Humanoid Robot Sensors Market Analysis (2025–2032): AI-Driven Perception Systems, Sensor Density Expansion, Competitive Landscape, and Asia Pacific Manufacturing Dominance

Overview

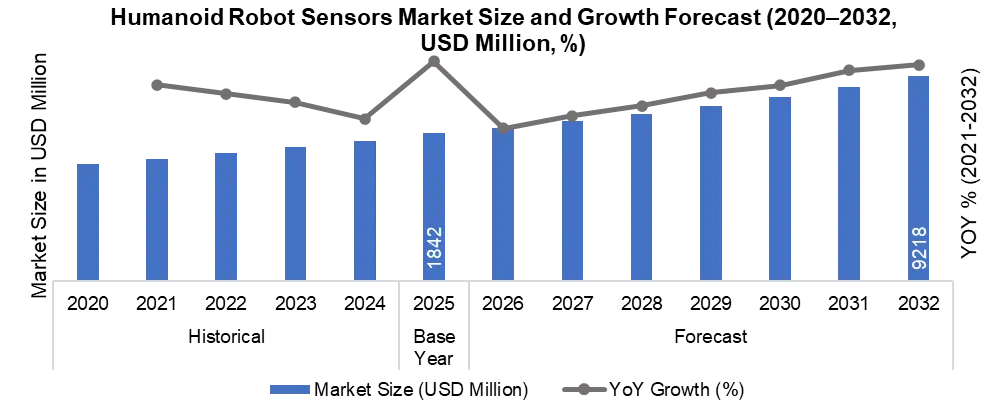

Global Humanoid Robot Sensors Market Size & Growth Outlook

The Global Humanoid Robot Sensors Market was valued USD 1,842 Million in 2025 and is projected to reach around USD 9,218 Million by 2032, growing at a CAGR of 25.8% during 2026–2032.

Global Humanoid Robot Sensors Market Overview

The humanoid robot sensors market represents the core intelligence layer of humanoid robotics systems, enabling perception, navigation, manipulation, and safe human interaction. The market is driven by AI-enabled sensing technologies, increasing robot deployment, and rising sensor density per robot.

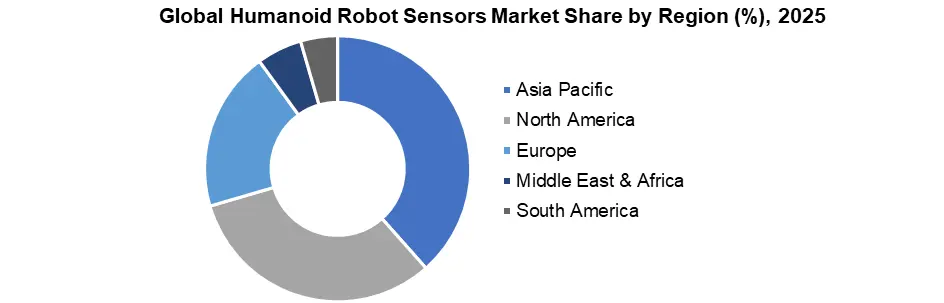

Asia Pacific dominated the market in 2025 due to strong manufacturing capabilities, while North America leads in technological innovation. Vision sensors hold the highest share, while tactile sensors are the fastest-growing segment.

Global Humanoid Robot Sensors Market Key Highlights

| Market Parameter | Value / Insight | Trend |

| Global Market Size (2025) | USD 1,842 Million | ↑ Strong Growth |

| Projected Market Size (2032) | USD 9,218 Million | ↑ Rapid Expansion |

| Forecast CAGR (2026–2032) | 25.80% | ↑ Accelerating |

| Fastest Growing Region | North America | ↑ Innovation Driven |

| Largest Regional Market (2025) | Asia Pacific (39.2% Share) | ↑ Dominant |

| Leading Manufacturing Countries | China, Japan, South Korea | ↑ Consolidating |

