India Cement Market by Type(Portland,Blended,Others) and Application(Residential,Commercial,Infrastructure) - Forecast to 2030

Overview

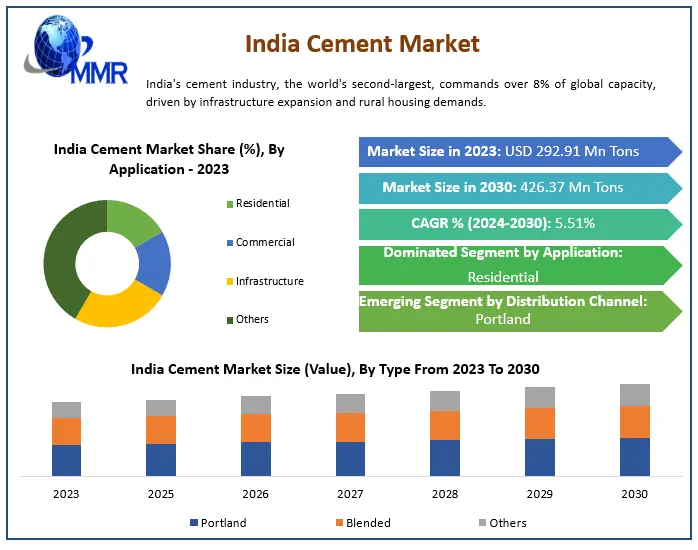

The India Cement Market size was valued at USD 292.91 Mn Tons in 2023 and the total India Cement revenue is expected to grow at a CAGR of 5.51% from 2024 to 2030, reaching nearly USD 426.37 Mn Tons by 2030.

The infrastructure industry in India, crucial for economic growth, drives the real estate and construction sectors, boosting cement production, essential for utilities, bridges, roads, and metropolitan facility improvements.

India Cement Market Overview

The infrastructure industry in India is crucial to the country economic growth since it fosters the expansion of variety of industries such as real estate and construction. The crowing construction industry, which in turn benefits from the rising need for urban dwelling, facilitates the production of cement, which significantly boost the India Cement Market growth. The infrastructure sector includes the provision of utilities, construction of bridges and dams, the construction of roads and the improvement of the metropolitan facilities. The India cement industry is the key sector in achieving these and other objectives.

The India cement market is largest in the world, both in terms of production and consumption. The sector has witnessed steady growth over the years, driven by the increasing demand for housing, infrastructure development, and commercial projects. India has a substantial cement production capacity, with numerous cement plants located across the country. The production capacity has increased over the years to meet the growing demand for cement in various sectors.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

India Cement Market Dynamics

Infrastructure Development and Government Initiatives to boost the India Cement Market growth

The Indian government's commitment to ambitious projects, such as the National Infrastructure Protection Plan (NIPP) and the Bharatmala road projects, has led to substantial demand for cement. These initiatives aim to enhance the country's transportation networks, including highways and roadways, necessitating large quantities of cement for construction. The Pradhan Mantri Awas Yojana (PMAY), with its urban and rural components (PMAY-U and PMAY-G), is a crucial driver for the India Cement Market. PMAY aims to provide affordable housing to all citizens, aligning with the government's vision of 'Housing for All' by 2022. The construction of millions of housing units under this scheme has led to a substantial demand for cement, particularly in the residential construction sector.

India is undergoing rapid urbanization, with an increasing percentage of the population migrating to urban areas. According to projections, 39% of India's population is expected to reside in urban areas by 2030, compared to the current 35%. Urbanization entails the construction of residential and commercial infrastructure, leading to a surge in demand for cement in various construction projects The average size of Indian households has been decreasing, from 5.3 members in 2011 to 4.6 members in 2019. This shift towards smaller households is a noteworthy driver for the India cement market. Smaller households result in the construction of more residential units to accommodate the growing population, translating into a consistent demand for cement.

Price Sensitivity and Affordability to Restrain India Cement Market growth

In certain segments of the market, particularly in residential construction, there exists a degree of price sensitivity. The cost of cement, a key component in construction, that influence consumer and builder decisions, which significantly limits the India Cement market growth. Affordability concerns limit the adoption of cement in construction projects, particularly in regions where cost considerations play a crucial role. The India cement market faces competition from alternative building materials, such as steel and wood, which is preferred in specific construction scenarios. Builders and developers might choose alternative materials based on factors like ease of use, cost, or environmental considerations, impacting the demand for cement. Increased awareness of environmental sustainability is influencing decision-making in the construction industry. Cement production is energy-intensive and contributes to carbon emissions. Environmental concerns and the carbon footprint associated with cement production lead to a shift towards more sustainable and eco-friendly building materials, affecting the demand for traditional cement. The construction industry in India exhibits variations in terms of quality standards and practices. In some cases, there is a need for improved training and adherence to best practices to ensure the effective use of cement. Issues related to inconsistent construction practices affect the perception and acceptance of cement in the market.

