalist to statement-driven designs. The gold, diamond, and silver jewelry trends showcase a blend of mixed metals, baroque pearls, and asymmetrical forms, merging traditional craftsmanship with avant-garde creativity. At the same time, the rising appeal of custom-made and handcrafted jewelry market reflects consumers’ desire for personalization, where every piece tells a unique story .

The surge of digital jewelry retail platforms has revolutionized how consumers discover and purchase jewelry. Online jewelry stores now offer affordable luxury jewelry through immersive shopping experiences, including AR try-ons and AI customization tools, bridging the gap between accessibility and exclusivity. Additionally, the growing popularity of bespoke engagement jewelry and sustainable wedding collections. As technology, sustainability, and design innovation converge, stands as a milestone year for a jewelry market ethical brilliance, artistic experimentation, and emotional connection.

To know about the Research Methodology:-Request Free Sample Report

Jewelry Market Dynamics:

Evolving Fashion Trends, Celebrity Influence, and Technological Innovations Driving the Growth of the Global Jewelry Market Through Personalization, Digital Commerce, and Luxury Demand

The Jewelry Market is witnessing strong growth driven by evolving fashion trends and increasing consumer demand for personalized and luxury products. Nearly 65% of jewelry buyers globally make purchase decisions based on current fashion trends, highlighting how closely jewelry aligns with style preferences. Designers and brands continually adapt their collections to suit evolving aesthetics — from minimalist designs preferred by 40% of urban consumers to bold statement jewelry gaining traction among millennials and Gen Z shoppers. Celebrity influence remains significant; more than 70% of consumers report being inspired by red-carpet events and celebrity endorsements when purchasing jewelry. Collaborations between designers and high-profile personalities have become a proven strategy to capture attention and strengthen brand loyalty.

Periods of economic prosperity significantly boost jewelry consumption. Surveys suggest that jewelry sales rise by 20–25% during times of higher disposable income and consumer confidence. Weddings and engagements remain the strongest purchasing occasions, accounting for nearly 50% of fine jewelry sales worldwide. Luxury jewelry brands experience notable spikes in demand during such periods, as consumers seek premium and exclusive designs.

Additionally, the convenience of digital commerce has changed consumer behavior more than 35% of jewelry purchases are now made online. Improved logistics, secure payments, and easy customization options have helped e-commerce reshape jewelry retail, especially among younger consumers who value accessibility and choice.

Technology is reshaping the jewelry manufacturing process. The use of Computer-Aided Design (CAD) and 3D printing has increased production efficiency by 30–40%, enabling intricate and customized jewelry creations that were previously difficult to achieve manually. These innovations allow brands to introduce new designs faster, meeting market demand for uniqueness and personalization. Around 45% of jewelers globally now use digital modeling or additive manufacturing to enhance precision and reduce production lead times. As consumers increasingly prefer bespoke jewelry, technology continues to be a critical growth enabler for both traditional and contemporary jewelers market.

Sustainability, Ethical Sourcing, and Technological Innovation Redefining the Global Jewelry Industry Amid Rising Consumer Awareness, Counterfeit Challenges, and Digital Transformation

Despite promising growth, the jewelry industry faces key challenges linked to shifting consumer expectations. Over 55% of consumers now prioritize sustainability and ethical sourcing in their jewelry purchases. Demand for conflict-free diamonds, fair-trade metals, and eco-friendly production has prompted major brands to overhaul their supply chains and improve transparency. However, these transitions are complex and costly. Counterfeit jewelry remains concern, with fake products accounting for an estimated 8–10% of global jewelry sales. The shortage of skilled artisans, particularly in handcraft-based jewelry, adds further strain labor costs in skilled jewelry manufacturing have risen by 15–20% in the past five years.

Sustainability and ethical sourcing are gaining strong momentum, with lab-grown diamonds now accounting for nearly 10% of global diamond sales a figure expected to rise steadily. Cultural and symbolic jewelry has also become increasingly popular, with over 30% of buyers seeking designs that hold personal or spiritual meaning. Technology integration is another defining trend, as smart jewelry such as fitness-tracking rings and connected pendants continues to attract tech-savvy consumers. The digital shopping innovation is transforming how jewelry is purchased: augmented reality (AR) and virtual try-on tools have improved online conversion rates by up to 25%, giving consumers confidence in their purchases and reducing returns.

| Jewelry Market Trend | Key Insights & Figures |

| Personalized & Custom Jewelry | Demand for customized jewelry up by 40% in 3 years; 45% of jewelers use CAD/3D printing. |

| Celebrity & Influencer Impact | 70% of buyers influenced by celebrity endorsements and red-carpet appearances. |

| Minimalist & Modern Designs | 40% of urban consumers prefer minimalist jewelry; demand for simplicity and elegance rising. |

| Cultural & Symbolic Jewelry | 30%+ of global buyers seek jewelry with spiritual or cultural symbolism. |

| Smart & Tech-Integrated Jewelry | Smart jewelry market growing at 20–25% annually; includes fitness rings and connected pendants. |

| Luxury & High-End Jewelry | Premium jewelry demand rises 20–25% during economic upturns; 50% of sales from weddings and engagements. |

| Counterfeit & Imitation Concerns | Fake jewelry represents 8–10% of global sales, affecting brand trust and quality perception. |

| Skilled Labor & Artisan Shortage | Labor costs in handcrafted jewelry rose 15–20% over 5 years due to artisan scarcity. |

