SECTION A – GLOBAL UNIFIED THREAT MANAGEMENT MARKET INTRODUCTION

A1. Executive Market Landscape and Industry Overview

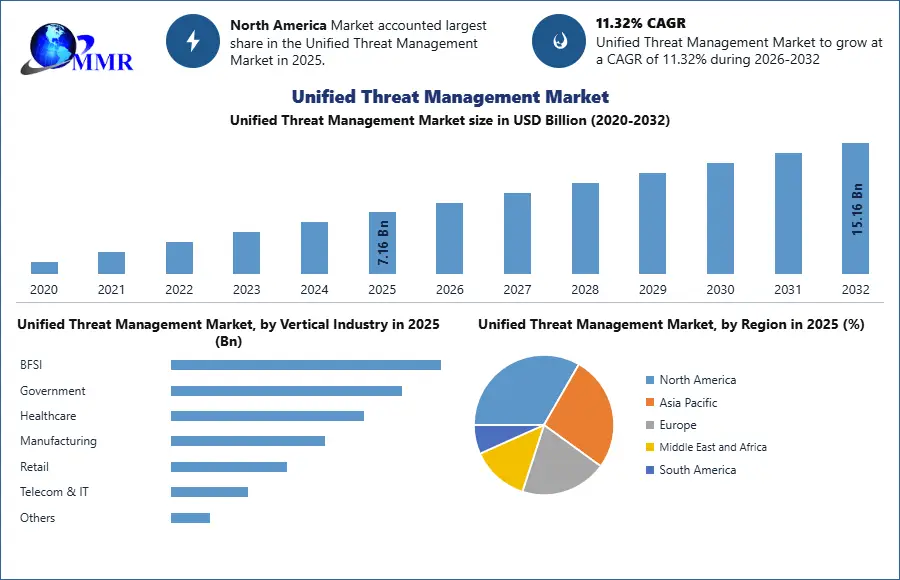

1.1. Global Unified Threat Management Market Size (Value USD Bn.), 2025–2032

1.2. Global UTM ecosystem definition, scope boundaries, and segmentation framework covering integrated cybersecurity platforms and network security integration

1.3. Adoption intensity comparison by region (cybersecurity maturity, cloud adoption pace, digital transformation levels, SME penetration, and enterprise IT security readiness)

1.4. Organized vs fragmented market structure mapping (global cybersecurity vendors, network security OEMs, MSSPs, and regional UTM providers)

1.5. Investor thesis: rising cyber threats, demand for unified security platforms, SME digitalization, cloud adoption, and cybersecurity cost optimization across industries

1.6. Competitive intensity and consolidation signals (cybersecurity partnerships, platform integration, AI-driven security innovation, product expansion, managed services growth, and M&A activity in the ecosystem)

