Target Drone Market 2025–2032: Autonomous Target Systems, Weapon Testing, and Defense Training Driving Market Transformation

Overview

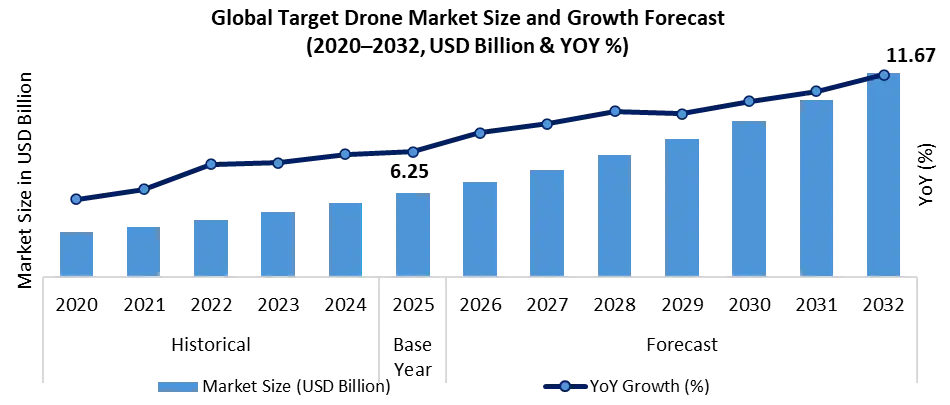

Global Target Drone Market Size was valued at USD 6.25 Billion in 2025 and is projected to reach USD 11.67 Billion by 2032, registering a strong CAGR of 8.12% during the forecast period. The Target Drone Market Size and Share are expanding steadily, driven by increasing adoption of cost-effective target drones for threat simulation, drone simulation systems, and defense training drone systems across global military forces.

The evolving target drones market ecosystem, supported by real-time data processing and advanced materials, is enhancing combat readiness and operational efficiency. The increasing complexity of multi-domain warfare and the need for adaptive training environments are key factors shaping market demand.

To know about the Research Methodology:-Request Free Sample Report

Target Drone Market Overview:

The Target Drone industry growth is supported by rising global defense spending, growing territorial conflicts, and the need for realistic combat training environments. The demand for target and decoy drones, weapon testing platforms, and ISR training systems is expanding as modern warfare becomes more complex and technology-driven.

Additionally, advancements in autonomous UAV systems, AI-enabled flight control, and high-performance propulsion technologies are improving the accuracy and reliability of target drones. However, challenges such as skilled workforce shortages and operational complexities persist. Ongoing defense contracts, partnerships, and R&D investments are expected to support steady expansion, partnerships, and R&D investments are expected to support steady expansion of the Target Drone Market during 2026-2032.

Target Drone Market Demand Analysis (2025)

• Defense Sector Dominance: Majority of demand originates from military forces for combat training, missile testing, and air defense evaluation.

• High Demand for Aerial Target Drones: Aerial platforms dominate (50%+ share) due to use in live-fire exercises and radar calibration.

• Preference for Remotely Piloted Systems: Higher consumption of remotely piloted target drones (55%+), driven by operational reliability and ease of deployment.

