Veterinary Diagnostics Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

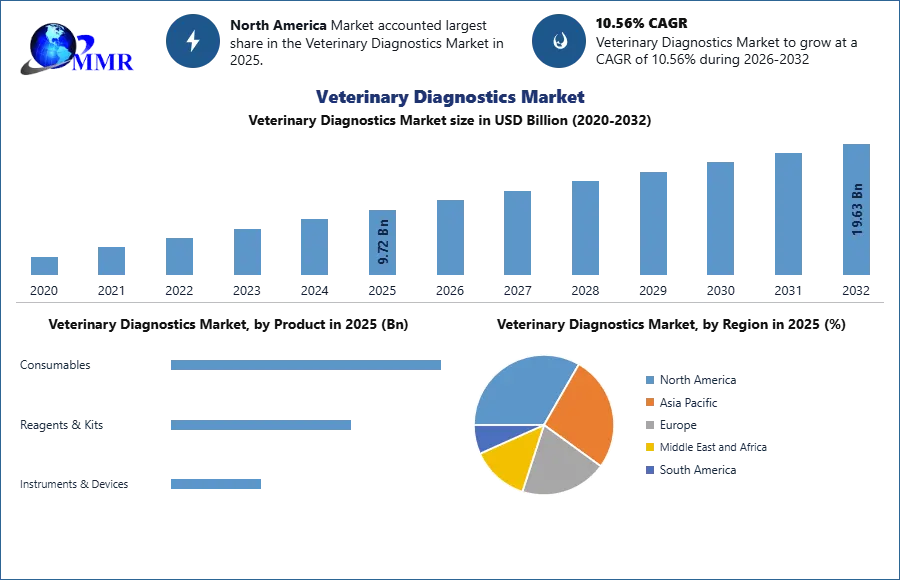

Global Veterinary Diagnostics Market size was valued at USD 9.72 Bn. in 2025, and the total Global Veterinary Diagnostics Market revenue is expected to grow by 10.56% from 2026 to 2032, reaching nearly USD 19.63 Bn.

Global Veterinary Diagnostics Market Overview

Veterinary diagnostics refers to the testing that detects, monitors, and analyzes diseases and health conditions in animals. It encompasses a wide range of technologies, including immunodiagnostics, molecular diagnostics, clinical biochemistry, and rapid point-of-care testing. These diagnostics play a crucial role in managing the health of livestock, companion animals, and wildlife.

The veterinary diagnostics market is experiencing significant growth as pet ownership increases, awareness of zoonotic diseases rises, and greater emphasis is placed on the preventive care of animals. The livestock industry is driving demand for diagnostic tests, prompted by new food safety regulations and demands for improved animal production practices, as well as veterinary use in emerging markets. Adoption of diagnostics in these emerging markets faces challenges around cost, rural infrastructure, and regulatory issues.

This report examines current market trends, levels of adoption by region, technology developments, and the activities of major companies involved in the veterinary diagnostics space. North America led the Veterinary Diagnostics Market in 2025, due to significant investments in veterinary healthcare infrastructure and the evolution of diagnostic technologies. Major players such as IDEXX Laboratories and Zoetis are leveraging advancements in molecular and digital platforms, which can reduce the time tests take, increase accuracy, and add to diagnostic or overall healthcare offerings. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Global Veterinary Diagnostics Market Dynamics

Increased prevalence of Tran-boundary and zoonotic diseases to Drive Veterinary Diagnostics Market growth

Approximately, 30 major diseases in humans are spread by animals. The majority of human illnesses are transmitted by household pets such as dogs and cats and livestock such as pigs, chickens, cattle, goats, and camels. Among the primary zoonotic illnesses transferred from animals to people are zoonotic gastrointestinal disease, leptospirosis, cysticercosis, zoonotic TB, and rabies. The occurrence of transboundary illnesses has also increased. For example, foot-and-mouth disease (FMD) was estimated to affect approximately 77% of the global livestock population in 2018 in countries across Africa, the Middle East, and Asia, as well as a small area of South America, with a morbidity rate of 100%. (In susceptible cattle populations).

The lack of Veterinary professionals in developing countries to Create Veterinary Diagnostics challenges

The global animal healthcare market is experiencing a scarcity of trained veterinarians and pathologists. This is especially true in developing regions such as APAC and Latin America, where there is a significant imbalance between demand and supply for veterinary specialists. According to the World Animal Health Information Database (2017), India had 180,821 veterinary practitioners. The basic rule is that at least one veterinary doctor for every 5,000 animals. According to Vet Extension (2018), India's overall livestock population was 512.05 million, implying a need for 60,000 veterinarians dedicated only to bovine animals. When chickens, sheep, goats, pigs, and other animals are included, the demand would increase. Currently, one of the key challenges restricting veterinarians' adoption of modern diagnostic technologies is a shortage of qualified veterinarians and diagnostic infrastructure, particularly in developing nations.