India Cement Market Segment Analysis

By Type, Portland Cement plays a dominant role in the India cement market, accounting for approximately 60% of the market share. It is the most commonly used type of cement thanks to its versatility, strength, and durability, making it suitable for a wide range of construction applications including residential, commercial, and infrastructural projects. Portland Cement is essential for the construction of roads, bridges, and dams, as well as urban development projects, driving the growth of India's real estate and construction sectors. Its widespread availability and reliable performance contribute significantly to meeting the country's growing demand for infrastructure development and modernization, thereby playing a crucial role in supporting India's economic growth and development.

Based on End-User, the market is segmented into Builders and Contractors, Individual Home Builders, and Government and Public Sector. Builders and Contractors is expected to hold the largest India Cement Market share over the forecast period. The Builders and Contractors segment in the India cement market refers to a key category of stakeholders involved in the construction industry. This segment includes individuals, firms, or entities engaged in building and construction activities. Builders and contractors play a pivotal role in the procurement, planning, and execution of construction projects, making them significant consumers of cement. Builders and contractors are responsible for the execution of construction projects. This includes tasks such as project planning, material procurement, labor management, and overseeing the entire construction process. Builders and contractors are bulk consumers of cement, as the material is a fundamental component in various construction applications, which drives the India Cement market growth. The volume of cement consumed by this segment is substantial and directly linked to the scale and frequency of their construction projects.

India Cement Market Regional Insight

Pioneering Infrastructure Growth with Unstoppable Momentum to boost India Cement Market growth

As the second-largest global cement producer, India commands over 8% of the world's installed capacity, showcasing its immense potential for growth in the infrastructure and construction sectors. With a favorable outlook, the India cement industry is poised to reap substantial benefits from India's developmental drive. Driven by increasing rural housing demands, the consumption of cement in India has witnessed consistent growth, fueled by its affordability in terms of INR/kg, making it an accessible choice. The industrial sector, rebounding robustly from the pandemic shock, stands as a key catalyst for cement industry demand. This resurgence positions the sector for long-term growth, presenting a compelling case for increased cement demand, which drives the India Cement Market growth.

Comprising a total of 210 large cement plants, India's cement landscape is concentrated in key regions, including Andhra Pradesh, Rajasthan, and Tamil Nadu, which account for 77 of these facilities. Southern India leads the pack, housing approximately 32% of the nation's cement production capacity, while the North, Central, West, and East regions contribute 20%, 13%, 15%, and 20% respectively.

According to the estimate of the National Council for Cement and Building Materials (NCCBM), India’s cement industry is expected to add 80 million tonne capacity by 2025. Being the second largest cement producer in the world after China, India contributes over 8 per cent to the global installed capacity in cement production. India has potentially rich deposits of limestones in different regions of the country essentially required for cement production.

India Cement Market Scope: Inquire before buying

| India Cement Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | USD 292.91 Mn Tons |

| Forecast Period 2024 to 2030 CAGR: | 5.51% | Market Size in 2030: | USD 426.37 Mn Tons |

| Segments Covered: | by Type | Portland Blended Others |

|

| by Application | Residential Commercial Infrastructure Others |

||

India Cement Producer Include:

1. Ultratech Cement

2. Ambuja Cement

3. ACC Limited

4. Shree Cement Limited

5. Dalmia Bharat

6. Birla Corporation Limited

7. India Cement Limited

8. The Ramco Cement Limited

9. NU Vista Limited

10. Raymond Cement Industries

11. Heidelberg Cement Indian Limited

12. Cement Corporation of Indian

13. Aditya Cement

14. Deccan Cement Limited

15. J.K. Cement Limited

16. Others

Frequently asked Questions:

1. Why is the infrastructure industry crucial for India's economic growth?

Ans: The infrastructure industry in India is crucial as it fosters the expansion of various sectors like real estate and construction, contributing significantly to economic growth.

2. What does the infrastructure sector encompass?

Ans: The infrastructure sector includes the provision of utilities, construction of bridges and dams, the building of roads, and the improvement of metropolitan facilities.

3. What are the key drivers of the India Cement Market?

Ans: Infrastructure development, government initiatives like NIPP and Bharatmala, and housing schemes such as PMAY are key drivers of the India Cement Market.

4. What challenges does the India Cement Market face in terms of price sensitivity?

Ans: Price sensitivity, affordability concerns, and competition from alternative building materials can restrain the growth of the India Cement Market.

5. Who are the major consumers in the India Cement Market based on end-users?

Ans: Builders and Contractors are expected to hold the largest share, playing a pivotal role in the procurement, planning, and execution of construction projects.