India Footwear Market: by Product Type (Casual Footwear, Active/Sport Footwear, Leather Footwear), Material (Leather, Rubber, Synthetic) Distribution Channel (Online Retail, Department Stores, Specialty Stores)- Forecast to 2034

Overview

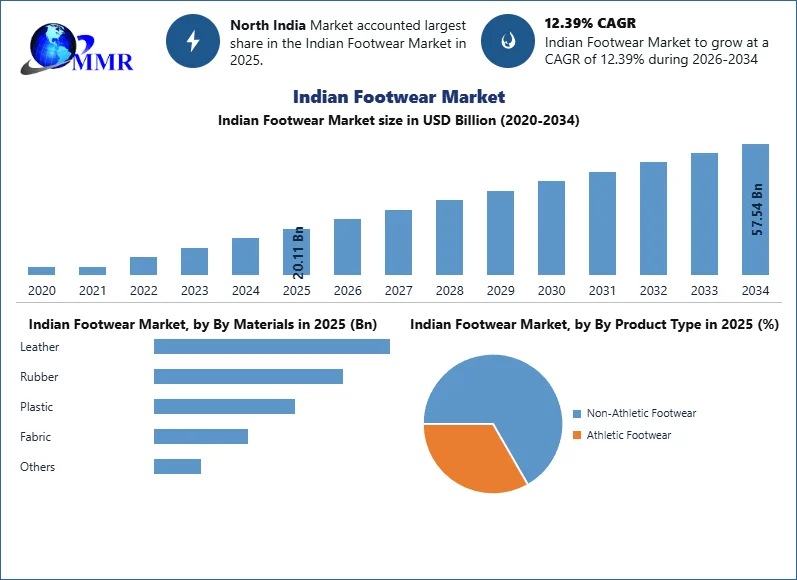

The India Footwear Market was valued at USD 20.11 billion in 2025 and is projected to reach USD 57.54 billion by 2034, registering a CAGR of 12.39% during the forecast period (2025–2034). Growth is driven by rising disposable incomes, expanding e-commerce, increasing demand for branded and athletic footwear, and the rapid growth of organized retail across India.

India Footwear Market Overview

Indian footwear market is witnessing growth driven by higher disposable incomes, urbanization, retail development, and increasing demand for branded, athleisure, and premium footwear. India remains one of the leading producers of footwear on the global platform while internal demand is fueled by the rising middle class, online shopping, and changing fashion trends. Investments in production capacities, innovation, and sustainable footwear options offered by both domestic and international brands help the market grow.

India is one of the major manufacturers of footwear globally due to the presence of well-developed production clusters in such states as Tamil Nadu, Uttar Pradesh, and Maharashtra. According to the Council for Leather Exports (CLE), the exports of India's leather and non-leather footwear rose by 25% to USD 5.7 billion in FY 2024-25. The main export markets of India included the United States, the United Kingdom, Germany, and the UAE. The labour-intensive footwear and leather industry creates jobs for about 4.2 million people in the country.

Initiatives of the government have further improved the prospects of the industry in the long run. The IFLDP is facilitating the process of technological upgradation, infrastructural improvements, mega footwear cluster formation, and capacity building for the MSME sector. Apart from that, the Union Budget of 2025 has incorporated specific initiatives to improve the process of local manufacturing of footwear and its components, designing, increasing employment, and foreign investments under the "Make in India" slogan. All these steps are expected to make the exports more competitive, increase production, and make India a favored sourcing location for the footwear industry.

To know about the Research Methodology :- Request Free Sample Report

India's Footwear Revolution: From Production Powerhouse to Export Giant

India has emerged as one of the world's leading footwear manufacturing and export hubs, supported by a large raw material base, competitive manufacturing costs, and a well-established production ecosystem. According to ITC Trade Map, India's total merchandise exports reached approximately USD 446.6 billion in 2025, reflecting the country's strengthening position in global trade. The footwear industry remains a key contributor to India's labour-intensive manufacturing sector, with major production clusters located in Tamil Nadu, Uttar Pradesh, Maharashtra, Andhra Pradesh, and West Bengal, serving both domestic and international markets.

India's footwear export sector recorded strong momentum during FY 2024–25, with leather and non-leather footwear exports increasing by nearly 25% to approximately USD 5.7 billion, exceeding the export target set by the Government of India. According to the Council for Leather Exports (CLE), the industry is expected to surpass USD 6.5 billion in exports during FY 2025–26, driven by rising demand from key markets such as the United States, Germany, the United Kingdom, France, and the UAE, along with increasing global sourcing diversification toward India.

