Hard Luxury Goods Market by Product Type, Gender, Distribution Channel and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

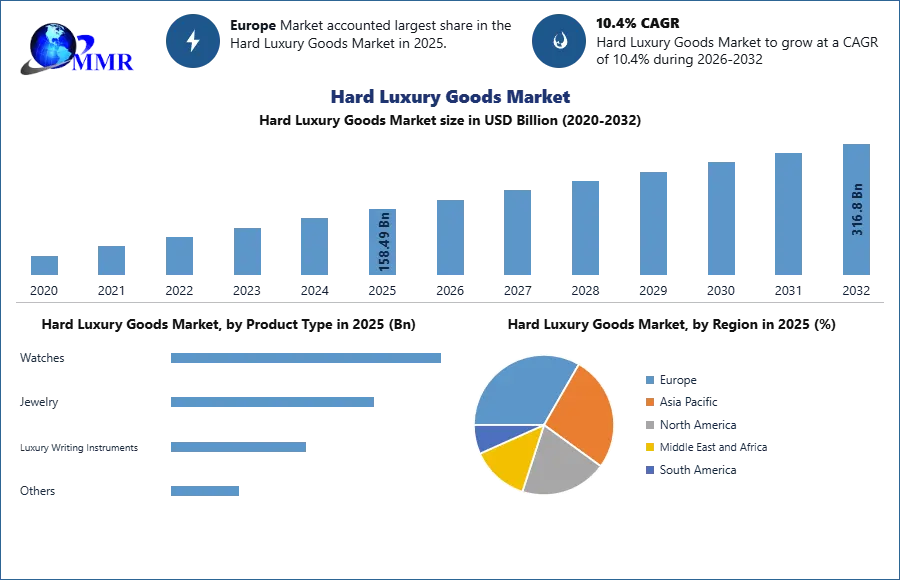

Hard Luxury Goods Market was valued at USD 158.49 Billion in 2025, and it is expected to reach USD 316.80 Billion by 2032, exhibiting a CAGR of 10.4% during the forecast period (2026-2032)

Hard luxury goods are long-lasting things such as jewels and watches. Every item of jewellery and watch in hard luxury is one-of-a-kind and meant to be timeless works of art. Hard luxury is a mainstay of the personal luxury goods industry and continues to account for a large share of sales; however, it has been characterised by relatively low growth in recent years due to an economic slowdown and changing consumption habits, particularly in the Greater China region, which fueled sales at the start of the decade. When compared to other nations, China made the highest revenue of USD 22,000 million in 2022.

In 2022, per person revenues of USD 8.93 were earned in proportion to overall population data. Consumers' rising taste for cutting-edge and sophisticated items has fueled global sales of hard luxury goods. During the forecast period, the growing number of high-net-worth people in developed nations, as well as rising disposable income in developing markets, are expected to have a favourable impact on this market.

The Global Hard Luxury Goods Market is segmented by product type, gender and distribution channel. Based on product type, the market is segmented into Watches, Jewelry, and Others. Based on gender, the market is segmented into Female and Male. Based on distribution channel, the market is segmented into Online Stores, Department Stores, Monobrand Stores, and Specialty Stores. Based on region, the market is segmented into North America, Asia Pacific, Europe, Middle East & Africa, and South America. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Hard Luxury Goods Market Research Methodology

The Global Hard Luxury Goods Market report provides an evaluation of the market for the forecast period. The report comprises various segments as well as an analysis of the trends and factors that are playing a substantial role in the market. In the report, the market outlook section mainly encompasses fundamental dynamics of the market which include drivers, restraints, opportunities, and challenges faced by the industry. Based on the understanding of requirements, a secondary research is conducted to identify the segment specifications, qualitative and quantitative data along with the factors responsible for the growth of the market. The secondary source referred for the research are press releases, company annual reports, government websites, and research papers related to market. Moreover, quantitative and qualitative data is extracted from paid database like Reuters, Bloomberg, Hoovers, etc. The secondary research carried out at primary level is verified by primary research.

