Tokenization Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2030

Overview

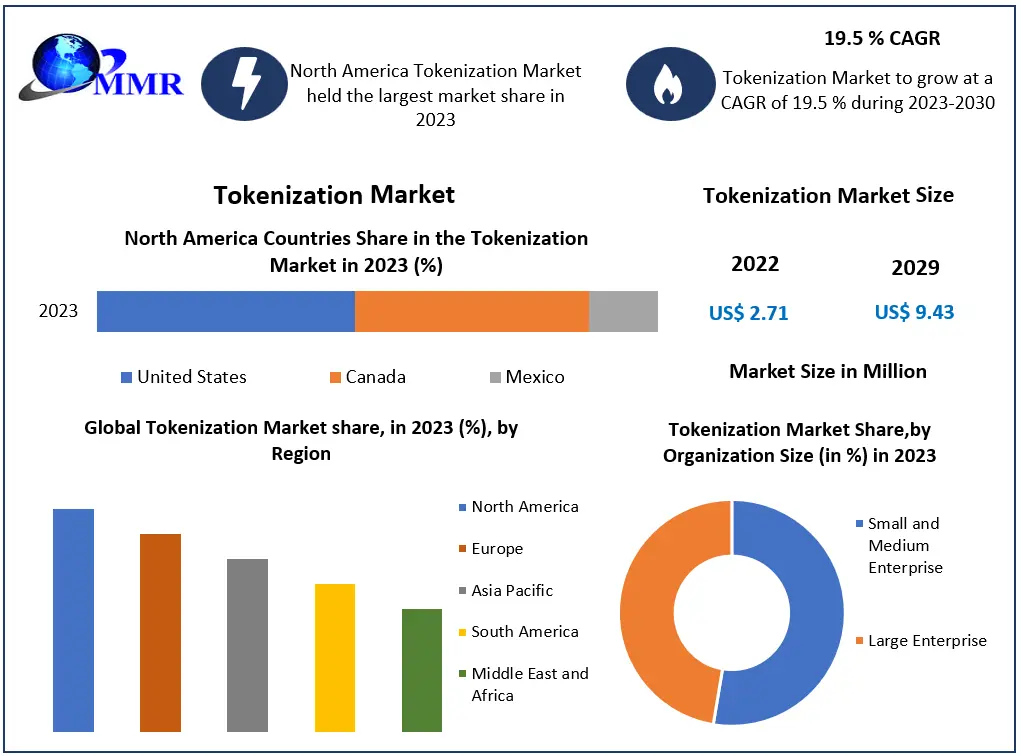

Global Tokenization Market size was valued at USD 2.71 Bn in 2023 and is expected to reach USD 9.43 Bn by 2030, at a CAGR of 19.5%.

Tokenization Market Overview

Tokenization involves substituting sensitive data with distinct identification symbols that preserve crucial information without compromising security. Businesses, particularly small and midsize ones, adopt tokenization to reduce the storage of sensitive data, enhancing security in credit card and e-commerce transactions. This approach minimizes the complexities and expenses associated with adhering to industry standards and government regulations while ensuring data security. Tokenization serves as a method to substitute sensitive data such as PANs, PHI, and PII with surrogate values or tokens. In the dynamic landscape of encryption methodologies, where data transforms unintelligible text necessitating decryption, tokenization distinguishes itself by maintaining the format of sensitive information. It converts such data into non-sensitive tokens, possessing equal length and structure. These tokens, a cornerstone in the Tokenization Market, preserve essential characteristics of the original data, including character set and length, ensuring strong security without compromising key attributes.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The Tokenization Market growth is primarily boosted by mounting apprehensions regarding data security breaches and privacy violations, sparking widespread adoption of tokenization solutions across diverse industries. This surge is particularly boosted by the exponential increase in digital transactions, particularly witnessed in the e-commerce, banking, and healthcare sectors. This increase in digital interactions has intensified the need for secure data handling, substantially amplifying the demand for tokenization methodologies. The presence of stringent regulatory frameworks such as GDPR and PCI DSS acts as an essential force, compelling organizations not only to adhere to but surpass compliance standards. This regulatory landscape fortifies the market's upward trajectory. The industry's horizons increase with the pervasive adoption of cloud-based infrastructures and seamless integration of IoT devices across sectors. This integration significantly broadens tokenization applications, empowering secure data transmission and storage within these advanced technological ecosystems.