Expanding Access and Technological Advancements to Create the Veterinary Diagnostics Market Opportunity

The Global Veterinary Diagnostics Market is expanding primarily due to the rise in pet ownership, increased awareness of zoonotic diseases, and growth in the livestock sector. Key opportunities include the development of rapid point-of-care (PoC) diagnostics, which are essential in rural and emergency settings, as well as the growing use of AI-enabled platforms that enhance diagnostic accuracy. Companies like IDEXX Laboratories continue to dominate the PoC tool market. In the livestock industry, diagnostics for disease monitoring and surveillance are rapidly emerging, particularly in countries such as India and Brazil. Collaborative approaches to animal health, often led by government initiatives through public-private partnerships (PPPs), are enhancing access to animal healthcare and driving market demand for scalable diagnostic solutions.

Global Veterinary Diagnostics Market Segment Analysis

Based on Testing Type, In 2025, the Immunoassays (Immunodiagnostics) segment dominated the veterinary diagnostics market primarily due to its widespread application in detecting infectious diseases, hormone levels, and metabolic disorders in animals. Immunoassays such as ELISA and lateral flow tests offer rapid, highly sensitive, and cost-effective diagnostic solutions, making them the preferred choice for both point-of-care testing and laboratory analysis. The rising incidence of zoonotic diseases, coupled with increasing pet ownership and livestock health monitoring, has further fueled demand for fast and reliable diagnostic tools.

Additionally, continuous technological advancements, such as automated immunoassay analyzers and multiplex assays, have improved testing efficiency and accuracy, supporting their large-scale adoption by veterinary clinics, diagnostic laboratories, and animal health companies worldwide.

By End-Use, the Laboratories segment held the largest market share of about 49% in 2025 and is expected to lead the market at the end of the forecast period. Laboratory diagnosis is an essential component of any monitoring or control program. Most nations maintain a national laboratory that tests for Transboundary Animal Diseases (TADs) and offers assistance for national disease eradication and control programs, and these factors are driving the segment growth. Many national and state laboratories are creating quality assurance programs to ensure the trustworthiness of testing findings. Veterinary services rely on the diagnostic skills of the laboratory system to respond to TAD introductions and to offer the monitoring programs required to identify disease introductions and verify disease freedom.

The veterinary diagnostic laboratories are the foundation of any country's veterinary service. They include national, state, and private veterinary laboratories. These laboratories offer diagnostic testing and consulting for Transboundary animal illnesses, as well as animal surveillance, disease monitoring, import/export testing, consultation, and interpretation of diagnostic data, research, and quality assurance operations. In addition to interpreting test findings for clinical cases, laboratory professionals provide experience in the establishment of animal disease management and eradication programs. Participation in quality assurance and proficiency testing is growing, and many nations are working to get laboratory accreditation.

Veterinary diagnostic laboratories maintain and develop their competence in animal disease diagnostics, allowing veterinary services to respond to transboundary animal disease invasions as well as endemic disease issues.

Global Veterinary Diagnostics Market Regional Insights

North America led the Global Veterinary Diagnostics Market, thanks to its path-breaking veterinary healthcare infrastructure, pet ownership rates, and increasing demand for preventive animal healthcare. The U.S. regularly accounts for the largest share, providing advantages from relatively larger investments in R&D, more efficient reimbursement policies, and a growing public awareness of zoonotic diseases. Additionally, both government and private support of animal disease monitoring and surveillance programs enhances the creation constantly in North America.

Veterinary Diagnostics Market Government Funding

| Government/Program | Initiative | Funding | Focus Area |

| U.S. Department of Agriculture (USDA) | National Animal Health Laboratory Network (NAHLN) | USD 121 Mn. | Disease Surveillance & Diagnostic Testing |

| Canada (CFIA) | Veterinary Biologics Program | USD 60 Mn. | Animal Health Testing & Vaccine Regulation |

| NIH (USA) | One Health Initiative | USD 100 Mn. | Zoonotic Disease Research & Integrated Diagnostics |

Veterinary Diagnostic Market Competitive Landscape

The Global Veterinary Diagnostics Market is competitive, led by leading participants, and has a high rate of innovation and strategic growth. While the increased demand has spurred entry and investment for many players, the level of competition in the market is generally driven by technology differentiation and consolidation strategy. IDEXX Laboratories (US) is the leading participant in the Global Veterinary Diagnostics market, as it has implemented a strategy that complements a full suite of diagnostic tests and diagnostic instruments (e.g. analyzers) for companion animals and livestock.

