Sugar Substitutes Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

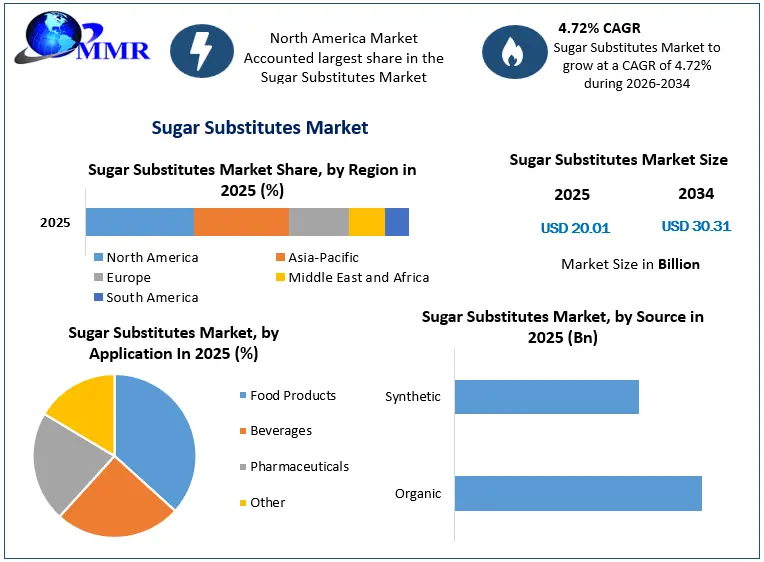

Global Sugar Substitutes Market size was valued at USD 20.01 Bn in 2025 and is expected to reach USD 30.31 Bn by 2034, at a CAGR of 4.72 %.

Sugar Substitutes Market

Sugar substitutes are chemical or plant-based substances used to sweeten or enhance the flavor of foods and drinks. It is also called “artificial sweeteners” or “non-caloric sweeteners” and used as a tabletop sweetener (for example, to sweeten a glass of iced tea) and/or as an ingredient in processed foods and drinks. Most of the sugar substitutes are many times sweeter than sugar, some have low calories and others have little to no calories They are regulated as food additives by the U.S. Food and Drug Administration (FDA). This means that the FDA reviews scientific evidence to be sure that a sugar substitute is safe before it is used in foods and drinks.

Sugar Substitutes Market Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

The increasing consumer awareness and concerns regarding health and wellness are expected to drive the sugar substitute market growth. With growing awareness about the adverse effects of excessive sugar consumption on health, including obesity, diabetes, and dental issues, consumers are seeking healthier alternatives. Sugar substitutes offer a way to enjoy sweetness without the negative health impacts associated with traditional sugar, making them increasingly popular among health-conscious consumers.

Sugar Substitutes Market Dynamics

Health-Conscious Consumer Trends to Drive the Market Growth

Sugar comes from a variety of sources, including sugarcane. It's a sweet carbohydrate that's utilized in a variety of cuisines. Sugars that are commonly used include monosaccharides (simple sugar), galactose, and fructose. Sucrose is the sugar eaten, and it hydrolyzes into glucose and fructose when consumed. Sugar is mostly used as a sweetener and in baked items. Sugar consumption causes weight gain, acne, diabetes, cancer, depression, rapid skin aging, and fatty liver, among other health problems. Consumer desire for sugar replacements has shifted as health consciousness has grown. For adults and children with overweight or obesity, sugar substitutes also might help manage weight in the short term. That's because sugar substitutes often are low in calories or have no calories. But it's not clear whether sugar substitutes help people manage their weight over the long term.

With growing awareness of health risks associated with excessive sugar consumption, there's a surge in demand for sugar substitutes. Consumers are actively seeking alternatives to reduce calorie intake, manage weight, and address health conditions such as diabetes and obesity. As a result, the sugar substitutes market is witnessing significant growth driven by the preference for healthier lifestyles. Sugar Substitutes Manufacturers are innovating to offer natural, low-calorie, and functional sweeteners to meet diverse consumer needs, tapping into this trend and driving Market growth.

The level of health consciousness among the population affects industry demand. Health-conscious consumers are more likely to purchase juices and smoothies given the perceived health benefits of a nutritious diet that contains fruit and vegetables. Health consciousness indicates consumer attitudes toward health issues and lifestyle choices. The health consciousness is expected to increase, providing the Sugar Substitutes industry with an opportunity for revenue growth.

