India Electric Vehicle Powertrain Market by Component, Propulsion Type and Vehicle Type - Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

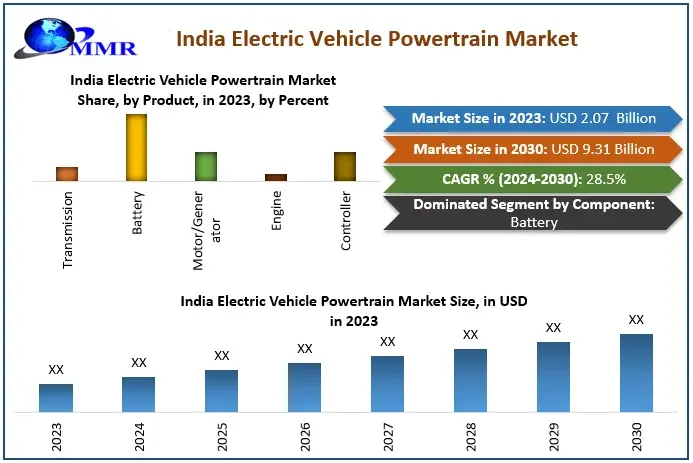

India Electric Vehicle Powertrain Market Size is expected to grow at a CAGR of 28.5% throughout the forecast period, to reach US$ 9.31 Billion by 2030

The electric vehicle (EV) powertrain market in India is experiencing significant growth due to technological advancements, environmental concerns, and a supportive government policy environment. With a population of over 1.4 billion and increasing urbanization, India is at a pivotal moment in the transition toward sustainable mobility. The powertrain comprising critical components such as the battery, motor/generator, transmission, engine, and controller—is fundamental to EVs as it determines overall vehicle performance, range, and efficiency. As a result, the development and adoption of efficient EV powertrains are essential to India’s EV market growth.

The market analyzed across key components, propulsion types (battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs)), and vehicle types (including passenger cars, two-wheelers, commercial vehicles, and three-wheelers). electric vehicle (EV) powertrain represents a unique set of opportunities within the India Electric Vehicle Powertrain Market demand.

The growth of the electric vehicle market is critical for energy transition in the country, reducing the belief on oil imports and rising demand for renewable power. Additionally, technology improvement, cost reduction and local manufacturing of lithium-ion batteries are expected to catalyze the growth of the Electric Vehicle market in India. India has set ambitious goals to reach specific EV sales targets by 2030: 30% for private cars, 70% for commercial vehicles, 40% for buses, and 80% for two-wheelers and three-wheelers. This translates to an aim of having 80 million EVs on Indian roads by 2030, aligning with the 'Make in India' initiative to encourage complete domestic EV production.

The year 2023 witnessed a significant 49.25% growth in EV sales in India, reaching 1.52 million units, highlighting steady progress in the sector’s early stages. Globally, the shift to electric vehicles is creating new opportunities for automotive suppliers, and India’s EV battery market is anticipated to expand from USD 16.77 billion in 2023 to USD 27.70 billion by 2028. In terms of infrastructure, as of February 2024, India has 12,146 operational public EV charging stations, with Maharashtra leading, followed by Delhi and other states. A recent report from the Confederation of Indian Industry (CII) highlighted the need for at least 1.32 million charging stations across the country by 2030 to support the rapid EV growth, which translates to over 400,000 installations annually which boost India Electric Vehicle Powertrain Market.

To know about the Research Methodology:-Request Free Sample Report

India Electric Vehicle Powertrain Market Dynamics:

India Electric Vehicle Powertrain Market Driver:

The Indian government has actively promoted EV adoption as a part of its broader strategy to reduce fossil fuel dependence and curb urban pollution level. Programs like the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme have incentivized both EV manufacturers and consumers, with the aim of achieving substantial reductions in pollution from traditional vehicles. These policies offer subsidies, tax benefits, and grants for EV manufacturers, helping to make EVs a more attractive option for consumers across the country. Environmental consciousness is on the rise, as air pollution becomes a public health crisis in many cities. The growing awareness of climate change and health impacts associated with vehicle emissions is encouraging individuals and businesses to consider EVs as a cleaner alternative to traditional vehicles drives the India Electric Vehicle Powertrain Market.