A2. Global Unified Threat Management Market Dynamics

2.1. Unified Threat Management Market Trends

2.2. Unified Threat Management Market DROC

2.3. PORTER’s Five Forces Analysis

2.4. PESTLE Analysis

A3. IT Infrastructure, Cloud & Cybersecurity Convergence Framework

3.1. Evolution of enterprise IT infrastructure and increasing network complexity

3.2. Role of UTM in unified IT-security architecture consolidation

3.3. Convergence of IT operations and cybersecurity functions integration

3.4. Shift toward cloud, hybrid, and edge computing environments adoption

3.5. Transition from perimeter-based to integrated security models evolution

3.6. Impact of digital transformation on enterprise security design frameworks

A4. Cyber Threat Landscape & Intelligence Analysis

4.1. Rising frequency and sophistication of global cyberattacks landscape

4.2. Ransomware, phishing, and advanced persistent threats (APTs) growth

4.3. Expansion of attack surface due to cloud and remote work adoption

4.4. Industry-specific cyber risk exposure across key verticals

4.5. Role of threat intelligence in real-time security response systems

4.6. Predictive threat modeling and advanced detection capabilities

A5. Technology Evolution & UTM Functional Innovation

5.1. AI and machine learning integration in advanced UTM systems

5.2. Next-generation firewall and integrated security evolution trends

5.3. Automation and security orchestration capabilities enhancement

5.4. Cloud-native and virtual UTM platform development acceleration

5.5. Behavioral analytics and adaptive security systems innovation

5.6. Integration with SIEM, SOAR, and unified monitoring platforms

A6. Cost, ROI & Pricing Model Analysis

6.1. Cost comparison: UTM vs standalone security tools efficiency

6.2. ROI benefits for SMEs and large enterprises adoption

6.3. CAPEX vs OPEX-based security models evaluation

6.4. Subscription vs perpetual licensing structures evolution

6.5. Managed security services cost efficiency optimization

6.6. Pricing sensitivity across enterprise size segments

A7. Procurement, Adoption & Operational Behavior

7.1. Enterprise UTM procurement decision-making process analysis

7.2. Vendor selection criteria and evaluation factors framework

7.3. SME vs large enterprise adoption patterns comparison

7.4. Managed Security Service Provider (MSSP) dependency increase

7.5. Cybersecurity skill gap and operational challenges impact

7.6. Training and workforce readiness for UTM systems adoption

A8. Deployment Models & Infrastructure Maturity

8.1. Cloud vs on-premise vs hybrid deployment trends analysis

8.2. Multi-site and distributed enterprise security challenges growth

8.3. Network scalability and infrastructure readiness assessment

8.4. IoT and connected device security implications expansion

8.5. Edge computing integration in security environments evolution

8.6. Regional digital maturity variations across markets

A9. Regulatory, Compliance & Data Protection Landscape

9.1. Global cybersecurity regulations (GDPR, CCPA, etc.) framework

9.2. Industry-specific compliance frameworks implementation

9.3. Data localization and privacy laws enforcement trends

9.4. Auditability and reporting requirements strengthening

9.5. Compliance-driven security investments acceleration

9.6. Enterprise risk governance implications development

A10. Security Architecture & UTM Functional Stack

10.1. Evolution of layered UTM architecture frameworks

10.2. Integration of firewall, IDS/IPS, VPN, antivirus modules

10.3. Zero Trust security implementation via UTM platforms

10.4. Centralized monitoring and unified threat response systems

10.5. Interoperability with enterprise security ecosystems

10.6. Role of UTM in security consolidation strategies

A11. Vendor Ecosystem & Service Model Evolution

11.1. Global UTM vendor ecosystem structure mapping

11.2. Shift from product-based to service-based cybersecurity models

11.3. Role of MSSPs and cloud providers expansion

11.4. Channel ecosystem (VARs, SI partners, distributors) dynamics

11.5. Subscription-based security delivery models adoption

11.6. Market consolidation and strategic partnerships trends

A12. End-User Adoption & Use Case Analysis

12.1. SME vs large enterprise adoption patterns analysis

12.2. Multi-branch and distributed enterprise usage models

12.3. Industry-specific deployment use case scenarios

12.4. Cloud-first vs legacy IT adoption environments

12.5. Remote workforce security use case expansion

12.6. MSSP-driven deployment models growth

A13. Regional Security Maturity & Market Landscape

13.1. North America cybersecurity maturity leadership

13.2. Europe compliance-driven adoption patterns

13.3. Asia-Pacific SME-driven growth acceleration

13.4. Latin America emerging cybersecurity adoption trends

13.5. Middle East & Africa government-led initiatives expansion

13.6. Regional cloud readiness differences assessment

A14. Digital Transformation & Strategic Alignment

14.1. Alignment of cybersecurity with digital transformation strategies

14.2. Security-first architecture in modernization programs adoption

14.3. UTM role in enterprise risk management frameworks

14.4. Integration into business continuity planning strategies

14.5. Board-level cybersecurity investment decision trends

14.6. Security in digital-first business model evolution

A15. Market Outlook & Future Evolution

15.1. Transition toward AI-driven autonomous security systems

15.2. Evolution toward XDR and unified cybersecurity platforms

15.3. Expansion of Zero Trust architecture adoption globally

15.4. Growth of fully cloud-native security ecosystems

15.5. Decline of legacy standalone security tools usage

15.6. Long-term convergence of IT and cybersecurity platforms

A16. Security Performance, Benchmarking & KPIs Analysis

16.1. UTM performance benchmarking across vendors and solutions

16.2. Threat detection accuracy and false positive rate analysis

16.3. Network latency and performance impact of UTM deployment

16.4. System uptime, reliability, and service availability metrics

16.5. Security incident response time performance evaluation

16.6. Benchmarking against next-generation security platforms (NGFW, XDR)

A17. Industry Digitalization & Vertical Security Intensity Index

17.1. Degree of digitalization across key industries

17.2. Cybersecurity intensity across BFSI, healthcare, manufacturing, etc.

17.3. Industry-specific dependency on network security systems

17.4. Variation in UTM adoption intensity by vertical

17.5. Risk-weighted cybersecurity investment priorities by industry

17.6. Digital maturity vs cybersecurity maturity correlation

A18. Security Investment & Enterprise Budget Allocation Trends

18.1. Enterprise cybersecurity budget allocation trends

18.2. Share of UTM in overall cybersecurity spending

18.3. Shift toward managed security service spending

18.4. IT vs cybersecurity budget convergence trends

18.5. SME cybersecurity investment constraints

18.6. Future investment outlook for unified security platforms

A19. Global Unified Threat Management Market size and Forecast by Segmentation (by Value USD Billion) (2025-2032)