Rising Diabetic Population to Boost the Sugar Substitutes Market Growth

Sugar substitutes are widely used in food products, beverages, dietary supplements, as well as pharmaceuticals. Artificial sweeteners are commonly used in processed foods, such as soft drinks, canned foods, baked pastries and sweets, as well as other types of desserts, jams jellies and dairy products, including sweet yogurts. The increasing prevalence of diabetes globally is a major driver for the sugar substitute market. Diabetics need to manage their blood sugar levels effectively, necessitating a shift towards low-glycemic index sweeteners. As awareness about diabetes and its management spreads, more individuals are opting for sugar substitutes to control their sugar intake without sacrificing taste. This demographic represents a substantial consumer base for the sugar substitutes market, propelling growth through the development of diabetic-friendly sweeteners and related products. According to the National Diabetes Statistics Report, 10.5% of the entire population of the US market had diabetes throughout the historic forecast period that ended in 2022. Furthermore, 2% of adults in the United States were unaware that they had diabetes, while 21.4 percent of all adults in the United States had diabetes. The increased obesity in the region is pressuring consumers to reduce their sugar intake, resulting in a strong growth driver for the Sugar Substitutes Market over the forecast period.

Table No 1: Diabetes Prevalence by Country in 2025

| Sr No | Country | Diabetes Rate | Prevalence of Obesity |

| 1 | Pakistan | 30.8% | 8.6% |

| 2 | Kuwait | 24.9% | 37.9% |

| 3 | Nauru | 23.4% | 61% |

| 4 | New Caledonia | 23.4% | - |

| 5 | Northern Mariana Islands | 23.4% | - |

| 6 | Marshall Islands | 23% | 52.9% |

| 7 | Mauritius | 22.6% | 10.8% |

| 8 | Egypt | 20.9% | 32% |

| 9 | Solomon Islands | 19.8% | 22.5% |

| 10 | Qatar | 19.5% | The Silence of Obesity |

Health Concerns and Regulation to Restrain the Market Growth:

The sugar substitutes market revolves around health concerns and regulatory challenges and is expected to restrain market growth. Despite their popularity as alternatives to sugar, some artificial sweeteners have faced scrutiny over potential health risks, such as metabolic disorders, weight gain, and even cancer. Heightened awareness of these risks has led to increased regulatory scrutiny, with authorities imposing stricter guidelines and limitations on the use of certain sugar substitutes. For instance, The World Health Organization (WHO) has released a new guideline on non-sugar sweeteners (NSS), which recommends against the use of NSS to control body weight or reduce the risk of noncommunicable diseases (NCDs). Low/no calorie sweeteners undergo thorough safety evaluations by authorities like EFSA and JECFA for approval in the EU. The 11 approved sweeteners include acesulfame-K, aspartame, and sucralose. Regulations, such as Directive 94/35/EC and Regulation 1333/2008, govern their use. Approval requires extensive safety testing, with an Acceptable Daily Intake (ADI) set for each sweetener. EFSA is re-evaluating sweeteners' safety, with aspartame already confirmed as safe. Comprehensive information on regulation and safety is available through resources like the ISA booklet and infographic. Consequently, manufacturers face hurdles in developing and marketing these products, as they must navigate complex regulatory landscapes and address consumer skepticism regarding their safety and long-term health implications.

Taste and Texture Limitations: Another key growth restraint stems from taste and texture limitations associated with sugar substitutes. While advancements have been made in developing alternatives that mimic the sweetness of sugar, many still fall short in replicating its taste and texture accurately. Consumers often perceive a noticeable difference in flavor or mouthfeel when substituting sugar with artificial sweeteners, which deters widespread adoption. Additionally, some sugar substitutes may exhibit undesirable aftertastes or inconsistencies in performance when used in various applications, posing challenges for food and beverage manufacturers striving to maintain product quality and consumer satisfaction. Overcoming these taste and texture limitations remains a significant obstacle for the sugar substitute market to achieve broader acceptance and Sugar Substitutes Market penetration.

Expanding Applications in the Food and Beverage Industry to Create Lucrative Opportunity for Market Growth

The food industry is constantly changing and adapting to new trends and preferences. Although sugar is one of the most commonly used sweeteners in the food industry and is found in a wide variety of products, from candy and baked goods to beverages and condiments, there has been a recent increase in demand for alternative sweetening options. The food and beverage industry represents a vast landscape of opportunities for Sugar Substitutes Market. With advancements in food technology and formulation, sugar substitutes now mimic the taste and texture of sugar more effectively, expanding their applications across various product categories such as beverages, confectionery, bakery, dairy, and more. Additionally, as manufacturers innovate to meet consumer demand for healthier options without compromising taste, the use of sugar substitutes in product formulations is becoming more prevalent. This expansion into diverse food and beverage segments is driving growth in the sugar substitute market as manufacturers seek to cater to evolving consumer preferences and dietary needs.

