India Electric Vehicle Motor Market - Industry Structure Evaluation, Demand Drivers Analysis, Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2034

Overview

India Electric Vehicle Motor Market size was valued at USD 1.56 Bn in 2025 and is expected to reach USD 6.88 Bn by 2034, at a CAGR of 17.92 %.

India Electric Vehicle Motor Market Overview

Electric vehicle (EV) motors are essential to the operation of electric vehicles, converting electrical energy stored in the battery into mechanical energy that propels the vehicle. Unlike internal combustion engines (ICE), which rely on fuel combustion to generate power, EV motors use alternating current (AC) to rotate the wheels. The process begins with direct current (DC) from the battery being converted to AC by an inverter. The inverter controls the speed and torque of the motor by adjusting the frequency and amplitude of the AC signal.

EV motors have regenerative braking capabilities, where the motor acts as an alternator during deceleration, converting kinetic energy back into electrical energy, which is stored in the battery. Key components of an EV motor system include the electric motor, inverter, battery, controller, and charger. These components work together seamlessly, contributing high efficiency, fewer moving parts and significantly reduced maintenance compared to traditional ICE vehicles, making EV motors a crucial technology in the transition toward sustainable transportation. Increasing awareness towards energy conservation and acceptance of electric vehicles are driving the demand for Electric Vehicle Motors industry in India. India Electric Vehicle Motor Market is driven by rapid urbanization and stringent regulations towards power consumption. Initiatives such as Make in India resulted in growth in demand for electric vehicle motors in India.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

India Electric Vehicle Motor Market Dynamics

Strong Government Support and Localization Initiatives Accelerating the India Electric Vehicle Motor Market

Increasing government support through incentive programs, domestic manufacturing initiatives, and charging infrastructure expansion is a key driver of the India Electric Vehicle (EV) Motor Market in 2025. The Government of India has shifted its focus from demand incentives alone to building a comprehensive EV manufacturing ecosystem through the PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE) Scheme, launched with a total outlay of ₹10,900 crore. The scheme supports the adoption of more than 2.8 million electric vehicles, including electric two-wheelers, three-wheelers, trucks, ambulances, and buses, while also allocating ₹2,000 crore for public charging infrastructure and ₹780 crore for upgrading vehicle testing agencies. Complementing this are the PLI Scheme for the Automobile and Auto Components sector, the Advanced Chemistry Cell (ACC) Battery PLI Scheme, and the Scheme to Promote Manufacturing of Electric Passenger Cars (SMEC), which encourage localization of EV motors, power electronics, controllers, and battery systems. The government's emphasis on domestic value addition, Make in India manufacturing, and charging network expansion is attracting significant investments from global and domestic OEMs, accelerating EV production and increasing demand for high-efficiency traction motors across passenger vehicles, commercial vehicles, and electric two- and three-wheelers. These initiatives are expected to significantly drive the growth of the India Electric Vehicle Motor Market over the forecast period.

Expansion of EV Component Manufacturing and Global Investments Creating Growth Opportunities for the India EV Motor Market

The rapid expansion of electric vehicle component manufacturing and increasing investments by global and domestic manufacturers present a significant opportunity for the India Electric Vehicle Motor Market. In 2025, the Government of India introduced the Scheme to Promote Manufacturing of Electric Passenger Cars (SMEC), offering reduced import duties to global automakers that commit a minimum investment of ₹4,150 crore (US$500 million) in local EV manufacturing facilities. This policy is expected to attract leading international EV manufacturers while strengthening domestic production of critical components such as traction motors, motor controllers, power electronics, and drive systems. Simultaneously, the PM E-DRIVE Scheme and the PLI Scheme for Auto Components are encouraging suppliers to establish localized manufacturing ecosystems for advanced EV components, reducing import dependence and enhancing India's position as a global EV manufacturing hub. Growing investments in integrated EV supply chains, combined with increasing demand for locally manufactured electric drivetrains, are creating substantial opportunities for motor manufacturers, Tier-1 suppliers, and technology providers. As India scales up EV production for both domestic consumption and exports, the localization of electric motor manufacturing is expected to improve cost competitiveness, accelerate technology adoption, strengthen supply chain resilience, and drive long-term growth in the India Electric Vehicle Motor Market.