Jewelry Market Segment Analysis:

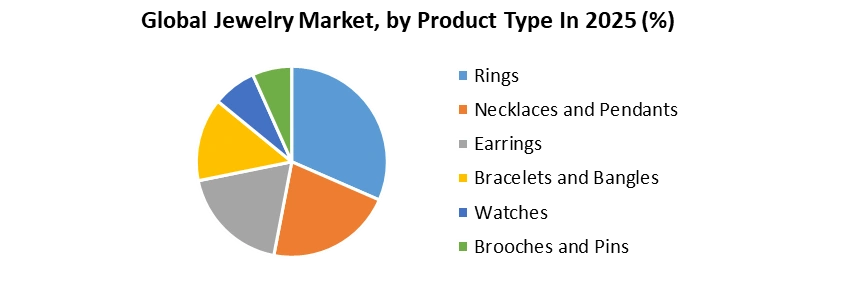

Based on Product Type, the Jewelry Market is segmented into Rings, Necklaces and Pendants, Earrings, Bracelets and Bangles, Watches, and Brooches and Pins. The Rings segment dominated the market in 2025 and is projected to maintain its lead through the forecast period. Globally, it is estimated that more than 70% of engagement proposals include a ring purchase, with over 60 million rings sold annually across various categories. Engagement rings and wedding bands continue to be timeless symbols of love and commitment, contributing heavily to revenue streams for jewelers. Moreover, bridal jewelry accounts for nearly half of total ring sales in many emerging markets. Alongside traditional purchases, fashion and statement rings have become popular among Gen Z and Millennials, who increasingly purchase jewelry for self-expression rather than ceremonial purposes. The rise of gender-neutral jewelry collections has also diversified product lines and expanded the consumer base. Other key categories Necklaces, Pendants, Earrings, and Bracelets remain strong, driven by festive, luxury, and casual wear demand. For instance, earrings and bracelets together make up about 35% of global jewelry transactions, reflecting their versatility and gifting appeal. The continued evolution of materials, designs, and personalization such as engraved pieces or mix-metal combinations—further fuels jewelry market growth.

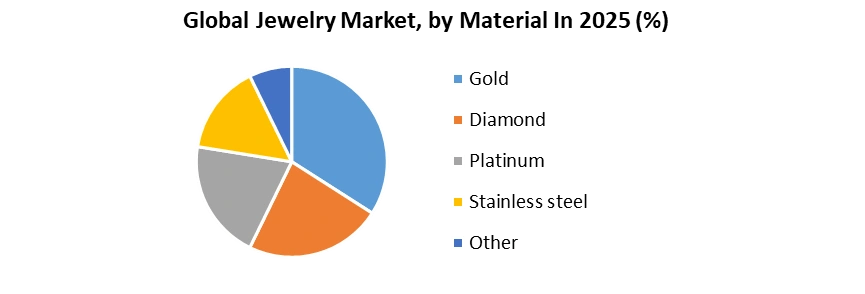

Based on Material, the jewelry market is divided into Gold, Diamond, Platinum, Stainless Steel, and Others. The Gold and Diamond segments accounted for the largest share in 2025 and will continue to dominate. On average 48% of all jewelry produced globally contains gold, reflecting its deep cultural and emotional value. In India alone, over 400 tons of gold jewelry are purchased annually, much of it linked to weddings and festivals. Diamond jewelry remains the centerpiece of luxury, with an estimated 80% of diamond jewelry sales associated with engagement and anniversary gifts. The demand for lab-grown diamonds has increased by over 25% annually since 2022, appealing to sustainability-conscious consumers. Their lower cost typically 40% less than natural diamonds has widened accessibility. Platinum jewelry, prized for its durability, is gaining traction among young urban buyers, particularly in Japan and South Korea, where one in five engagement rings now features platinum. The growth of stainless steel and titanium jewelry; it appeals to younger buyers due to affordability and hypoallergenic properties, representing 15–18% of total fashion jewelry sales globally.

Jewelry Market Regional Insight

The Asia-Pacific Jewelry Market remains the most vibrant and diverse globally, driven by rich traditions, rising income levels, and digital transformation. The region accounts for nearly 60% of global jewelry demand, led by India, China, Thailand, and Indonesia. India’s jewelry exports surpassed USD 35 billion in 2025, supported by its strong gold and diamond processing industry. China, on the other hand, is the largest producer of synthetic gemstones, manufacturing over 10 billion carats annually, catering to both domestic and export markets. Thailand has emerged as a global hub for gemstone cutting, employing over 800,000 skilled workers in jewelry and accessory production.

