Global Zero Waste Packaging Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

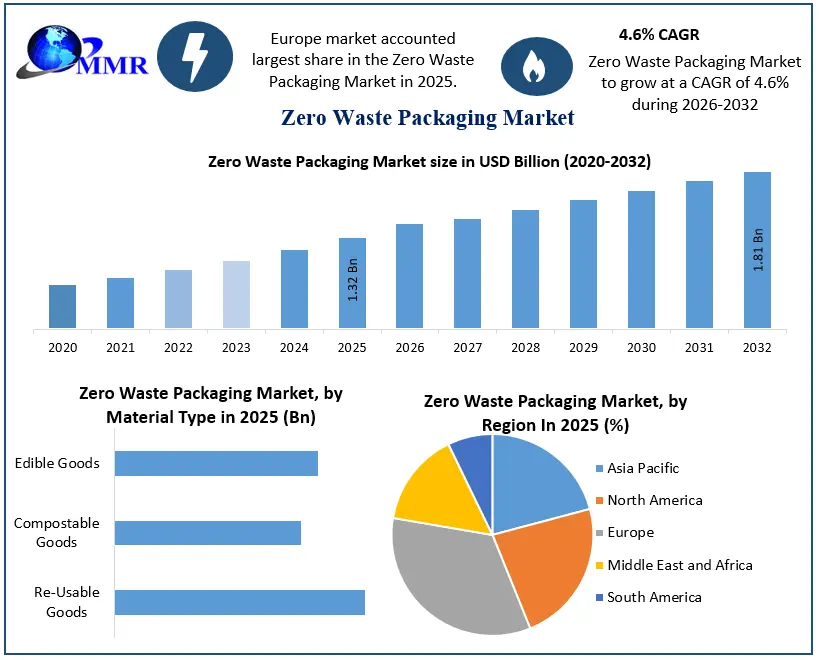

Zero Waste Packaging Market was valued at USD 1.32 Bn. in 2025 and is expected to reach USD 1.81 Bn by 2032, at a CAGR of 4.6% during the forecast period.

Zero Waste Packaging Market Overview

Zero waste packaging promotes the design and use of packaging that is reusable, recyclable, or compostable, ensuring no waste ends up in landfills by aligning with circular economy design principles. The report highlights the growing availability of biodegradable, reusable, and recyclable packaging across sectors such as food & beverage, personal care, e-commerce, and retail.

However, there are several complexities and challenges affecting supply and demand dynamics. While regulatory pressure and rising consumer awareness are driving high demand, challenges such as sourcing raw materials and environmental limitations are slowing supply.

Regionally, Europe leads the market due to stringent environmental policies, followed by North America and the Asia-Pacific region. The report also profiles key players, including Loop Industries, Tetra Pak, Loliware, Amcor, and DS Smith, along with the contributions from end-user segments.

The food & beverage and e-commerce sectors have shown the highest adoption of sustainable packaging in recent years. This shift is not just a matter of regulatory compliance or branding; it is also contributing positively to the overall brand image of the products. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Zero Waste Packaging Market Dynamics

Sustainability and Regulation to drive the Zero Waste Packaging Market growth

The Zero Waste Packaging Market is primarily driven by heightened environmental awareness among consumers and stringent government regulations promoting sustainable practices. As the report involves rising concerns about plastic pollution and carbon emissions, we have been compelled to adopt eco-friendly packaging alternatives. The corporate social responsibility initiatives and consumer preference for environmentally responsible brands are accelerating the shift toward zero waste solutions. Major industries such as food & beverage and personal care are leading this transition, with many companies embedding sustainability into their brand values and packaging strategies.

Innovation and Emerging Markets to create Zero Waste Packaging Market Opportunities

The growth opportunities within the zero waste packaging market, particularly through technological innovation and expanding application areas. Emerging materials such as edible packaging, plant-based plastics, and compostable films are opening new avenues for product development. Developing regions, especially in Asia-Pacific and Latin America, present untapped potential due to increasing urbanization and shifting consumer behaviour. E-commerce and digital retail are also providing a fertile ground for growth, with startups and established players alike investing in sustainable and cost-effective delivery solutions.

Cost, Infrastructure, and Supply Chain hurdles to create Zero Waste Packaging Market Challenges

Despite the promising outlook, the report identifies several key challenges hampering the full-scale adoption of zero waste packaging. One major barrier is the high production cost associated with sustainable materials compared to traditional plastic alternatives. Additionally, limited recycling infrastructure and a lack of standardization in waste management practices can hinder effective implementation. Businesses often face logistical hurdles in sourcing biodegradable inputs at scale, especially in regions where supply chains are underdeveloped. These challenges require coordinated efforts between governments, manufacturers, and environmental agencies.