The Rise of India’s Footwear Industry: Investment Insights and Market Trends

The India footwear sector continues to attract significant domestic and foreign investments as global manufacturers diversify their sourcing strategies and expand production capacity in the country. Backed by 100% Foreign Direct Investment (FDI) under the automatic route, competitive manufacturing costs, and supportive government policies, India is emerging as a preferred destination for footwear production, particularly in southern manufacturing clusters.

In 2025, major investments were announced by leading global footwear manufacturers to strengthen India's manufacturing ecosystem. Vietnam-based Evervan Group signed a Memorandum of Understanding (MoU) with the Government of Tamil Nadu to establish a large-scale non-leather footwear manufacturing facility with an investment of approximately ₹5,000 crore (USD 600 million). The project is expected to create around 50,000 direct jobs over the coming years, significantly enhancing India's export-oriented footwear manufacturing capacity. In addition, global brands and contract manufacturers continue to expand sourcing and production operations across Tamil Nadu and Uttar Pradesh to serve growing demand from North America and Europe.

India Footwear Market Dynamics

The Dynamic Forces Driving Growth in India's Footwear Market

The India footwear market is driven by various key factors. Increasing disposable incomes are aiding consumers to spend more on higher quality and branded footwear, while rapid development and changing lifestyles are growing the demand for fashionable and diverse footwear options. Increasing awareness of health & fitness is also boosting the India footwear market for athletic and sports footwear.

The growth of E-commerce has made footwear more nearby, notably in remote areas, driving sales further. Furthermore, experience to worldwide fashion trends and a large, youthful population are driving demand for stylish and trendy footwear. Government initiatives like 'Make in India' are supporting domestic production, and the raise of organized retail, along with the opening of exclusive brand outlets, is boosting consumer access to a expansive range of footwear choices. These factors combined are driving the growth of the India footwear market.

Challenges and Growth Barriers in India's Footwear Industry

The Indian footwear markets on the brink of major growth, but several challenges may hinder its potential. One key challenge is the stagnation in production capacity, presently at around 2.2 billion pairs annually. This stagnation is mostly due to policies that prioritize SME businesses, combined with a heavy tax burden on the organized industry, which has suppressed the industry's growth. This issue poses a possible threat to the exchequer, as India's existing production capacity is insufficient to meet future demand. As demand for footwear increases, India could become heavily reliant on imports, mainly from China, which benefits from a well-organized industry, ample production capacity, and low production costs. If India's per capita demand for footwear scopes the current average of developed markets by 2032, domestic production at present levels would only be able to meet 25 per cent of the demand, possibly resulting in an annual forex loss of around USD 55 billion due to imports.

Rising Trends and Opportunities in the Indian Footwear Market

Footwear market in India has been experiencing dynamic growth focused by various emerging trends and opportunities. One major trend is the rise in demand for athleisure and sports footwear, as consumers progressively prioritize health, comfort, and style. This shift is inducing brands to expand their product helps and innovate with technology-driven features, like fitness tracking. Another significant trend is the rising prominence on sustainability, with consumers obtaining eco-friendly and properly produced footwear. This shift presents opportunities for brands to adopt environmental practices, use recyclable materials, and accelerate transparency in their supply chains.

Additionally, growing digital platforms is transforming how consumers shop for footwear, indicating to increased online sales and the need for a strong digital presence. As disposable incomes rise and growth go faster, there is also a growing India Footwear market for premium and fashion-forward footwear. Brands that can essentially capitalize on these trends by focusing on sustainability, innovation, and digital engagement are well-positioned to follow in the increasing Indian footwear market.

India Footwear Market Segment Analysis

In 2025, the Product Type segment is dominated by Non-Athletic Footwear, particularly Flip-Flops/Slippers and Sneakers, due to their affordability, comfort, and widespread daily usage across urban and rural populations. Flip-flops and slippers hold a significant share driven by India's climate and price-sensitive consumer base. However, Athletic Footwear is the fastest-growing segment, fueled by increasing health awareness, rising participation in sports and fitness activities, and the growing influence of athleisure trends. Within this category, Running Shoes and Sports Shoes witness strong demand, especially among urban youth and working professionals. Trekking and hiking shoes are gaining traction but remain niche compared to other categories.

