Steam Boiler Systems Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

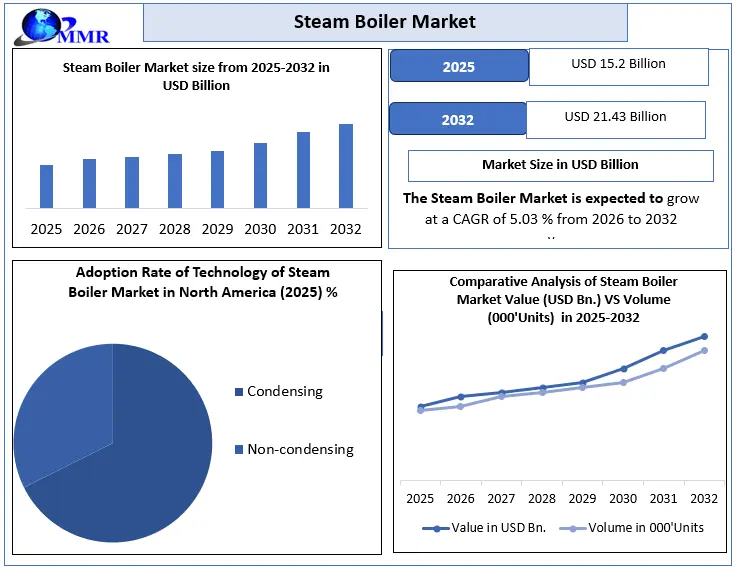

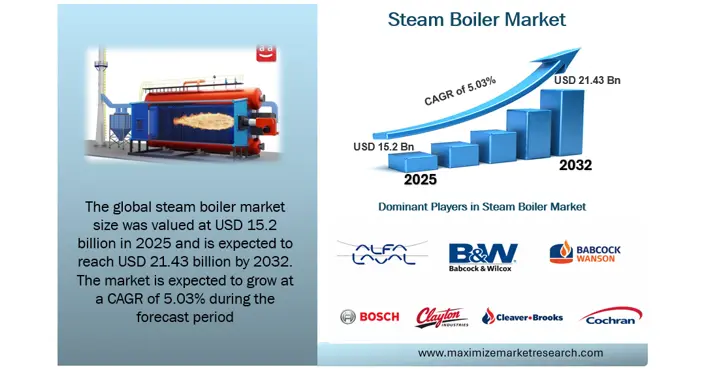

The Global Steam Boiler Market size was valued at USD 15.2 Billion in 2025 and is expected to reach USD 21.43 Billion by 2032. The market is expected to grow at a CAGR of 5.03% during the forecast period.

