Global Hepatitis B Market Size by Therapy, Product Type, End User and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

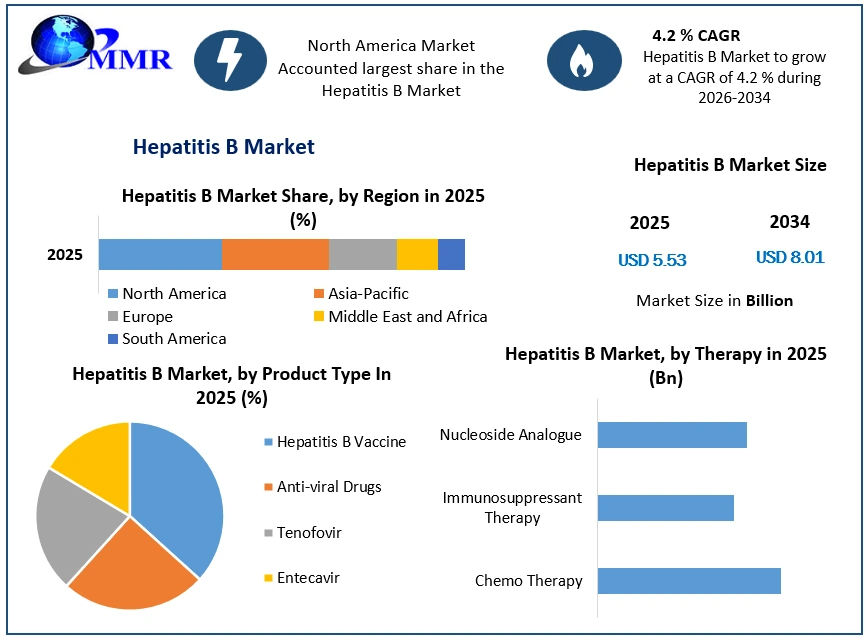

Hepatitis B Market size was valued at USD 5.53 Billion in 2025 and the total Hepatitis B Revenue is expected to grow at a CAGR of 4.2 % from 2026 to 2034, reaching nearly USD 8.01 Billion in 2034.

Hepatitis B Market Overview:

HBV is a small, double-stranded DNA virus in the family Hepadnaviridae. Serologic markers for HBV infection include HBsAg, antibodies to HBsAg (anti-HBs), immunoglobulin class M (IgM) antibodies to hepatitis B core antigen (IgM anti-HBc), and immunoglobulin class G (IgG) anti-HBc (IgG anti-HBc).

To know about the Research Methodology :- Request Free Sample Report

Across the selected countries, the mechanisms for procuring antiretroviral (ARV) drugs for HIV programs depend on the funding mechanism. Commodities funded by government budget funds are procured by national procurement. Commodities funded by nongovernment entities are done outside the national procurement system. The GFATM procurements are done through its online procurement system (Wambo.org), and the U.S. President’s Emergency Plan for AIDS Relief (PEPFAR) procurements through PEPFAR’s procurement service agent that delivers to the in-county central warehouses.

Three out of six countries, namely India, Rwanda, and Uganda, fall under the bucket of publicly coordinated HBV programs. The countries have centralized financing with services being delivered free of charge to patients. Commodities in the countries are centrally procured and distributed to facilities, which has resulted in low prices of TDF between US$2.60 – 4.60 per pack. The Rwanda Medical Supply (RMS) Ltd is responsible for procuring diagnostic and treatment commodities in the country and an annual quantification exercise is conducted to inform national procurement. RMS pools the drug requirement at the program level and procures via an open tender which is awarded for one year with the possibility of renewal twice.