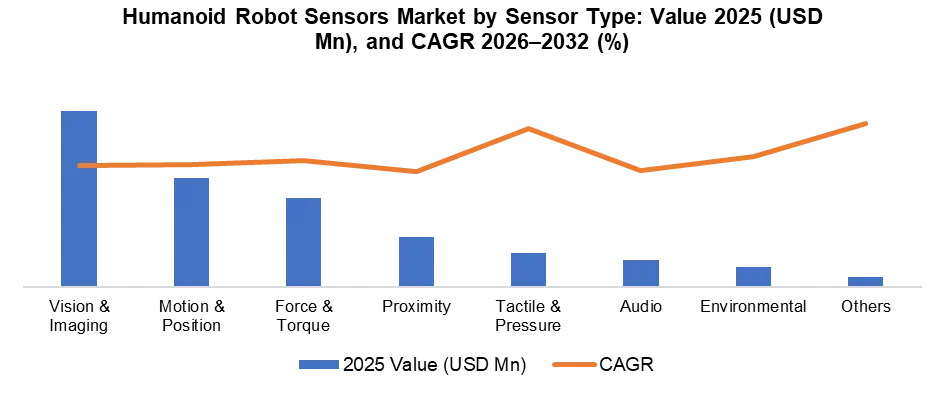

| Top Sensor Segment | Vision & Imaging Sensors (34.2%) | ↑ Structural |

| Fastest Growing Segment | Tactile & Pressure Sensors | ↑ Emerging |

| Avg Sensors per Robot | 40–80 Units | ↑ Increasing Density |

| Key Technology Trend | AI Sensor Fusion | ↑ Transformational |

To know about the Research Methodology :- Request Free Sample Report

Sensor Type and Volume Usage per Humanoid Robot

| Sensor Type | Average Units per Robot | Usage Role |

| Vision & Imaging Sensors | 4–8 | Object detection, navigation, perception |

| Motion & Position Sensors (IMU, Encoders) | 10–20 | Balance, movement, orientation |

| Force & Torque Sensors | 6–12 | Precision control, grip, interaction |

| Proximity Sensors | 4–10 | Obstacle detection, safety |

| Tactile & Pressure Sensors | 10–20 | Touch sensing, human interaction |

| Audio Sensors | 2–6 | Voice recognition, communication |

| Environmental Sensors | 2–5 | Temperature, safety monitoring |

| Total Sensors per Robot | 40–80 Units | Integrated sensing system |

Sensor Ecosystem in Humanoid Robotics

The sensor ecosystem in humanoid robotics market forms the core intelligence layer that enables robots to perceive, analyze, and interact with their surroundings. It includes key humanoid robot sensors such as vision and imaging sensors (cameras, LiDAR), motion and position sensors (IMU, gyroscopes, encoders), and force-torque and tactile sensors for human-safe interaction. These advanced robotics sensors generate real-time data, supporting applications like navigation, object recognition, and autonomous decision-making. The rising demand for AI-powered humanoid robots and smart sensing technologies is accelerating the adoption of high-performance sensors across industrial and service robotics.

The ecosystem is supported by semiconductor components, MEMS sensors, and optical technologies, ensuring high precision and reliability. The increasing use of sensor fusion in humanoid robots, combining multiple sensing technologies, enhances accuracy, safety, and operational efficiency. Additionally, growing demand for human-centric robotics, AI-enabled perception systems, and next-generation robotics sensors is driving innovation in tactile and force sensing technologies. As sensor density in humanoid robots continues to increase, this ecosystem is becoming a key growth driver in the global humanoid robot sensors market, influencing scalability, performance, and future automation trends.

Technology Innovation in Humanoid Robot Sensors Market

The humanoid robot sensors market is undergoing rapid transformation driven by advancements in AI-enabled sensing technologies, sensor fusion, and edge computing. The integration of next-generation robotics sensors, including vision systems, LiDAR, IMU, and tactile sensors, is enabling humanoid robots to achieve real-time perception, precision control, and autonomous decision-making.

Innovations in MEMS-based sensors, low-power electronics, and high-resolution imaging systems are significantly improving sensor accuracy, latency, and energy efficiency, making robots more adaptable to complex and unstructured environments. Additionally, the development of AI-powered sensor fusion platforms is allowing multiple sensor inputs to be processed simultaneously, enhancing operational safety, reliability, and performance. As a result, advanced humanoid robot sensors are becoming a critical differentiator in robot scalability, deployment efficiency, and industrial automation applications.

Humanoid Robot Sensors Market Key Trends

1. Adoption of AI-Powered Sensor Fusion Systems

The increasing use of sensor fusion in humanoid robots is enabling seamless integration of vision, motion, and tactile sensors, improving accuracy, real-time analytics, and decision-making capabilities. This trend is critical for enhancing autonomous robotics and intelligent perception systems.

