Technical Foam Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2030

Overview

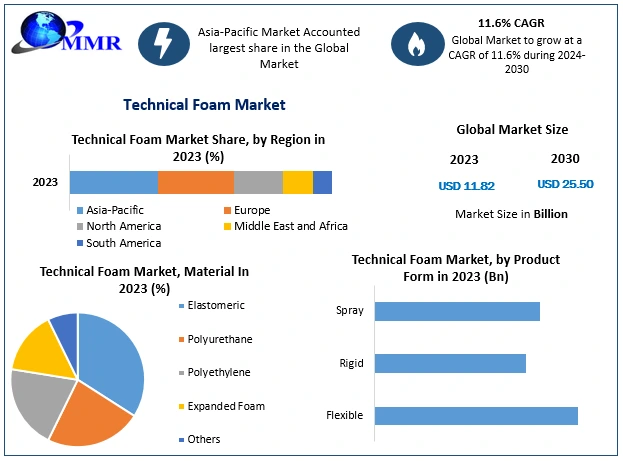

Technical Foam Market was valued at USD 11.82 Billion in 2023, and it is expected to reach USD 25.50 Billion by 2030, exhibiting a CAGR of 11.6 % during the forecast period (2024-2030)

Bio-based foams in Technical Foam Market are not a new concept, but the trend is still alive and well, thanks to fresh product developments. TR-EECell foam product line (N and RN bio-based grades) received DIN CERTCO bio-based certification at the highest level (>85% Bio-based) in 2019. TR-EECell is a cross-linked polyethylene foam that is bio-based. The product is nearly completely composed of raw ingredients obtained from biomass (sugar cane). The ethanol required for the foam is derived from fermented sugar cane juices extracted during the final three squeezing operations, making it unfit for human consumption.

The polymers required for the manufacturing of bio-based PE foam are generated by polymerizing this ethanol. BioFoam is particularly eco-friendly thanks to its renewable materials. BioFoam can be reformed into a new foam product or recycled into solid PLA after usage. Furthermore, vehicle manufacturers employ Woodbridge's bio-based PU foam products for applications such as seating systems, interior elements, headrests, headliners, and trim coverings. Its bio-based foams can replace up to 16% of polymer-based energy-absorbing materials.  To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Technical Foam Market Dynamics

Demand from the Electronics Industry for Foam-Based Packaging to drive Technical Foam Market

Technical foams absorb stress and vibration while providing cushioning capabilities, making them an ideal choice for electronic equipment protective packaging. During the forecast period, the global electronics market is expected to rise substantially. Furthermore, the growing middle-class population increases demand for consumer gadgets. The rapid expansion of internet services in various major and emerging nations throughout the world is creating substantial development possibilities for the consumer electronics market, which is expected to enhance foam-based electronic packaging solutions such as clamshells and cases. The rise of e-commerce logistics is likely to drive more demand for electronic packaging.

Demand from the Automotive Industry for Technical Foam Market

The automotive industry was a key driver of technical foams in 2023 and is likely to continue to be a prominent contributor over the forecast period. Foams are primarily used in the automotive sector to improve fuel efficiency, comfort, noise dampening, and the protection of in-vehicle equipment. Automotive foam materials offer a broad range of applications, including large commercial vehicles and small commercial vehicles. Polymeric foams are lightweight by nature, allowing the industry to build low-emission, fuel-efficient cars.

Increasing Demand for Building Insulation to drive Technical Foam Market

Foam-based insulation solutions are crucial in terms of energy savings. According to the Association of Plastics Manufacturers in Europe (APME), one kilogramme of oil used to create expanded polystyrene for a building saves the equivalent of 75 kg of oil over the course of 25 years. Polystyrene foams have a high strength-to-weight ratio and can bear a large level of load, allowing them to replace traditional heavy materials in construction. Furthermore, technological foams contribute to larger energy savings by insulating the interior temperature. As a result, effective foam material selection is intended to limit air, water, vapour, and temperature transmission in a structure.

Increasing Demand from the Healthcare Industry

Global healthcare spending is expected to grow during the forecast period. The need for medical grade cushioning and packing is expected to expand as the population grows and healthcare expenditure rises. Orthopedic implant packing is made from foam materials such as XLPE and PU. Medical device packaging and custom thermoforming into trays or clamshells employ rigid polyester and polypropylene foams. Foam-based medical packaging helps to protect the integrity of the packaged product, allowing it to meet stringent quality control standards.

Environmental Concerns Pertaining to Foam Materials

The availability of a diverse selection of eco-friendly alternatives, as well as increased government awareness about environmental difficulties caused by plastics, are expected to have a negative influence on market growth. Spray polyurethane foam is a typical construction insulation material that includes several chemicals that are harmful to people and other species. In packaging applications, for example, recycled plastics, bamboo fibre, and biodegradable polymers can replace traditional polystyrene foams. These new discoveries have a detrimental influence on market growth.