Hepatitis B market Dynamics:

Driving Factors and Opportunities in the Global Hepatitis B Vaccine Market

The rise in HBV diagnosis incidence increased the number of tests performed as well as improved disease awareness and the continuation of strong screening initiatives. The increasing number of hepatitis B cases globally is the primary driver of hepatitis B vaccine market growth. Governments are taking initiatives to raise awareness among residents about the benefits of the hepatitis B vaccine. In addition, continued awareness of hepatitis treatment owing to collaborations and associations in major organizations and the presentation of fewer approaches to hepatitis treatment are other factors driving the market growth. Limited access to hepatitis B treatment and diagnosis in many resource-constrained settings, as well as the rising prevalence of hepatitis B infections, are expected to drive the global hepatitis B market through the forecast period. Rising awareness and affordability are two key factors that increase the rate of diagnosis before a person has advanced liver disease. Rising awareness and the development of new types of medications with higher efficacy are expected to provide a good opportunity for the global hepatitis B vaccines market.

Government Initiatives and Novel Therapies Propel Growth in Hepatitis B Vaccination Market

Rising government initiatives, policies, and awareness programs have played a significant role in promoting hepatitis b vaccination. An increased number of hepatitis B infections and deaths has significantly highlighted the importance of preventing hepatitis B infection and its associated health burdens. Various Governments have implemented numerous strategies to increase vaccine coverage including mandating hepatitis B vaccination for infants, children, and high-risk populations. Integrating the vaccine into routine immunization schedules and providing financial support for vaccination programs is expected to boost the market share.

Food and Drug Administration (FDA) has approved the supplemental new drug application (sNDA) for Vemlidy (tenofovir alafenamide) 25 mg tablets as a once-daily treatment for chronic hepatitis B virus (HBV) infection in pediatric patients 12 years of age and older with compensated liver disease. The launch of novel hepatitis medication therapies is expected to drive market expansion through the forecast period.

Regulatory Hurdles and Time Constraints In the Hepatitis B Market

Vaccines under FDA regulation undergo various rigorous review procedures by laboratories to ensure the product’s efficacy, safety, purity, and potency. Producing a vaccine around 15 years to establish its safety and efficacy. The factors contributed to such a long process arise with complexities at the time of the development process, the clinical trial process, and different regularity requirements in other regions. Processes with high time consumption contribute to additional time utilization owing to stringent regulatory policies by various administration organizations for approval, factors are expected to limit the introduction of new products by advanced technologies restraining market growth.

Hepatitis B Market Segmentation:

By End Users, the Hospitals & Retail Pharmacies sub-segment had dominated the market with a share of 70 % in 2025. The prevalence of viral hepatitis in the United States is a significant health problem, and pharmacists help. Pharmacists are uniquely positioned to raise patients' awareness of, prevent, and access treatment for severe diseases by administering vaccinations and counseling on prevention, testing, and treatment. The increasing number of private clinics in the Asia-Pacific and Latin America regions is projected to contribute to positive segment growth. Some referral hospitals provide hepatitis B surface antigen (HBsAg) testing refer eligible patients to a private lab for diagnostics, and write a drug prescription. TDF is available to patients from private hospitals/ pharmacies at US$30 per pack. Hospitals offer accessibility and convenience for individuals seeking hepatitis B vaccination through their regular visits for healthcare needs. Developed infrastructure and well-established storage facilities contribute to streamlined operations and reduce the risk of vaccine shortage and wastage in hospitals.

Hepatitis B Market Regional Insight:

North America's hepatitis B vaccine market accounted for over 38 % share in 2025 and is expected to grow at a considerable growth rate through the forecast period. The increased prevalence of hepatitis B infections coupled with the increased population at risk, including newborns, and healthcare workers among others is expected to fuel the market growth in the region. Canada considers hepatitis B, a huge concern as many people is suffering from Chronic Hepatitis B. Canada has invested in their research and drugs to manage the effluence of Hepatitis B. In Mexico, several pharmaceutical companies such as Laboratories Liomont S.A. are involved in the development and marketing of hepatitis B drugs and vaccines. But the market share for Mexico is lesser than that of its counterparts.

