Space Tourism Investment Promises Extraordinary Returns Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2029

Overview

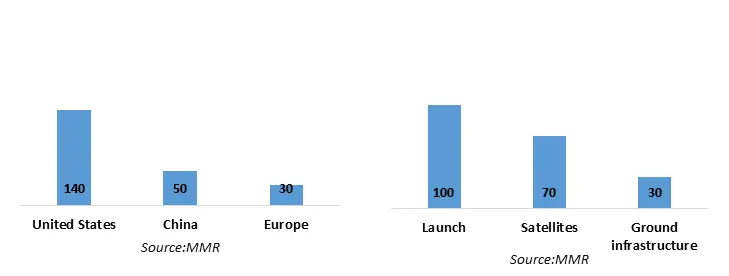

The total equity space tourism investment over the last years in the space economy was $177.7 billion, according to Space Capital. It was spread throughout 1,343 different space companies, with 75% of that to al coming from American and Chinese organizations. Singapore (6%), Britain (4%), Indonesia (3%) and India (3%), in that order, were the next in line. A record $8.9 billion was invested overall in infrastructure (launch, satellites, logistics, etc.) in 2020. The space economy isn't just rockets, spaceships and tourism. The companies involved in applications, like positioning, navigation and earth observation, account for the major share of funds each year to drive the space industry.

The Global Space Economy (USD Trillion)

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The amount of investment activity in the space industry has grown significantly in recent years. Total yearly investment increased from $300 million to more than $10 billion between 2018 and 2021. Investment fell behind 2021 during the first half of 2022 but remained above average historically, indicating that the space sector may be durable despite the difficulties of the present market environment. Space companies have used five main strategies to access capital in recent years private-venture funds, spin-offs, partnerships, special-purpose acquisition companies (SPACs), and internal investment and R&D.

Space infrastructure provides increasing investment opportunities

The growing interest among investors in the commercialisation and eventual industrialisation of space is according to grow in the number of investment opportunities in the space technology industry. Currently, there are thousands of companies involved in the New Space economy and many are emerging as possible investments with a variety of business models and space projects. Not all are going to succeed, and investors need to be careful in picking their vehicles.

Furthermore, because of the hostile environment in space, operational risks must be considered. In addition to posing a threat to the collaborative environment, Russia's conflict in Ukraine also poses a clear and present danger to the mission integrity of orbiting platforms, including those that have not yet been launched, due to the rise in space debris in low-Earth orbit (LEO) as a result of its ASAT (anti-satellite) missile test last year. Governments all around the globe are clearly interested in using more affordable access to space to create their own space programs, which aids economic growth. For example, the 2021 National Space Strategy of the UK government demonstrates a wide commitment to innovation in the space industry and creates a favourable climate for investment and continued growth within the sector.

The first satellite launch into orbit from Cornwall's new spaceport is expected to take place later this year. The UK space industry, under the direction of the UK Space Agency, aims to have 10% of the worldwide market by 2030. Over £16 billion and 45,000 people are employed in the UK's space industry. The New Space-time span makes use of more compact, less expensive, 500 kg or less tiny satellites that may be launched in networks to offer worldwide coverage. Micro-satellites under 100 hg and nano-satellites under 10 kg are also covered. As operational life teams are roughly five years, lead times may be as low as one year, and payload technology can spirally advance more often. In addition, one rocket may carry up to 120 units at once due to its size to increase efficiency.

Internal investment and R&D Have Made Breakthrough Innovations in Space Industry

The next generation of space capabilities can be funded internally by larger, more established space companies with significant capital on their bank sheets. For example, Northrop Grumman has a fully-owned subsidiary named Space Logistics to offer geosynchronous satellite operators cooperative space logistics and in-orbit satellite servicing. Raytheon Technologies invested in new manufacturing facilities that debuted in August 2022 to increase its internal capacity for producing commercial and defence satellites after purchasing satellite producer Blue Canyon Technologies in 2021.

Consumer Communication and Satellite Services Drive Space Market Expansion

The communication sector and the research and commercial sectors might be considered to be the two main potential markets in the space business. Currently making up around 25% of the industry, communication consumer television primarily is expected to grow as internet infrastructure and more satellite services become available over the coming two decades. Additionally, there is a significant non-commercial player market for satellites, which includes military and academic researchers.

In an effort to strengthen the space economy and accelerate the growth of space exploration, there have been more efforts to promote private sector participation in space missions. The recently established Space Law of the UAE intends to promote investment and encourage private sector participation in space sector activities.