India Electric Vehicle Powertrain industrial sector is witnessing rapid expansion, driven by government incentives, increasing environmental awareness, and advances in technology. Through initiatives like the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme, India is aiming to significantly boost EV adoption, transforming its transportation landscape toward sustainability and innovation. Leading industry players are focused on enhancing EV charging infrastructure. Hyundai Motor India, for instance, is expanding accessibility to EVs by developing an ultra-fast charging network, with 11 new stations in cities like Mumbai, Pune, Ahmedabad, Hyderabad, Gurugram, and Bangalore, as well as key highways.

The significant driver is the reduction in battery costs, which traditionally accounted for a substantial portion of EV expenses. Technological advances and increasing production have significantly down the price of lithium-ion batteries, making EVs more financially feasible and boosting demand. In addition, urbanization and rising disposable incomes have positioned more Indian consumers to adopt EVs, particularly within the middle class. This trend is reinforced by the Aatmanirbhar Bharat (self-reliant India) initiative, which aims to reduce dependence on imports and bolster domestic EV manufacturing. This push for local manufacturing and supply chain development has been essential in growing the India Electric Vehicle Powertrain Market.

• FAME II Scheme: India’s Faster Adoption and Manufacturing of Hybrid and Electric Vehicles” (FAME II) scheme, launched in 2019, provides substantial subsidies and incentives for EVs, covering two-wheelers, three-wheelers, and public transportation. Under FAME II, the Indian government has allotted subsidies for over 1.5 million electric two-wheelers and aims to encourage localization in EV production.

• Production Linked Incentive (PLI) Scheme: This scheme incentivizes local manufacturing of EV components, including advanced batteries and electric powertrain parts, reducing India’s dependence on imports and encouraging more efficient, cost-effective production. Companies like Ola Electric and Ather Energy are benefiting from these incentives, focusing on domestic production of electric two-wheelers.

India Electric Vehicle Powertrain Market Restraints:

The high initial costs of EVs continue to deter many potential buyers, particularly in the price-sensitive two-wheeler and three-wheeler segments. While battery costs have decreased, EVs generally still have a higher upfront price compared to traditional internal combustion engine (ICE) vehicles, creating a price barrier in the Indian market. The lack of a comprehensive and accessible charging infrastructure is another significant barrier to large-scale EV adoption. Although public and private sectors are making efforts to expand the charging network, its current insufficiency, especially for long-distance travel, affects the usability of EVs, for commercial and passenger vehicles in India Electric Vehicle Powertrain Market growth. For example, MG ZS EV and Hyundai Kona Electric offer premium features but remain on the higher end of the price spectrum, making them less accessible to the average consumer. Consequently, many buyers hesitate to choose EVs due to the initial price barrier.

The general lack of awareness among consumers regarding EV technology. Many potential buyers are unfamiliar with EV benefits or have misconceptions about the range, durability, and performance of EVs, which discourages adoption. Additionally, the widespread range anxiety among consumers, due to concerns about the limited driving range of EVs and sparse charging infrastructure, is a significant factor hindering wider adoption. Overcoming these challenges requires an ongoing commitment to expanding infrastructure and educating consumers which drives the India Electric Vehicle Powertrain Market investment.

India Electric Vehicle Powertrain Segment Analysis:

The India Electric Vehicle Powertrain Market is segmented by components batteries, motors/generators, transmission, controllers, and engines. Batteries witnessed highest market share in 2023. The major cost driver, and with continued advancements in lithium-ion and emerging battery technologies, battery performance, cost, and longevity are anticipated to improve, making EVs more viable for broader market segments. Motors and controllers, responsible for propulsion and energy regulation, are essential components seeing advancements that enhance efficiency and driving range. As EV technology advances, more efficient transmission systems are being developed, allowing for improved energy efficiency and driving performance and India Electric Vehicle Powertrain Market investment and customer base.

