Social Gaming Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

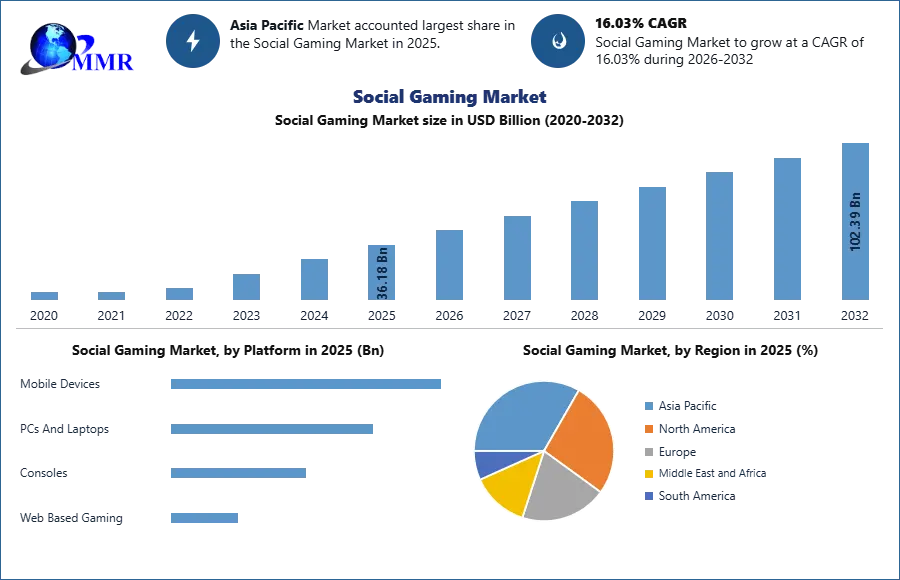

The Global Social Gaming Market was valued at USD 36.18 Billion in 2025 and is estimated to grow at a CAGR of 16.03% over the forecast period, reaching USD 102.39 Billion by 2032.

Social Gaming Market Overview:

Social gaming refers to digitally connected games designed around player interaction, community participation, competition, collaboration, and content sharing across mobile devices, PCs, consoles, and web platforms. The category includes casual, strategy, simulation, role-playing, and other multiplayer-led experiences where social connection is central to retention and monetization. Market growth has been driven by the expansion of smartphone gaming, broader access to digital payments, stronger live-service content strategies, and the rising use of chat, guild, leaderboard, and creator-led engagement mechanics. Technology development has increasingly focused on cross-platform continuity, cloud-enabled access, AI-assisted content workflows, real-time communication features, and social discovery tools that make gameplay more visible and shareable. Demand outlook remained positive as publishers continued prioritizing community-centric game design, continuous content updates, and monetization models built around player progression, customization, and repeat engagement across globally connected gaming ecosystems.

To know about the Research Methodology :- Request Free Sample Report

Social Gaming Market Dynamics:

During the forecast period, rising smartphone demand is expected to boost the social gaming market growth.

The demand for mobile phones has risen dramatically in recent years. Growing smartphone applications are leading to increased market support for social gaming. Smartphones run on a variety of operating systems, including iOS, Android, BlackBerry OS, and Windows, which allow users to perform multiple tasks at once. With the help of operating systems, different social games may be downloaded on mobile devices. The phone's huge memory capacity, which ranges from 16 to 64 GB, enables for the storage of many games. As a result, these factors are expected to boost the social gaming market growth over the forecast period.

During the forecast period, restrictions on social networking sites are expected to hamper the social gaming market growth.

Texas Hold'em poker, Farmville, Candy Crush, and Criminal Case are among the most popular online games on social networking sites like MySpace, Facebook, and Google+. The restriction on social networking sites like Facebook, MySpace, and Twitter has resulted in significant market losses. Many Islamic countries, including Iran, Pakistan, and Indonesia, have made social networking sites illegal. This is also considered forbidden in Middle Eastern cultures. Such sites have been restricted primarily for security concerns. As a result, these factors are expected to hinder the social gaming market growth over the forecast period.

