In Vitro Diagnostics Quality Control Market Size by Product And Service, Technology, End User, Manufacturer Type, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

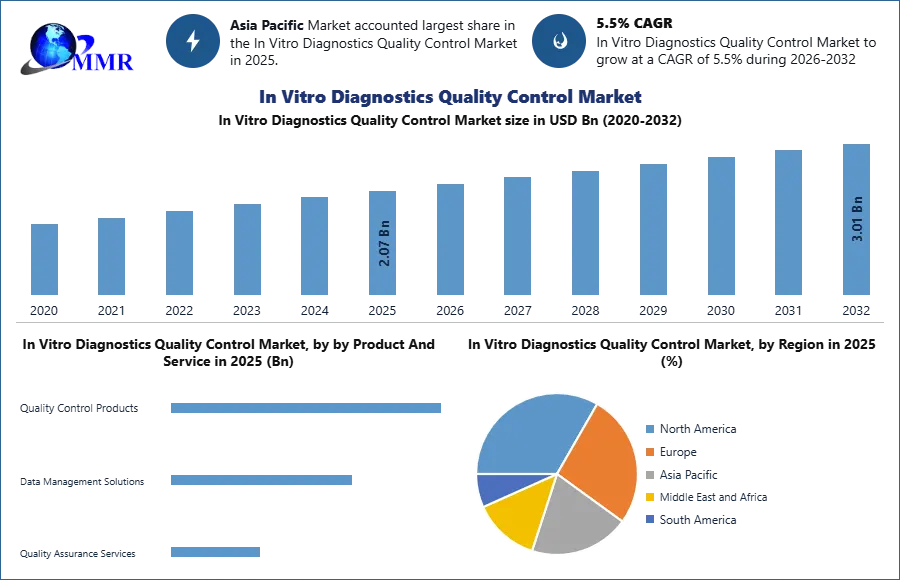

In Vitro Diagnostics Quality Control Market was valued at USD 2.07 Bn in 2025 and is expected to reach USD 3.01 Bn by 2032, growing at a CAGR of 5.5% during the forecast period.

Global In Vitro Diagnostics Quality Control Market Overview:

In Vitro Diagnostics (IVD) is a crucial and rapidly growing component of the global healthcare system, adding value to patients, medical professionals, and the industry while also improving population well-being. IVD quality controls are samples/materials that are used to verify the dependability of the IVD testing system in order to assure the correctness of test findings and to assess the influence of factors such as environmental conditions and operator performance on test results.

In Vitro Diagnostics Quality Control market's growth include an increase in the global incidence of infectious illnesses, HIV, and malignancies, which demand innovative diagnostic methods for effective treatment and quality controls to monitor their performance. According to the Joint United Nations Programme on HIV and AIDS (UNAIDS), 24.5 million HIV patients globally received antiretroviral medication in 2019. Likewise, greater government involvement in controlling infectious disease outbreaks, as well as an increase in demand for quality evaluation support and fast diagnosis systems, are anticipated to contribute to the global In Vitro Diagnostics Quality Control market's growth during the forecast period.

The existence of supportive regulatory authorities and a rising number of licensed clinical laboratories globally are expected to be significant drivers driving In Vitro Diagnostics Quality Control market growth during the forecast period. Diagnostic research labs are experiencing rapid evolution due to the increasing prevalence of chronic conditions, such as diabetes, Cardiovascular Diseases (CVDs), and infectious diseases. Many private and governmental laboratories are going through laboratory certification procedures in order to fulfill industry standards, increase procedural volume, and attract more patients. CLIA-accredited laboratories are eligible for Medicare and Medicaid payments.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

In Vitro Diagnostics Quality Control Market Dynamics:

Growing authorized clinical laboratories across the globe

The growing global burden of various diseases has resulted in an increase in the number of laboratory tests. To fulfill this need, the number of laboratories in the public and commercial sectors has increased rapidly. With the development of the COVID-19 pandemic in December 2019, the demand for diagnostic testing has grown. Many government agencies have established additional laboratories in response to the outbreak and to increase laboratory testing capacity.

In most countries, clinical laboratories must get regulatory body certification before performing diagnostic tests. However, certification to ISO 15189:2012 and other comparable standards is becoming essential in a number of countries. Authorities analyze a laboratory's quality system and competency based on specified requirements during the accreditation procedure. European nations such as Belgium, France, Hungary, Ireland, and Lithuania require certification for numerous laboratory tests, although Finland, the Netherlands, Sweden, Switzerland, and the United Kingdom have nearly completed clinical laboratory certification.

