Thermoform Packaging Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2034

Overview

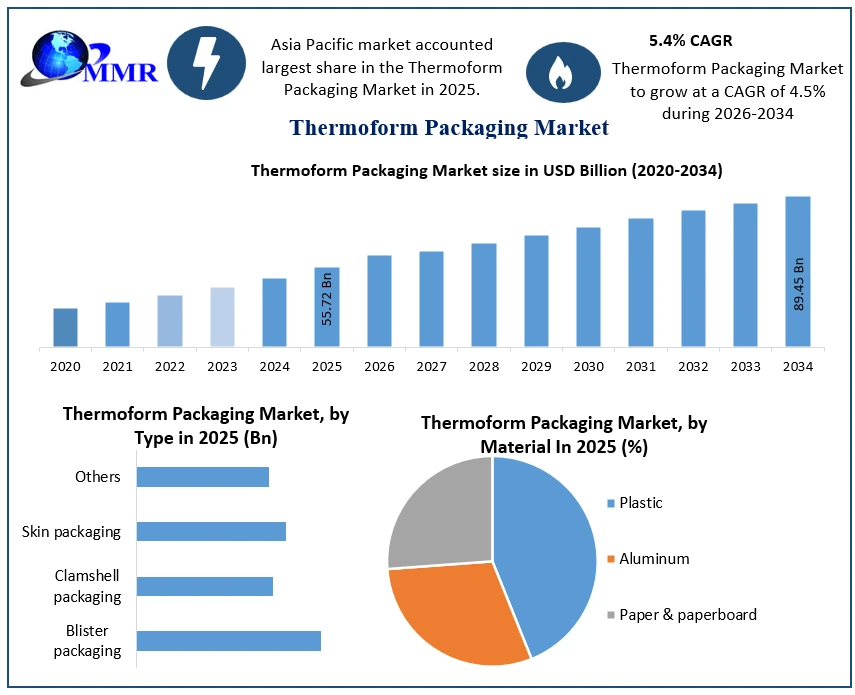

Thermoform Packaging Market was valued at US$ 55.72 Bn. in 2025 and the total Thermoform Packaging revenue is expected to grow at 5.4% from 2026 to 2034, reaching nearly US$ 89.45 Bn.

Thermoform Packaging Market Overview:

Thermoforming companies can provide better goods because of technological advancements in materials, tooling, and machinery. Now, parts may maintain high levels of efficiency and quality despite having undercuts, deep draws, and little draws. The thermoforming business has new potential and uses because of diverse materials including high-temperature polymers. Products that have been thermoformed are useful in most sectors because they have a wide range of applications. Food, medicine, automobiles, cosmetics, hardware, housewares, construction, audio/visual, appliances, transportation, office equipment, toys, military, and electronics are some of the major industries that rely on these products.

Thermoformers have grown so confident in their method since the 1980s that they have exceeded their expectations and built solid production lines that can create finished thermoformed products from resin pellets rather than sheets, in addition to recycling their waste with minimum oversight. Since the equipment is now digitized, self-monitoring and diagnostic functions are now possible.

Due to advancements in electronics, particularly intricate equipment does not currently require more than one person to handle and manage. Because indigenous knowledge would no longer be sufficient, the labor market for the thermoforming industry is expected to experience a shortage of trained and experienced technical staff. As a result, product launches and investments, etc., would serve to increase the general understanding of thermoformers among investors and industry professionals and grant this established industry greater maturity.

Thermoform Packaging Market Report Scope:

The Thermoform Packaging market is segmented based on Type, Heat Seal Coating, Material, End-Use Industry, and Region. The growth of various segments helps report users in acquiring knowledge of the many growth factors expected to be prevalent throughout the market and develop different strategies to help identify core application areas and the gap in the target market. The report provides an in-depth analysis of the market and contains meaningful insights, facts, historical data, and statistically supported and industry-validated market statistics. It also includes estimates based on an appropriate set of assumptions and methodologies.

The bottom-up approach has been used to estimate the market size. Key Players in the Thermoform Packaging market are identified through secondary research and their market revenues are determined through primary and secondary research. Secondary research included a review of annual and financial reports of leading manufacturers, while primary research included interviews with important opinion leaders and industry experts such as skilled front-line personnel, entrepreneurs, and marketing professionals. Some of the leading key players in the global Thermoform Packaging market include Amcor Limited, Bemis Company, and WestRock Company. They are continuously strategizing on mergers and acquisitions, strategic alliances, joint ventures, and partnerships for the growth of their market shares.

Thermoform Packaging Market Growth Outlook

To know about the Research Methodology:-Request Free Sample Report

Thermoform Packaging Market Dynamics:

3D Printed Thermoforming Tools:

In terms of production time, cost, and quality, additive manufacturing has radically transformed the way thermoformers and OEMs perceive tooling. Catalysis, a tool fabricator, can 3D print tooling in half the time and at half the cost of traditional metal tooling while retaining the same level of quality. In addition, 3D printing enables the creation of more complicated tooling for low-to-medium volume manufacturing parts, overcoming limits imposed by traditional tooling design.