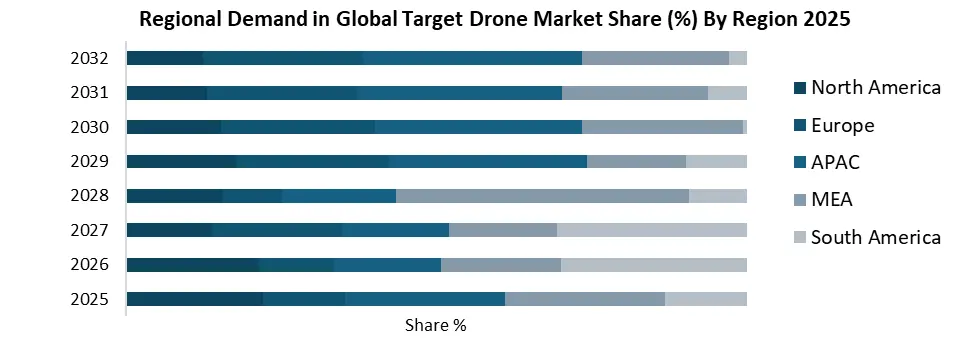

• Regional Demand Concentration

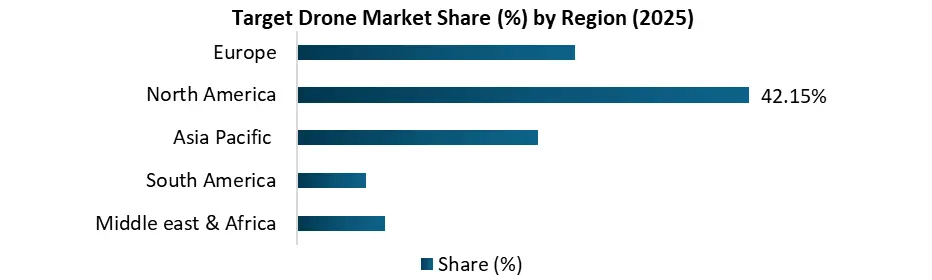

o North America leads (42.15% in 2025 due to high defense spending and advanced training infrastructure.

o Asia-Pacific is the fastest-growing region, supported by double-digit defense UAV procurement growth in India, China, and South Korea, driven by defense modernization and geopolitical tensions.

Growth Factors Target Drone Market:

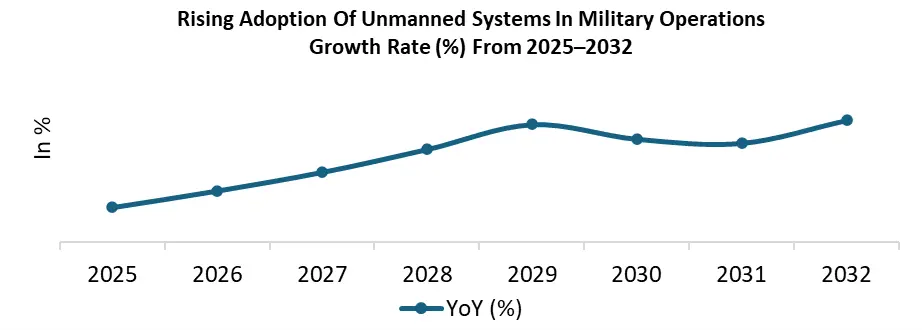

The Target Drone Market is driven by the rising adoption of unmanned systems in military operations, supporting applications like combat training, missile testing, and air defense simulation. The use of remotely piloted target drones reduces operational risks, lowers costs, and improves efficiency compared to manned systems. Growing demand for defense UAV systems, real-time training environments, and autonomous drone technologies is contributing to market expansion.

Advancements in military training technologies are further supporting growth, as target drones enable realistic combat scenario simulation across air, land, and marine platforms. Features such as infrared augmentation, AI-enabled systems, and advanced sensors enhance threat replication and training accuracy. Strong focus on defense modernization and technology-driven warfare continues to drive demand in the Target Drone Market.

Key Challenges Impacting the Target Drone Market Growth:

The Target Drone Market faces various operational and regulatory challenges that impact its growth. One of the key limitations is the short endurance and limited operational range of sub-scale target drones, which typically offer flight durations of only 1–2 hours, restricting their effectiveness in long-duration military training and realistic combat simulations. This limitation reduces their ability to accurately replicate advanced battlefield threats, thereby affecting training efficiency. Furthermore, the Target Drone Market is constrained by stringent government regulations related to UAV operations, including airspace restrictions and line-of-sight requirements, which limit the deployment of advanced target drone systems. These regulatory barriers hinder the adoption of beyond-visual-line-of-sight (BVLOS) operations, restrict innovation, and slow down investments in defense UAV technologies, ultimately impacting the overall growth of the Target Drone Market.

Target Drone Market Key Trends:

• Integration of Autonomous Flight Capabilities – Adoption of autonomous systems enabling precise and repeatable mission execution in training environments.

• AI-Enabled Navigation and Adaptive Target Systems – Use of artificial intelligence for dynamic threat simulation and real-time response adaptation.

• Expansion of Counter-Drone (C-UAS) Training Simulations – Growing use of target drones to replicate hostile UAVs for testing anti-drone and air defense systems.

• Miniaturization of Target Drones – Development of compact drones for enhanced operational flexibility and deployment across varied scenarios.

• Integration with Advanced Weapon and Missile Testing Systems – Increasing alignment of target drones with modern missile systems for realistic combat simulation.

• Advancements in Flight Control, Navigation, and Payload Capacity – Continuous improvements enhancing accuracy, endurance, and mission reliability.