Based on Materials, Rubber and Plastic dominate the market in 2025 due to their low cost, durability, and suitability for mass production, making them highly preferred in the mass segment. These materials are extensively used in slippers, sandals, and affordable footwear categories. Leather, on the other hand, holds a strong position in the premium and luxury segments, driven by demand for formal and high-quality footwear. Fabric-based footwear is gaining popularity, particularly in athletic and casual segments, due to its lightweight, breathable, and comfort-oriented properties. Overall, while traditional materials continue to lead, there is a gradual shift toward innovative and sustainable materials.

Based on Distribution Channel, Offline channels, particularly Specialty Stores and Brand Outlets, dominate the market in 2025 as consumers prefer trying footwear before purchase to ensure comfort and fit. However, Online Retail is the fastest-growing segment, driven by the rapid expansion of e-commerce platforms, attractive discounts, wide product variety, and increasing smartphone penetration. Department stores and supermarkets contribute moderately, mainly in urban areas. The shift toward omnichannel retailing is becoming a key trend, with brands strengthening both online and offline presence.

Recent Developments

Bata India Limited: In May 2025, Bata India announced its continued premiumization strategy by expanding the Power, Hush Puppies, and Floatz portfolios while accelerating digital and omnichannel retail initiatives. The company also continued optimizing its manufacturing footprint and supply chain to improve operational efficiency and profitability.

Metro Brands Limited: During FY2025, Metro Brands expanded its premium retail presence across India through new store openings while strengthening partnerships with global brands including Crocs, Foot Locker, and FitFlop. The company continued investing in omnichannel capabilities and premium footwear formats to cater to growing consumer demand.

Campus Activewear: In FY2025, Campus Activewear increased investments in product innovation and manufacturing automation while expanding its sports and athleisure footwear portfolio. The company also strengthened its distribution network across Tier II and Tier III cities through exclusive brand outlets and multi-brand retail expansion.

Liberty Shoes Limited: In 2025, Liberty Shoes accelerated its retail transformation by expanding exclusive brand outlets and increasing its focus on lightweight, sustainable, and comfort-driven footwear collections. The company also enhanced its e-commerce presence to strengthen direct-to-consumer sales.

Phoenix Kothari Footwear: In 2025, Phoenix Kothari Footwear announced the development of India's first non-leather footwear component manufacturing park in Perambalur, Tamil Nadu. The project aims to attract component manufacturers from Taiwan, Singapore, China, and other countries, reducing import dependence and strengthening India's export-oriented footwear supply chain.

| India Footwear Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 20.11 USD Bn |

| Forecast Period 2026-2032 CAGR: | 12.39% | Market Size in 2034: | 57.54 USD Bn |

| Segments Covered: | By Product Type | Non-Athletic Footwear Boots Flip-Flops/Slippers Sneakers Others Athletic Footwear Running Shoes Sports Shoes Trekking/Hiking Shoes Others |

|

| By Materials | Leather Rubber Plastic Fabric Others |

||

| By Pricing | Luxury Premium Mass |

||

| By Distribution Channel | Online Retail Department Stores Specialty Stores Supermarkets Brand Outlets Others |

||

| By End User | Men Women Kids |

||

India Footwear Market Regional Analysis:

Based on Region, North India leads the India footwear market in 2025, driven by high population density, strong retail infrastructure, and significant demand across both urban and semi-urban areas. West India follows closely, supported by economic hubs and higher disposable incomes, particularly in states like Maharashtra and Gujarat. South India shows strong growth due to increasing urbanization, rising middle-class population, and expanding retail networks. East India is an emerging market with growing demand, supported by improving economic conditions and retail penetration. Overall, regional growth is influenced by urbanization, income levels, and access to organized retail channels.