Consumer Perception, Regulatory Ambiguity, and Cost Sensitivity Challenge to Restrain the Zero Waste Packaging Market

The market restraints include consumer skepticism regarding the performance and durability of sustainable packaging solutions. Some biodegradable or compostable materials may not perform well under certain environmental conditions, leading to concerns over product safety and shelf life. Regulatory ambiguity in labeling and certification standards also creates confusion for both producers and consumers. Moreover, in cost-sensitive markets, businesses are reluctant to invest in expensive packaging changes without clear ROI, limiting adoption in price-competitive segments.

Zero Waste Packaging Market Segment Analysis

Based on Material type, the market is segmented into Re-Usable Goods, Compostable Goods, and Edible Goods. Among these, the Compostable Goods segment dominated the Zero Waste Packaging Market in 2024. This dominance is driven by growing environmental concerns, stringent government regulations on plastic usage, and rising consumer demand for sustainable packaging solutions.

Compostable packaging, typically made from natural materials such as cornstarch, bagasse, and cellulose, offers an eco-friendly alternative that decomposes without leaving harmful residues. It is widely used in sectors like food and beverage, retail, and e-commerce, where single-use yet biodegradable solutions are increasingly favored. The advancements in material science and increasing corporate investments are enhancing the functionality and cost-efficiency of compostable goods, reinforcing their leading position in the market.

Based on the Distribution Channel, the market is segmented into Offline Store and Online Store. Among these, the Offline Store segment dominated the Zero Waste Packaging Market share. This dominance can be attributed to the traditional consumer preference for physically inspecting products before purchase, especially in sustainable or eco-friendly packaging that emphasizes tactile quality and visual appeal. Many zero-waste products are sold in specialty organic stores, supermarkets with sustainable sections, and local markets that prioritize environmentally conscious goods. The offline retail enables better consumer education and in-store demonstrations, which are critical in conveying the benefits of zero waste alternatives. Although the Online Store segment is growing due to rising e-commerce adoption and global outreach, it still trails behind offline channels in regions where direct consumer interaction remains influential in driving purchases.

Zero Waste Packaging Market Regional Analysis

Europe emerged as the dominant region in the Zero Waste Packaging Market in 2024, accounting for over 35% of the global market share, according to industry estimates. This dominance is fueled by stringent regulatory frameworks, such as the European Union’s Green Deal and Circular Economy Action Plan, which aim to ensure that all packaging in the EU market is reusable or recyclable by 2030. Countries like Germany, which recycles more than 67% of its waste, and France, with policies banning single-use plastics for certain products since 2021, are leading contributors.

The widespread adoption of Extended Producer Responsibility (EPR) laws across the region mandates producers to manage post-consumer waste, accelerating the shift towards sustainable packaging. The major European companies like Unilever and Nestlé have pledged to make 100% of their packaging recyclable or reusable by 2025, investing significantly in compostable, refillable, and biodegradable packaging solutions. The strong consumer demand, where 72% of European consumers prefer products with eco-friendly packaging, further strengthens Europe's leadership in the global market.

Zero Waste Packaging Market Competitive Analysis

The Zero Waste Packaging Market consists of a competitive landscape with key players focused on sustainable innovation, the development of eco-friendly materials, and partnerships for competitive advantage. Industry leaders like Loop Industries (Canada), Luxe Pack (Monaco), Biopak (Australia), Tetra Pak (Switzerland), and Amcor plc (Switzerland) are leading the way in developing recyclable, compostable, and reuse packaging solutions. Meanwhile, companies such as Avani Eco and Lifepack of Indonesia are gaining market share for their biodegradable packaging made from natural products, including cassava and agricultural waste. Likewise, in U.S. markets, PulpWorks, Agilyx Corporation, and Earthpack are also leading as advocates for plastic-free alternatives and closed-loop packaging systems. All these players are forming partnerships with major consumer goods and retail brands to implement zero waste practices in food & beverage, cosmetics, and e-commerce. As these players continue to innovate and align effectively with global sustainability aspirations, they are continually moving to develop and shape the growth of the zero waste packaging industry.