High cost of electric vehicle motor to Hamper Market Growth

Electric vehicles, despite their rising popularity and increasing number of launches, face substantial barriers due to the high costs associated with their core components, particularly the motor. The primary driver of these costs is the advanced technology required to produce electric motors, which involves high-end materials and complex manufacturing processes. Electric motors rely heavily on rare earth metals such as lithium, cobalt, and nickel, which are not only expensive but also involve costly extraction and processing, which hamper India Electric Vehicle Motor Market growth. These materials constitute a significant portion of the total cost, with battery packs alone accounting for 30-40% of an EV's price.

The high R&D investments needed to develop and refine electric motor technology further contribute to the overall expense. Automakers are compelled to pass these costs onto consumers, making EVs less affordable compared to traditional internal combustion engine (ICE) vehicles. The lack of skilled personnel in the evolving field of EV technology also exacerbates the cost issue, as the industry struggles with a shortage of qualified professionals to manufacture and repair these vehicles

India Electric Vehicle Motor Market Segment Analysis

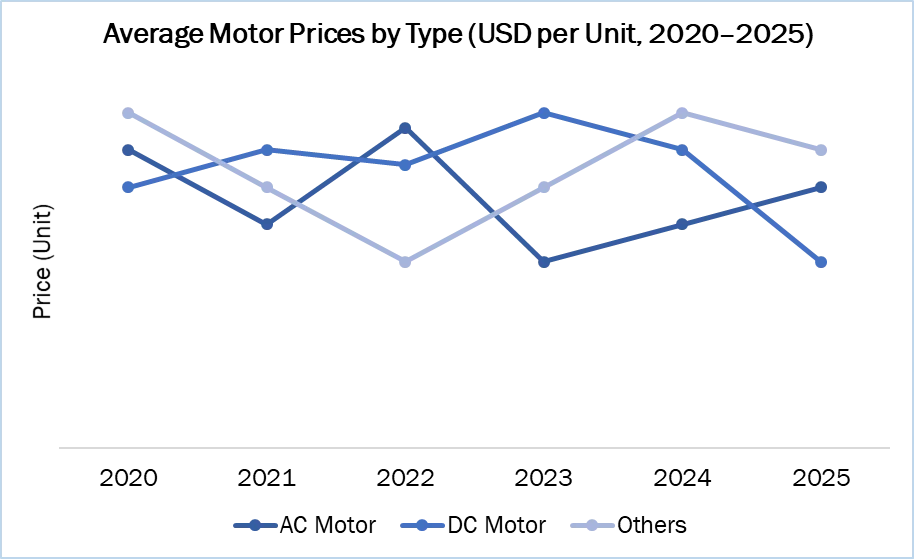

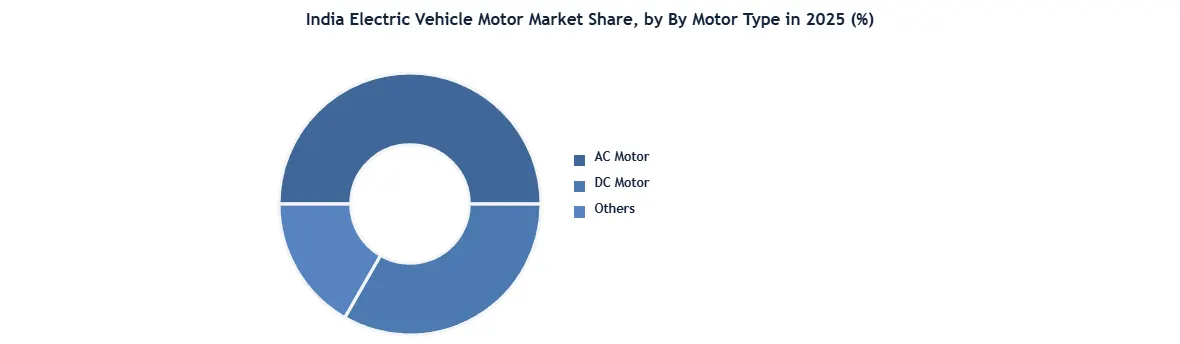

Based on the Motor Type, the market is segmented into Alternating Current (AC) Motor and Direct Current (DC) Motor. A Direct Current (DC) Motor is expected to dominate the India Electric Vehicle Motor Market over the forecast period. A DC motor operates by converting electrical energy into mechanical energy through a process involving key components such as the armature, stator, commutator, and carbon brushes. The armature, which is the rotating part of the motor, is housed within the stator a stationary component that generates a magnetic field. This magnetic field is created by the field windings or permanent magnets, which interact with the armature's magnetic field when direct current is applied.