Target Drone Market Segment Analysis:

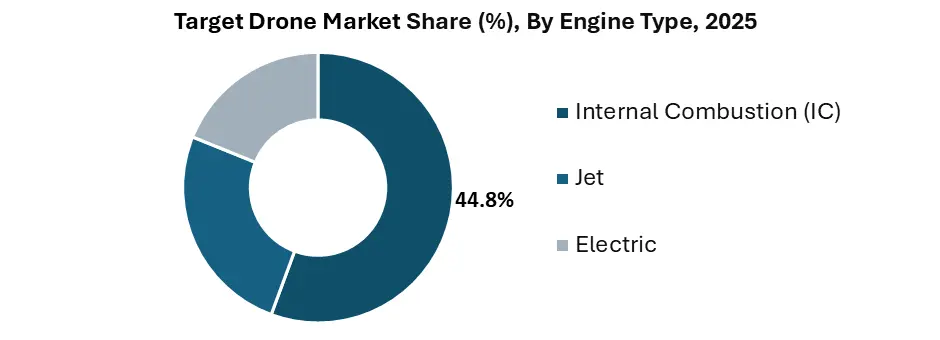

Based on Engine Type, Internal Combustion (IC) segment is positioned to lead the Target Drone Market, capturing a 44.8% revenue share in 2025. This growth is driven by its cost-effectiveness, operational reliability, and suitability for medium-range training missions. IC-powered drones are widely deployed across defense training programs due to their proven performance and lower operational complexity. Meanwhile, jet-powered drones are increasingly used for high-speed target simulation in advanced missile and radar testing, and electric drones are witnessing gradual adoption for low-noise, short-duration, and cost-sensitive training applications.

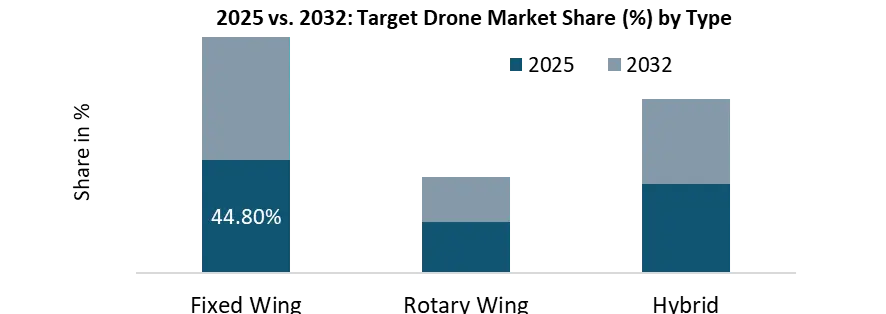

By Type, the Fixed-Wing Drones segment commands the largest revenue share at 58.92% in 2025 owing to its superior flight endurance and high-speed capabilities. Fixed-wing target drones are widely used in air defense exercises and long-range simulations, making them the preferred choice for defense agencies. In contrast, rotary-wing drones are utilized for short-range and low-speed training scenarios, while hybrid drones are gaining traction due to their multi-mission flexibility, although their adoption remains comparatively limited.

By Payload Capacity, the Medium (20–40 Kg) segment held the largest 42.13% share of the global Target Drone Market in 2025 as it offers an optimal balance between endurance, payload capacity, and cost efficiency. These drones are widely used across defense training and weapon testing applications, making them the most practical choice for military operations. The low payload segment is primarily used for basic training and short-range simulations, while the high payload segment supports advanced and high-performance simulations, though its adoption is limited due to higher costs and operational requirements.

Target Drone Market Regional Analysis:

In 2025, North America leads the Target Drone Market with a 42.15% share, supported by strong defense budgets, advanced military training infrastructure, and the presence of major defense contractors. The focus on combat readiness, missile testing, and air defense system evaluation is driving sustained demand for unmanned aerial targets (UATs) across the region. In Europe, growth is supported by NATO-led defense initiatives and increasing training exercises, particularly following the Russia–Ukraine conflict. Countries such as the U.K. are expanding their target drone fleets, with contracts aimed at strengthening air defense training capabilities, contributing to steady expansion of the Target Drone Market. The Asia-Pacific region is emerging as the fastest-growing market, driven by rising defense modernization programs, increasing territorial tensions, and expanding indigenous UAV development in countries such as China, India, and South Korea. Programs like India’s Abhyas and Lakshya and China’s UAV testing initiatives are supporting demand for target drone systems in both training and tactical applications.