19.1. Global Unified Threat Management Market Size and Forecast, By Component

19.1.1. Hardware

19.1.2. Software

19.2. Global Unified Threat Management Market Size and Forecast, By Service

19.2.1. Consulting

19.2.2. Managed UTM

19.2.3. Support & Maintenance

19.3. Global Unified Threat Management Market Size and Forecast, By Deployment Mode

19.3.1. Cloud-based

19.3.2. On-premise

19.4. Global Unified Threat Management Market Size and Forecast, By Enterprise Size

19.4.1. Large Enterprises

19.4.2. Small and Medium-Sized Enterprises (SMEs)

19.5. Global Unified Threat Management Market Size and Forecast, By Distribution Channel

19.5.1. Direct Sales

19.5.2. Value Added Resellers (VARs)

19.5.3. Distributors

19.6. Global Unified Threat Management Market Size and Forecast, By Vertical Industry

19.6.1. BFSI

19.6.2. Government

19.6.3. Healthcare

19.6.4. Manufacturing

19.6.5. Retail

19.6.6. Telecom & IT

19.6.7. Others

SECTION B – COMPETITIVE INTELLIGENCE & INDUSTRIAL ECOSYSTEM

B1. Company Profiles: Key Players

1.1. Global UTM & Network Security Platform Leaders (Large-scale enterprise security, global presence, integrated cybersecurity platforms)

1.1.1. Fortinet, Inc. (global leader in UTM and next-generation firewall platforms)

1.1.2. Cisco Systems, Inc. (enterprise security leader with integrated UTM, Firepower, and SecureX ecosystem)

1.1.3. Check Point Software Technologies Ltd. (advanced UTM gateways and unified security architecture provider)Palo Alto Networks (next-generation UTM and cloud-native security platform leader)

1.1.4. Sophos Ltd. (SME-focused UTM appliances and endpoint-integrated security solutions)

1.2. Tier-2 Security Appliance & Managed Security Providers (Mid-market UTM and hybrid security expertise)

1.2.1. WatchGuard Technologies, Inc. (SMB-focused UTM appliance and network security solutions)

1.2.2. SonicWall Inc. (UTM appliances with strong SME and branch office penetration)

1.2.3. Barracuda Networks, Inc. (cloud-connected UTM and firewall security platforms)

1.2.4. Juniper Networks, Inc. (SRX firewall-based UTM and AI-driven network security solutions)

1.2.5. Huawei Technologies Co., Ltd. (UTM-enabled enterprise and telecom network security systems)

1.3. Tier-3 Regional & Specialized Security Vendors (Cost-efficient and localized cybersecurity solutions)

1.3.1. Hillstone Networks, Inc. (network security and UTM firewall solutions for mid-market enterprises)

1.3.2. Clavister (European UTM and cybersecurity appliance provider)

1.3.3. Comodo Security Solutions, Inc. (cloud-based UTM and endpoint security solutions)

1.3.4. Venustech (China-based network security and UTM appliance provider)

1.3.5. Zoho Corporation Pvt. Ltd. (ManageEngine-based network and security management tools)

1.3.6. Rohde & Schwarz (Cybersecurity division with secure network gateway solutions)

1.4. Emerging Cybersecurity & Next-Generation Security Players (AI-driven, cloud-native, and XDR-enabled security ecosystems)

1.5. SentinelOne (AI-powered endpoint and extended detection security platforms)

1.6. CrowdStrike Holdings, Inc. (cloud-native cybersecurity and threat intelligence leader)

1.7. Versa Networks (SASE and UTM-integrated SD-WAN security platform provider)

1.8. Proofpoint, Inc. (email security and advanced threat protection solutions)

1.9. A10 Networks (application security and DDoS protection integrated solutions)

1.10. ESET North America (endpoint and network security with UTM-adjacent capabilities)

B2. Competitive Benchmarking Matrix

2.1. Product portfolio comparison by security deployment type (hardware UTM, software UTM, cloud-based security, and SASE-integrated platforms) + enterprise application coverage (SME networks, branch security, cloud workloads, and hybrid IT environments)

