Headlight Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

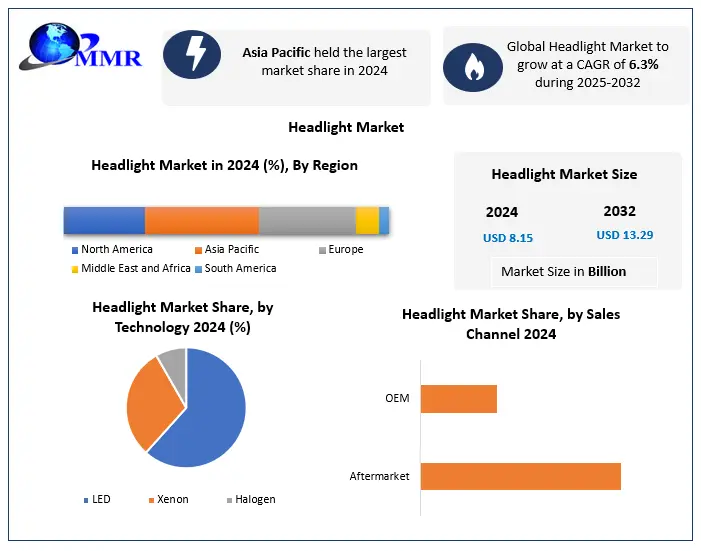

Global Headlight Market was valued at US$ 8.15 Bn in 2024 and the total Headlight Market revenue is expected to grow at 6.3% of CAGR through 2025 to 2032, reaching nearly US$ 13.29 Bn.

Headlight Market Overview

Headlight is a mounted vehicle light designed to illuminate road ahead, ensuring safe driving in low visibility condition such as night, fog or rain.

Global headlight market has been experiencing significant growth driven by advancement in lighting technology, increasing vehicle production and stringent safety regulation. Headlight play critical role in vehicle safety, visibility and aesthetic with innovation like LED, laser and adaptive lighting system gaining traction for their energy efficiency and superior illumination. Headlight market is further propelled by rising demand for luxury and electric vehicle which often incorporate advanced lighting solution.

Asia Pacific led global headlight demand due to its massive automotive manufacturing base, rapid urbanization and growing middle class adoption of premium vehicle. China, Japan and South Korea are at forefront driven by strong OEM investment, government safety regulation and consumer demand for advanced features. Major players like Osram, Philips, Hella and Koito are investing in smart headlight technology including matrix LED and autonomous adaptive system to enhance night time driving safety. With trend like connected vehicles, autonomous driving and customization shaping the industry, headlight market is poised for sustained expansion, catering to OEMs, aftermarket demand and next gen mobility solutions. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Headlight Market Dynamics

OLED Penetration to Drive Headlight Market Growth

The primary drivers of this growth include increased attention to road safety, rising demand for improved car technology, and advancements in interior lighting solutions. The latest and most popular trend in the automotive headlight market is the use of OLED for both interior and external headlights. Interior ambient lighting is quite important in the interior of a vehicle. Automobile manufacturers provide multi-colour environment lighting, and car owners may choose the lamplight colour and brightness to enhance their driving experience, which drive the headlight market.

Thanks to Apple, OLED has gained popularity over the last few years. After the introduction of OLED in the iPhone X as a full-screen dynamic light with low afterglow and low power consumption, automotive manufacturers recognized OLED as a potential. OLED is unlike any other light source. It makes advantage of organic matter's self-luminous property, which consumes less energy and generates soft, low-blue light that is extremely comparable to natural light.

Furthermore, OLED lighting has a low heat value, which is beneficial to environmental conservation. The thin and light characteristics of OLED grabbed the interest of vehicle manufacturers since it helps deliver convenience and freedom to design while also enabling patterned lighting.

As a result, OLED technology is emerging as the most demanding and actively penetrating technology in automotive headlights, healthcare, and a variety of other sectors. Furthermore, automakers such as Audi and BMW have already used OLED in their vehicles and have progressed to OLED-based interior illumination for cars. For example, Audi's A8 and S8 models will come standard with digital OLED rear lights in 2024. On the A8, customers may select between two light signatures (the S8 offers three possible signatures). Audi claims the first vehicles will be delivered in the second quarter of 2024. OLED Works manufactures OLED panels.

The taillights of the 2020 H9 Hongqi (a Chinese manufacturer owned by FAW Car company) sedan are illuminated with OLED lighting panels. Each module of the H9 contains four red OLED displays. The panels are 131x32 mm and include 5 segments each. The color code is CIY (0.69, 0.31). Yeolight manufactures the panels.

Increasing Demand for Laser Lights to Create Opportunities in Headlight Market

Laser light is an absolute innovation in vehicle lighting and the next big step forward after the introduction of halogen, xenon, and LED headlight technology. This lighting trend brings up entirely new possibilities for the design and performance of headlights.