Growth prospects in the region are bolstered by several factors, including a high illness burden, increasing access to medicines, improved healthcare and sanitation, and more awareness about hepatitis immunization. Countries like India, China, Indonesia, and others in the South Asian economic region are constantly growing their healthcare expenditure and reimbursement coverage to ensure more people have access to high-quality medical treatment. In addition, the Asia-Pacific area is expected to benefit from the rising demand for generic pharmaceuticals.

The African region accounted for 26% of the global burden for Hepatitis B and 125,000 associated deaths. The Middle East and Africa, on the other hand, have the lowest market share for hepatitis B treatments because of strict government regulations, the presence of underdeveloped economies, a lack of awareness, and low healthcare spending in the area.

Ethiopia has an estimated 11 million people living with HBV (prevalence of 9.4 percent). Ethiopia is committed to halting transmission by providing access to safe, affordable, and effective care to those living with HBV. The Ethiopian government has scaled up its HBV program by increasing the number of health facilities providing treatment services from 13 to 90. The Ethiopian National Viral Hepatitis Treatment Guidelines recommend TDF and ETV therapies for chronic HBV, with TDF being the most widely used. A revolving drug fund (RDF) is used to aggregate demand and procure centrally to leverage volume-based pricing. The Ethiopian Pharmaceutical Supply Service (EPSS) is the procurement agency tasked with procuring healthcare commodities in the country and its purchase.

Rwanda has an estimated HBV burden of 399,000 (HBV prevalence of 0.82 percent) infections. The country’s Viral Hepatitis program sits within the wider HIV program at Rwanda Biomedical Centre (RBC). The program is in a scaling stage, and HBV diagnosis and treatment services are available at all health facilities across the country, entirely free to the patients. HBV screening is mandatory for pregnant women through antenatal care. Free screening services are available for the general population.

India has an estimated 33 million people living with HBV (HBV prevalence at around 0.95 percent). The Indian government has established the National Viral Hepatitis Control Program (NVHCP) which offers free diagnostics for the management of patients with hepatitis B or C. The viral hepatitis program is scaling, with 868 facilities nationwide (across most district hospitals and some sub-district hospitals) providing hepatitis treatment. It is 100 percent domestically funded by the Government of India, and all services are offered free of cost to patients.

Hepatitis B Market Recent Industry Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 28 May 2026 | Ionis Pharmaceuticals, Inc. | Partnered with GSK to announce positive pivotal Phase 3 data (B-Well 1 and B-Well 2 trials) for bepirovirsen, an investigational antisense oligonucleotide for chronic hepatitis B. | The drug demonstrated statistically significant functional cure rates in participants with baseline HBsAg levels below 1000 IU/ml, offering a path to redefine lifelong therapy paradigms. |

| 22 May 2026 | Gilead Sciences, Inc. | Received U.S. FDA approval for its injection drug Hepcludex (bulevirtide) to treat chronic hepatitis delta virus (HDV) in adults with compensated cirrhosis. | As the first-ever approved option for HDV, this milestone specifically targets and reduces dangerous liver disease complications in hepatitis B/hepatitis delta co-infected patients. |

| 14 May 2026 | GlaxoSmithKline Biologicals | Secured a formal U.S. FDA product approval letter for updates regarding its recombinant vaccine, ENGERIX-B. | The approval strengthens the market availability of standard preventative regimens protecting individuals from infection across all known subtypes of the hepatitis B virus. |

| 28 April 2026 | GlaxoSmithKline plc (GSK) | Obtained U.S. FDA Breakthrough Therapy Designation and Priority Review acceptance for its New Drug Application of bepirovirsen. | The regulatory fast-tracking positions the asset for an optimized review timeline, setting a target PDUFA action date of October 26, 2026. |

| 15 April 2026 | Arbutus Biopharma Corporation | Granted U.S. FDA Fast Track Designation for imdusiran (AB-729), an RNAi therapeutic developed for chronic hepatitis B treatment. | The designation accelerates clinical development support for an option designed to reduce all surface antigens (HBsAg) and reawaken host immune control. |

Hepatitis B Market Competitive Landscape:

On 19 Feb. 2023- AstraZeneca announced the successful completion of the acquisition of Icesave, Inc., a US-based clinical-stage biopharmaceutical company focused on developing differentiated, high-potential vaccines using an innovative, protein virus-like particle (VLP) platform. As a result of the acquisition, Icesave has become a subsidiary of AstraZeneca, with operations in Seattle, US.