2.2. Capability benchmarking: threat detection accuracy, latency performance, scalability, AI-based automation, cloud integration readiness, and centralized security management efficiency

2.3. Price-position mapping: premium enterprise cybersecurity platforms vs mid-range UTM appliance vendors vs cost-efficient SME-focused security providers

B3. Strategic Moves and Partnership Mapping

3.1. Strategic collaborations between cybersecurity vendors, cloud providers, and telecom operators for integrated UTM deployment expansion

3.2. Co-development initiatives in cloud-native security platforms, SASE architecture, and AI-driven threat intelligence systems

3.3. Regional expansion strategies through MSP partnerships, channel ecosystems, and enterprise digital transformation programs

3.4. M&A activity: acquisition of cybersecurity startups, cloud security platforms, and AI-driven threat detection firms

B4. Competitive Benchmarking & Brand Positioning

4.1. Market share comparison by deployment type (enterprise UTM appliances vs cloud-based UTM vs managed security services vs hybrid security platforms)

4.2. Product differentiation benchmarking (threat detection accuracy, integration capability, scalability, automation level, and deployment flexibility)

4.3. Geographic footprint comparison across North America, Europe, APAC, and Middle East cybersecurity adoption landscapes

4.4. R&D and innovation focus (AI-based threat intelligence, cloud-native security, automation, and Zero Trust integration) vs traditional appliance-based models)

B5. Competitive Intelligence & Strategic Performance Analysis

5.1. Year-over-Year (Y-o-Y) revenue growth rate (%) comparison across key cybersecurity and UTM vendors

5.2. Profit margin (%) comparison across enterprise security platforms and managed security service providers

5.3. Capital investment intensity (% of revenue) – R&D spending, cloud infrastructure expansion, and AI security development benchmarking

5.4. Revenue vs net earnings analysis – financial performance comparison across FY2025 / latest reporting cycle

B5. Company Profile: Key Players

6.1. Detailed Profile considering the parameters:

6.1.1. Overview

6.1.2. Business Portfolio

6.1.3. Financial Overview

6.1.4. SWOT Analysis

6.1.5. Strategic Analysis

6.1.6. Recent Developments

6.2. WatchGuard Technologies, Inc.

6.3. Sophos Ltd.

6.4. Huawei Technologies Co., Ltd.

6.5. IBM Corporation

6.6. Juniper Networks, Inc.

6.7. Hillstone Networks, Inc.

6.8. Cisco Systems, Inc.

6.9. Barracuda Networks, Inc.

6.10. SonicWall Inc.

6.11. Check Point Software Technologies Ltd.

6.12. Hewlett Packard Enterprise (HPE)

6.13. Fortinet, Inc.

6.14. Trend Micro Incorporated

6.15. ESET North America

6.16. Zoho Corporation Pvt. Ltd.

6.17. A10 Networks

6.18. SentinelOne

6.19. Venustech

6.20. Versa Networks

6.21. Proofpoint, Inc.

6.22. CrowdStrike Holdings, Inc.

6.23. Rohde & Schwarz

6.24. Palo Alto Networks

6.25. Comodo Security Solutions, Inc.

C. STRATEGIC OUTLOOK: GLOBAL UNIFIED THREAT MANAGEMENT MARKET

C1. Revenue Pool Mapping & Value Hotspots

1.1. Revenue distribution by deployment type (hardware-based UTM appliances, cloud-based UTM, software-defined security, managed security services, and hybrid security platforms)

1.2. Regional revenue concentration across North America, Europe, Asia-Pacific, and Middle East & Africa cybersecurity markets

1.3. SME vs enterprise vs government vs telecom security application mix and adoption intensity

1.4. Replacement demand versus new deployment driven by cloud migration, ransomware threats, and network modernization requirements