The food industry utilizes both simple and complex carbohydrates for various functional purposes such as sweetness, viscosity, and texture. Starches, gums, and pectins serve as thickening agents, while simple sugars add sweetness and texture. To combat health concerns associated with added sugars, food manufacturers use sugar substitutes, including artificial sweeteners like saccharin, aspartame, and sucralose, as well as natural options like stevia. Sugar alcohols like xylitol and sorbitol are also used. While sugar substitutes reduce calorie intake and tooth decay risk, concerns exist regarding their effects on weight gain and blood glucose levels. Gastrointestinal upset is a common side effect of sugar alcohol. As a result, limiting consumption of both added sugars and artificial sweeteners is advised for optimal health and is expected to drive the sugar substitutes market growth.

Table No 2: Sweeteners and Sugar Alternatives in the Food Industry

| Category | Examples | Uses |

| Natural Sweeteners | Sorbitol | Used as a sugar substitute in products for diabetics |

| Found in low-calorie products like protein bars and sugar-free beverages | ||

| Added to confectionery to prevent moisture loss and maintain product freshness | ||

| Xylitol | Used in candies, chocolates, chewing gum, and low-sugar desserts | |

| Popular in low-calorie diet products such as dairy, jams, jellies, and ice cream | ||

| Erythritol | Commonly added to low-calorie and sugar-free foods such as chocolate and candy | |

| Improves texture and moisture absorption in baked goods and candies | ||

| Glucose | Used in various sweet treats like candies, ice cream, desserts, and beverages | |

| Fructose | Used in prolonging the shelf life of baked goods and maintaining the texture of confectionery | |

| Artificial Sweeteners | Sucralose | Found in low-calorie products for diabetics like diet foods, frozen foods, and desserts |

| Suitable for sweetening beverages and baked goods due to its solubility and stability | ||

| Aspartame | Commonly used in flavored mineral waters, yogurts, isotonic drinks, and sweetened sodas | |

| Glucose-Fructose Syrup | Glucose-Fructose Syrup | Enhances flavor and color of products |

| Prevents crystallization in jams, candies, and ice cream | ||

| Provides moisture and softness in baked goods like cookies and cakes |

Sugar Substitutes Market Segment Analysis

Based on Product Type, the high-intensity sweeteners segment held the largest Sugar Substitutes Market share in 2025. High-intensity sweeteners are ingredients used to sweeten and enhance the flavor of foods. Because high-intensity sweeteners are many times sweeter than table sugar (sucrose), smaller amounts of high-intensity sweeteners are needed to achieve the same level of sweetness as sugar in food. People choose to use high-intensity sweeteners in place of sugar for several reasons, including that they do not contribute calories or only contribute a few calories to the diet. Also, the High-intensity sweeteners generally will not raise blood sugar levels. As a result, the growing health and wellness trend globally is expected to boost the application scope of high-intensity sweetness. The low-intensity sweeteners segment is expected to witness substantial growth during the forecast period due to the increasing consciousness about oral health. Several low-intensity sweeteners, including xylitol, erythritol, mannitol, and sorbitol, have desirable characteristics and are used in a wide range of foods to decrease glycemic levels, which is anticipated to drive segment growth. High-fructose syrups are widely used in the food and beverage industry as they are easy to handle and do not crystallize in solution.

Based on Application, the beverages segment accounted for the largest Sugar Substitutes Market share in 2025. This growth is driven by the growing demand for low as well as no-calorie formulations among consumers. High-intensity sweeteners are widely used in foods and beverages marketed as "sugar-free" or "diet," including baked goods, soft drinks, powdered drink mixes, candy, puddings, canned foods, jams and jellies, dairy products, and scores of other foods and beverages. Furthermore, the market for sugar substitutes, particularly natural sweeteners derived from monk fruit, agave, and stevia, is anticipated to grow as consumers are more inclined toward organic, natural, convenient, and functional beverages. The increasing demand for sports and health nutrition drinks with enhanced nutritional value and is expected to boost segment growth in the global market. However, the food segment is expected to grow at a CAGR of 5.8% from 2026 to 2034 due to changing consumer habits and increased awareness about low-calorie food and dairy products

Sugar Substitutes Market Regional Insight

North America dominated the largest Sugar Substitutes Market share in 2025. A key driving factor behind this growth is the region's increasing emphasis on promoting low-calorie food consumption. Additionally, the rising popularity of healthy food and beverage choices among North American consumers is expected to fuel market expansion. In the United States, shifting food trends influenced by socioeconomic and demographic changes have played a significant role. The younger demographic, in particular, demonstrates a preference for exploring new and innovative products, driven by heightened awareness of diet-related health issues. Regulatory changes in the US, advocating for limited sugar intake, further contribute to this trend. For instance, The FDA prohibits the use of cyclamates and their salts (such as calcium cyclamate, sodium cyclamate, magnesium cyclamate, and potassium cyclamate) in the U.S. Whole-leaf and crude stevia extracts are subject to an Import Alert. They are also not permitted for use as sweeteners. These forms of stevia differ from certain highly purified steviol glycosides obtained from stevia leaves, which have been the subjects of GRAS notices; the FDA has not objected to the use of sweeteners of these highly refined substances. Furthermore, there is a noticeable trend within the food and beverage industries towards substituting artificial sweeteners for sugar across various products, reflecting a broader shift towards healthier alternatives.