Based on Propulsion Type, is categorized into Battery Electric Vehicles (BEVs) and Plug-In Hybrid Electric Vehicles (PHEVs). BEVs, which operate solely on electric power stored in batteries, witnessed the highest market share in 2023, influencing India’s EV landscape, particularly in the passenger and two-wheeler segments. The dominance of BEVs is largely attributed to their simplicity and reduced operating costs, making them appealing for the Indian market, where cost efficiency is a priority. Smaller passenger vehicles and two-wheelers have especially benefitted from BEVs due to their straightforward designs, lower maintenance needs, and the rapid reduction in battery costs. Additionally, with government schemes favoring zero-emission vehicles, BEVs have become the go-to choice for environmentally conscious consumers looking for fully electric options without the complexities of hybrid engines which boost market technological advancement.

Plug-In Hybrid Electric Vehicles (PHEVs) offer a compelling solution for specific consumer needs. PHEVs combine an electric motor with an internal combustion engine, allowing drivers to use electric power for shorter commutes while relying on gasoline for longer trips. This hybrid flexibility is valuable in areas where charging infrastructure remains underdeveloped or sparse. The availability of PHEVs enables consumers to gradually transition towards electric mobility without the range anxiety associated with pure electric models. However, limited awareness, higher costs, and the push for a complete transition to electric vehicles have kept PHEVs in a smaller niche, they are influencing potential as India continues to expand its EV charging infrastructure across regions propel the India Electric Vehicle Powertrain Market investment targeted customers in production analysis.

India Electric Vehicle Powertrain Market Analysis:

The objective of the report is to present a comprehensive analysis of India Electric Vehicle Powertrain Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of industry with dedicated study of key players that includes market leaders, followers and new entrants by region.

PORTER, PESTEL analysis with the potential impact of micro-economic factors by region on the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give clear futuristic view of the industry to the decision-makers.

The report also helps in understanding India Electric Vehicle Powertrain Market dynamics, and structure by analyzing the market segments, and projecting the India Electric Vehicle Powertrain Market size. Clear representation of competitive analysis of key players by type, price, financial position, product portfolio, growth strategies, and regional presence in the India Electric Vehicle Powertrain Market make the report investor’s guide.

India electric vehicle powertrain market Scope: Inquire before buying

| India Electric Vehicle Powertrain Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | USD 2.07 Billion |

| Forecast Period 2024 to 2030 CAGR: | 28.5% | Market Size in 2030: | USD 9.31 Billion |

| Segments Covered: | by Component | Transmission Battery Motor/Generator Engine Controller |

|

| by Propulsion Type | Battery Electric Vehicle Plug-In Hybrid |

||

| by Vehicle Type | Passenger Cars Two-Wheelers commercial Vehicles Three-Wheelers |

||

India Electric Vehicle Powertrain Market, Region

North India

South India

West India

East India

India Electric Vehicle Powertrain Market Key Players

1. AVTEC Ltd.

2. Hyundai Motor India Limited

3. Maruti Suzuki India Limited

4. Tata Autocomp Systems Limited

5. Sintercom India Ltd

6. Electrodrive Powertrain Solutions Pvt Ltd.

7. Physics Motors Technology

8. C-electric Automotive Drives

9. Elecnovo Pvt Ltd, Bengaluru

10. Quanteon Powertrain

11. Cell Propulsion

12. Rizel Automotive

13. Vinuruk Technologies

14. Napino Auto & Electronics Ltd

15. Jayem Automotives

Frequently Asked Questions:

1. What is the growth rate of market?

Ans: The market is growing at a CAGR of 28.5% during forecasting period 2023-2030.

2. What is scope of the India Electric Vehicle Powertrain Market report?

Ans: India Electric Vehicle Powertrain Market report helps with the PESTEL, PORTER, Recommendations for Investors & Leaders, and market estimation of the forecast period.

3. Who are the key players in India Electric Vehicle Powertrain Market?

Ans: The important key players in the India Electric Vehicle Powertrain Market are AVTEC Ltd., Hyundai Motor India Limited, Maruti Suzuki India Limited, Tata Autocomp, and Systems Limited.

4. What is the study period of this Market?

Ans: The India Electric Vehicle Powertrain Market is studied from 2023 to 2030.