Darrell Stafford and Rick Shibko created Catalysis Additive Tooling in 2015. 3D-printed thermoforming tools may be produced in less than two weeks and at a far cheaper cost than aluminum tools. Although 3D printed tooling can be an excellent alternative to classic RenShape, wood, or aluminum tooling, it is simply one tool in the arsenal and will not replace traditional tooling. The technique that is ideal for the application is always determined by the project quantity, part size, and materials being made. Although alternative 3D printing technologies would work for thermoforming tools, binder jet 3D printing technology with a Catalysis coating package is often the best solution in terms of speed and cost. This special coating package provides the necessary strength and thermal qualities to the underlying 3D binder jet print to resist the thermoforming process. Different 3D printing methods can be integrated into a single tool in specific applications.

Supply Chain Issues within the Thermoforming Industry:

Delays in procuring tooling, resources to create the components, and keeping enough people to make the products are important concerns in the sector. The challenges of keeping teams together while adhering to timelines and commitments are crucial. Employees were unwilling to come to work during the pandemic, and some went missing unexpectedly during the worst of the outbreak when these items were most needed. Countless firms were forced to lay off staff to survive, or they lost key team members due to unexpected retirements or government incentives. Many folks are still dealing with this problem.

Supply chain concerns begin with basic materials. Suppliers agree to timeframes, while buyers plan their schedules based on this. Suppliers are unable to supply on time because they cannot obtain their supplies. Raw material volatility and price fluctuation have also occurred. Because of the inability to get replacement components rapidly, equipment maintenance and downtime have increased. Due to raw material shortages, the cost and lead time of any new equipment and tooling have increased. Because of government constraints, the sector has experienced man-made energy challenges. For example, California must balance its energy consumption by using wind, natural gas, and electricity.

Promising Machinery Improvements for Thermoforming:

Automation and improved temperature and speed control to enhance throughput and part quality, also faster die changeover configurations, and equipment that operates within a cell to reduce human participation are the most alluring and emerging machinery improvements. CNC routers and robots have significantly advanced in the field of component trimming to reduce time and increase part quality. There have also been several improvements in the thin-gauge sector for full automation and reduced manpower.

AI interactive tools for real-time FAT (Factory Acceptance Test) and SAT (Site Acceptance Test) values have greatly aided distant involvement and problem-solving throughout the pandemic. Due to the COVID outbreak, there has been a strong drive for equipment with characteristics that reduce work and exposure. Material advances have enhanced plug aids for improved material distribution and down gauging.

Molds and tools must be able to communicate with machines. Machines must be capable of providing all input to the user. These qualities are not frequently seen in heavy-gauge processing equipment. Process optimization is critical for cost and throughput control. The advancements made in the thin-gauge industry's equipment would also greatly boost efficiency in heavy-gauge thermoforming equipment. Companies need to figure out how to make technology more cost-effective and there is always a demand for constant development, ease of setup, and faster throughput.

Thermoform Packaging Market Segment Analysis:

By End-Use Industry, the food and beverage segment is expected to grow at a CAGR of 6.1% during the forecast period. Many thermoformed products in use today have been made to replace their original use forms; this situation has occurred so quickly that it is almost impossible to remember what they were; for example, it is difficult to remember that hamburgers were packed before single-piece polystyrene packaging or what material covered the interior of refrigerators. The list below begins with the product with the most thermoformed components manufactured and progresses in declining order to the product with the least production.

1. Packaging industry - The packaging sector has profited the most from the thermoforming process since its inception, owing to its high productivity and cost-benefits. Most packing machinery (blister) is now high-speed automated feeding. These "form-fill-seal" systems are used to package cosmetics, cold meats, soft beverages, sweets, stationery, and other items.

2. Takeaway industry - There are many thermoformed items utilized in the growing "takeaway" market, ranging from entire food containers (containers with partitions) to packaging for hamburgers, sandwiches, soft drinks, and so on. This industry often demands a print on thermoformed packaging. Trays, mugs, sandwich containers, hamburgers, hot dogs, and other similar goods may be printed before or after thermoforming.

3. Food packaging industry - The most common consumers of thermoformed containers are supermarkets. The materials utilized are low-cost thermoplastics. These containers are meant to be stacked or organized in various ways. Containers for meat, fruit, eggs, and vegetables are examples.