2. Rising Demand for Advanced Vision and Imaging Sensors

The demand for vision sensors in humanoid robots, including 3D cameras, LiDAR, and depth sensing technologies, is expanding rapidly. These AI-driven imaging systems are essential for object detection, navigation, and human interaction, making them the largest segment in the robotics sensors market.

3. Growth of Tactile and Force Sensing Technologies

The shift toward human-centric robotics is driving adoption of tactile sensors and force-torque sensors, enabling robots to perform delicate and precise tasks. This trend is particularly important in healthcare robotics, service robots, and collaborative automation.

4. Miniaturization and Low-Power Sensor Innovation

Advancements in MEMS sensors, compact electronics, and energy-efficient designs are leading to the development of miniaturized humanoid robot sensors. These innovations support higher sensor density, reduced power consumption, and improved robot mobility, enhancing overall system efficiency.

5. Integration of Edge AI and Real-Time Processing

The integration of edge AI in robotics sensors is enabling real-time data processing and reduced latency, eliminating dependence on cloud computing. This trend enhances robot autonomy, response time, and operational reliability, especially in industrial and defense applications.

Humanoid Robot Sensors Market Recent Developments 2025-2026

| Company | Year | Development | Impact |

| RoboSense | 2025 | Launched AI-driven LiDAR sensors and humanoid robotics platform | Strengthens sensor fusion and perception capabilities in humanoid robots |

| Sanctuary AI | 2025 | Integrated advanced tactile sensors in Phoenix humanoid robot | Improves precision manipulation and human interaction accuracy |

| Nature Sensors Research | 2026 | Developed SuperTac multimodal tactile sensor with ~94% accuracy | Enables human-like touch perception and material detection |

| XELA Robotics | 2026 | Introduced uSkin 3D tactile sensors with full-hand coverage | Enhances dexterity and multi-surface sensing capability |

| Bosch | 2026 | Launched MEMS-based pressure + IMU sensors detecting ultra-light touch | Improves sensitivity and human-safe interaction |

| AIDIN Robotics | 2026 | Developed next-gen tactile sensors mimicking human touch | Supports advanced humanoid interaction and sensing realism |

| Figure AI | 2025 | Introduced next-gen sensor suite with 60% wider vision and low latency | Enhances real-time perception and robotic performance |

Humanoid Robot Sensors Market Segment Analysis

The humanoid robot sensors market by sensor type is segmented into vision and imaging sensors, motion and position sensors, force and torque sensors, proximity sensors, tactile and pressure sensors, audio sensors, and environmental sensors. Among these, vision and imaging sensors dominate the market, accounting for approximately 34.2% share in 2025, driven by rising demand for AI-powered perception, object recognition, and autonomous navigation. Technologies such as 3D cameras and LiDAR sensors are widely adopted in advanced humanoid robotics.

The motion and position sensors segment, including IMU, gyroscopes, and encoders, plays a critical role in ensuring balance, stability, and movement accuracy. Meanwhile, force and torque sensors are high-value components used for precision control and safe human interaction. The demand for tactile and pressure sensors is growing rapidly due to increasing focus on human-centric robotics and touch-based interaction. Additionally, proximity, audio, and environmental sensors support safety, communication, and environmental awareness, making them essential for next-generation humanoid robot sensor integration and AI-driven automation systems.

Humanoid Robot Sensors Market Regional Analysis

• Asia Pacific dominates the humanoid robot sensors market in 2025, accounting for 39.34% market share, driven by strong robotics manufacturing, semiconductor ecosystem, and cost-efficient sensor production. China leads in robotics sensor manufacturing and LiDAR systems, while Japan excels in precision sensors and advanced humanoid robotics, and South Korea supports MEMS and imaging sensors. India is emerging with growing investments in AI-powered robotics and automation technologies.

• North America is a key innovation hub, led by the United States and Canada, with strong capabilities in AI-enabled sensors, vision systems, and edge AI technologies. The region focuses on high-performance humanoid robot sensors, with increasing adoption in industrial automation, defense robotics, and healthcare applications.