Technical Foam Market Segment Analysis

Based on Product Form, Flexible segment dominated the technical foam market in 2023. The fundamental reason for this is the versatility of flexible foams. Flexible foams are employed in the two largest end consumers of technical foams, the automobile and building industries. Furthermore, the leading competitors in the technical foams market provide innovation in their flexible foam products. Their product line ranges in density, thickness, and stiffness. Product diversification in flexible foams is expected to enhance market acceptance and consequently demand. Cushioning materials such as flexible foams are utilised in home and office furniture, beds, and car textiles. It is made up of many types of foam that are utilised for cushioning. They are used to provide acoustic and thermal insulation, as well as moisture, chemical, and flame protection.

Based on Material, Polyurethane segment dominated the technical foam market in 2023. The market is expected to develop due to a significant increase in demand for polyurethane foam in building, furniture, and automotive applications. Polyurethane is appropriate for different furniture foams and automobile seats due to its low density, low heat conduction coefficient, and low water absorption. The density of polyurethane foams used in cushion materials and couch sets is approximately four times that of ordinary rubber. Furthermore, advances in additive manufacturing for polyurethane foam enable for the printing of goods in customised sizes and forms for packaging applications, thus driving market development.

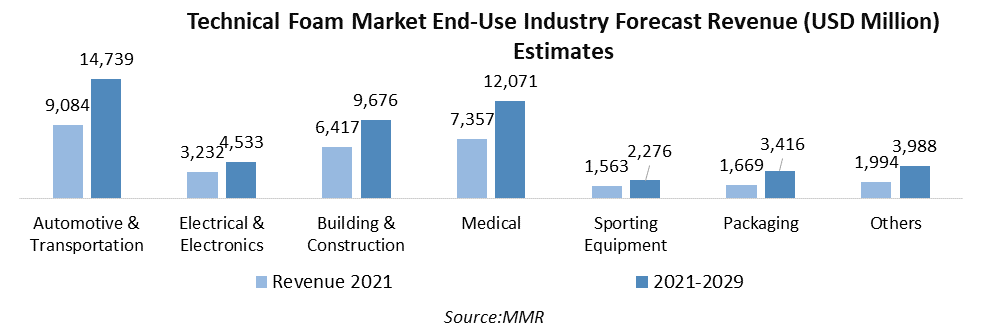

Based on End-Use Industry, Automotive & Transportation segment is expected to hold the highest technical foam market share during the forecast period. To improve fuel efficiency, the automobile industry focuses on decreasing total vehicle weight. Improving fuel efficiency while following environmental rules is expected to help this category develop during the forecast period. Aside from energy savings, the usage of foam components improves passenger comfort by decreasing outside sounds. These material solutions provide outstanding energy absorption, dampening, and acoustic insulation, allowing passengers to ride in peace and comfort. Flexible foam for vehicle seats with high durability and long-term comfort are gaining popularity among foam producers and car seat makers. As a result, an increase in the use of foam materials in automobile parts is expected to keep the market growing steadily.

Technical Foam Market Regional Insights

Technical Foam Market Regional Insights

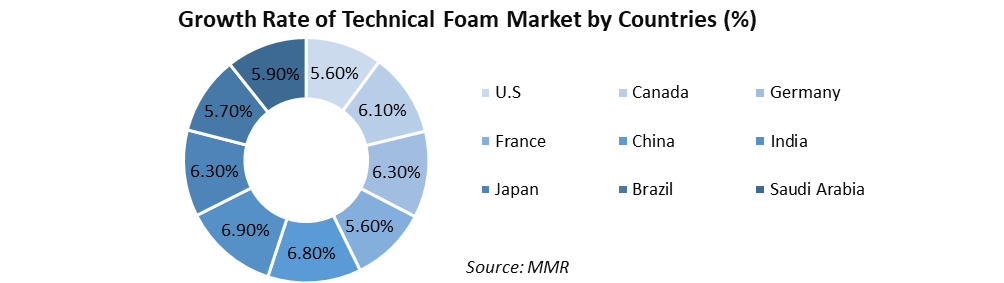

Asia Pacific region dominated the technical foam market in 2023 and is expected to witness a CAGR of 5.8% during the forecast period. China held 48.6% of the total market share in 2023. This is because the pace of construction activity in China has accelerated significantly during the previous decade. The medical industry is also increasing its need for foam products. Furthermore, China is the Asia-Pacific centre for low-cost electronics equipment manufacturing, including manufacturers such as Foxconn, Flextronics, and Jabil. Because of China's massive population and high consumer expenditure, it is the largest smartphone market in Asia-Pacific. Demand for rigid foam-based electronic packaging solutions is driven by such considerations. India, like China, will be an important area for the growth of the technical foam market over the forecast period.

