Hydrogen Aircraft Market Size by Power Source, Platform, Passenger Capacity, Ranger, Technology, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

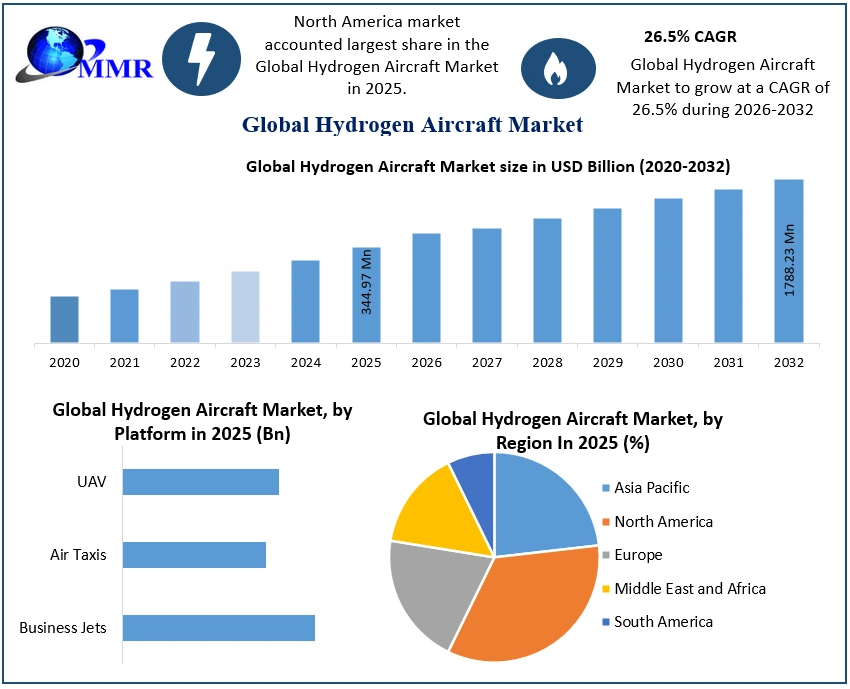

The Hydrogen Aircraft Market Market size was valued at USD 344.97 Million in 2025 and the total Hydrogen Aircraft Market revenue is expected to grow at a CAGR of 26.5% from 2025 to 2032, reaching nearly USD 1788.23 Million by 2032.

Hydrogen Aircraft Market Overview:

Hydrogen Aircraft is a type of airliner that works on Hydrogen fuel. Hydrogen Aircraft uses Hydrogen as a source for internal combustion engines or Hydrogen Cells as a fuel source. Hydrogen is high in density compound that provides a cost-efficient and environmentally friendly alternative for aviation fuel. Rising environmental concerns by governments of developed nations have propelled the demand for Hydrogen Aircraft. An increase in demand for clean fuel by the civil aviation industry and a range of benefits provided by Hydrogen Aircraft over conventional aircraft have resulted in a growth in the Hydrogen Aircraft Market.

To know about the Research Methodology :- Request Free Sample Report

Hydrogen Aircraft Market Dynamics

A report by Rocky Mountain Institute published in July states that 2.5% of the carbon emission is a result of global air travel. Increased preference for a zero-carbon environment by developed nations has resulted in a rise in demand for alternatives for fossil fuels. While Biofuels have their drawbacks, Hydrogen provides a lightweight and high-density fuel medium with nearly zero carbon footprints. An increase in the number of aviation firms investing in carbon-emission-free fuel technology has resulted in a rise in demand for Hydrogen Aircraft.

Aim to achieve near to zero dependence on fossil fuels as aviation fuel by leading aircraft manufacturing and operating firms has resulted in a rising demand for a cost-efficient alternative for aviation fuel. With strategic investment in building zero-emission commercial aircraft by leading firms like

Honeywell Aerospace, Boeing, and Airbus, demand for Aircraft that run on Hydrogen is expected to increase rapidly.

More than 100 countries came into an alliance with the aim to achieve carbon neutrality by 2050 at the Paris Climate Accord in. Countries in the European Union, UAE, Saudi Arabia, South Korea, and Canada have joined an alliance aiming for net-zero carbon emission by 2050. Increased awareness by governments across the world towards carbon emission has resulted in a rise in demand for Hydrogen Aircraft.