• Europe holds a significant share, driven by Germany, France, the UK, and Sweden, with leadership in precision engineering, industrial sensors, and robotics integration. Strong regulatory standards and safety compliance support the adoption of advanced robotics sensing technologies.

• Middle East & Africa is an emerging market, with UAE and Saudi Arabia investing in smart cities, AI-driven robotics, and intelligent sensor technologies, supporting gradual adoption of humanoid robot sensors.

• South America is witnessing steady growth, led by Brazil and Mexico, driven by increasing industrial automation, robotics deployment, and demand for advanced humanoid robot sensors.

Humanoid Robot Sensors Market Competitive Analysis

The humanoid robot sensors market competitive landscape is moderately consolidated, with key players competing on technology innovation, sensor accuracy, and AI integration capabilities. Leading companies such as Sony, Bosch, Honeywell, Intel, and ATI Industrial Automation dominate key segments including vision sensors, MEMS sensors, and force-torque sensors, strengthening their position in the advanced robotics sensors market.

The market is driven by strategic partnerships between sensor manufacturers and humanoid robot OEMs, enabling integration of AI-powered sensor systems, LiDAR, and sensor fusion technologies. Companies are increasingly focusing on R&D investments, miniaturization, and low-power sensor development to enhance performance, efficiency, and scalability. Additionally, emerging players from China and the United States are intensifying competition by offering cost-effective humanoid robot sensors and AI-driven sensing solutions, accelerating innovation and expanding the global humanoid robot sensors market.

Humanoid Robot Sensors Market Scope: Inquire before buying

Competitive Landscape Heatmap: Humanoid Robot Sensors Market (Top Players)

Legend: VH = Very High | H = High | M = Medium | L = Low

| Company | AI/Software | Sensor Hardware | Supply Chain | Capital Access | China Exposure | Commercial Stage |

| NVIDIA | VH | H | VH | VH | M | VH |

| Intel | VH | H | H | VH | M | VH |

| Sony | H | VH | VH | H | M | VH |

| Bosch | M | VH | VH | H | M | VH |

| Honeywell | M | VH | H | H | L | H |

| ATI (Novanta) | L | VH | H | M | L | H |

| Keyence | M | VH | H | VH | L | VH |

| Omron | M | H | H | H | M | H |

| Samsung | H | VH | VH | VH | H | VH |

| TSMC | H | VH | VH | H | VH | VH |

| Robosense | M | H | VH | M | VH | H |

| Hesai | M | H | VH | M | VH | H |

| Valeo | M | H | H | M | M | H |

| Infineon | H | VH | VH | H | M | VH |

| Analog Devices | H | VH | H | H | L | VH |

Humanoid Robot Sensors Market Future Opportunity

The humanoid robot sensors market presents significant growth opportunities driven by the rapid adoption of AI-powered robotics, automation, and human-centric machines. Increasing demand for advanced vision sensors, tactile sensors, and sensor fusion technologies is creating opportunities for innovation in AI-enabled perception systems and real-time analytics. The expansion of industrial automation, healthcare robotics, and service robots is further accelerating sensor demand. Additionally, opportunities exist in low-cost MEMS sensors, edge AI integration, and miniaturized sensor solutions, enabling scalability and mass adoption. Emerging markets, particularly in Asia Pacific and North America, offer strong potential for sensor manufacturers to expand production and technological capabilities.

Frequently Asked Questions

Q1. What is the size of the humanoid robot sensors market?

Ans: The humanoid robot sensors market was valued at USD 1,842 Million in 2025 and is projected to reach USD 9,218 Million by 2032, growing at a CAGR of 25.8%.

Q2. Which sensor type dominates the humanoid robot sensors market?

Ans: Vision and imaging sensors dominate the market with around 34% share, driven by demand for AI-powered perception, object recognition, and navigation systems.

Q3. What is the average number of sensors used in a humanoid robot?

Ans: A typical humanoid robot uses approximately 40–80 sensors, including vision, motion, force, tactile, and proximity sensors.

Q4. Which region leads the humanoid robot sensors market?

Ans: Asia Pacific leads the market, accounting for nearly 39% share in 2025, driven by strong manufacturing and semiconductor capabilities.

Q5. Which segment is expected to grow the fastest?

Ans: Tactile and pressure sensors are the fastest-growing segment due to increasing demand for human-like interaction and touch-based sensing.