Laser headlights are one of the market's most modern headlight technologies. They initially appeared in Germany, where drivers need lights on expressways for more than 600m due to their fast speeds. Laser is currently the only technology that allows for such long-distance lighting. Laser headlights operate differently from LED headlights. A laser diode (typically blue) impacts a sequence of micromirrors, following which a phosphor element helps in the creation of white light, and finally a number of lenses. The width of the light beam may be controlled by adjusting the location of the micromirrors. The headlight can emit a small, brilliant beam or a broad, long-range beam, which drives the headlight market.

One of the most important driving factors of laser headlights is the addition of a second infrared laser to the lighting system. This second light source might also function as a Lidar to measure the distance to various obstacles or as a night vision camera. This second light source might possibly be used as a communication transmitter to other automobiles or road features. For example, The BMW i8 and Audi R8 LMX were released almost immediately with the first series production automobiles featuring laser headlights. The new BMW 7 Series with new features launched in 2020.

As a system partner, OSRAM was significantly involved: the laser full beam is based on OSRAM Specialty Lighting innovations. The whole beam of these cars has a range of up to 600 meters as a consequence of this laser technology, which is double the distance of the current standard LED headlights.

High Cost of Headlights and Repair Costs to Hamper Headlight Market growth

The growing requirement for operational efficiency improved overall safety, and increased visibility is likely to drive demand for headlights. Intelligent headlights, on the other hand, are linked to car sensors, allowing them to automatically change based on the driving environment. This gradually raises the price of headlights used in automobiles.

Certain automotive parts are growing more expensive as cars become more complex and technologically advanced, which is hampering the headlight market during the forecast period. While this method may still be viable for some models, for the majority of automobiles, this simple repair has become more complicated and time-consuming. On some vehicles, the entire headlamp must be removed, which may require the removal of the entire bumper.

If customers only need to replace the headlight bulb, a package of halogen replacement bulbs can cost as little as $15. Customers may have to spend more for HID replacement bulbs depending on the type of bulb they want. The cost of replacing a whole headlight assembly varies greatly based on the brand and model of the vehicle, as well as whether it is a sedan, pickup truck, or SUV. The cost of a high-quality headlight assembly can be anywhere in the range of $250-$700.

Headlight Market Segment Analysis:

Based on Technology, the Headlight Market is segmented into Xenon, LED, and Halogen. LED is expected to dominate the market during the forecast period. Global Automotive LED Product Trend and Regional Market Analysis,' the global penetration rate of LED headlights will exceed 60% in 2024, with penetration in new energy vehicles (NEV) exceeding 90%. The automotive LED light sector has grown significantly in the previous half-decade as global demand for premium automobile cars has increased. The rising human population may drive the demand for LED headlights during the forecast period.

The demand for energy-efficient lighting solutions is driving the growth of the automotive LED headlights market. The EV industry is largely driven by growing environmental concerns and government efforts. The effectiveness of lighting systems is important to automotive safety. As a result, automotive headlamp OEMs and suppliers are increasingly focused on offering an efficient lighting system in automobiles. When it comes to light output, LED headlights can illuminate a longer distance than halogen headlamps. During the forecast period, these factors will drive the global automotive LED headlights market.

Based on the Vehicle Type, the Headlight Market is segmented into passenger cars and commercial vehicles. Passenger cars are expected to dominate the headlight market during the forecast period. Passenger vehicles include two-wheelers, three-wheelers, and passenger cars. The development of this market sector is due to rising purchasing power, growing automotive demand among the population, as well as the rapid expansion of such cars' manufacturing and sales.

In comparison to the Q1 and Q2 sales of 2020, the OICA reported that the global sale of passenger cars climbed by 26% in 2024. Similar to this, an IBEF study states that India sold 27.11 lakh units of passenger automobiles in FY21. The need for adaptive headlights is fueled by these advances. The popularity of e-bikes, e-scooters, and other eco-friendly vehicles is increasing as a result of rising public awareness of environmental concerns and government attempts to encourage the use of such vehicles. As a result, demand for passenger cars with headlights has increased.

Headlight Market Regional Insights:

Asia Pacific dominated the market with a 43% share in 2024. Due to the region's industrialization and urbanization, growing economies like China and India are expected to drive the growth of the automotive headlight market in APAC.

The automotive headlight market is now dominated by China in terms of installation, which in turn increases the need for the market in the region. In 2018, China, which is the world's largest car manufacturing country, manufactured 27,809,196 automobiles. Several significant automakers are based in the country, including SAIC Motor, Dongfeng, FAW, and Chang'an. A few western auto manufacturers are also concentrating on growing in China to provide a wider range of customers.

For instance, to improve its capacity for growth, French supplier Valeo developed its tech centre in central China. Additionally, regional players are concentrating on creating an effective lighting solution in order to gain a dominant market position. Therefore, it is expected that the growth of the automotive headlight market in the country would be primarily driven by the country's robust automotive sector and the growing focus of western automakers on expansion into the country.