Oct. 10, 2023 – The Hepatitis B Foundation, a global nonprofit headquartered in the U.S., coordinated the highly successful 2023 International HBV Meeting, held Sept. 19-23 in Kobe, Japan.

China – June 26, 2023 – Brii Biosciences Limited (“Brii Bio,” “we,” or the “Company”, stock code: 2137. HK), a biotechnology company developing therapies to improve patient health and choice across diseases with high unmet needs, announced that it entered into definitive agreements with Qpex Biopharma (“Qpex”) and third parties in connection with the acquisition of Qpex by Shionogi.

Hepatitis B Market Scope: Inquiry Before Buying

| Global Hepatitis B Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 5.53 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.2% | Market Size in 2034: | US $ 8.01 Bn. |

| Segments Covered: | by Therapy | Chemo Therapy Immunosuppressant Therapy Nucleoside Analogue |

|

| by Product Type | Hepatitis B Vaccine Anti-viral Drugs Tenofovir Entecavir |

||

| by End User | Hospital Pharmacies Retail Pharmacies Online Pharmacies |

||

Hepatitis B Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Hepatitis B Market Key Players:

1. Gilead Sciences - USA - Antiviral medications

2. Bristol-Myers Squibb - USA - Antiviral medications

3. AbbVie - USA - Antiviral medications

4. Abbott Laboratories - USA - Diagnostic tests

5. Thermo Fisher Scientific - USA - Diagnostic tests

6. Becton, Dickinson and Company - USA - Diagnostic tests

7. Johnson & Johnson - USA - Diagnostic tests

8. Dynavax Technologies Corporation - USA - Vaccines

9. MedImmune - USA – Vaccines

10. GlaxoSmithKline - UK - Vaccines

11. Merck & Co. Inc. - USA – Vaccines

12. Pfizer Inc. - USA - Vaccines

13. Novartis AG - Switzerland - Antiviral medications

14. Siemens Healthineers - Germany - Diagnostic tests

15. Roche - Switzerland - Diagnostic tests

16. Sanofi Pasteur - France - Vaccines

17. Qiagen N.V. - Netherlands - Diagnostic tests

18. F. Hoffmann-La Roche AG - Switzerland - Antiviral medications

19. Astellas Pharma - Japan - Antiviral medications

20. GeneOne Life Science Inc. - South Korea - Vaccines

21. Hualan Biological Engineering Inc. - China - Vaccines

22. Mitsubishi Tanabe Pharma - Japan - Antiviral medications

23. Serum Institute of India - India - Vaccines

24. Zydus Cadila - India - Vaccines

25. Beijing Tiantan Biological Products Co., Ltd. - China – Vaccines

26. Bio-Manguinhos – Brazil – Vaccines

27. Saudi Biological Industries – Saudi Arabia - Vaccines

Frequently Asked Questions:

1] What segments are covered in the Hepatitis B Market report?

Ans. The segments covered in the Hepatitis B Market report are based on Therapy, Product Type, and End Users.

2] Which region is expected to hold the highest share in the Hepatitis B Market?

Ans. The North American region is expected to hold the highest share of the Hepatitis B Market.

3] What is the market size of the Hepatitis B Market by 2034?

Ans. The market size of the Hepatitis B Market by 2034 will be $ 8.01 Billion.

4] What is the forecast period for the Hepatitis B Market?

Ans. The Forecast period for the Hepatitis B Market is 2026- 2034.