High costs of Quality Control (QC) systems and additional expenses

Installing a QC process in a clinical laboratory necessitates substantial expenditure. Laboratories must also keep committed employees on hand to administer the QC system. Also, regardless of the number of tests completed, QC procedures entail equal expenses. As a result, the expense of implementing QC processes is prohibitively expensive for clinical laboratories that perform limited quantities of diagnostic tests. This, along with economic restrictions in many hospitals and laboratories in both developed and emerging countries, is expected to result in a decrease in the adoption of In Vitro Diagnostics Quality Control market

In addition, the expense of data management solutions to handle QC data and QA services for independent diagnostic test assessment raises the total cost for end users. Small hospitals and laboratories may be unable to handle the higher expenditures even after deploying data management technologies.

Increasing need for multi-analyte controls

Technological developments have resulted in the creation of a new type of multi-analyte and multi-instrument controllers. These unique controls combine many instrument-specific controls into a single control, allowing clinical laboratories to save money and significantly reduce the time required for QC operations.

Multi-analyte controls, which may be utilized with numerous reagents and devices, are important in screening and diagnostic operations. Several multi-analyte controls are currently available on the market, including Liquichek Tumor Marker Control (Bio-Rad Laboratories), Acusera Infectious Disease (Serology) Controls (Randox Laboratories), AcroMetrix Multi-Analyte Controls—Transplant (Thermo Fisher Scientific), and ACCURUN 1 Series 4400 Multi-Analyte Positive Control (Accura) (SeraCare Life Sciences). Previously, laboratories had to keep more than thirty unique controls in order to execute QC operations; however, with the advancement of multi-analyte controls, clinical laboratories can now provide reliable and exact test findings with only one or two multi-analytes.

Multi-analyte controls on the market for immunoassay testing assist laboratories in performing QC tests for fifty or more parameters in the same blood, including cardiac and tumor indicators, hormones, therapeutic medicines, renal functions, and vitamins. Additionally, these controls do not need to be updated with reagent batches, allowing for long-term QC monitoring. The growing popularity of these controls is thus expected to continue providing considerable growth opportunities for IVD quality control market players.

Increasingly complicated regulatory procedure

IVD organizations have experienced challenges in recent years as a result of an increasingly complicated regulatory procedure. For more than two decades, the FDA has stressed its regulatory jurisdiction over LDTs and associated goods while exercising enforcement discretion over such tests. However, in recent years, the FDA has stated that further regulation of LDTs and related devices is required, and the agency intends to produce a guideline paper on the subject. The Quality System Rule (QSR), 21 CFR Part 820, and the labeling regulation, 21 CFR 809.10, apply to both tested and unassayed QC items.

The FDA's standards, notably for 510(k) notifications, have grown in recent years, necessitating more data and information than previously. This move, which results in unexpected premarket submission requirements, is particularly detrimental to IVD producers that require 510(k) approval.

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 11 March 2026 | Precedence Research / bioMérieux | BioMérieux announced the commercial expansion of its GENE-UP® PRO HRM, the first DNA-based molecular test designed to detect heat-resistant molds. | This development provides laboratories with a high-precision molecular reference tool, reducing diagnostic errors in industrial and clinical microbiology settings through rapid molecular-level identification. |

| 23 February 2026 | Fortune Business Insights | Industry data confirmed that the independent/commercial laboratories segment reached a significant growth milestone, fueled by the adoption of automated multi-analyte QC solutions. | The shift toward centralized, automated QC platforms allows standalone labs to maintain strict quality compliance while managing high-throughput testing volumes for chronic diseases. |

| 01 July 2025 | Randox Laboratories Ltd. | Randox Laboratories launched a new RIQAS External Quality Assessment (EQA) program specifically for pre-eclampsia testing. | This initiative enhances global diagnostic standardization for maternal health, enabling laboratories to benchmark performance and ensure the accuracy of life-critical biomarker assays. |

| 15 June 2025 | Revvity, Inc. | Revvity introduced three new Mimix™ reference standards tailored for Next-Generation Sequencing (NGS) and droplet digital PCR (ddPCR) in vitro diagnostic applications. | These FDA-aligned standards allow laboratories to minimize assay variability and improve test performance monitoring for complex somatic mutations in human genomic DNA. |

| 28 April 2025 | Roche / Universitätsklinikum Heidelberg | Roche announced the launch of a CE-marked Chest Pain Triage algorithm, an IVD medical device integrated with existing diagnostic hardware. | By combining high-sensitivity troponin assays with algorithmic quality controls, the system accelerates clinical decision-making in cardiac care while maintaining rigorous diagnostic safety standards. |

| 14 January 2025 | Bio-Rad Laboratories, Inc. | Bio-Rad launched the Unity Next Peer QC software platform, designed to provide labs with real-time peer comparison and centralized reporting. | The platform enables instant detection of systematic errors, allowing high-throughput laboratories to perform rapid root-cause analysis and avoid costly repeat testing of patient samples. |