China and India both have growing populations and rising wealth levels. As a result, the need for building insulation solutions rises. Dow Inc. announced on November 8, 2019, the launch of a new polyol factory producing rigid polyurethane foam in Rayong, Thailand, to be used for insulation products. During the forecast period, such new innovations are expected to generate profitable prospects for the technical foam market. The demand for technical foams for the construction sector is expected to increase throughout the forecast period in order to meet the expanding population and urban infrastructure. Polymer foams account for over 70% of total output generated locally. As per capita income and private spending have increased, India has emerged as one of the world's major marketplaces for electronic items. Such reasons boost the country's demand for technical foams.

The presence of large producers like as Dow Inc. and Rogers Corporation are positive towards the growth of the region’s technical foam industry. Furthermore, growth in construction projects in various states in the United States contributes to market growth. Ongoing infrastructure expenditures and smart city initiatives are two important factors influencing the growth of the market for various technical foams. In North America, the residential sector is forecasted to develop rapidly in the United States, opening up new market prospects. According to the American Community Survey, two-thirds of localities with more than 5,000 residents in the United States are still overcrowded. This opens the way for additional residential structures to be built. Furthermore, high per capita income is a driver of growth in nations such as the United States and Canada. This is expected to fuel the region's automobile industry.

The presence of large producers like as Dow Inc. and Rogers Corporation are positive towards the growth of the region’s technical foam industry. Furthermore, growth in construction projects in various states in the United States contributes to market growth. Ongoing infrastructure expenditures and smart city initiatives are two important factors influencing the growth of the market for various technical foams. In North America, the residential sector is forecasted to develop rapidly in the United States, opening up new market prospects. According to the American Community Survey, two-thirds of localities with more than 5,000 residents in the United States are still overcrowded. This opens the way for additional residential structures to be built. Furthermore, high per capita income is a driver of growth in nations such as the United States and Canada. This is expected to fuel the region's automobile industry.

Technical Foam Market Scope: Inquire before buying

| Technical Foam Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 11.82 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 11.6% | Market Size in 2030: | US $ 25.50 Bn. |

| Segments Covered: | by Product Form | Flexible Rigid Spray |

|

| by Material | Elastomeric Polyurethane Polyethylene Expanded Foam Others |

||

| by End-Use Industry | Electricals & Electronics Automotive & Transportation Commercial Buildings Office Equipment Medical Others |

||

Technical Foam Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Technical Foam Market Key Players

North America:

1. Dow Inc. (US)

2. Huntsman Corporation (US)

3. UFP Technologies, Inc. (US)

4. Foam Fabricators (US)

5. Carpenter (US)

6. Pregis Corporation (US)

7. Sonoco Products (US)

8. Polyfoam Corporation (US)

9. Wm. T. Burnett & Co. (US)

Asia Pacific:

1. SEKISUI CHEMICAL CO., LTD (Japan)

2. INOAC Corporation (Japan)

3. Changzhou Tiansheng New Forms Co. Ltd. (China)

Europe:

1. BASF SE (Germany)

2. Armacell International S.A. (Germany)

3. LANXESS AG (Germany)

4. Trelleborg AB (Sweden)

5. Recticel NVISA (Belgium)

Middle East & Africa:

1. SABIC (Saudi Arabia)

Frequently Asked Questions:

1] What is the current size of the global Technical Foam market?

Ans. The current size of the global Polystyrene Foam market USD 11.82 Bn. in 2023.

2] What are the major players currently dominating the global Technical Foam market?

Ans. Dow Inc. (US), SEKISUI CHEMICAL CO., LTD (Japan), INOAC Corporation (Japan), Changzhou Tiansheng New Forms Co. Ltd. (China), Huntsman Corporation (US), UFP Technologies, Inc. (US), Foam Fabricators (US)are among the major players currently dominating the global Technical Foam market.

3] Which Technical Foam market segment has the potential to register the highest market share during the forecast period?

Ans. The Automotive & Transportation end-use industry segment has the potential to generate highest revenue share of the Technical Foam market, in terms of volume and value, during the forecast period.

4] Which is the dominating region in the global Technical Foam market?

Ans. Asia Pacific region is the dominating region in the global Technical Foam market. Countries like China, India, Taiwan, Japan, Malaysia, Thailand, South Korea are emerging economies with fastest-growing market share of the region.

5] What is the major factor driving the growth of Technical Foam market in the Asia Pacific region?

Ans. The easy availability of raw materials and high demand from end-use industries are factors driving the growth of Technical Foam market in Asia Pacific region.