Tokenization Market Dynamics

Increasing focus on data security and compliance with regulations to boost Market Growth

As organizations confront an increasing array of cyber threats and data breaches, safeguarding sensitive information becomes paramount. Tokenization, as a strong security measure, has gained prominence for its efficacy in thwarting unauthorized access and breaches, offering protection against hackers, viruses, physical theft, and inadvertent data loss. The burgeoning landscape of data protection regulations, spanning issues of residency, governance, and disclosure, compels enterprises to prioritize data security and compliance. Significant regulations such as the PATRIOT Act, GDPR, Privacy Act, Personal Data Protection Act, Digital Privacy Act and LGPD, among others, underscore the global imperative for stringent data protection measures. The EU's GDPR, serving as a foundational framework, emphasizes the secure processing of personal data, reinforcing the importance of measures ensuring confidentiality, integrity, and availability. The heightened focus on compliance standards such as NIST, FedRAMP, PCI, ISO27001, ISO27032, BSI, and IETF underscores the heightened priority placed on ensuring adherence to robust security and regulatory frameworks. In this landscape, the tokenization market emerges as a strategic solution, aligning with the imperative for secure data handling and compliance with evolving global regulations.

The surge in attention towards bolstering data security and adhering to regulatory requirements is poised to drive the growth of the tokenization market. According to MMR, a substantial 75% of organizations are actively engaged in the collection and storage of sensitive data, either presently utilizing it or having strategic plans for future use. Tokenization emerges as a formidable solution in this landscape, safeguarding sensitive information by substituting it with tokens, which serve as substitutes for the original data.

For instance, in the case of a customer's 16-digit credit card number, tokenization replaces it with a randomized combination of numbers, letters, or symbols. This intricate tokenization process not only secures the customer's credit card details but also renders them impervious to potential attackers. Consequently, online payment transactions are significantly fortified, ensuring an increasing level of security. The growing emphasis on data protection and compliance is expected to boost the adoption of tokenization, positioning it as an essential component in fortifying the overall security posture of organizations which boosts the Tokenization Market.

Integration of Decentralized Finance (DeFi) is the lucrative opportunity for the Market Growth

The integration of the Decentralized Finance (DeFi) market represents a transformative shift in the financial landscape, leveraging cryptocurrency and blockchain technology to revolutionize traditional financial transactions. DeFi, aimed at democratizing finance, seeks to dismantle centralized institutions, replacing them with peer-to-peer relationships that offer a comprehensive range of financial services. This incorporates everything from everyday banking and loans to intricate contractual relationships and asset trading. The market features prominent partners such as Mudrex, BlackBull Markets, and Skilling, highlighting the growing acceptance of DeFi solutions. Operating on the principles of blockchain and cryptocurrency, DeFi disrupts conventional finance by empowering individuals through direct peer-to-peer exchanges, circumventing the need for intermediaries and fostering financial inclusivity. DeFi's expansive potential is vividly demonstrated across a spectrum of applications, encompassing decentralized exchanges (DEXs), e-wallets, stablecoins, non-fungible tokens (NFTs), and cutting-edge financial instruments like flash loans. In the dynamic landscape of the Tokenization Market, DeFi influencing and shaping various sectors with its innovative and decentralized financial tools.

This paradigm shift comes with inherent risks, including a lack of consumer protections, susceptibility to hacking, collateralization constraints, and the need for secure private key management. As the total locked value in DeFi protocols approaches INR 3 trillion, individuals seeking involvement are encouraged to start with the basics of setting up a crypto wallet, trading digital assets on decentralized exchanges, and exploring stablecoins for a gradual immersion into this dynamic and evolving financial ecosystem. The integration of DeFi not only challenges the established norms of centralized finance but also offers enthusiasts and investors an opportunity to participate in a decentralized, transparent, and globally accessible financial paradigm, albeit one that demands cautious and informed engagement.