In the report, Porter examines competition, new entrants in the market, supplier power, buyer power, and the threats of the substitute products and services in the market. PESTLE identifies factors like political, economic, sociocultural, technological, legal, and environmental, that may affect an organization and its competitive standing. The main approach used to calculate accurate market size is bottom-up market sizing approach, where macro and micro view of all the potential customers, revenue and current market is considered as a whole. On the other hand, the research is also conducted by considering micro level segment that can be realistically targeted and calculated, which results in better forecasting and more accurate data on amore granular level. This approach is conducted by obtaining data from reliable sources like Gartner, McKinsey and the Bureau of Labor Statistics, and analysing multiple sources.

COVID-19 Impact on Hard Luxury Goods Market

Amid the coronavirus pandemic, every company's first responsibility was to safeguard the health and safety of its employees, customers, and business partners. Indeed, luxury corporations have shifted their focus to meet pressing public-health needs: factories that formerly created hard luxury products now produce face masks and hand sanitizer, and many luxury groups have made monetary commitments to hospitals and other non-profit organisations. Simultaneously, with millions of people relying on the luxury-goods industry for a living—from factory workers and retail-store employees to small-town artisans and craftspeople—industry leaders are planning ahead and grappling with longer-term strategic questions to ensure their businesses' survival.

Even before the pandemic, independent luxury-goods wholesalers in Europe (many of which are small, family-owned boutiques) and some of the large North American luxury department stores were struggling, thanks in part to luxury brands' shift to vertical integration over the last 20 years and, more recently, the rise of e-commerce. Some of them may be forced out of business as a result of the pandemic. Firms who have not yet fully migrated to a vertically integrated distribution strategy, as well as startup brands that rely on wholesale channels to attract new customers and finance the development of their full collections, might be harmed. Wholesalers are expected to implement aggressive sales and discount practises in order to survive, which might harm the premium positioning of brands that do not have a concession model in the longer term.

Hard Luxury Goods Market Dynamics

Hard Luxury Adapting e-commerce: Soft luxury, which includes products like leather accessories, purses, and designer apparel, has adapted particularly successfully to e-commerce, with it estimated that 9 percent of soft luxury purchases are now made online. Hard luxury, which includes products such as jewellery and watches, has taken longer to adapt. Less than 5% of the hard luxury market is now available online, and several manufacturers are sceptical that their customers will ever want to make such large purchases online.

Bold movements by existing houses into new areas of specialisation are assisting in the growth of hard luxury online. In order to acquire market share, brands that have previously concentrated on soft luxury have recently made steps to manufacture and sell hard luxury products. For example, Louis Vuitton shifted its focus from apparel and luggage to develop a jewellery business with an internet presence. These are big moves by the norms of a cautious, conservative sector.

Emerging Technology Embedded Products: Innovative and fashionable goods that incorporate technological aspects in jewellery and watches are estimated to boost product demand. Totwoo Fashion Technology, a smart jewellery producer, unveiled a new line, 'Wonderland,' in April 2019, showing social interactive wearable technology pendants with intelligent cores. The core is used to transmit data from jewellery to mobile applications through Bluetooth. Likewise, in 2020. Totwoo unveiled its new 'Morse Code Series,' a series developed for couples in which a Morse code rhythm necklace sends a notice to the other person whenever the first person taps his/her necklace. Long-distance remote sensing (Love rhythm), love code pair conversation, step tracking, phone notification, personalised alert, and private journal are among the additional functions of the necklace. As a result, the advent of smart luxury items is expected to propel the hard luxury industry forward.

Rising Number of Wealthy Population: Hard luxury items are products that are primarily sought after by the wealthy. The hard luxury goods industry is expected to grow due to an increase in the number of rich people. For example, in January 2020, over 2,153 billionaires worldwide possessed more money than the 4.6 billion individuals who constitute 60% of the global population. Companies are attempting to attract the attention of the millennial and GenZ populations by giving personalised product offerings. As a result, rising demand for high-end fashion items from the wealthy population would drive market development.

