Aircraft Flight Control System Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

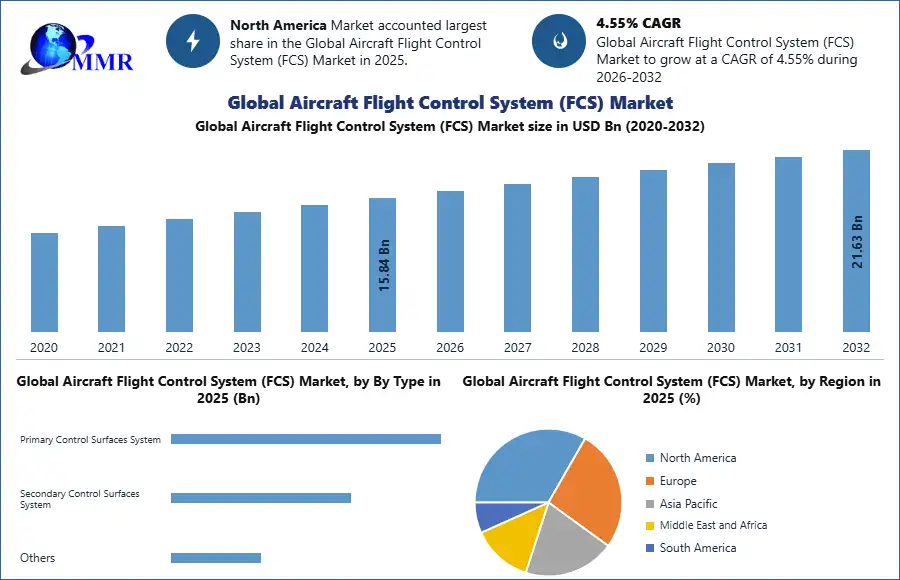

Aircraft Flight Control System Market size was valued at USD 15.84 Bn. in 2025 and the total revenue is expected to grow at a CAGR of 4.55% through 2026 to 2032, reaching nearly USD 21.64 Bn.

Aircraft Flight Control System Market Overview:

The Aircraft Flight Control System Market is expected to reach US$ 18.93 billion by 2029, thanks to growth in the component segment. The report analyzes Aircraft Flight Control system market dynamics by region, component, type, technology, and end-user.

Flight control surfaces, respective cockpit controls, connecting linkages, and the essential operational mechanisms for controlling an aircraft's direction in flight make up a traditional fixed-wing aircraft flight control system. Because they modify speed, aircraft engine controls are also considered flying controls.

In-flight dynamics, the principles of aircraft controls are explained. The basic technique used on airplanes initially debuted in a recognizable form on Louis Bleriot’s pioneer-era monoplane design, the Bleriot VIII, in April 1908.

To know about the Research Methodology:- Request Free Sample Report

Aircraft Flight Control System Market Dynamics:

Orders and delivery of aircraft are increasing:

Air travel has become more inexpensive as per capita income has increased across countries. This has led to the global surge in aviation passenger travel. According to a study conducted by the International Air Transport Association (IATA) in May 2021, the number of passengers is expected to exceed 8 billion by 2035, with an annual growth rate of 5.21%. Over the next 20 to 30 years, demand for commercial aviation is expected to quadruple. Also, the profitability of airlines has improved as a result of better fuel economy in aircraft operations. Factors such as aircraft design, navigation and flight patterns, and weather conditions all influence aircraft operational efficiency.

The efficiency of aircraft operations has been improved thanks to advancements in navigational technologies and efficient aircraft operations such as flight operations, technical operations, and ground operations. These factors have resulted in an increase in aircraft orders around the world, which may drive the global market over the forecast period.

The Asia Pacific has a slew of new aircraft producers:

One of the biggest opportunities for the global market to expand during the forecast period is for an emerging aircraft manufacturer in the Asia Pacific and Latin America. Commercial Aircraft Corporation of China, Ltd. (COMAC), Embraer SA (Brazil), and Mitsubishi Aircraft Corporation (Japan) are just a few of the new aircraft manufacturers on the stage. COMAC makes commercial, business, and regional aircraft, while Mitsubishi Aircraft Corporation manufactures regional aircraft.

Increased air passenger traffic is expected to increase demand for commercial aircraft, business jets, and regional transport aircraft, which may provide these manufacturers with growth opportunities for new aircraft production and, as a result, growth in the aircraft flight control system market during the forecast period.

Stringent rules and regulations:

Because of the inherent danger connected with flying operations, the aviation business is one of the most heavily regulated industries. Aircraft and aircraft component manufacturers, particularly aircraft flight control system makers, are bound by a slew of bilateral, national, and international regulations and standards. Different regulatory agencies oversee the standards of safety connected with aircraft operating in different countries across the world.

Aircraft Flight Control System Segment Analysis:

In 2025, the Primary Flight Control System (Surfaces System) segment dominates the market due to its critical role in controlling aircraft stability and maneuverability during all phases of flight. These systems, including ailerons, elevators, and rudders, are essential for safe operation, making them indispensable across all aircraft categories.