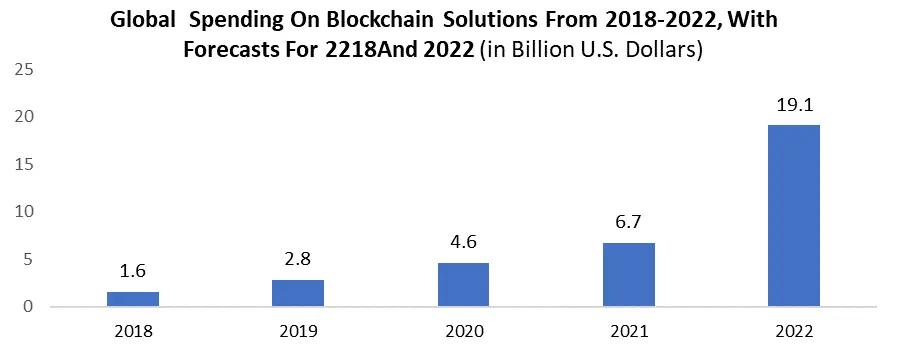

The Tokenization market is poised for substantial growth with the global surge in spending on blockchain solutions. The integration of Decentralized Finance (DeFi) amplifies its prospects, presenting a lucrative opportunity. As organizations increasingly invest in blockchain and embrace DeFi, the Tokenization market stands to benefit from this evolving landscape.

Interoperability challenges among different blockchain networks hamper Market Growth

The tokenization market faces formidable hurdles due to interoperability challenges among diverse blockchain networks. This hampers the seamless representation of real-world assets through digital tokens on blockchain platforms, limiting their portability between networks and impeding overall liquidity. The resulting ecosystem fragmentation confines tokenized assets to specific networks, hindering the formation of a unified marketplace. Interoperability issues introduce complexity, necessitating developers and businesses to adapt solutions to diverse protocols, leading to increased development costs and project delays. Concerns over data inconsistencies and security vulnerabilities arise, impacting accurate asset representation and ownership records across networks. Regulatory compliance complicates matters as different blockchain networks adhere to varied frameworks. While ongoing efforts, including cross-chain protocols and bridges, aim to address these challenges, achieving full interoperability is crucial for the seamless and secure transfer of tokenized assets, fostering market growth and widespread adoption.

Tokenization Market Regional Insights

North America dominated the Tokenization Market in 2023 and is expected to continue its dominance over the forecast period. The United States has shown a relatively positive and progressive regulatory stance towards blockchain technology and cryptocurrencies. Clarity and regulatory support provide a conducive environment for businesses and investors to explore tokenization opportunities. North America, and the U.S. in particular, boasts advanced technological infrastructure. This facilitates the development and deployment of blockchain and tokenization solutions, attracting tech-savvy entrepreneurs and enterprises to the market.

The region has a well-established and influential financial industry. Traditional financial institutions in North America are increasingly exploring blockchain and tokenization to enhance efficiency, reduce costs, and offer innovative financial products. North America has seen significant interest from institutional and retail investors in blockchain-based assets, including tokenized securities. This investor interest contributes to the growth and development of the tokenization market in the region. The region is home to a vibrant ecosystem of startups, tech companies, and blockchain-focused organizations. This ecosystem fosters innovation, leading to the development of new tokenization solutions and platforms. There is a high level of awareness and education about blockchain technology and its applications in North America. This facilitates greater acceptance and adoption of tokenization across various industries.