Steam Boiler Market Size and Growth Potential

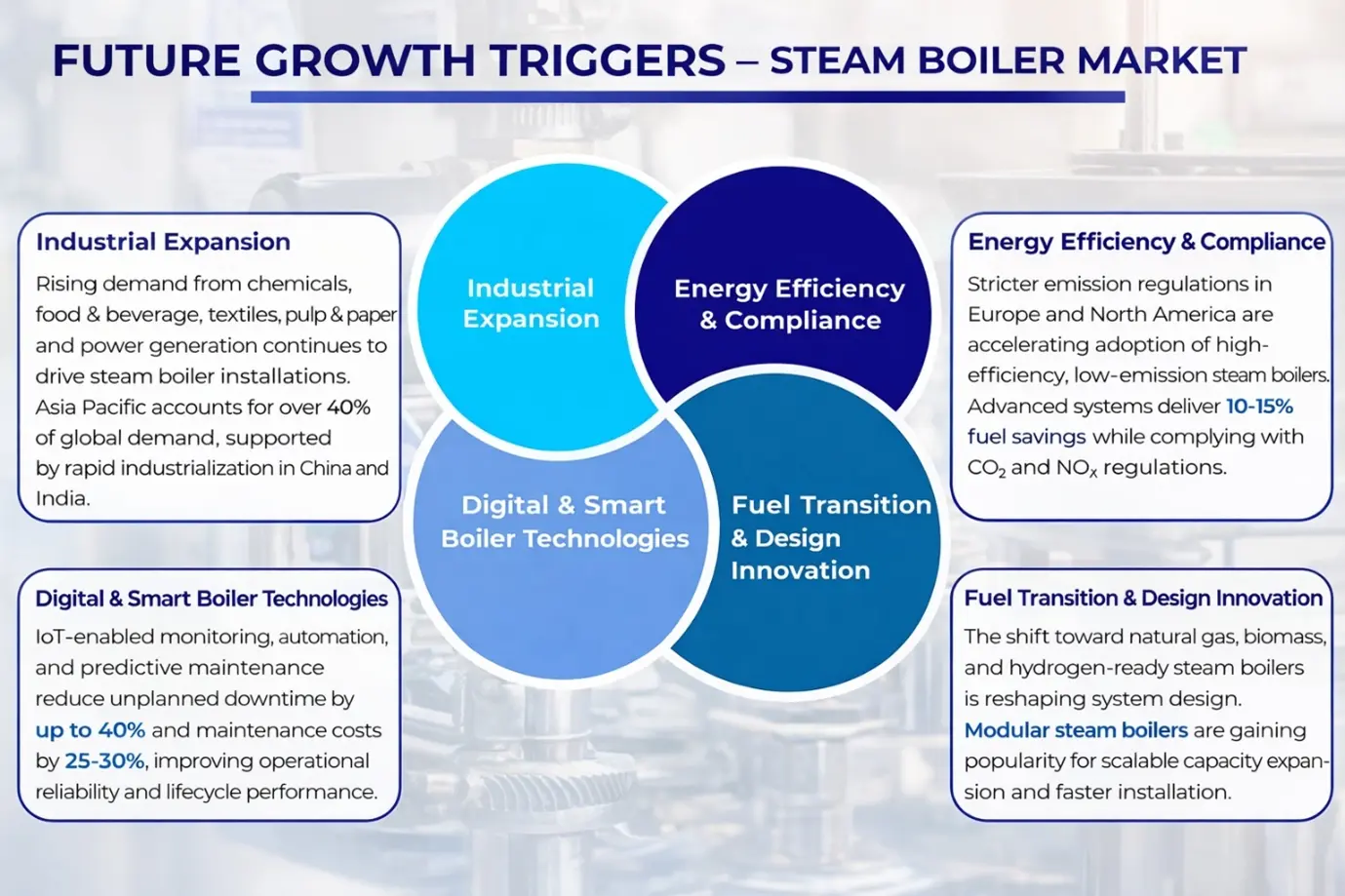

The steam boiler market is experiencing steady and structurally resilient growth, underpinned by long-term demand from industrial manufacturing, power generation, refining, and large commercial infrastructure. Market expansion is supported by a well-defined value chain encompassing raw material sourcing, fabrication, engineering, and quality assurance, which collectively shape production economics and capital intensity. Technological advancements—particularly energy-efficient designs, automated control systems, and digital monitoring—are improving operational reliability, lowering lifecycle costs, and enabling predictive maintenance.

To know about the Research Methodology :- Request Free Sample Report

The market ecosystem comprises global OEMs, component suppliers, EPC partners, and service providers, with aftermarket services and long-term service agreements emerging as key sources of recurring, high-margin revenue. Growth momentum is increasingly driven by high-capacity boilers exceeding 250 MMBTU/hr, natural gas-fired systems, and condensing technologies that align with tightening environmental regulations and emissions standards. Competitive intensity remains moderate, as established multinational players such as GE Vernova, Bosch, Babcock & Wilcox, and Thermax dominate large, capital-intensive and high-risk installations, while regional manufacturers compete effectively in price-sensitive, mid-scale segments. From a regional perspective, Asia Pacific delivered volume-led growth driven by industrialization and power capacity additions, Europe generated attractive retrofit and compliance-driven service revenues, and North America provided stable, service-led cash flows, positioning the steam boiler market as a low-volatility, long-term industrial investment opportunity.