In the global social gaming market, improvements in browser experience is expected to create significant growth opportunities.

High-quality browser-based games are being developed by the social gaming market. Richer and more complicated 3D social games are being developed by companies. Adobe released a beta of Flash Player, which is intended to support accelerated 3D, while Unity released a Flash export feature. Social games are simple to install on smartphones and tablet computers. The majority of games are available for free. As a result, consumers are more inclined to play browser-based games that provide a similar thrill and experience to those provided by an Xbox or PlayStation.

Smartphone and tablet sales are on the rise. The personal computer is a popular choice.

Globally, the need for smartphones and tablet computers is driving the growth of social games. Mobile devices make games available 24 hours a day, seven days a week. This is largely driving its growth in the segment. PCs and smartphones are commonly utilised for social gaming because they provide users with convenient access and convenience.

The largest gaming platform is available on social networking sites.

Social networking sites like Facebook, Twitter, MySpace, and Friendster are currently the most popular places to play games, contributing significantly to the growth of social gaming. In comparison to other platforms, social networking platforms are significantly more convenient.

Mobile-First Social Engagement Ecosystem

The market was primarily supported by the continued expansion of smartphone-led gaming behavior and the integration of real-time interaction features such as multiplayer rooms, guilds, chat, gifting, co-op progression, and friend-based competition. Mobile devices commanded 71.55% of social gaming revenue in 2025 in one competitive benchmark, reflecting how accessibility, always-on connectivity, and app-centric discovery continued to widen the active player base. The commercial advantage of mobile also came from short-session gameplay design, lower user onboarding friction, and stronger compatibility with notifications, referral loops, and social retention mechanics.

Monetization Maturity And Live-Ops Depth

A major growth driver was the increasing sophistication of monetization architecture across social games. In-app purchases accounted for 47.95% of 2025 revenue in one market view, while another benchmark placed in-app purchases at 40% of category revenue, showing a clear leadership position for this model. This reflected the industry’s dependence on digital items, progression boosts, event passes, collectible systems, personalization assets, and time-limited offers. Social gaming increasingly operated through live-service models where publishers used analytics, community events, and content refresh cycles to improve payer conversion, retention, and long-term engagement.

Platform Convergence And Social Discovery Innovation

The market also benefited from the convergence of gaming, creator ecosystems, and social-media-style discovery. Roblox introduced Moments, a short-form gameplay sharing feature, while Samsung expanded mobile cloud gaming into the U.K. and Germany, reducing download friction for mobile users. These developments showed that social gaming was evolving beyond conventional app sessions into a broader engagement layer built around shareable content, cross-device continuity, instant access, and community-led discovery. This strengthened the category’s appeal among younger players, streamers, and socially connected user cohorts.

Social Gaming Market Segment Analysis:

Social Gaming Market Segmentation, By Platform

Based on platform, the market has been divided into Mobile Devices, PCs And Laptops, Consoles, and Web Based Gaming. Among these, the Mobile Devices sub-segment was projected to generate the maximum revenue. The Mobile Devices sub-segment witnessed the highest market share in the global social gaming market in 2025. This segment dominated because smartphones had become the most scalable delivery channel for socially connected gameplay, supported by app-store accessibility, integrated payments, push notifications, friend invites, chat-based interactions, and continuous user engagement throughout the day. In 2025, mobile devices accounted for 71.55% of market revenue in one competitive benchmark. Mobile-led formats also aligned better with casual and hybrid-casual mechanics, short session loops, and viral referral behavior, making them commercially stronger than PC, console, or browser-centered alternatives for social interaction–driven game ecosystems.

Social Gaming Market Segmentation, By Game Type

Based on game type, the market has been divided into Casual Games, Strategy Games, Simulation Games, Role Playing Games, Multiplayer Online Battle Arena Games, Sports Games, and other game types. Among these, the Casual Games sub-segment generated the maximum revenue in 2025. This segment dominated because casual games offered the lowest barrier to entry, easy social sharing, quick session design, broad demographic appeal, and strong compatibility with gifting, leaderboard, challenge, and event-based engagement models. In 2025, casual titles held 37.55% share in one market benchmark, while another competitive reference placed casual games at 38%. Their dominance was reinforced by the ability to attract large non-core audiences and convert them into repeat users through simple mechanics, frequent updates, and socially visible progression systems that encouraged multiplayer interaction without demanding steep learning curves.