Inclination Towards Sustainable Products: Lowering power use, using less water, and using safer raw materials are being emphasised to achieve supply chain sustainability. In November 2019, the Prada Group signed a Sustainability Linked Loan deal with the Credit Agricole Group. If Prada meets its sustainability standards, it will be able to lower interest rates on a 50 million euro five-year sustainability term loan. Among the sustainability goals are the usage of Re-Nylon (regenerated nylon) in the creation of items and attaining LEED Gold or Platinum Certification for the company's outlets. As a result, increased attempts to produce sustainable luxury products are expected to stimulate demand for eco-friendly hard luxury items.

High Price of Jewelry & Watches: Hard luxury necessitates greater investment, and the cost of hard luxury is often substantially more than that of soft luxury. As a result, hard luxury sales, which include items such as jewellery and watches, have been slower than soft luxury sales. Apparently, less than 5% of hard luxury transactions are made online now, and most hard luxury vendors are sceptical that their luxury consumers would buy hard luxury products online as readily as they buy soft luxury.

Hard luxury is evolving in part because soft luxury is changing. Changes in global purchasing patterns imply new clients to serve, notably in the BRIC countries. Everyone is arguing about how to engage younger audiences who do not act like previous generations of consumers. Brands have been lowering their demanding pricing points in order to include profitable diffusion brands and approachable price points in order to draw in new consumers. Thomas Sabo, Michael Kors, and Kate Spade are examples of " affordable luxury."

Adaption of Second-Hand Branded Items: Second-hand items are sold at auctions, charity events, bazaar-style fundraisers, privately operated consignment stores, and other similar venues. As second-hand items are supplied at a cheaper cost than the original price of the product, a rising trend of acquiring second-hand branded products or renting luxury goods is estimated to affect the market of original hard luxury goods. Rising consumer living standards, aided by rising disposable income levels, have resulted in an increase in demand for second-hand luxury items in both established and emerging countries, with the millennial and urbanised populations preferring high-end fashion accessories at reduced rates.

Furthermore, the widespread availability of pre-owned luxury goods on internet platforms, as well as the reducing stigma associated with using pre-owned luxury products, have slowed market development. Similarly, the rising counterfeiting trend, in which items mimicking premium brands are sold at cheaper rates, is estimated to restrain market growth.

Hard Luxury Goods Market Segment Analysis

Based on the product type, the market is segmented into watches and jewelry. Because of the growing demand for smart luxury watches, timepieces are the most significant income producers. Watches are estimated to be the most valuable product in the global hard luxury goods market, with sales increasing at a CAGR of 10.08 percent during the forecast period. However, due to the increasing demand for various types of jewellery goods are expected to have a constant growth in demand during the forecast period.

Based on the gender, the market is classified into men and women. Women are seen to be a more lucrative purchasing market for hard luxury items than males. Women would account for the majority of the market, owing to a growing preference for accessories such as watches, necklaces, rings, earrings, and bracelets. Emerging male grooming trends would promote the expansion of the male category, with branded high-end timepieces seeing increased demand from men. As a result, several businesses are focused on providing goods that can meet the diverse needs of both end-users.

