Smart Meters Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

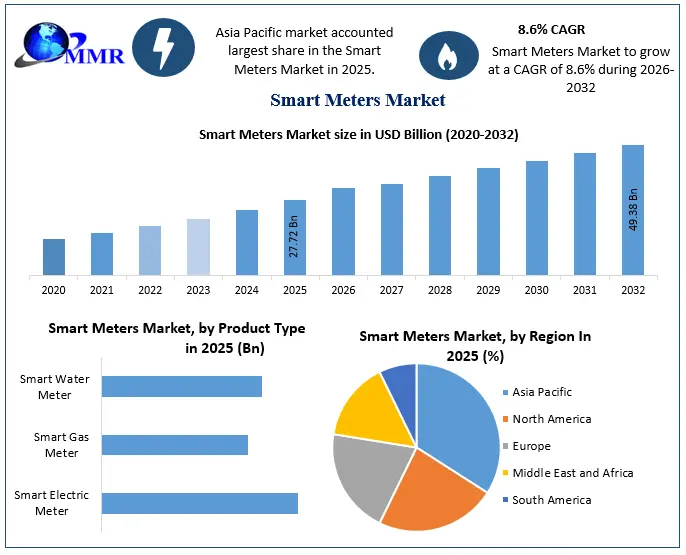

The Smart Meters Market size was valued at USD 27.72 Billion in 2025 and the total Smart Meter revenue is expected to grow at a CAGR of 8.6 % from 2026 to 2032, reaching nearly USD 49.38 Billion by 2032.

Smart Meters Market Overview:

The Smart Meters Market is of paramount importance in the modern energy landscape, facilitating efficient energy management and promoting sustainability. Smart meters offer both qualitative and quantitative benefits, enabling consumers to monitor their energy usage in real-time and make informed decisions to reduce consumption and lower utility bills. Moreover, for utility providers, smart meters enhance operational efficiency by automating meter readings, detecting energy theft or tampering, and improving outage management. These devices Contributes its role in achieving research objectives related to energy conservation, grid optimization, and environmental impact reduction.

Smart meters find applications across various sectors, including residential, commercial, and industrial. In the residential sector, smart meters empower homeowners to monitor and manage their energy usage, optimize appliance usage, and reduce utility bills. In commercial and industrial settings, smart meters enable businesses to track energy consumption in real-time, identify inefficiencies, and implement energy-saving measures to improve operational efficiency and reduce costs.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Smart Meters Market Dynamics:

Segment Analysis – Global Smart Meters Market

By Product Type,

The Smart Electric Meter segment dominated the global Smart Meters Market in 2025 and is expected to maintain its leading position throughout the forecast period. The segment's dominance is driven by large-scale smart electricity meter rollouts, increasing investments in smart grid infrastructure, and government mandates for advanced metering deployment. Smart electric meters enable real-time energy monitoring, remote meter reading, demand response, outage detection, and accurate billing, making them an integral component of modern power distribution networks. The growing integration of renewable energy sources, electric vehicle (EV) charging infrastructure, and distributed energy resources is further accelerating the adoption of smart electric meters across residential, commercial, and industrial sectors.

The Smart Gas Meter segment is expected to witness substantial growth during the forecast period, driven by the increasing focus on improving gas distribution efficiency, reducing operational losses, and enhancing consumer billing accuracy. Utilities are increasingly deploying smart gas meters to enable remote monitoring, leak detection, consumption analytics, and predictive maintenance. Government initiatives promoting digital utility infrastructure, coupled with rising investments in advanced metering infrastructure (AMI) for natural gas networks, are expected to support the expansion of this segment.

The Smart Water Meter segment is anticipated to register significant growth during the forecast period, supported by increasing concerns over water conservation, leakage management, and sustainable water resource utilization. Smart water meters provide real-time consumption data, remote monitoring capabilities, and early leak detection, helping utilities reduce non-revenue water losses and optimize distribution networks. Rising urbanization, smart city initiatives, and investments in intelligent water management systems are expected to further drive the adoption of smart water meters worldwide.

By Technology,

The Advanced Metering Infrastructure (AMI) segment dominated the global Smart Meters Market in 2025 and is expected to maintain its leading position throughout the forecast period. The segment's growth is driven by the increasing deployment of two-way communication networks that enable real-time data collection, remote meter reading, outage management, demand response, and dynamic pricing. Utilities are increasingly investing in AMI solutions to improve grid reliability, enhance operational efficiency, and support smart grid modernization initiatives. Furthermore, the integration of AMI with IoT, artificial intelligence (AI), and cloud-based analytics is enabling utilities to optimize energy management and improve customer engagement, thereby accelerating market growth.