India Footwear Market Competitive Analysis

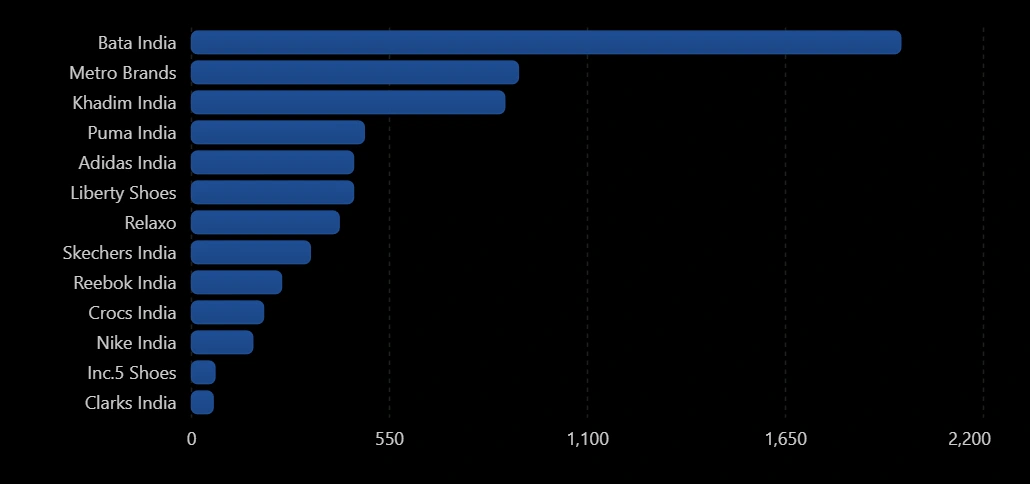

The India footwear industry is dominated by key players like Bata India, Relaxo Footwears, Metro Brands, Campus Activewear, and Liberty Shoes, each with unique market strategies. Bata India is a market leader, leveraging its extensive retail network with over 1,500 stores nationwide. Its focus on modernizing stores and enhancing its digital presence has strengthened its brand appeal among urban consumers. In comparison, Relaxo Footwears targets the mass market with affordable and durable products, particularly excelling in the flip-flops and casual footwear segments.

Metro Brands, known for its premium offerings, has grown its market share through acquisitions and partnerships, like its recent stake in Cravatex Brands, to diversify its product line. Campus Activewear has carved a niche in the athleisure segment, focusing on youth-oriented and sports footwear, capitalizing on the growing demand for stylish and affordable sports shoes. Liberty Shoes continues to hold a significant share in the mid-segment India footwear market, leveraging its strong distribution network.

The competitive landscape is shaped by factors like brand loyalty, product diversification, and pricing strategies, with each company adapting to the evolving consumer preferences and the rising trend of online shopping to maintain its market position.

India Footwear Market Scope: Inquire before buying

Key Players in India Footwear Market

- Nike India

- Adidas India

- Crocs India

- Puma Sports India

- Reebok India

- Relaxo

- Bata India Ltd.

- Liberty

- Ajanta Shoes

- Khadims

- Campus Activewear

- Paragon

- Action Footwears Pvt. Ltd.

- Sreeleathers

- Catwalk

- Metro Brands Limited.

- Lallan Shoes

- Red Chief (RSPL Group)

- Footwear

- Dayz Footwear

- Red Tape

- Woodland

- Others

FAQs

1. What is the size of the India Footwear Market in 2025?

The India Footwear Market was valued at USD 20.11 billion in 2025 and is projected to reach USD 57.54 billion by 2034, expanding at a CAGR of 12.39% during the forecast period. Market growth is driven by rising disposable incomes, rapid urbanization, expanding e-commerce, and increasing demand for branded and athletic footwear.

2. What are the key drivers of the India Footwear Market?

The India footwear market is driven by increasing consumer spending, growing demand for athleisure and premium footwear, rapid expansion of organized retail, rising online footwear sales, and government initiatives such as the Indian Footwear and Leather Development Programme (IFLDP) and 100% FDI in footwear manufacturing.

3. How is India's footwear export industry performing in 2025?

India's footwear export industry recorded strong growth in FY 2024–25, with leather and non-leather footwear exports reaching approximately USD 5.7 billion, supported by increasing demand from the United States, Germany, the United Kingdom, France, and the UAE. The country's competitive manufacturing ecosystem and expanding production capacity continue to strengthen its position in the global footwear market.

4. Which companies are leading the India Footwear Market?

Leading companies operating in the India Footwear Market include Bata India, Metro Brands, Campus Activewear, Relaxo Footwear, Liberty Shoes, Khadim India, Puma India, Adidas India, Nike India, Crocs India, Reebok India, and Skechers India. These companies are focusing on retail expansion, product innovation, digital transformation, and manufacturing investments to strengthen their market presence.

5. What are the future trends shaping the India Footwear Market?

The future of the India Footwear Market is expected to be driven by sustainable footwear manufacturing, increasing adoption of recycled and eco-friendly materials, expansion of domestic manufacturing under the Make in India initiative, growth in athleisure footwear, AI-enabled retail experiences, and rising investments by global manufacturers to position India as a major footwear production and export hub.