Increased demand for fuel-efficient and environmentally sustainable commercial aircraft has resulted in a rise in demand for aircraft that work on hydrogen. To tap this market, Airbus launched 3 new concept aircraft that have 2 hybrid hydrogen turbofan engines and holds liquid hydrogen tanks underneath their wings On September 21, . These Aircraft are considered the world’s first zero-emission commercial aircraft and work on Hydrogen as their primary source of fuel.

The rising preference for cost-efficient and easy to maintain aircraft by the aviation industry has resulted in the entry of various new players in the Hydrogen Aircraft Manufacturing market. UK-based ZeroAvia, Inc. took a successful trial of their first six-seater commercial aircraft that fully works on Hydrogen Cells. This is the world’s first commercial-size aircraft that triumphantly took hydrogen fuel cell-powered flight.

Restraints:

The high cost required for building Hydrogen fuel-based infrastructure acts as the major restraining factor here.

The need for special lightweight vacuum insulated tanks to maintain fuel below its 20 K boiling point is limiting the rapid scale adaption of Hydrogen Aircraft by the Aviation industry.

Hydrogen Aircraft Market Segment Analysis:

The Hydrogen Aircraft Market is segmented

By Power Source, Convenience in using has resulted in making Hydrogen Fuel Cell dominate the power source segment in the Hydrogen Aircraft Market. More than 45% of the concept Hydrogen Aircraft built have Hydrogen Fuel Cell as its source. Increased expenditure on research for building hydrogen fuel-efficient engine that follows combustion by Lockheed Martin and other firms is observed.

By Platform, The rising preference for cost-efficient drones by the military and commercial sectors has resulted in a rapid growth in the Hydrogen operated UAVs in the forecasted period. UAVs that act as miniature Hydrogen Aircraft have observed a 5.5% increase in demand from the commercial sector in the year 2025.

By Passenger Capacity, Increased preference for cost-efficient aircrafts having passenger capacity in the range of 5-10 has forecasted to dominate the

Hydrogen Aircraft Market in the forecasted period. Hydrogen Aircraft having a capacity of 5-10 Passengers have observed an advanced booking of 150 aircraft from the Lockheed Martin Corporation by the US Air Force in 2025.

By Range, Increased demand for inter-city air travel carriers by people living in developed nations has resulted in medium-range Hydrogen Aircraft dominate the market in the forecasted period. A rise in demand for environmentally efficient air carriers has resulted in a 4% increase in demand for Hydrogen Aircraft having a range of 500 km-1500 km. by the top management officials of firms present in Europe.

By Technology, The increased research on the use of Hydrogen as an alternative for aviation fuel has resulted in the development of fully hydrogen-powered aircraft that is forecasted to dominate the civil aviation market by 2050. The rising preference for Hydrogen Fuel as a power source for aircraft has resulted in a 4.5% increase in demand for Fully Hydrogen-powered Aircraft by defense sectors of the US, Israel, and Japan in the year 2025.

The rising preference for environment-friendly aeroplanes has resulted in a 15% increase in the orders received by UK-based startup ZeroAvia in 2025, to manufacture Hydrogen Aircraft having a capacity of 4-10 Passengers and a range less than 500 Km. An increase in demand for Fuel-efficient airliners by the US defense sector has resulted in a pre-order for 25 Hydrogen Aircraft to Airbus having a range of 500 Km to 1500 Km.

Increased focus on a greener future by the global civil aviation industry has resulted in an 8.5% increase in demand for Hydrogen Aircraft in 2025 having a range of 1500 Km to 4000 Km. The rising environmental concerns by different governments have resulted in a rise in demand for Hydrogen Aircraft having long-range.

| Global Hydrogen Aircraft Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 344.97 USD Mn |

| Forecast Period 2026-2032 CAGR: | 26.5% | Market Size in 2032: | 1788.2 USD Mn |

| Segments Covered: | By Power Source | Hydrogen Combustion Hydrogen Fuel Cell |

|

| By Technology | Fully Hydrogen-Powered Aircraft Hybrid Electric Aircraft |

||

| By Platform | Urban Air Mobility EVTOL Unmanned Aerial Vehicle Business Jets Others |

||

| By Range | Up to 1000 km 1000 km to 2000 km Over 2000 km |

||

| By Passenger Capacity | Up to 4 Passengers 5 to 10 Passengers More than 10 Passengers |

||

| By Application | Commercial Military Cargo |

||

Hydrogen Aircraft Market Regional Insights

The presence of an established commercial aviation sector has resulted in making North America the biggest manufacturer and consumer of Hydrogen Aircraft. Re-entry of the USA in Paris Agreement in January has projected double-digit growth in the North American Hydrogen Aircraft Market in the forecasted period.