Other notable players include Randox Laboratories (UK) and Virbac (France), who are solidifying their presence in global markets by augmenting their veterinary diagnostic capabilities to increase their response to demand in animal health solutions and zoonotic disease surveillance, which are growing areas across most external or emerging markets.

Global Veterinary Diagnostics Market Recent Development

| Company Name | Date | Recent Development |

| IDEXX Laboratories (USA) | Mar 2025 | Launched Cancer Dx canine lymphoma screening test in North America, Q1 revenues reached USD 998 M appropriate of record diagnostic utilization growth. |

| Zoetis (USA) | Feb 2025 | Received USDA conditional approval for its updated bird flu vaccine for poultry, bolstering livestock diagnostics . |

| Thermo Fisher Scientific (USA) | 2025 | Expanded its VetMX rapid assay series, adding new molecular and immunodiagnostic test kits for animal infectious diseases . |

| bioMerieux SA (France) | 2025 (planned) | Advanced deployment of its AdiaGENE veterinary molecular platform, targeting farm-animal infectious disease testing. |

| Heska (USA) | 2023–2025 | Following acquisition by Mars Petcare, Heska scaled up point-of-care diagnostic instrument distribution, strengthening its vet-clinic footprint |

Global Veterinary Diagnostics Market Trends

• The Increasing Role of Point-of-Care (PoC) Testing in Clinics and Farms

Altering the veterinary landscape by providing rapid point-of-care diagnostics that are accurate, accessible, and can now be obtained outside of a traditional lab setting.

A new partnership between Companion Animal Healthcare and HT BioImaging announced in March 2022 results in co-branded HTVet point-of-care imaging devices that will be marketed in the U.S. and Canada, increasing the accessibility of diagnostics in general practice.

• Integration of AI and Cloud-enabled Diagnostics

AI-enabled analysis and cloud-based platforms are improving data sharing between clinics and labs to simplify test interpretation.

IDEXX's Q4 2024 earnings report showed a strong uptake of its AI-enabled Cancer Dx screening test for canine lymphoma, made possible by integrated cloud-based diagnostics.

• Expansion of Mobile and Telemedicine-enabled Diagnostics

Mobile diagnostics and telehealth technologies offer new touchpoints for expanded access to veterinary services for medical professionals, owners, and patients, particularly in remote areas or underserved communities.

A rapid ASF detection kit was launched by the faculty at Assam Agricultural University (India) to detect African Swine Fever at the point-of-care in less than 10 minutes and was supported by the Department of Biotechnology, India.

Veterinary Diagnostics Market Scope: Inquire before buying

| Veterinary Diagnostics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 9.72 USD Billion |

| Forecast Period 2026-2032 CAGR: | 10.56% | Market Size in 2032: | 19.63 USD Billion |

| Segments Covered: | by Product | Consumables, Reagents & Kits Instruments & Devices |

|

| by Species | Cattle Canine Feline Caprine Equine Ovine Porcine Avian Others |

||

| by Testing Type | Analytical Services Diagnostic Imaging Bacteriology Pathology Molecular Diagnostics Immunoassays Parasitology Serology Virology |

||

| by Disease Type | Infectious Diseases Non-Infectious Diseases Hereditary, Congenital, and Acquired Diseases General Ailments Structural and Functional Diseases |

||

| by End-Use | Laboratories Veterinary Hospitals and Clinics Point-Of-Care/In-House Testing Research Institutes and Universities |

||

Global Veterinary Diagnostics Market by Region

North America (United States, Canada and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam, Indonesia, Philippines, Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America)

Key Players / Competitores Proflies Coverd Veterinary Diagnostics Market Report in Strategic Perspective

North America

1. IDEXX Laboratories Inc. (USA)

2. Zoetis Services LLC (USA)

3. Heska Corporation (USA)

4. Thermo Fisher Scientific, Inc. (USA)

5. Antech Diagnostics Inc. (Mars, Inc.) (USA)

6. VCA Animal Hospitals (Mars, Inc.) (USA)

7. Neogen Corporation (USA)

Europe

8. bioMérieux SA (France)

9. Virbac Corp (France)

10. Alvedia (France)

11. Randox Laboratories Ltd. (UK)

12. Biopanda Reagents (UK)

13. INDICAL BIOSCIENCE GmbH (Germany)

14. Fassisi GmbH (Germany)

15. QIAGEN N.V. (Germany)

16. Agrolabo S.p.A. (Italy)

Asia-Pacific

17. Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

18. Shenzhen Bioeasy Biotechnology Co. Ltd. (China)

19. BioNote Inc. (South Korea)

20. FUJIFILM Holdings Corporation (Japan)

21. IM3Vet Pty Ltd. (Australia)