The commutator, a rotary electrical switch, plays a crucial role by ensuring that the direction of current through the armature windings is reversed at appropriate intervals, enabling continuous rotation. The simplicity and cost-effectiveness of DC motors, coupled with their high torque at low speeds, make them particularly well-suited for a wide range of electric vehicles. These motors provide efficient performance and reliable acceleration, which are essential for both passenger and commercial EVs, which boosts India Electric Vehicle Motor Market growth. DC motors are more compatible with the direct current output from batteries, reducing the need for additional components such as inverters that are required for Alternating Current (AC) motors.

The lower complexity and cost of DC motors contribute to a more affordable overall vehicle price, which is a significant advantage in a price-sensitive market like India. Furthermore, the established supply chain and development infrastructure for DC motors in India support their widespread use across various electric vehicle segments. Although AC motors, particularly Permanent Magnet Synchronous Motors (PMSMs), are gaining traction due to their higher efficiency and regenerative braking capabilities, DC motors continue to lead the market. Their cost advantages, performance benefits, and ease of integration with battery systems ensure their dominance in the India Electric Vehicle Motor Market.

By Electric Vehicle Type, the market is categorized into Battery Electric Vehicles, Hybrid Vehicles and Plug-in Hybrid Vehicles. Battery Electric Vehicle held the largest India Electric Vehicle Motor Market Share in 2025. BEVs are charged through an external power source, typically a standard 120-volt outlet, with the onboard charger converting alternating current (AC) electricity to direct current (DC) to recharge the battery. This battery then powers the electric motor, which drives the vehicle’s wheels. BEVs offer several advantages, including being fun to drive, quiet, and quick off the line. They are also convenient to recharge, eliminating trips to the gas station, and come with benefits such as access to carpool lanes and various incentives. Their operation costs are lower, and maintenance is cheaper due to fewer moving parts.