The established goal to reach carbon neutrality by 2050 has resulted in an 8.5% increase in the orders placed for Hydrogen Aircraft to Boeing and Airbus by different governments present in Europe. Increased preference for air carriers that leaves little to zero carbon footprints has resulted in a 6% increase in demand for Hydrogen Aircraft by corporations like Netflix, JP Morgan Chase, and Microsoft that are part of the Sustainable Aviation Buyers Alliance.

The Asia-Pacific is showing a low growth rate which is concentrated mostly in environmentally-conscious countries like Japan, South Korea, and Bhutan. The Middle East and Africa’s region is showing a growth rate of 4.8% in demand for Hydrogen Aircraft in as compared to the first decade of the 21st Century. The presence of a big aeronautical industry in countries like Israel and the zero-carbon emission goal by governments of UAE and Saudi Arabia has projected an increased growth in the Hydrogen Aircraft Market present in this region in the forecasted period.

South American Market is showing a low growth rate, the reason for which is the absence of strong aviation industry in this region.

The objective of the report is to present a comprehensive analysis of the Hydrogen Aircraft Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Hydrogen Aircraft Market dynamics, structure by analyzing the market segments and Project the Hydrogen Aircraft Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Hydrogen Aircraft Market make the report investor’s guide.

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 26 March 2026 | ICAO / World Economic Forum | The Global Aviation Sustainability Outlook 2026 was released, establishing a unified industry framework for scaling hydrogen-powered flight and infrastructure. | The framework accelerates capital investment and provides regulatory clarity for manufacturers moving from prototypes to commercialization. |

| 22 December 2025 | ZeroAvia | ZeroAvia signed a definitive agreement with the Korean Atomic Energy Research Institute (KAERI) to develop advanced composite liquid hydrogen storage systems. | This collaboration enhances fuel density and aircraft range, critical for extending hydrogen propulsion to large narrow-body aircraft. |

| 15 October 2025 | ZeroAvia | The company secured a €21 million European Union grant to implement the world’s first network of hydrogen-powered commercial aircraft in Norway. | This funding establishes operational viability for regional routes and validates hydrogen refueling infrastructure in a real-world aviation ecosystem. |

| 18 June 2025 | Airbus & MTU Aero Engines | Airbus and MTU Aero Engines signed a Memorandum of Understanding (MoU) to jointly develop hydrogen fuel cell propulsion for the ZEROe project. | The partnership combines heavy-duty engine expertise with airframe design to reach the 2035 entry-into-service target for zero-emission aircraft. |

| 14 May 2025 | RVL Aviation | RVL Aviation announced the deployment of the first ZeroAvia ZA600-powered Cessna Caravan for commercial hydrogen-electric freighter operations. | This marks the transition of hydrogen technology into revenue-generating cargo services, proving the reliability and cost-efficiency of fuel cell powertrains. |

| 25 March 2025 | Airbus | During the 2025 Airbus Summit, the company officially selected hydrogen fuel cell technology as the primary propulsion method for its future zero-emission aircraft. | This strategic pivot streamlines R&D resources toward fuel cell stacks, moving away from direct combustion for its initial commercial rollout. |

Hydrogen Aircraft Market Scope: Inquire before buying

Hydrogen Aircraft Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Hydrogen Aircraft Market, Key Players

- Airbus S.A.S.

- Boeing Co.

- Embraer S.A.

- BAE Systems plc

- Bell Helicopter (Textron Inc.)

- Israel Aerospace Industries (IAI)

- GKN Aerospace

- Karem Aircraft

- Bye Aerospace

- Volta Volare

- DeLorean Aerospace

- ZeroAvia Inc.

- H2FLY GmbH

- Beyond Aero

- Stralis Aircraft

- Sirius Aviation

- Ecojet

- Aerodelft

- Apus Group

- Flyka

- Pipistrel d.o.o.

- Skai (Alaka’i Technologies)

- Urban Aeronautics Ltd.