Zero Waste Packaging Market Recent Developments:

01 October 2025SmartSolve IndustriesThe packaging specialist launched PureNil™ 0, a plastic-free, 100% bio-based, printable, and water-soluble paper-based pouching substrate.This advanced solution enables true zero-waste flexible packaging for dry goods and single-serve foods, allowing consumers to safely flush, compost, or recycle the packaging after use.

| Date | Company | Development | Impact |

|---|---|---|---|

| 31 January 2025 | DS Smith plc | The company was acquired by International Paper to form a premier global provider of sustainable and zero-waste packaging solutions. | The merger accelerates the combined footprint across Europe and North America while driving large-scale engineering of 100% recyclable and reusable fiber-based packaging. |

| 20 February 2025 | TIPA Corp | The brand officially launched 312MET, a high-barrier, fully home-compostable packaging substrate specifically designed for salty snacks and dry food applications. | This breakthrough expands the portfolio of functional zero-waste flexible alternatives, helping food brands bypass plastic-reliant laminates while keeping high shelf-life performance. |

| 30 October 2025 | SmartSolve Industries | The company secured a USD 1 million JobsOhio Research and Development Grant to expand its R&D center footprint in Ohio. | The financial influx accelerates the commercial scaling and testing of advanced water-soluble and zero-waste packaging materials for consumer-packaged goods. |

| 23 April 2026 | Biome Bioplastics | The developer entered into a CAD 1.5 million joint initiative with Renaissance BioScience to engineer and scale renewable bioplastics via fermentation technologies. | The 2-year project targets replacing petroleum-based raw inputs with bio-based building blocks to optimize the production of compostable and zero-waste packaging layers. |

Zero Waste Packaging Market Scope: Inquire before buying

| Zero Waste Packaging Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 1.32 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.6% | Market Size in 2032: | USD 1.81 Bn. |

| Segments Covered: | by Material Type | Re-Usable Goods Compostable Goods Edible Goods |

|

| by Distribution channel | Offline Store Online Store |

||

| by End User Industry | Food and Beverage Healthcare Personal Care Industrial Others |

||

Zero Waste Packaging Market by Region

North America (United States, Canada and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam, Indonesia, Philippines, Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America)

Zero Waste Packaging Market Key Players are:

North America

1. Tetra Pak – Denton, Texas, USA

2. Amcor – Ann Arbor, Michigan, USA

3. DS Smith – Atlanta, Georgia, USA

4. Berry Global Group – Evansville, Indiana, USA

5. Ecovative Design – Green Island, New York, USA

6. Loliware – New York, New York, USA

7. PulpWorks Inc. – Walnut Creek, California, USA

8. TerraCycle / Loop – Trenton, New Jersey, USA

9. WestRock – Atlanta, Georgia, USA

10. World Centric – Rohnert Park, California, USA

11. Ranpak – Concord Township, Ohio, USA

Asia Pacific

1. Uhtamaki – Mumbai, India (Asia HQ)

2. Amcor Flexibles India – Pune, India

3. SCG Packaging – Bangkok, Thailand

4. Toyo Seikan Group – Tokyo, Japan

5. Greatview Aseptic Packaging – Beijing, China

6. Uflex Ltd. – Noida, India

7. Avani Eco – Bali, Indonesia

8. PakFactory – Hong Kong, China

9. Biopak – Sydney, Australia (Asia-Pacific operations through Malaysia & Singapore)

10. Hero Packaging – Sydney, Australia

11. Toppan Printing Co. Ltd. – Tokyo, Japan

12. Nippon Paper Industries – Tokyo, Japan

13. Shanghai Forests Packaging Group – Shanghai, China

14. Yash Pakka Ltd. – Ayodhya, India

Europe

1. Tetra Pak – Pully, Switzerland

2. DS Smith Plc – London, United Kingdom

3. Amcor Plc – Zurich, Switzerland (Global HQ, with major operations in Europe)

4. Mondi Group – Vienna, Austria

5. Smurfit Kappa Group – Dublin, Ireland

6. Stora Enso – Helsinki, Finland

7. Huhtamaki Oyj – Espoo, Finland

8. Constantia Flexibles – Vienna, Austria

9. Papacks – Cologne, Germany

10. Notpla Ltd. – London, United Kingdom

11. Sulapac Ltd. – Helsinki, Finland

12. BIO-LUTIONS International AG – Hamburg, Germany

13. Coveris Group – Vienna, Austria

14. Elopak – Oslo, Norway

15. Ranpak BV – Heerlen, Netherlands

Frequently Asked Questions:

1. Which region has the largest share in the Zero Waste Packaging Market?

Ans: The Europe region held the highest share in 2025.

2. What is the growth rate of the Zero Waste Packaging Market?

Ans: The Global Market is expected to grow at a CAGR of 4.6% during the forecast period 2026-2032.

3. What is the scope of the Global Zero Waste Packaging Market report?

Ans: The Global Zero Waste Packaging Market report helps with the PESTEL, Porter's, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in the Global Zero Waste Packaging Market?

Ans: The important key players in the Global Zero Waste Packaging Market are – Loop Industries Inc., PulpWorks, Inc., Lifepack, Avani Eco., Loliware, Aarohana Ecosocial Development, Package Free, Loliware, Biome Living Pty. Ltd., Smartpaddle Technology Pvt. Ltd., Waste-A-Weigh, and Relife Group.