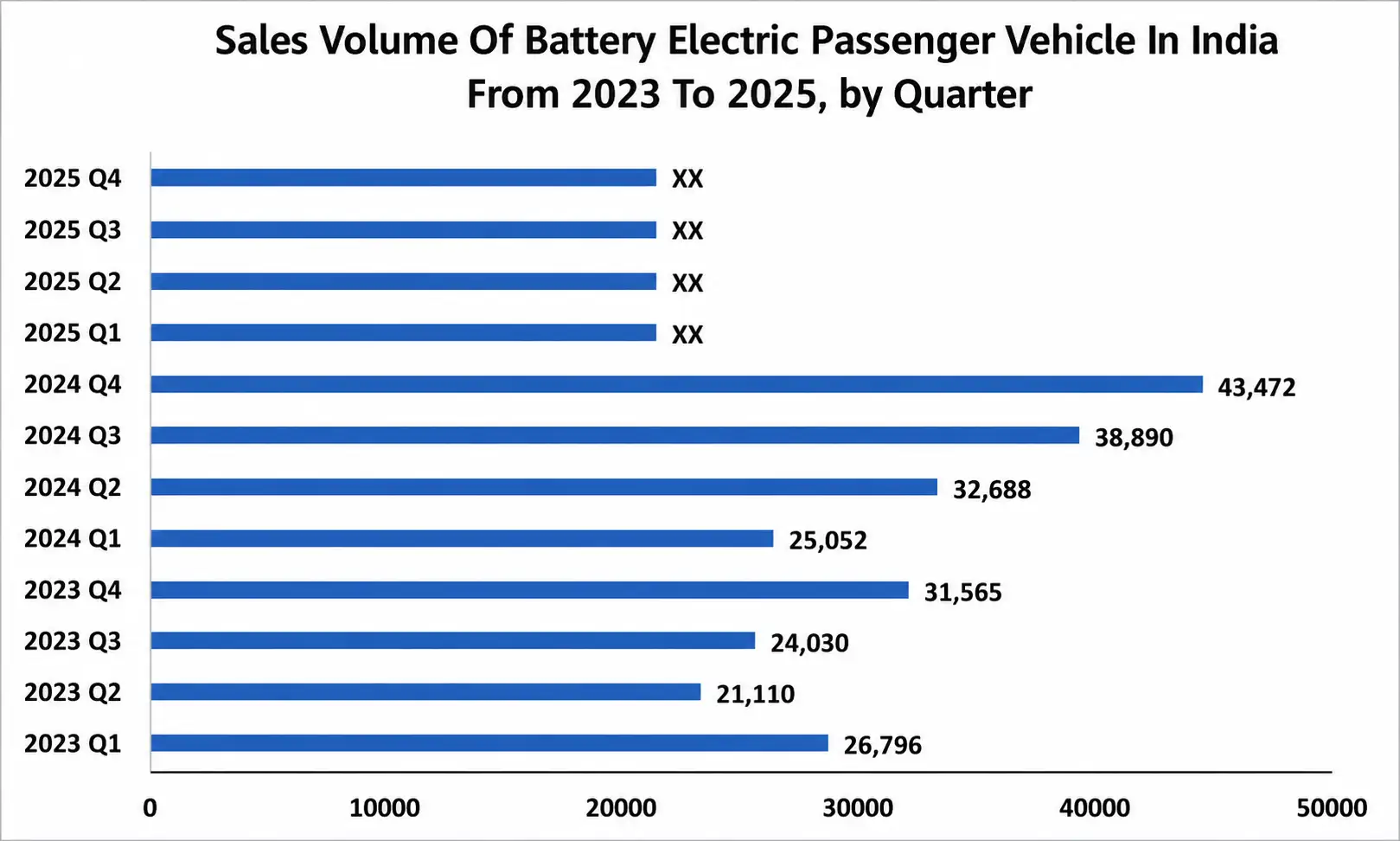

In India, the sales volume of battery electric passenger vehicles surged to over 500,000 units in 2023. The electric vehicle motor market in India experienced significant growth, driven by increased adoption and advancements in technology, contributing to a vibrant and expanding EV sector.

BEVs use high-energy-density lithium-ion batteries, which are usually positioned below the seats for better weight distribution. These batteries are as large as 100 kWh, allowing for driving ranges from about 100 to over 500 miles on a full charge, with even higher ranges anticipated in the future. The market for BEVs in India is expanding rapidly, supported by more than 120 available models and an increasing number of options expected to become available. This surge is driven by the vehicles' high-tech nature, the environmental benefits of zero emissions, and the growing infrastructure for charging. BEVs are therefore a central component of the India Electric Vehicle Motor Market, reflecting the shift towards more sustainable and efficient transportation solutions.

India Electric Vehicle Motor Market Regional Insights

West India is expected to dominate the India Electric Vehicle Motor Market during the forecast period. The combination of strategic industrial advantages, supportive government policies, and robust market demand. The region, encompassing states such as Maharashtra and Gujarat, is home to significant automotive hubs like Pune and Mumbai, which provide a well-established infrastructure for EV manufacturing and assembly. This industrial prowess is bolstered by proactive state policies promoting electric mobility. Maharashtra, in particular, has introduced attractive incentives, subsidies, and supportive frameworks that encourage EV manufacturers to facilitate consumer adoption through reduced costs and financial benefits.

West India exhibits higher urbanization levels and environmental consciousness, with major cities like Mumbai and Ahmedabad leading the charge in adopting electric vehicles. This urban focus drives substantial demand for EVs and, consequently, for EV motors. The region has also seen considerable progress in developing EV charging infrastructure, addressing one of the critical barriers to EV adoption and enhancing the India Electric Vehicle Motor Market viability. These combined factors create a conducive environment for the growth of the EV motor market, positioning West India as a leader in the sector.

Competitive Analysis

The India Electric Vehicle Motor Market is highly competitive, with participation from vehicle OEMs, Tier-1 auto component suppliers, motor manufacturers, and emerging EV technology companies. Tata Motors and Mahindra Electric Mobility hold strong positions through their expanding electric vehicle portfolios and domestic manufacturing capabilities. Component suppliers such as Sona BLW Precision Forgings, Varroc Group, Napino Auto & Electronics, SEG Automotive India, Sterling E-Mobility Solutions, and C-Electric Automotive Drives are strengthening their presence by supplying traction motors, motor controllers, power electronics, and drivetrain components to EV manufacturers.

Emerging companies such as Shakti EV Mobility, Rizel Automotive, Compage Automation, EMF Innovations, Physics Motors Technology, Konmos Technologies, Elecnovo, and Gremot Mobility are focusing on cost-effective motors, customized EV powertrain solutions, electric conversion kits, and localized component development. Competition in 2025 is driven by localization, motor efficiency, lightweight design, rare-earth magnet sourcing, integrated e-axle development, and partnerships with EV OEMs, as companies aim to reduce import dependency and support India’s growing electric mobility ecosystem.