1.5. High-value cybersecurity solutions share and advanced AI-enabled UTM platform adoption rate (2025)

C2. Impact of Macro Drivers & Industry Trends on Market Expansion

2.1. Rapid growth in cyber threats, cloud computing adoption, and hybrid IT environments

2.2. AI, automation, and threat intelligence advancements driving intelligent security systems

2.3. Digital transformation and enterprise modernization accelerating cybersecurity investments

2.4. Data privacy regulations, compliance mandates, and sovereignty laws shaping security strategies

C3. Value-Led vs Volume-Led Competitive Strategy

3.1. Premium vendors focusing on AI-driven, integrated cybersecurity and advanced threat protection platforms

3.2. Volume-driven strategies in SME markets with cost-efficient UTM appliance deployments

3.3. Brand positioning of global cybersecurity leaders versus regional security solution providers

3.4. Managed security service agreements versus product-based security deployment models

3.5. Cost efficiency as a key driver in SME and mid-market cybersecurity adoption

C4. Portfolio Prioritization & Product Mix Strategy

4.1. Expansion of integrated UTM portfolios across enterprise, SME, and government applications

4.2. Growth in cloud-native, virtualized, and software-defined security solutions

4.3. Development of next-generation firewall, endpoint integration, and unified threat platforms

4.4. Focus on AI-powered threat detection, automation, and behavioral analytics systems

4.5. Integration of UTM with XDR, SIEM, and SASE-based security ecosystems

C5. Regional Expansion & Market Entry Roadmap

5.1. North America leadership in advanced cybersecurity innovation and enterprise security adoption

5.2. Europe compliance-driven market with strong GDPR and data protection requirements

5.3. Asia-Pacific rapid SME-driven growth and increasing digital infrastructure penetration

5.4. Latin America emerging cybersecurity adoption with growing enterprise digitization

5.5. Middle East & Africa expansion driven by government cybersecurity initiatives and digital transformation programs

C6. Pricing & Margin Sustainability Strategy

6.1. Subscription-based, license-based, and managed security pricing models across UTM solutions

6.2. Cost structure impact of hardware appliances, cloud infrastructure, and AI security capabilities

6.3. Managed security service contracts and long-term enterprise cybersecurity agreements

6.4. Pricing differentiation across SME, enterprise, and government cybersecurity deployments

6.5. Premium pricing driven by advanced threat intelligence, automation, and integration capabilities

C7. R&D & Product Strategy Linked to Commercial Outcomes

7.1. Development of AI-driven threat detection and automated security response systems

7.2. Innovation in cloud-native security architecture and virtual UTM platforms

7.3. Software-defined cybersecurity infrastructure and orchestration capabilities

7.4. Integration of hybrid security models across endpoint, network, and cloud environments

7.5. Advancements in Zero Trust architecture and adaptive security frameworks

C8. Customer Engagement & Long-Term Partnerships

8.1. Strategic partnerships with enterprises, governments, and managed security service providers

8.2. Collaboration with cloud providers, telecom operators, and technology integrators

8.3. Joint cybersecurity ecosystem development with regulatory bodies and industry alliances

8.4. Long-term managed security agreements for continuous threat monitoring and protection

C9. Delivery Model & Operational Strategy

9.1. Security deployment aligned with enterprise IT modernization and cloud migration cycles

9.2. Integration of cloud-based, on-premise, and hybrid UTM deployment models

9.3. Operational scalability through centralized security orchestration and automation tools

9.4. Optimization of cybersecurity infrastructure through standardized deployment frameworks

9.5. Remote monitoring and centralized management of distributed security environments

C10. Business Model & Value Proposition Canvas

10.1. Key partners including cloud providers, cybersecurity vendors, and MSSPs

10.2. Core value proposition centered on unified threat protection, scalability, and cost efficiency

10.3. Target segments covering SMEs, enterprises, government, and telecom sectors

10.4. Revenue streams from hardware appliances, subscriptions, and managed security services

C11. Risk & Downside Scenarios (2026–2032)

11.1. High complexity of cybersecurity infrastructure limiting SME adoption in cost-sensitive markets

11.2. Operational risks due to skill shortages, system misconfiguration, and cyberattack sophistication

11.3. Regulatory changes and compliance burden impacting deployment flexibility

11.4. Supply chain risks affecting hardware availability and cybersecurity technology components

C12. Investment & M&A Priorities

12.1. Acquisition of cybersecurity startups specializing in AI, cloud security, and threat intelligence

12.2. Strategic partnerships between global vendors and MSSPs for market expansion

12.3. Investment in Zero Trust architecture, XDR platforms, and automation-driven security systems

12.4. Expansion of cloud infrastructure and cybersecurity innovation capabilities

C13. 7-Year Strategic Roadmap (2026–2032)

13.1. Revenue growth driven by increasing cyber threats, cloud adoption, and digital transformation

13.2. Strengthening of unified cybersecurity platforms across enterprise and SME markets

13.3. Scaling partnerships across cloud providers, MSSPs, and enterprise clients globally

13.4. Expansion of AI-driven, automated, and integrated cybersecurity ecosystems

13.5. Regional penetration growth led by Asia-Pacific, North America, and Europe cybersecurity markets

SECTION D: INSIGHTS & ACTIONABLE RECOMMENDATIONS

D1 . Key Findings

D2. Strategic Moves & Industry Outlook

D3. Research Methodology