Tokenization Market Segment Analysis

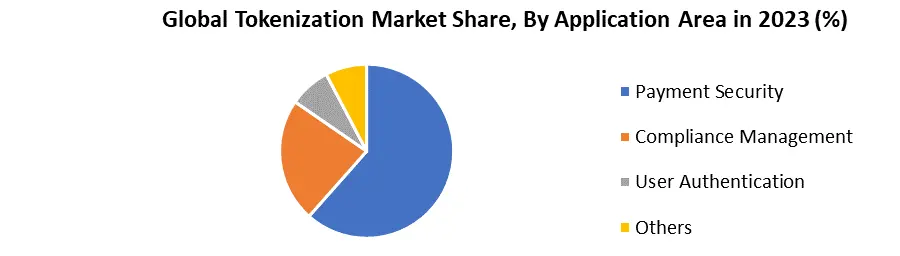

Based on the Application Area, the market is segmented into Payment Security, Compliance Management, User Authentication and Others. Payment Security is expected to have the highest growth rate over the forecast period. The payment industry handles highly confidential information, including credit card numbers and personal identification details, making it a prime target for cyber threats. Tokenization addresses this vulnerability by replacing such sensitive data with tokens, rendering any intercepted information meaningless without the corresponding tokens. Compliance requirements, particularly the Payment Card Industry Data Security Standard (PCI DSS), mandate stringent security measures, and tokenization serves as a key solution to meet these standards. In the rapidly growing landscape of e-commerce and digital transactions, tokenization instills confidence in consumers engaging in online payments, contributing to the overall trustworthiness of payment platforms.

The adoption of tokenization is driven by the increase in mobile payments and digital wallets, where secure transactions are essential. As a standardized and widely accepted method, tokenization enhances security across the global payment ecosystem, gaining widespread acceptance from major financial institutions. The emphasis on payment security reflects the industry's commitment to protecting valuable financial information and maintaining consumer trust in the face of evolving cyber threats.

Global Tokenization Market Scope: Inquire before buying

| Global Tokenization Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 2.71 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 19.5% | Market Size in 2030: | US $ 9.43 Bn. |

| Segments Covered: | by Component | Tokenization Software Tokenization Services Tokenization Hardware Others |

|

| by Application Area | Payment Security Compliance Management User Authentication Others |

||

| by Tokenization Technique | Random Tokenization Format-Preserving Tokenization Hash-Based Tokenization Encryption-Based Tokenization Others |

||

| by Deployment Mode | On-premises Cloud-Based Hybrid Others |

||

| by Organization Size | Small and Medium Enterprise Large Enterprise |

||

| by End User | Financial Services and Banking Healthcare Retail and E-Commerce Government and Public Sector Others |

||

Tokenization Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Tokenization Key Players

Global

1. Gemalto NV (Thales) (La Défense, France)

2. Symantec Corporation (NortonLifeLock) (Tempe, Arizona, USA)

3. Square, Inc. (San Francisco, California, USA)

4. Vormetric (Thales) (San Jose, California, USA)

Tokenization Key players in North America

1. TokenEx (Oklahoma City, Oklahoma, USA)

2. Hewlett Packard Enterprise (HPE) (San Jose, California, USA)

3. First Data Corporation (Fiserv) (Brookfield, Wisconsin, USA)

4. CyberSource (Visa Inc.) (Foster City, California, USA)

5. Square, Inc. (San Francisco, California, USA)

6. CipherCloud ( San Jose, California, USA)

7. Apple Inc. (Cupertino, California, USA)

8. Mastercard (Purchase, New York, USA)

9. Verizon Communications Inc. (New York City, New York, USA)

10. Discover Financial Services (Riverwoods, Illinois, USA)

11. Bluefin(Atlanta, Georgia, USA)

Tokenization Key players in Asia Pacific

1. Square Enix Holdings Co., Ltd (Tokyo, Japan)

2. Ant Financial Services (Alipay) (China)

3. Ripple (Singapore)

Frequently Asked Questions:

1] What is the growth rate of the Global Tokenization Market?

Ans. The Global Tokenization Market is growing at a significant rate of 19.5% during the forecast period.

2] Which region is expected to dominate the Global Tokenization Market?

Ans. North America is expected to dominate the Tokenization Market during the forecast period.

3] What is the expected Global Tokenization Market size by 2030?

Ans. The Tokenization Market size is expected to reach USD 9.43 Billion by 2030.

4] Which are the top players in the Global Tokenization Market?

Ans. The major top players in the Global Tokenization Market are Gemalto (Thales) (La Défense, France),Symantec Corporation (NortonLifeLock) (Tempe, Arizona, USA),Square, Inc. (San Francisco, California, USA),Vormetric (Thales) (San Jose, California, USA), TokenEx (Oklahoma City, Oklahoma, USA) and Others.

5] What are the factors driving the Global Tokenization Market growth?

Ans. Increasing concerns for data security, regulatory compliance demands and the increasing adoption of blockchain solutions are expected to drive market growth during the forecast period.