How Private-venture funds help space industry

Venture capital (VC) investments in the space industry have grown significantly over the last few years as investors have come to grow the long-term commercial potential of the industry. The many active VC investors in the space sector include Andreessen Horowitz, Founders Fund, and Lux Capital. Much of the capital has surged to early-stage space companies, allowing space start-ups with less mature products or a longer path to profitability to fund the R&D of capital-intensive products while working to capture early customer revenue.

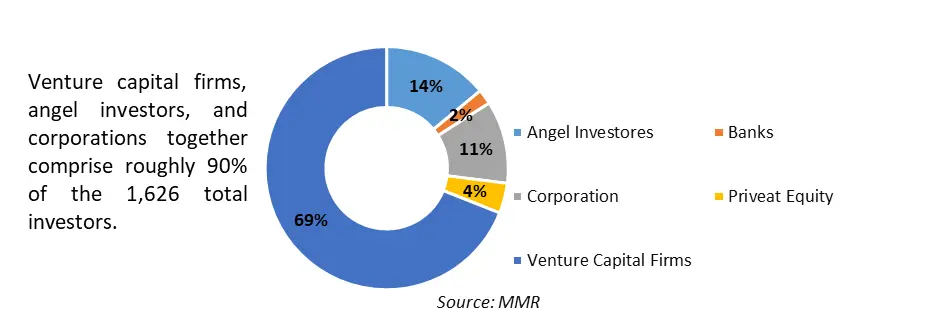

Investors Invested In 212 Start-up Space Companies In 2021

In April 2021, Astranis Space Technologies received a $250 million series C round of funding for smaller, less costly geostationary communication satellites. In a fundraising round, Relativity Space raised $650 million to scale up manufacturing of their fully reusable, wholly 3-D printed Terran R rocket in June 2021. In order to develop manufacturing for inexpensive satellite launch vehicles, ABL Space Systems received $200 million at a $2.4 billion value in October 2021. For the construction of the Starlink broadband, satellite-based internet infrastructure as well as the Starship rocket, SpaceX raised $1.5 billion in May 2022 at a $125 billion value.

Space Companies like SpaceX, Blue Origin, and Relativity Space, as well as others, are making investments in the creation and commercialization of novel technologies including reusable launch vehicles. For instance, SpaceX collected roughly $2 billion in the US in 2022 and has a bold plan for 2023 that includes 87 rocket launches, a prolonged lunar exploration effort, and an expansion of the Starlink internet service. These private businesses are also diversifying into new markets, such as satellite-based services.

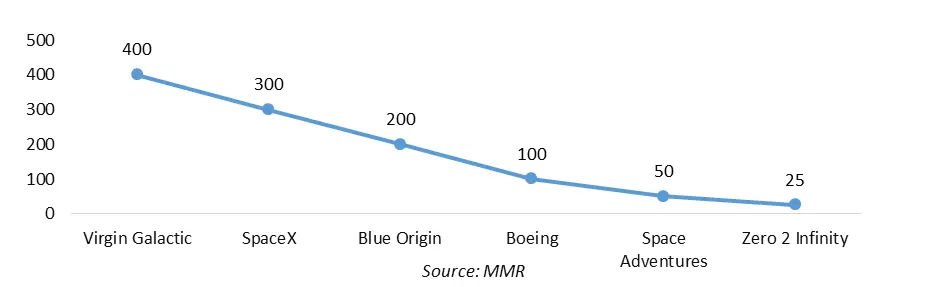

The investment in space tourism by leading space companies in 2022 (USD Million)

In the coming ten years, as the space industry grows, private enterprises will probably play a bigger part in it. According to 98% of senior executives surveyed, new developments like in-space manufacturing and space data services would undoubtedly increase the involvement of private enterprises in the space sector.

Strategic Partnership across the value chain

Partnerships with investment companies can help organizations in the space sector grow their corporate venture arms more swiftly and enhance their capacity to act fast on interesting investment opportunities. Such alliances are advantageous to investment firms as well since they can use the contacts in the sector, the technical know-how, and the resources of the space business to help their portfolio companies flourish.

For instance, Boeing and the aerospace private investment firm AE Industrial Partners collaborated to run Boeing's venture capital fund HorizonX.8 In July 2022, the two organizations announced the opening of a second HorizonX venture fund with the aim of raising $250 million to invest in promising start-ups in the fields of digital enterprise applications, future mobility, networks, security, space, and sustainability. This announcement marked a further strengthening of the two organizations' partnership. The MMR report for space tourism and investment are covered a detailed analysis of partnership and M&A competitive benchmarking to understand the industry competition.