Key Growth Drivers Shaping the Global Steam Boiler Market:

Integration of Digital Monitoring & Smart Boiler Systems

Digital monitoring and smart boiler systems are a key growth driver for the global steam boiler market, specifically for power plant and major industry applications of steam boilers. The U.S. Department of Energy benchmarks have shown that fuel efficiency can be improved by 5-15% and unplanned downtime can be reduced by up to 40% with the use of IoT-enabled sensors, AI-based analytics, and automated controls. Power utilities using smart boilers such as those supplied by Cleaver-Brooks and Mitsubishi Heavy Industries report a decrease in maintenance costs of almost 30%. Safety, emission compliance, and predictive maintenance capabilities provide long-term operational reliability and sustainability through enhanced predictive capabilities offered by these technologies.

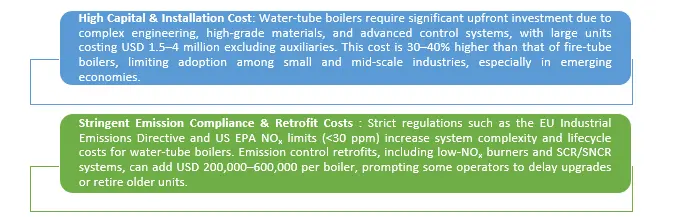

Key Restraining Factors Impacting the Steam Boiler Market

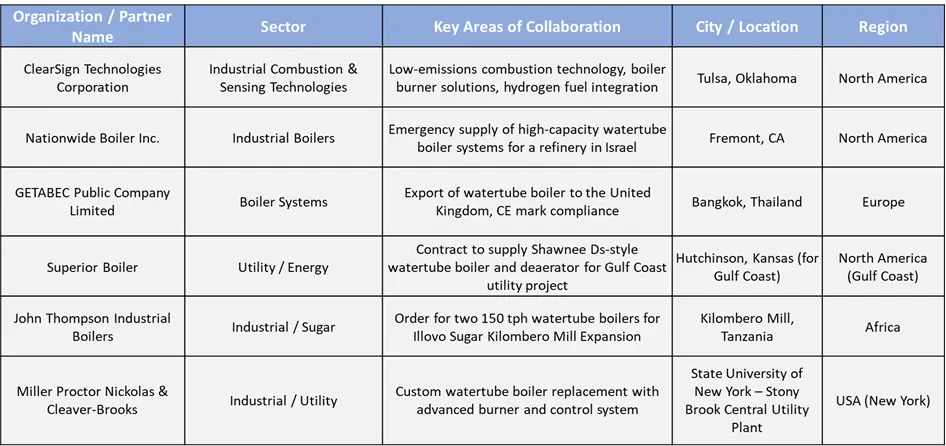

Strong Project Pipeline Signals Long-Term Investment Stability:

The global pipeline of awarded and under-construction boiler projects highlights sustained capital investment across utilities, refining, and heavy industry. Rising adoption of high-capacity, low-emission, and hydrogen-ready systems indicates strong long-term demand visibility, supporting stable returns for manufacturers, EPC partners, and technology providers across developed and emerging markets.

Major Projects (Pipeline) Globally — Planned, Awarded, Under Construction

The Steam Boiler Market is characterized by long project cycles and infrastructure-oriented investments, with high entry barriers due to capital-intensive requirements and stringent performance guarantees. Financing in this market often favors established OEMs with proven execution records and reference projects, as lenders prioritize bankable, low-risk suppliers. With the growth of EPC-led, ECA-backed, and service-based financing models, manufacturers that offer technical reliability, emissions compliance, and comprehensive lifecycle services are best positioned to capture stable, long-term value from the expanding global steam boiler project pipeline.