The Secondary Control Surfaces System segment also shows strong demand, particularly in enhancing aerodynamic efficiency and passenger comfort through components such as flaps, slats, and spoilers. The Others segment, including trim and auxiliary systems, maintains steady demand, primarily supporting performance optimization and redundancy functions.

Based on Component, Flight Control Computers (FCC) hold the largest market share in 2025 due to their central role in processing pilot inputs and managing automated flight operations. Increasing adoption of digital and autonomous systems further strengthens this segment.

Actuators and Control Surfaces also represent significant demand, as they directly execute flight commands and influence aircraft movement. Meanwhile, Sensors & Feedback Devices are the fastest-growing segment, driven by rising demand for real-time data monitoring and enhanced system accuracy. Cockpit Controls maintain stable demand, while the Others segment supports auxiliary and integration functions.

| Global Aircraft Flight Control System (FCS) Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 15.84 USD Bn |

| Forecast Period 2026-2032 CAGR: | 4.55% | Market Size in 2032: | 21.63 USD Bn |

| Segments Covered: | By Type | Primary Control Surfaces System Secondary Control Surfaces System Others |

|

| By Fit | Line Fit Retrofit |

||

| By Component | Flight Control Computers (FCC) Actuators Cockpit Controls Sensors & Feedback Devices Control Surfaces Others |

||

| By Technology | Hydromechanical Systems Fly-by-Wire (FBW) Systems Power-by-Wire (PBW) Systems Fly-by-Light (FBL) Systems Others |

||

| By Aircraft Platform | Commercial Aircraft Narrow Body Wide Body Regional Jet Military Aircraft Combat & Multirole Military Transport Aircraft Military Helicopter Others General Aviation Business Jets Light Aircraft Unmanned Aerial Systems Civil and Commercial Drones Defense and Government Drones Advanced Air Mobility (AAM) eVTOL Urban Air Mobility (UAM) |

||

| By Application | Commercial Aviation Military Aviation Business & General Aviation Others |

||

Aircraft Flight Control System Regional Insights:

Based on Region, North America leads the global Aircraft Flight Control System market in 2025, driven by the presence of major aircraft manufacturers, strong defense spending, and rapid adoption of advanced avionics technologies.

Europe follows closely, supported by established aerospace infrastructure and increasing investments in next-generation aircraft programs.

Asia Pacific is the fastest-growing region, fueled by expanding commercial aviation, rising air passenger traffic, and increasing defense budgets in countries such as China and India.

Other regions, including Latin America, Middle East & Africa, show moderate growth, supported by gradual fleet expansion and improving aviation infrastructure.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 23 March 2026 | Collins Aerospace | The company expanded its digital avionics portfolio by launching a next-generation flight management solution with integrated real-time data analysis capabilities. | Enhances the company's competitive positioning in the high-growth software-defined flight control segment. |

| 14 January 2026 | BAE Systems | Successfully completed the first flight test of its lightweight fly-by-wire system specifically designed for autonomous eVTOL platforms. | Positions the firm as a first-mover in the emerging Urban Air Mobility (UAM) flight control market. |

| 12 November 2025 | Airbus | Released a critical software firmware update for over 6,000 A320 aircraft to mitigate control system data corruption risks from solar radiation. | Directly addresses operational safety standards and reinforces the necessity of cybersecurity in flight control. |

| 15 July 2025 | Safran S.A. | Finalized the strategic acquisition of the flight control and actuation business unit from Collins Aerospace. | Significantly increases Safran's global market share and technical capacity in digital flight control architectures. |

| 18 May 2025 | Honeywell | Announced an expanded partnership with Vertical Aerospace to certify flight control systems for the VX4 electric air taxi. | Strengthens its supply chain presence within the sustainable aviation and electric propulsion sub-sectors. |

| 02 April 2025 | FAA | The Federal Aviation Administration committed to a September 2025 rollout for the modernized NOTAM database to improve pilot messaging reliability. | Drives demand for avionics hardware upgrades compatible with advanced digital messaging protocols. |

The objective of the report is to present a comprehensive analysis of the market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the global market dynamics, structure by analyzing the market segments and projecting the global market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the global market makes the report investor's guide.

Aircraft Flight Control Industry Ecosystem

Aircraft Flight Control System Market Scope: Inquire before buying

Aircraft Flight Control System Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Aircraft Flight Control System Market Report in Strategic Perspective:

- Honeywell International Inc.

- Moog Inc.

- Safran S.A.

- BAE Systems PLC

- Parker Hannifin Corporation

- Thales Group

- Collins Aerospace (Raytheon Technologies Corporation)

- Curtiss-Wright Corporation

- Liebherr Group

- Woodward, Inc.

- Nabtesco Corporation

- Leonardo S.p.A.

- Saab AB

- Northrop Grumman Corporation

- The Boeing Company

- Airbus S.A.S.

- Embraer S.A.

- Dassault Aviation

- Mitsubishi Heavy Industries Ltd.

- Triumph Group Inc.

- TE Connectivity Ltd.

- Sensata Technologies Holding PLC