The Automatic Meter Reading (AMR) segment is expected to witness steady growth during the forecast period, driven by its cost-effectiveness and ease of deployment, particularly in regions transitioning from conventional metering systems. AMR technology enables one-way communication for automated meter data collection, reducing manual meter reading costs and improving billing accuracy. The technology continues to be widely adopted by utilities seeking operational efficiency with lower infrastructure investments. However, as utilities increasingly prioritize real-time monitoring and bidirectional communication capabilities, many AMR deployments are gradually being upgraded to AMI-based systems, supporting the evolution of advanced digital utility networks.

Global Smart Meters Market Scope: Inquire before buying

| Smart Meters Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 27.72 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 8.6% | Market Size in 2032: | US $ 49.38 Bn. |

| Segments Covered: | By Product Type | Smart Electric Meter Smart Gas Meter Smart Water Meter |

|

| By Technology | Advanced Metering Infrastructure (AMI) Automatic Meter Reading (AMR) |

||

| By End-Use | Residential Commercial Industrial |

||

Global Smart Meters Market, by Region

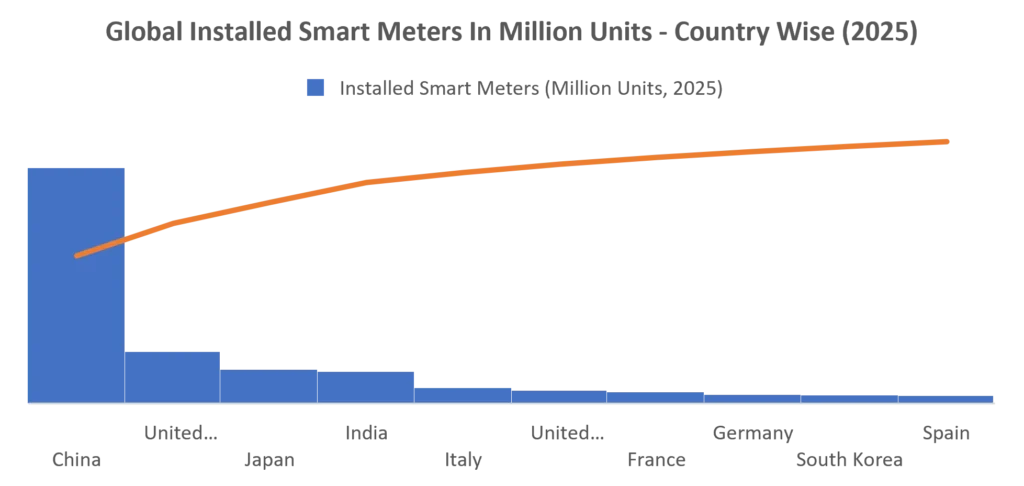

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Smart Meters Market Key Players:

North America:

1. Aclara Technologies LLC - USA

2. Itron Inc. - USA

3. Sensus USA Inc. - USA

4. Neptune Technology Group Inc. - USA

5. Badger Meter – USA

6. General Electric Ltd - USA

Europe:

1. Elster Group SE - Germany

2. Kamstrup A/S - Denmark

3. Diehl Stiftung & Co. KG - Germany

4. IGL Genesis Technologies - Germany

5. Pietro Fiorentini - Italy

6. Sagemcom SAS - France

7. Apator S.A - Poland

8. Honeywell International

9. EDMI - UK

Asia-Pacific:

1. Jiangsu Linyang Energy Co. Ltd - China

2. Ningbo Sanxing Electric Co. Ltd - China

3. Hexing Electric Company Ltd - China

4. Holley Metering Limited - China

5. Shenzhen Hemei Group Co. Ltd – China

6. Wasion Group Holdings - China

FAQs:

1. What are the growth drivers for the Smart Meters market?

Ans. Increasing mobile device management activities driving the Smart Meters Market

2. What are the major restraining factors for the Smart Meters Market growth?

Ans. Reduction in Investments for Infrastructure Development and Low Investment Returns is a restraining factor of Smart Meters Market

3. Which region is expected to lead the Smart Meters Market during the forecast period?

Ans. Asia Pacific is expected to lead the Smart Meters Market during the forecast period

4. What is the projected market size and growth rate of the Smart Meters Market?

Ans. The Smart Meters Market size was valued at USD 27.72 Billion in 2025 and the total Smart Meter revenue is expected to grow at a CAGR of 8.6 % from 2026 to 2032, reaching nearly USD 49.38 Billion by 2032.

5. What segments are covered in the Smart Meters Market report?

Ans. The segments covered in the Smart Meters Market report are Product Type, Technology, End Use, and Region.