In Vitro Diagnostics Quality Control Market Segment Analysis:

In 2025, the Product and Service segment of the In Vitro Diagnostics Quality Control Market is primarily driven by strong demand for Quality Control Products. These products are essential for ensuring the accuracy, reliability, and consistency of diagnostic test results across clinical laboratories and hospitals. Laboratories increasingly rely on multi-analyte control materials and third-party quality controls to meet regulatory requirements and maintain testing standards. Data Management Solutions are also witnessing increasing adoption as laboratories implement digital platforms to track quality metrics, automate reporting, and improve compliance with regulatory guidelines. Meanwhile, Quality Assurance Services are gaining importance as healthcare institutions outsource validation, proficiency testing, and compliance management to specialized providers, ensuring consistent laboratory performance and operational efficiency.

Based on Technology, Clinical Chemistry and Immunochemistry represent the most widely used technologies in 2025 due to their extensive application in routine diagnostic testing, including metabolic panels, hormone analysis, and infectious disease detection. Molecular Diagnostics is emerging as the fastest-growing technology segment, driven by the increasing demand for genetic testing, infectious disease detection, and personalized medicine. Technologies such as PCR-based assays require stringent quality control measures to maintain diagnostic accuracy. Microbiology and Hematology technologies also contribute significantly to market demand, particularly in hospital laboratories managing infection monitoring and blood analysis. Coagulation/Hemostasis testing continues to grow steadily due to the rising prevalence of cardiovascular diseases and blood disorders, increasing the need for reliable diagnostic quality control solutions.

Based on End User, Clinical Laboratories dominate the market in 2025 as they conduct a large volume of diagnostic tests daily and require strict quality control procedures to ensure accurate results. Hospitals also represent a major segment, driven by the integration of advanced diagnostic testing within hospital laboratories and the need for continuous monitoring of patient health parameters. Academic and Research Institutes contribute to market growth through increasing research activities involving diagnostic technologies and biomarker validation. Home-care settings are gradually adopting diagnostic quality control solutions as point-of-care testing expands, particularly for chronic disease monitoring. Other end users, including specialty diagnostic centers and public health laboratories, also contribute to steady demand for quality control products and services.

In Vitro Diagnostics Quality Control Market Regional Insights:

In Vitro Diagnostics Quality Control Market Scope: Inquire before buying

| In Vitro Diagnostics Quality Control Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 2.07 USD Bn |

| Forecast Period 2026-2032 CAGR: | 5.5% | Market Size in 2032: | 3.01 USD Bn |

| Segments Covered: | by Product And Service | Quality Control Products Data Management Solutions Quality Assurance Services |

|

| By Technology | Immunochemistry Clinical Chemistry Molecular Diagnostics Microbiology Hematology Coagulation / Hemostasis Other Technologies |

||

| By End User | Hospitals Clinical Laboratories Academic and Research Institutes Home-care Other End Users |

||

| By Manufacturer Type | IVD Instrument Manufacturers Third Party Quality Control Manufacturers Independent Third Party Quality Controls Instrument Specific Third Party Quality Controls |

||

In Vitro Diagnostics Quality Control Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

In Vitro Diagnostics Quality Control Market, Key Players

1. Bio-Rad Laboratories, Inc.

2. Randox Laboratories Ltd.

3. Thermo Fisher Scientific, Inc.

4. LGC Limited

5. Abbott Laboratories

6. Roche Diagnostics

7. Siemens Healthineers

8. Danaher Corporation

9. Fortress Diagnostics

10. SERO AS

11. Sysmex Corporation

12. Ortho-Clinical Diagnostics

13. Helena Laboratories Corporation

14. Quidel Corporation

15. Sun Diagnostics, LLC.

16. Seegene Inc.

17. ZeptoMetrix Corporation

18. Qnostics

19. Bio-Techne Corporation

20. Microbiologics

21. Microbix Biosystems

22. Streck, Inc.

23. Alpha-Tec Systems

24. Maine Molecular Quality Controls, Inc.

25. Grifols, S.A.