Even the US government recognizes the advantages of working together with investment companies to promote innovation in the field. The US Space Force and the investment company Embedded Ventures established a collaboration on R&D potential to support the expansion of the US space industry in October 2021.

An increase in technical advancement, particularly in the field of launches, is primarily to blame for this. Reusability, which is SpaceX's area of expertise, was one of the key factors in lowering launch costs, which made it less expensive and simpler for businesses to launch their payloads into space. Another factor is the miniaturization of technology, which has led to the development of more compact, lighter, and more cost-effective satellites like the standardized Cubesat.

A new type of competition will change market dynamics

Companies with horizontal integration are already developing into a business ecosystem. These businesses focus on providing building-block goods and services such as launch vehicles, training, life support equipment, space suits, flight control systems, launch facilities, mission planning, and management. Companies that specialize in providing space tourism products and services based on economies of scale and best-of-breed will emerge from this ecosystem. A private astronaut mission recruiting and management is an example; companies like Space Adventures concentrate on offering consumers unique space experiences. Other organizations including NASA, NASTAR, Zero-G, SpaceX, and Roscosmos are among those with which Space Adventures has contracts for the training and launch services. For example, Commercial facilities for launching and receiving spacecraft are known as spaceports. Commercial spaceports are sprouting up all over the place. 13 spaceports in the US are currently licensed by the FAA.

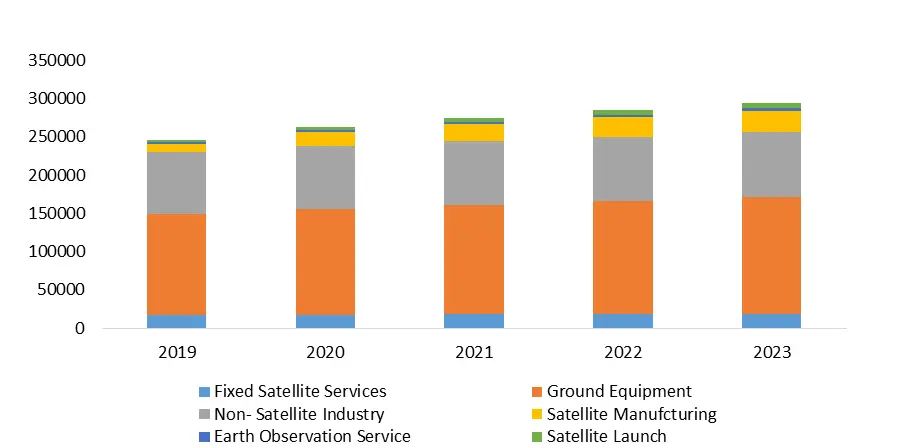

The Top Sectors For Space Investment Over The Past 5 Years (USD Billion) (2019-2023)

Over the next ten years, the space tourism market is expected to experience a vertical-to-horizontal market shift. Markets like personal computers and telecom equipment, which were once controlled by massive vertically integrated companies, have undergone similar changes in the past. Such a change began with the establishment of the business environment already stated. It is expected that venture capital investments in commercial space enterprises would contribute to the change. Customers will profit from lower prices and more options.

Why MMR

"Maximize Market Research (MMR) Analysis in Space is a reputable research and consulting firm, offering comprehensive expertise across various sectors. Our professional services cater to the entire space value chain, encompassing emerging space enterprises, startups, Fortune 500 organizations, and established aerospace companies worldwide.

With a global presence in key regions such as the United Kingdom, Australia, Canada, Japan, Luxembourg, New Zealand, and the United Arab Emirates, we also have experienced space professionals strategically located in Washington, DC, Colorado, California, Texas, and Alabama.

At MMR, we pride ourselves on providing unique insights and unbiased viewpoints on critical aspects like the US Department of Defense, government policies, open architecture solutions, and corporate transformations. Our team of experts has hands-on experience in rocket launches, satellite remote sensing systems, global communications solutions, in-depth analysis of the commercial space economy, and securing private capital for space technology firms.

We maintain an extensive repository of resources, enabling us to leverage our expertise, reputation, qualifications, and diverse perspectives, setting us apart from our competitors in delivering exceptional value to our clients."

Top Space tourism companies

1. Space Adventures

2. Virgin Galactic

3. Blue Origin

4. SpaceX

5.Boeing

6.Roscosmos

7.Zero2Infinity

8.World View Enterprises

9.Bigelow Aerospace

10.Axiom Space

11.Orion Span

12.ZERO-G