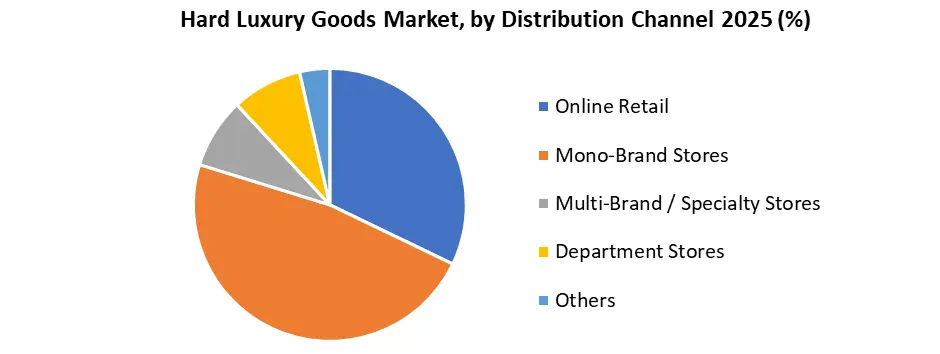

Based on the distribution channel, the market is categorized into monobrand stores, specialty stores, department stores, and online stores. Monobrand and speciality stores are selling more hard luxury products than the other two sectors, and this trend is expected to continue in the coming years. Customers may directly view and touch the items at monobrand and specialty stores, allowing them to compare their qualities in-person. Companies are attempting to improve their market footprint by increasing their presence in retail or department shops. For example, in February 2020, Burberry announced the acquisition of Printemps in Paris, a department store chain that sells a wide range of luxury goods as well as fashion and beauty products. However, the convenience of purchasing through online channels would make it the fastest-growing area. The COVID-19 pandemic has created even more opportunity to enhance internet channels in the luxury industry. For example, in March 2020, Reliance revealed plans to launch a new e-commerce site in India for purchasing luxury commodities. As a result, the online purchasing of hard luxury products is estimated to continue in the near future.

However, the convenience of purchasing through online channels would make it the fastest-growing area. The COVID-19 pandemic has created even more opportunity to enhance internet channels in the luxury industry. For example, in March 2020, Reliance revealed plans to launch a new e-commerce site in India for purchasing luxury commodities. As a result, the online purchasing of hard luxury products is estimated to continue in the near future.

Hard Luxury Goods Market Regional Insights

Europe held the largest market share in 2025 and is estimated to dominate the hard luxury goods market during the forecast period. The presence of a significant number of important players in the area, including as LVMH, Burberry, Bvlgari, John Harrison, Cartier, Abraham Louis-Breguet, Chopard, Pandora Jewellers, Chanel, and others, is linked to Europe's leading share of the global hard luxury goods market. Switzerland hosts the industry's largest watch exhibitions. Almost every well-known watchmaker is based in Switzerland, mostly between the towns of Geneva and Basel. When it comes to the art of excellent clocks, Germany ranks in second only to Switzerland. The distinctive three-quarter plate, Glashutte striped finishing, and hand-engraved balance cocks are all quite appealing. Similarly, a surge in German-made watch movements is placing European watchmakers on the map.

London scored first among the top five cities in the world, accounting for 9.6 percent of worldwide new luxury shop openings, including hard and soft luxury products. In comparison to 2020, it climbed by around 41%. In the same ranking, Paris was rated fourth, accounting for 5.1 percent in 2020. Similarly, as a fashion powerhouse, Europe has a high number of luxury fashion weeks in countries such as Italy, France, and the United Kingdom, which is expected to support the rise of hard luxury products in the region.

The North American market is distinguished by the growing presence of a significant number of wealthy individuals, particularly in the United States, which has boosted product demand. In the United States, for example, the number of billionaires climbed from 298 in 2000 to around 614 in 2020. In 2022, the income earned by hard luxury items in the United States was USD 7,844 million.

Furthermore, the presence of a populace that is strongly attracted toward stylish garments and accessories has contributed fuel to the region's market expansion. The United States is home to several manufacturers, including Harry Winston, Tiffany & Co., Signet, Vortic, DuFrane, RGM, and others.

The Asia Pacific market is estimated to expand fast as the region's middle-class population's disposable incomes rise. Similarly, improved access to global premium brands would enhance product consumption. For example, in July 2020, Burberry, a British luxury goods firm, announced the opening of its first social retail store in Shenzhen for Chinese consumers, in collaboration with Tencent. The shop is approximately 539 sqm/5800 sqft in size, with approximately 10 rooms giving various interactive, customised purchasing experiences. Furthermore, with their increased disposable money, the region's expanding population of working women has accelerated purchase of women-centric luxury items such as smart watches and jewellery.