Regional Insights:

Asia Pacific dominated the market in the year 2025, and is expected to continue its dominance during the forecast period. The region led the market because it combined a very large mobile-first player base with strong smartphone penetration, fast digital payment adoption, culturally embedded gaming behavior, and a high concentration of major publishers and live-ops expertise. In 2025, Asia-Pacific retained 46.40% revenue share in one competitive benchmark, while another market view showed the region holding over 40% share in 2024. China remained a central revenue contributor, with one source indicating a market value of USD 4.2 Billion within the region. The region’s strength was further supported by creator ecosystems, esports spillover, and strong monetization performance in casual and socially networked mobile titles, which kept Asia Pacific ahead of North America and Europe in 2025.

Recent Developments

December 2024: Playtika entered a content partnership with IGT to bring established slot titles into its social casino portfolio, including Slotomania, Caesars Slots, and House of Fun. The move strengthened branded content depth in free-to-play social gaming and improved player engagement through recognizable land-based gaming IP adapted for digital social gameplay.

March 2025: Scopely announced an agreement to acquire Niantic’s games business, including Pokémon GO, Pikmin Bloom, Monster Hunter Now, Campfire, and Wayfarer. The transaction expanded Scopely’s scale in community-led and location-based gaming, reinforcing the strategic importance of social interaction, live events, and persistent player ecosystems in connected mobile gaming.

April 2025: Tencent Games presented updates on 46 titles at SPARK 2025, spanning mobile, competitive, and community-focused experiences. The breadth of announcements highlighted Tencent’s continued investment in socially engaging, multiplayer-oriented content and showed how large publishers were deepening live-service ecosystems to retain users through ongoing events, shared progression, and cross-title engagement.

August 2025: Samsung expanded its mobile cloud gaming platform into Europe, initially launching in the U.K. and Germany. This development was significant for social gaming because it reduced install friction, improved game discovery, and widened access to connected multiplayer experiences, helping publishers reach users more efficiently across mobile-first gaming environments.

September 2025: Roblox introduced Moments at RDC 2025, a new feature that lets users capture and share short-form gameplay clips. This was strategically important because it pushed social gaming into creator-led discovery and in-platform virality, strengthening the connection between gameplay, social sharing, user-generated promotion, and community-driven engagement loops.

Social Gaming Market Scope: Inquire before buying

| Social Gaming Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 36.18 Billion |

| Forecast Period 2026-2032 CAGR: | 16.03% | Market Size in 2032: | USD 102.39 Billion |

| Segments Covered: | by Platform | Mobile Devices PCs And Laptops Consoles Web Based Gaming |

|

| by Game Type | Casual Games Strategy Games Simulation Games Role Playing Games Multiplayer Online Battle Arena Games Sports Games Other Game Types |

||

| by Revenue Model | In App Purchases Advertisements Virtual Goods Subscription Services Premium Lead Generation |

||

| by Age Group | 13 To 18 Years 19 To 25 Years 26 To 35 Years Above 35 Years |

||

Social Gaming Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Social Gaming Market, Key Players:

- Zynga Inc.

- Electronic Arts Inc.

- Activision Blizzard, Inc.

- Tencent Holdings Limited

- Supercell Oy

- King Digital Entertainment

- Playtika Holding Corp.

- Roblox Corporation

- Epic Games, Inc.

- Gameloft SE

- NetEase, Inc.

- Ubisoft Entertainment S.A.

- Bandai Namco Entertainment Inc.

- Square Enix Holdings Co., Ltd.

- Scopely, Inc.

- GREE, Inc.

- Niantic, Inc.

- Miniclip SA

- Wooga GmbH

- Behaviour Interactive, Inc.

- DeNA Co., Ltd.

- PopCap Games, Inc.

- Socialpoint

- SYBO Games

- Peak Games