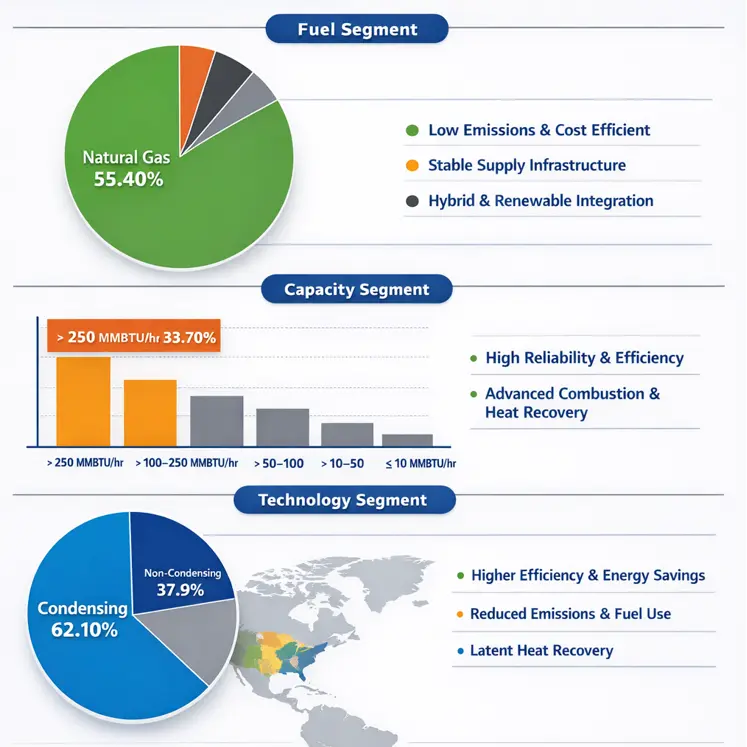

Global Steam Boiler Market Analysis: Segmentation by Fuel, Capacity, Technology & Applications

• Natural gas leads with 55.4% share in 2025 due to cost-efficiency and lower emissions. Hybrid and renewable integration are boosting sustainability.

• 250 MMBTU/hr boilers dominated at 33.7% in 2025, serving high-demand industrial and utility applications. They offer reliability and energy-efficient heat recovery.

• Condensing boilers held 62.1% share in 2025 with high efficiency and lower fuel use. They are favored for industrial and commercial emissions reduction.

The steam boiler market is driven by efficiency, sustainability, and high-capacity industrial needs. Natural gas and condensing technologies will continue to lead global adoption trends.

Steam Boiler Market by Key Countries Analysis (2025)

| Country | CAGR |

| China | 7.20% |

| India | XX% |

| Germany | 6.10% |

| France | 5.60% |

| UK | XX% |

| USA | 4.50% |

| Brazil | XX% |

China led the global steam boiler market at a CAGR of 7.20% in 2025, supported by large-scale power capacity additions, industrial expansion, and accelerated replacement of legacy coal-fired systems with high-efficiency, low-emission boilers supplied by players such as Harbin Electric, Dongfang Boiler, and Mitsubishi Heavy Industries.

Germany followed at 6.10% in 2025, driven by strict emissions norms and retrofit demand, with Bosch Industriekessel, Viessmann, and Babcock Wanson actively supplying condensing and hydrogen-ready systems. France, growing at 5.60% in 2025, benefits from district heating upgrades led by ALFA LAVAL and Cochran. The U.S. market, at 4.50% CAGR, remains mature but stable, dominated by Cleaver-Brooks, GE Vernova, and Babcock & Wilcox through retrofit and service-led revenue models. India, the UK, and Brazil offer emerging growth anchored in industrialization, refinery projects, and gradual regulatory tightening.

Regional policies and infrastructure investments create momentum

Regional policy frameworks and infrastructure investments are increasingly leading to shaping the steam boiler market. Rapid growth in industrialization and expansion in the power sector pose a higher demand for steam boilers in the Asia Pacific, with an increased demand projection from countries such as China and India. Europe has been advancing at a pace with tight regulatory frameworks toward a low-emission technology shape. North America also forms a critical market, with both the upgrading of industries and the integration of technology. It continues to invest in energy and industrial infrastructures from which steam boilers will be increasingly adopted by Middle Eastern and African nations. In summary, these regional developments have underscored how local policies can influence global demand trends.

Investing in Steam Boilers: Retrofit and Predictive Maintenance Lead Service Revenue Growth Globally.