Recent Development

January 2025: Mahindra inaugurated its dedicated Electric Origin manufacturing and battery assembly facility at Chakan, Maharashtra, to support production of its next-generation electric SUVs. The investment expands domestic EV manufacturing capacity and is expected to significantly increase demand for locally manufactured traction motors, motor controllers, e-axles, and other electric powertrain components, strengthening India's EV motor supply chain.

June 2025: The Government of India issued detailed operational guidelines under the Scheme to Promote Manufacturing of Electric Passenger Cars (SMEC), requiring approved manufacturers to invest at least ₹4,150 crore (US$500 million) in domestic EV manufacturing. The policy is expected to attract global automakers and encourage large-scale investments in localized production of electric motors, power electronics, and drivetrain systems, accelerating the growth of India's EV motor ecosystem.

August 2025: Suzuki Motor announced an investment of ₹700 billion (approximately US$8 billion) in India over the next five to six years while commencing production of its first electric vehicle at its Gujarat facility. India has been designated as Suzuki's global EV production hub, with exports planned to more than 100 countries. This investment is expected to drive substantial demand for domestically manufactured electric traction motors, inverters, and motor control systems.

October 2025: Sona BLW Precision Forgings (Sona Comstar) announced continued investments in expanding its electric drive systems business, including advanced traction motor technologies and rare-earth-efficient motor designs. These investments are expected to strengthen India's indigenous EV motor manufacturing capabilities, improve supply chain resilience, and support the transition toward high-efficiency electric powertrains.

March 2026: Valeo inaugurated a new electric powertrain manufacturing line at its Pune facility to expand production of electric propulsion systems for the Indian market. The project increases local manufacturing capacity for traction motors, integrated e-drive systems, and inverters, supporting India's localization goals while enhancing the country's position as a regional hub for EV powertrain manufacturing.

India Electric Vehicle Motor Market Scope: Inquire before buying

| India Electric Vehicle Motor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 1.56 USD Billion |

| Forecast Period 2026-2034 CAGR: | 17.92% | Market Size in 2034: | 6.88 USD Billion |

| Segments Covered: | By Motor Type | AC Motor Induction AC Motor Synchronous AC Motor DC Motor Brushed DC Motor Brushless DC Motor Others |

|

| by Component | Motor Stator Rotor, Shaft, and Bearing Permanent Magnet Casing Wiring & Connectors Others |

||

| by Propulsion Type | Battery Electric Vehicle Hybrid Vehicles Plug-in-Hybrid Vehicles |

||

| by Power Rating | Up to 20 kW 21 kW to 100 kW 101 kW to 250 kW Above 250 kW |

||

| by Powertrain Type | Single Motor Dual Motor Triple Motor Four Motor |

||

| by Application | Two-Wheelers Passenger Vehicles Commercial Vehicles Light Commercial Vehicle Medium & Heavy Commercial Vehicles |

||

| by Distribution Channel | OEM Aftermarket |

||

India Electric Vehicle Motor Market, by Region

North India

South India

East India

West India

India Electric Vehicle Motor Market, Key Players

- Tata Motors Ltd.

- Mahindra Electric Mobility Ltd.

- Sona BLW Precision Forgings Limited

- Varroc Group

- Napino Auto & Electronic

- SEG Automotive India

- Shakti EV Mobility Pvt. Ltd.

- Sterling E-Mobility Solution Ltd.

- Compage Automation

- EMF Innovations

- Physics Motors Technology

- Konmos Technologies

- C-Electric Automotive Drives

- Elecnovo

- Gremot Mobility

- Rizel Automotive

Others

Frequently Asked Questions:

1] What is the growth rate of the India Electric Vehicle Motor Market?

Ans. The India Electric Vehicle Motor Market is growing at a significant rate of 17.92% during the forecast period.

2] Which region is expected to dominate the India Electric Vehicle Motor Market?

Ans. West India is expected to dominate the India Electric Vehicle Motor Market during the forecast period.

3] What is the expected India Electric Vehicle Motor Market size by 2034?

Ans. The India Electric Vehicle Motor Market size is expected to reach USD 6.88 Bn by 2034.

4] Which are the top players in the India Electric Vehicle Motor Market?

Ans. The major top players in the India Electric Vehicle Motor Market are Tata Motors Ltd., Mahindra, Varroc Group and Others.

5] What are the factors driving the India Electric Vehicle Motor Market growth?

Ans. The increasing adoption of electric vehicles and government schemes in India are expected to drive market growth during the forecast period.