Headlight Market Competitive Landscape

Major Key Players in Headlight Market includes Koito, Stanley and HELLA GmbH & Co. KGaA. HELLA GmbH & Co. KGaA is globally recognized innovator in automotive headlight manufacturing specializing in high performance LED, matrix beam and laser lighting system. The company distinguishes itself through proprietary optical technology, advanced beam patterning algorithm and seamless integration with vehicle electronics positioning it as a preferred partner for premium automaker like Audi, BMW and Porsche. While competitor such as Koito (Japan) and Marelli (Italy) focus on cost efficient mass production, HELLA maintains a competitive edge through German engineered precision, in house LED driver IC development and patented adaptive lighting solution. However, it faces growing pressure from Chinese manufacturer like HASCO Vision and Changzhou Xingyu which offer aggressively priced alternative. To sustain leadership HELLA invest heavily in next gen digital micromirror headlights, vehicle to everything (V2X) communication enabled lighting and sustainable production processes ensuring its position at the forefront of intelligent and connected automotive lighting innovation.

Headlight Market Key Trends

• Rise of Adaptive & Digital Headlights: Matrix LED and Digital Light Processing (DLP) technologies are gaining traction, enabling glare-free high beams and projection of navigation/road signs onto the road.

• EV-Specific Lighting Designs: Signature lighting (e.g., animated welcome sequences) and aerodynamic light bars are becoming key brand differentiators for electric vehicles.

• Integration with ADAS & Autonomous Driving: Headlights now sync with LiDAR, cameras, and sensors to dynamically adjust beams for pedestrian detection or autonomous driving modes.

Headlight Market Key Developments

• Valeo SA (France): March 2024: Valeo launched its next-generation "SmartBeam" matrix LED headlights with AI-powered adaptive lighting, debuting in the 2025 Mercedes-Benz E-Class.

• Stanley Electric Co., Ltd. (Japan): January 2025: Stanley Electric unveiled ultra-thin OLED taillights with 3D holographic effects for a new Toyota luxury EV model, enhancing brand aesthetics.

• Osram GmbH (Germany): September 2024: Osram introduced LiDAR-integrated laser headlights for autonomous vehicles, partnering with BMW for their 2026 iNEXT SUV.

• Hyundai Mobis Co., Ltd. (South Korea): July 2024: Hyundai Mobis developed solar-rechargeable LED headlights for Hyundai/Kia EVs, reducing battery drain by 15% (first used in 2025 IONIQ 7).

• Varroc Lighting Systems (India, Varroc Group): November 2024: Varroc launched modular, plug-and-play LED headlights for Indian EV startups, cutting production costs by 20% for mass-market adoption.

Headlight Market Scope: Inquiry Before Buying

| Headlight Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 8.15 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 6.3% | Market Size in 2032: | USD 13.29 Bn. |

| Segments Covered: | by Technology | Xenon LED Halogen |

|

| by Vehicle Type | Passenger Cars Commercial Vehicles |

||

| by Sales Channel | OMEs Aftermarket |

||

Headlight Market, by region

North America (United States, Canada and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam, Indonesia, Philippines, Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America)

Headlight Market, Key Players are

North America

1. DE amertek corporation (US)

2. J.W. Speaker Corporation (US)

Europe

3. Hella GmbH & Co KGaA (Germany)

4. Robert Bosh GMBH (Germany)

5. Osram GmbH (Germany)

6. Magneti Marelli (Marelli Automotive Lighting) (Italy)

7. Valeo SA (France)

8. Koninklijke Philips N.V (Netherlands)

9. Lumileds (Netherlands)

10. ZKW Group (Austria)

11. Aspöck Systems GmbH (Austria)

Asia Pacific

12. Stanley electric Co.LTD (Japan)

13. Ichikoh Industries, Ltd. (Japan)

14. Koito manufacturing Co.LTD (Japan)

15. Denso Corporation (Japan)

16. HASCO Vision (China)

17. Changzhou Xingyu (China)

18. Hyundai mobis Co.LTD (South Korea)

19. SL Corporation (South Korea)

20. Varroc Lighting Systems (Varroc Group) (India)

Frequently Asked Questions

1] What segments are covered in the Global Headlight Market report?

Ans. The segments covered in the Headlight Market report are based on vehicle Type, Technology, and Sales Channel.

2] Which region is expected to hold the highest share in the Global Headlight Market?

Ans. The Asia Pacific region is expected to hold the highest share in the Headlight Market.

3] What is the market size of the Global Headlight Market by 2032?

Ans. The market size of the Headlight Market by 2032 is expected to reach US$ 13.29 Bn.

4] What is the forecast period for the Global Headlight Market?

Ans. The forecast period for the Headlight Market is 2025-2032.

5] What was the market size of the Global Headlight Market in 2024?

Ans. The market size of the Headlight Market in 2024 was valued at US$ 8.15 Bn.