Rapid digitization is reshaping jewelry retail in Asia-Pacific. More than 40% of jewelry sales in China now occur online, aided by secure payment systems, virtual try-on apps, and social commerce platforms like WeChat and TikTok. Digital customization tools allow users to personalize metal type, gemstone selection, and engraving options making luxury jewelry accessible to a wider audience. The expansion of global brands such as Tiffany & Co., Cartier, and Bulgari in Asia has intensified competition, with these companies opening over 200 new retail stores across the region between 2022 and 2025. The integration of traditional craftsmanship with AI-driven design, ethical sourcing, and 3D printing has further modernized the industry.

Sustainability and transparency are becoming major trends. Around 30% of millennial consumers in Asia prefer brands that use recycled metals and conflict-free gemstones. Additionally, digital traceability solutions—such as blockchain-based certification—are being adopted by major jewelers to ensure authenticity. With a growing middle-class population, increasing luxury spending, and digital innovation, the Asia-Pacific jewelry market is poised to remain a global leader. Its blend of heritage, modernity, and technological adoption continues to shape the evolution of the global jewelry industry.

Jewelry Market Competitive Landscape

The competitive landscape of the jewelry market is highly dynamic, featuring a blend of luxury jewelry houses, fast-fashion brands, local artisans, and innovative startups competing for consumer attention. Iconic brands like Cartier, Tiffany & Co., Bulgari, and Van Cleef & Arpels dominate the premium segment with exquisite craftsmanship, heritage designs, and celebrity endorsements, appealing to affluent buyers seeking exclusivity. In contrast, fast-fashion brands such as Swarovski, Pandora, and H&M Accessories offer trendy, affordable pieces and update collections every 4–6 weeks to align with shifting fashion trends. Meanwhile, over 2 million artisans in India and 1 million across Southeast Asia sustain the artisanal jewelry segment, emphasizing handcrafted, culturally rich designs. Technological innovation is reshaping the global jewelry industry, with startups like Mejuri and Blue Nile leveraging direct-to-consumer models, AI-driven customization, and virtual try-ons to modernize jewelry retail. Additionally, the rise of sustainable jewelry brands such as Brilliant Earth and Chopard reflects growing consumer demand for ethical sourcing, recycled metals, and transparent supply chains. Many companies now align with social impact initiatives, donating portions of revenue to causes like education and women’s empowerment. This fusion of luxury tradition, digital innovation, and sustainability defines the evolving global jewelry market and its competitive future.

Recent Development

In January 2025, Tiffany & Co. introduced its groundbreaking “Titan Setting” diamond design, featuring an 89-facet stone mounted without prongs, marking a leap in high-end craftsmanship and technology integration. This innovation showcases Tiffany’s ongoing effort to appeal to luxury jewelry consumers seeking exclusivity and modern elegance. The launch strengthened its leadership in the global fine jewelry market, blending artistry with precision engineering.

In July 2025, Pandora achieved a major sustainability milestone by transitioning to 100% recycled gold and silver in its jewelry production. Its Thai facility now operates entirely on renewable energy, eliminating over 58,000 tons of CO₂ emissions annually. This move cements Pandora’s role as a pioneer in sustainable jewelry manufacturing, appealing to environmentally conscious consumers.

In March 2025, Indian D2C jewelry brand GIVA secured ₹102 crore (US$12 million) in funding to expand its presence in the silver jewelry segment. The investment supports retail growth, new product lines, and stronger online channels, reflecting the booming affordable luxury jewelry market in Asia.

Jewelry Market Scope: Inquire before buying

| Global Jewelry Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 288.68 USD Bn |

| Forecast Period 2026-2032 CAGR: | 5.28% | Market Size in 2032: | 413.85 USD Bn |

| Segments Covered: | By Product | Ring Necklace Earring Bracelet Brooches Pendants Others |

|

| By Material | Platinum Gold Diamond Others |

||

| By Category | Fine Jewelry Costume Jewelry |

||

| by Customer Age Group | Below 18 18-24 25-34 35-44 45-54 55+ |

||

| By Price Range | Luxury Segment Affordable Luxury Economy Range |

||

| By End-user | Men Women Children |

||

| By Distribution Channel | Offline Department Stores & Multi-brand Outlets Jewelry Stores Online Brand Website Social Media Third-Party Marketplace |

||

Jewelry Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Jewelry Market, Key players

- Cartier International SNC

- Tiffany and Co.

- Bvlgari

- Van Cleef and Arpels

- Harry Winston

- Piaget

- Graff

- Mikimoto

- H. Stern

- Louis Vuitton Malletier SAS

- Signet Jewelers

- Swarovski AG

- Pandora

- Chow Tai Fook Jewellery Group

- Luk Fook Jewellery

- Senco Gold and Diamonds

- Tribhovandas Bhimji Zaveri (TBZ)

- Pure Gold Jewellers

- Lazurde

- Emperor Jewellery

- KGK Group

- Rajesh Exports

- Reliance Jewels

- Derewala Industries

- DWS Jewellery

- Alexis Bittar

- Ben Bridge Jeweler Inc.

- Malabar Gold and Diamonds

- Blue Nile Inc.

- Boucheron

- Brilliant Earth

- Buccellati

- Charles and Colvard Ltd.

- Chopard

- Damiani

- David Yurman

- De Beers Group

- Fame Diamonds