Asia Pacific region is expected to grow at the fastest rate and hold the largest proportion of the sugar substitutes market. Customers' lives in this region are rapidly changing, and they are becoming more health-conscious, strengthening the regional demand for natural sweeteners. In terms of diet diversity and growing urbanization, this region is likewise witnessing considerable changes. Furthermore, a movement in consumer preference towards low-sugar, high-energy meals has resulted from increased consumer understanding of health issues, as well as improved disposable expenditures. Sugar substitutes are expected to grow in popularity in North America. The engagement of major enterprises in the region is favorably influencing the regional market, as is a growth in the consumption of refined sugar substitutes as a result of growing awareness of sugar's detrimental implications.

Sugar Substitutes Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2026 | Cargill, Incorporated | Cargill expanded its advanced next-generation sweetener portfolio to meet rising global demand for clean-label formulations. | Enhances operational efficiency and broadens commercial scale for low-calorie food producers. |

| 10 February 2026 | Ingredion Incorporated | Ingredion launched upgraded plant-derived sugar reduction solutions featuring enhanced stevia-based ingredients. | Accelerates market penetration in health-focused beverage and bakery sectors. |

| 04 March 2026 | Roquette Frères | Roquette increased strategic investments in high-purity stevia ingredients to optimize taste profiles. | Improves sustainability metrics and reduces sugar content without compromising product quality. |

| 20 April 2026 | Ajinomoto Co., Inc. | Ajinomoto scaled up production lines for advanced high-intensity sweeteners targeted at functional foods. | Strengthens supply chain efficiency to fulfill surging dietary product requirements. |

Sugar Substitutes Market Scope: Inquire before buying

| Sugar Substitutes Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 20.01 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.72% | Market Size in 2034: | US $ 30.31 Bn. |

| Segments Covered: | by Product Type | High Fructose Syrup Low Intensity Sweeteners High Intensity Sweeteners |

|

| by Source | Organic Synthetic |

||

| by Application | Food Products Beverages Pharmaceuticals Other |

||

Sugar Substitutes Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Sugar Substitutes Key players

1. Tate & Lyle PLC

2. Roquette Frères

3. Archer Daniels Midland Company

4. DuPont de Nemours, Inc.

5. Cargill, Incorporated

6. Ingredion Incorporated

7. JK Sucralose Inc.

8. Ajinomoto Co., Inc.

9. The NutraSweet Co.

10. Sandsucker AG

11. Guilin Lain Natural Ingredients Corp.

12. Hucheng Haitian Pharm Co., Ltd.

13. HSWT France SAS

14. International Flavors & Fragrances Inc.

15. GLG Life Tech Corp.

16. Celanese Corporation

17. PCIPL

18. Mane SA

19. Döhler GmbH

20. Morita Kagaku Kogyo Co., Ltd.

21. zuChem

22. Van Wankum Ingredients

23. Tag Ingredients India Pvt. Ltd.

24. Sweetly SteviaUSA

25. Foodchem International Corporation

26. The Real Stevia Company AB

27. Stevia Hub India

28. Pyure Brands

29. XiliNat

30. Savanna Ingredients

Frequently Asked Questions:

1] What is the growth rate of the Global Sugar Substitutes Market?

Ans. The Global Sugar Substitutes Market is growing at a significant rate of 4.72 % during the forecast period.

2] Which region is expected to dominate the Global Sugar Substitutes Market?

Ans. North America is expected to dominate the Sugar Substitutes Market during the forecast period.

3] What is the expected Global Sugar Substitutes Market size by 2034?

Ans. The Sugar Substitutes Market size is expected to reach USD 30.31 Bn by 2034.

4] Which are the top players in the Global Sugar Substitutes Market?

Ans. The major top players in the Global Sugar Substitutes Market are Cargill, Inc. (USA), Ingredion Inc. (USA) and others.

5] What are the factors driving the Global Sugar Substitutes Market growth?

Ans. The growth of health-conscious consumers and an explanation of the food and beverages industry are expected to drive the Sugar Substitutes Market growth.

6] Which country held the largest Global Sugar Substitutes Market share in 2025?

Ans. The United States held the largest Sugar substitute market share in 2025.