The steam boiler market is increasingly shifting from equipment-led expansion to a service-driven growth model, with retrofit, upgrade, and preventive maintenance services forming the core long-term value pool. Europe remains the global leader in watertube boiler aftermarket services, driven by stringent emissions regulations and high replacement intensity, while North America benefits from monetizable long-term service agreements (LTSAs).

Asia Pacific offers scale-driven opportunities as older installations enter replacement cycles, and MEA and South America present selective, project-based growth in energy-intensive sectors. Structured preventive and predictive maintenance programs not only reduce unplanned outages by up to 60% but also improve fuel efficiency and extend asset life, converting watertube boilers from high-risk liabilities into optimized, regulation-compliant assets. For investors, this underscores a high-margin, resilient service market with predictable revenue streams, making retrofit, upgrade, and digital service solutions the strategic focus for capturing long-term returns in the global steam boiler market.

Steam Boiler Systems Market Scope: Inquire before buying

| Steam Boiler Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 15.2 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 5.03% | Market Size in 2032: | USD 21.43 Bn. |

| Segments Covered: | by Fuel Type | Coal Natural Gas Oil Others |

|

| by Capacity | > 250 MMBTU/hr ≤ 10 MMBTU/hr > 10 - 50 MMBTU/hr > 50 - 100 MMBTU/hr > 100 - 250 MMBTU/hr |

||

| by Technology | Condensing Non-condensing |

||

| by Application | Power Generation Oil & Gas / Refinery Boilers Chemical & Petrochemical Industrial Manufacturing Marine & Offshore Others |

||

The steam boiler market offers a resilient, long-term growth opportunity anchored in industrial infrastructure, regulatory compliance, and efficiency-driven modernization. Value creation is increasingly shifting toward high-capacity, low-emission systems and service-led business models that emphasize digitalization, predictive maintenance, and lifecycle optimization. Market leadership will favour manufacturers with strong engineering depth, EPC integration, and global service capabilities, while investors benefit from stable cash flows and high entry barriers. For end users, strategic procurement focused on lifecycle performance, reliability, and compliance will be critical to mitigating operational risk and maximizing returns, reinforcing the steam boiler market’s position as a low-volatility, mission-critical industrial segment.

Major Steam Boiler Companies

1. GE Vernova

2. Aggreko

3. ALFA LAVAL

4. Babcock & Wilcox

5. Babcock Wanson

6. Bosch Industriekessel

7. Clayton Industries

8. Cleaver-Brooks

9. Cochran

10. FERROLI

11. Forbes Marshall

12. Fulton

13. Hoval

14. Hurst Boiler & Welding

15. John Cockerill

16. Miura America

17. P.M. Lattner Manufacturing

18. PARKER BOILER

19. Precision Boilers

20. Thermax

21. VIESSMANN

22. Weil-McLain

23. Others

Large multinational players dominate high-risk installations due to their global service footprint, certification depth, and brand trust, while regional manufacturers compete in price-sensitive segments.

1. What segments are covered in the Steam Boiler Market report?

The Steam Boiler Market is segmented based on Product Type, Connectivity, End-User Industry, and Region, providing a comprehensive view of demand trends and growth opportunities.

2. Which region is expected to hold the highest share of the Steam Boiler Market?

North America is projected to hold the largest market share due to high industrialization, stringent fire and safety regulations, and widespread adoption in high-risk industrial sectors.

3. What is the market size of the Steam Boiler Market by 2032?

The global Steam Boiler Market is expected to reach USD 21.439 billion by 2032, reflecting robust demand across industrial and commercial applications.

4. What is the growth rate of the Steam Boiler Market?

The market is forecasted to grow at a CAGR of 5.03% during 2025–2032, driven by service-led retrofits, upgrades, and increasing regulatory compliance requirements.

5. Who are the major players in the Steam Boiler Market?

Key manufacturers include Honeywell, Siemens, Johnson Controls, MSA Safety, Emerson, Draeger, Minimax Viking, Spectrex, Det-Tronics, Rezontech, Halma, and Tyco International, leading in both equipment supply and aftermarket services.