Emerging Asia Pacific countries like as China, Japan, Singapore, India, and others are estimated to boost the region's hard luxury goods market growth. In 2022, China created 22,000 million dollars in sales, Japan generated 3,128 million dollars in revenue, and Singapore generated 2,050 million dollars in revenue. The increased demand for hard luxury products in Singapore is being fueled by new jewellery businesses and rising watch sales. Rapid urbanisation combined with rising disposable income in Thailand and Malaysia is expected to grow consumer base and make Thailand and Malaysia the leading contributors to the revenue of the Asia Pacific region's hard luxury goods industry, followed by Indonesia and the Philippines.

South America market is expected to increase steadily as the urban population in nations such as Brazil and Chile grows. Changes in the region's level of life are thus expected to boost consumer spending on luxury products. Furthermore, the Middle East and Africa are expected to witness an increase in demand for luxury goods from Gulf countries such as the United Arab Emirates and Saudi Arabia. As a result, significant firms have potential to grow their operations in this region.

The objective of the report is to present a comprehensive analysis of the global Hard Luxury Goods Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Hard Luxury Goods Market dynamic, structure by analyzing the market segments and projecting the Hard Luxury Goods Market size. Clear representation of competitive analysis of key players by segment type and regional presence in the Hard Luxury Goods Market make the report investor’s guide.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 08 April 2026 | LVMH and Prada Group | Announced a major scaling of blockchain-backed Digital Product Passports (DPP) across their hard luxury divisions to document item origin and craftsmanship. | This initiative enhances consumer trust and resale value by providing a verifiable identity for high-value jewelry and timepieces. |

| 05 January 2026 | Compagnie Financière Richemont | Implemented a strategic omnichannel expansion in the Middle East, adding dedicated retail space for flagship maisons like Cartier and Piaget. | This move targets high-net-worth individuals in emerging regions to offset slower growth in traditional Western markets. |

| 01 December 2025 | Titan Company | Reported a market capitalization of USD 38.53 billion following the aggressive rollout of its Zoya and Tanishq international boutiques. | The expansion solidifies the company’s position as a top global competitor in the accessible and high-end jewelry segments. |

| 09 November 2025 | Bain & Company | Published data showing that jewelry remained the strongest performing category in the personal luxury sector, outperforming leather and footwear. | This trend reaffirms the investment-grade nature of hard luxury goods during periods of macroeconomic volatility. |

| 15 July 2025 | Vacheron Constantin | Formalized a global Certified Pre-Owned (CPO) program to capture value from the secondary watch market. | The program allows the brand to maintain pricing integrity and quality control over its heritage assets in the resale ecosystem. |

Hard Luxury Goods Market Scope: Inquire before buying

| Hard Luxury Goods Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 158.49 USD Billion |

| Forecast Period 2026-2032 CAGR: | 10.4% | Market Size in 2032: | 316.8 USD Billion |

| Segments Covered: | by Product Type | Watches Jewelry Luxury Writing Instruments Others |

|

| by Gender | Male Female Unisex |

||

| by Distribution Channel | Online Retail Mono-Brand Stores Multi-Brand / Specialty Stores Department Stores Others |

||

| by Price Range | Entry-Level Luxury Mid-Level Luxury High / Ultra Luxury |

||

Hard Luxury Goods Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Hard Luxury Goods Market Report in Strategic Perspective:

- LVMH Moët Hennessy Louis Vuitton

- Compagnie Financière Richemont

- Hermès International

- Kering SA

- Chanel Limited

- The Swatch Group

- Chow Tai Fook Jewellery Group

- Titan Company Limited

- Graff

- Signet Jewelers

- Pandora

- Swarovski

- Ralph Lauren Corporation

- Prada S.p.A.

- Giorgio Armani S.p.A.

- Burberry Group

- Harry Winston

- Mikimoto

- Van Cleef & Arpels

- Bvlgari

- Audemars Piguet Holding SA

- Patek Philippe SA

- Rolex SA

- Lao Feng Xiang

- Malabar Gold and Diamonds