The Asia-Pacific region is emerging as the fastest-growing market, driven by rising defense modernization programs, increasing territorial tensions, and expanding indigenous UAV development in countries such as China, India, and South Korea. Programs like India’s Abhyas and Lakshya and China’s UAV testing initiatives are supporting demand for target drone systems in both training and tactical applications.

In the Middle East, growing missile defense drills and investments in UAV training systems by countries such as Saudi Arabia and the UAE are strengthening market adoption. South America, led by Brazil, is witnessing gradual growth through air force modernization programs and the deployment of cost-effective aerial targets.

Target Drone Market Competitive Landscape:

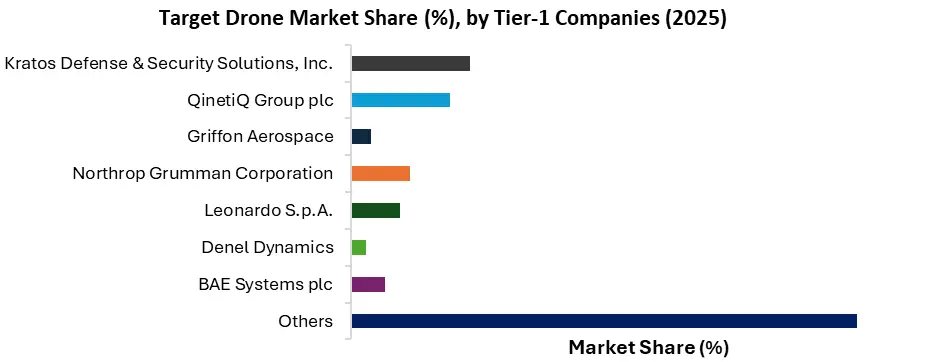

The Target Drone Market competitive landscape is moderately consolidated, with a mix of specialized target drone manufacturers and large defense OEMs focusing on advanced training systems, high-speed aerial target platforms, and autonomous UAV technologies. Key players are investing in AI-enabled target drones, jet-powered systems, and multi-domain training solutions to enhance combat simulation, missile testing, and air defense evaluation capabilities.

Leading companies include:

• Kratos Defense & Security Solutions, Inc. – Leader in high-performance aerial target systems and jet-powered target drones

• QinetiQ Group plc – Strong in advanced target drone solutions and defense training services

• Griffon Aerospace – Specializes in cost-effective target drones for military training applications

• Denel Dynamics – Focuses on high-speed target drones and missile testing systems

• Leonardo S.p.A. – Provides integrated defense training systems and target drone technologies

These companies are driving innovation in the Target Drone Market through defense contracts, product development, and strategic partnerships, strengthening their market share, competitive positioning, and technological capabilities in military UAV training and simulation systems.

Target Drone Market Recent Developments:

| Month & Year | Company | Development | Impact |

| January 2025 | QinetiQ Group plc | Continued global deployment of Banshee Jet 80+ target drones, with over 10,000 units produced. | ↑ Strengthens position in air defense training and expands global target drone adoption. |

| April 2025 | Kratos Defense & Security Solutions | Advanced production readiness of XQ-58 UAV variants for U.S. Marine Corps programs. | ↑ Enhances autonomous UAV capabilities and supports next-gen training & combat simulation. |

| July 2025 | Airbus & Kratos | Partnership to develop uncrewed combat drone (UCCA) for German Air Force. | ↑ Expands defense collaboration and drives innovation in high-end UAV and target simulation systems. |

Target Drone Market Scope: Inquire before buying

| Target Drone Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 6.25 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 8.12% | Market Size in 2032: | USD 11.67 Bn. |

| Segments Covered: | by Type | Fixed Wing Rotary Wing Hybrid |

|

| by Engine Type | Internal Combustion (IC) Jet Electric |

||

| by Target Type | Full-Scale Sub-Scale Free-Flying Towing |

||

| by Payload Capacity | Low (<20 Kg) Medium (20–40 Kg) High (>40 Kg) |

||

| by Mode of Operation | Remotely Piloted Autonomous Optionally Piloted |

||

| by Platform | Aerial Targets Ground Targets Marine Targets |

||

| by Component | Airframe Propulsion System Avionics & Navigation Systems Payload Systems Electrical Systems & Wiring Ground Control Station (GCS) |

||

| by Application | Combat Training Target & Decoy Weapon Testing & Evaluation Reconnaissance Training |

||

| by End User | Defense Commercial |

||

Target Drone Market by Region:

North America (United States, Canada, and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Ukraine, Austria, Poland, Portugal, Ireland, Switzerland, Romania, and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, Indonesia, Malaysia, Philippines, Thailand, Vietnam, and Rest of Asia Pacific)

Middle East and Africa (UAE, South Africa, Saudi Arabia, Bahrain, Kuwait, Oman, Qatar, Egypt, Nigeria, Israel, Turkey, Rest of ME&A)

South America (Brazil, Argentina, Chile, Colombia, and Rest of South America)

Key Players/Competitors Profiles Covered in the Target Drone Market Report in Strategic Perspective

North America:

• United States

1. Kratos Defense & Security Solutions, Inc.

2. Griffon Aerospace

3. AeroTargets International LLC

4. Northrop Grumman Corporation

5. The Boeing Company

6. Lockheed Martin Corporation

7. Raytheon Technologies Corporation

8. General Atomics Aeronautical Systems, Inc.

9. L3Harris Technologies, Inc.

10. Parsons Corporation

• Canada

11. CAE Inc.

12. L3Harris WESCAM

• Mexico

13. Hydra Technologies

Europe:

• United Kingdom

14. QinetiQ Group plc

15. BAE Systems plc

16. BlueBear Systems Research Ltd.

17. Ultra Electronics

• Germany

18. Rheinmetall AG

19. Airbus Defence and Space

• France

20. Safran Electronics & Defense

21. Thales Group

22. Dassault Aviation

• Italy

23. Leonardo S.p.A.

• Sweden

24. Saab AB

• Spain

25. Sistemas de Control Remoto (SCR)

26. Embention

• Finland

27. Robonic Ltd Oy

Asia-Pacific:

• China

28. China Aerospace Science and Technology Corporation (CASC)

29. AVIC (Aviation Industry Corporation of China)

• India

30. DRDO

31. Hindustan Aeronautics Limited (HAL)

• Japan

32. Mitsubishi Heavy Industries

• South Korea

33. Korea Aerospace Industries (KAI)

34. LIG Nex1

• Australia

35. Air Affairs Australia Pty Ltd.

Middle East & Africa:

• Israel

36. Israel Aerospace Industries Ltd. (IAI)

37. Elbit Systems Ltd.

• Turkey

38. Kadet Defence Systems

39. Turkish Aerospace Industries (TAI)

• United Arab Emirates

40. EDGE Group

41. Adcom Systems

• South Africa

42. Denel Dynamics

43. Paramount Group

South America:

• Brazil

44. Embraer Defense & Security

• Argentina

45. INVAP S.E.

FAQ – Target Drone Market

Q. What is the current size and outlook of the Target Drone Market?

Ans. The Target Drone Market is estimated to be valued at USD 6.25 Billion in 2025 and is projected to reach around USD 11.67 Billion by 2032, growing at a CAGR of 8.12% Over 2026-2032. Growth is supported by increasing defense spending, military training programs, and demand for advanced target simulation systems.

Q. What are the key factors driving the growth of the Target Drone Market?

Ans. Key drivers include rising adoption of unmanned systems, increasing combat training requirements, growing missile testing activities, and advancements in AI-enabled UAV technologies. The need for realistic threat simulation and cost-effective training solutions is also accelerating market demand.

Q. Which segments dominate the Target Drone Market?

Ans. Fixed-wing target drones dominate due to their long endurance and high-speed simulation capabilities. By engine type, internal combustion drones lead due to cost efficiency, while medium payload drones (20–40 Kg) hold the largest share due to their balance of performance and affordability.

Q. What are the major challenges in the Target Drone Market?

Ans. Major challenges include limited endurance of sub-scale drones, high initial costs for advanced systems, and stringent UAV regulations related to airspace and operations. Additionally, the shortage of skilled operators impacts deployment efficiency.

Q. What are the emerging trends in the Target Drone Market?

Ans. Key trends include the integration of AI and autonomous systems, growth in counter-drone (C-UAS) training, adoption of jet-powered high-speed drones, and increasing use of multi-domain training platforms. Continuous investment in next-generation UAV technologies is shaping future market growth.