Consumer goods corporations were compelled by the COVID-19 outbreak to alter their plans and put a hold on the introduction of new products in several areas. As a result, brand owners not only required fewer redesigns but also deprioritized creative packaging, which has had a direct influence on the global packaging sector. Brand owners are expected to expedite their product-launch plans to meet unmet market demand as the world starts to recover from the present public health and economic crises. The outbreak has also altered consumer behavior, which has led to increased expectations for package performance. Businesses in the $900 billion global packaging market need to step up their game to remain competitive if they want to survive the new normal.

Thermoform Packaging Market Regional Insights:

Packaging is a diverse USD 950 billion-plus industry with an excellent annual growth potential of over 3%. Geographically, emerging markets are expected to drive the majority of this growth, with packaging consumption expected to rise by USD 100 billion between 2020 and 2025. During the same period, markets in Western Europe and North America are forecast to grow at a rate of roughly 1% per year, although from a big base, with developed market packaging consumption (including Japan and Oceania) expected to increase by nearly USD 22 billion by 2025.

Plastic bags are being prohibited or penalized all around the world. Consumer initiatives are putting pressure on stores to reduce packaging. With less efficient garbage disposal infrastructure, the developing world may set an example. Meanwhile, e-commerce is increasing the visibility of transit packing in people's homes and raising awareness of ideas such as voids in boxes. The pandemic has shifted customers' preferences for new channels of purchase, as seen by significant increases in e-commerce shipments and remote-delivery services.Overall, the claimed low cost of thermoforming comes with a considerable environmental cost.

When compared to photopolymer signage, thermoforming has a very substantial carbon footprint because of the huge quantity of materials used, the inability to recycle, and the high risk of errors. The European Commission announced a new Circular Economy Action Plan in March 2020, as part of the European Green Deal, Europe's new goal for sustainable growth. Over the next decade, at least EUR 1 trillion is estimated to be spent, with the EU budget contributing the most, EUR 503 billion, and national governments contributing another EUR 114 billion. The subsequent EUR 279 billion would primarily come from the private sector, with the idea being that loan guarantees from the European Investment Bank would incentivize corporations to pursue riskier green projects.

Consumers globally are increasing their spending at online stores. Consumers in the United States are estimated to spend twice as much on items purchased from online grocery retailers. China also experienced a 200% increase in the sale of fresh food through online channels in 10 days in January 2020 compared to 2019. Sales of meat and vegetables increased by more than 400% through online outlets. Consumers are likely to exert significant pressure on cleanliness and safety requirements. Additionally, customers are becoming increasingly price-conscious. This will result in a significant shift by packaging companies toward achieving scales to thrive in a competitive market.

Thermoform Packaging Market Ecosystem

Thermoform Packaging Market Scope: Inquire before buying

| Thermoform Packaging Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 55.72 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 5.4% | Market Size in 2034: | US $ 89.45 Bn. |

| Segments Covered: | by Type | Blister packaging Clamshell packaging Skin packaging Others |

|

| by Heat Seal Coating | Water-based Solvent-based Hot-melt-based |

||

| by Material | Plastic Aluminum Paper & paperboard |

||

| by End-Use Industry | Food & beverage Pharmaceuticals Electronics Home & personal care Others |

||

Thermoform Packaging Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Thermoform Packaging Market, Key Players are:

1.WestRock Company (US)

2. Lacerta Group (US)

3. DuPont (US)

4. DS Smith (UK)

5. Sonoco Products (US)

6. Anchor Packaging (US)

7. Tekni-plex Inc (US)

8. Display Pack (US)

9. Archer Daniels Midland (US)

10.Berry Global Inc. (US)

11.Blisterpak, Inc. (US)

12.Brentwood Industries, Inc. (US)

13.CJK Thermoforming Solutions (US)

14.D&W Fine Pack (US)

15.Dart Container Corporation (US)

16.DISPLAY PACK (US)

17.Dordan Manufacturing Company (US)

18.Fabri-Kal (US)

19.Genpak(US)

20.Bemis Co., Inc. (US)

21.Mondini SPA (Italy)

22.Amcor Limited (Australia)

23.CONSTANTIA (Austria)

24.Huhtamaki Group (Finland)

25.BASF SE (Germany)

Frequently Asked Questions:

1. Which is the potential market for Thermoform Packaging in terms of the region?

Ans. APAC is the potential market for Thermoform Packaging in terms of the region.

2. What are the opportunities for new market entrants?

Ans. 3D Printed Thermoforming Tools.

3. What is expected to drive the growth of the Thermoform Packaging market in the forecast period?

Ans. Promising Machinery Improvements for Thermoforming.

4. What is the projected market size & growth rate of the Thermoform Packaging Market?

Ans. Thermoform Packaging Market was valued at US$ 55.72 Bn. in 2025 and the total Thermoform Packaging revenue is expected to grow at 5.4% from 2026 to 2034, reaching nearly US$ 89.45 Bn.

5. What segments are covered in the Thermoform Packaging Market report?

Ans. The segments covered are Type, Heat Seal Coating, Material, End-Use Industry, and Region.