Global Silicone Market Size by Type, End Use Industries, Distribution Channel and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

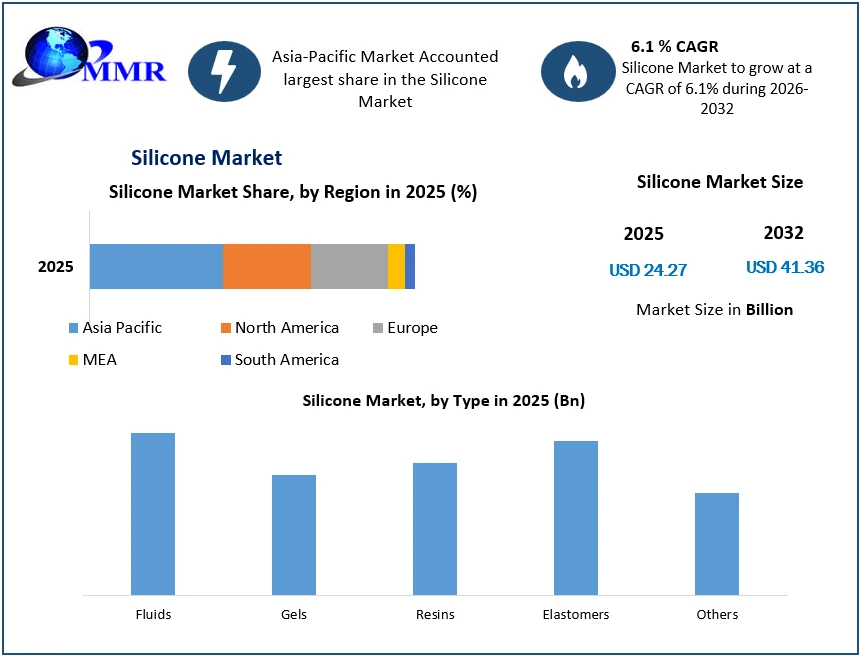

The Silicone Market size was valued at USD 24.27 Billion in 2025 and the total Silicone revenue is expected to grow at a CAGR of 6.1% from 2026 to 2034, reaching nearly USD 41.36 Billion.

Global Silicone Market Overview

Silicone is an important component of photovoltaic cells, which are used in solar panels. The growth of solar energy installations contributes to silicone demand. It is integral to the development of sensors, actuators, and other electronic components used in smart manufacturing, contributing to the Silicone Market demand.

The semiconductor sector is a large consumer of this component, and any increase in production prices has been affecting semiconductor and integrated circuit manufacture. This can result in higher component costs for electrical gadgets, affecting the entire electronic supply chain, influencing various industries, including the packaged food market, processed food industry, and ready-to-eat food market, where automation and electronics are widely used. China's electronics manufacturing sector, which includes consumer electronics, computers, and communication devices, is a major driver of silicone demand. The country's dominance in electronics manufacturing contributes significantly to its impact in this market.

To know about the Research Methodology :- Request Free Sample Report

Silicone Market Dynamics:

Rising Electronics Production to Boost the Silicone Demand

The increasing demand for silicone in the electronics industry is attributed to several factors. It is a versatile semiconductor material that plays a crucial role in the production of various electronic devices. Semiconductor devices are the backbone of electronic gadgets, providing the functionality and processing power required for a wide range of applications, from computing and communication to entertainment and automation. In the Asia-Pacific region, Taiwan is the biggest manufacturer of semiconductors; it accounts for over half of global production.

The electronics sector is characterized by ongoing technological breakthroughs, which result in the production of more sophisticated and powerful gadgets. China is the dominant country in the electronics industry. A variety of factors include the dominance of China in the electronics market, such as a large and trained workforce, low labor costs, and robust supply chain infrastructure. China has several large electronics firms, especially Foxconn, which assembles products for corporations such as Apple. Global smartphone and computer adoption has been a major driver of silicone consumption.

Expansion of the Solar Energy Sector Favors Silicone Market Development

The solar industry heavily relies on silicone for the production of photovoltaic cells used in solar panels. The solar industry demands high-purity silicone to ensure optimal efficiency in photovoltaic cells. This is typically achieved through the production of polycrystalline or monocrystalline silicone, with monocrystalline silicone often favored for higher efficiency. In 2022, solar PV (photovoltaic) generation climbed by a record 270 TWh (up 26%), reaching about 1300 TWh. Hence, the high demand for silicone in solar energy sector is anticipated to have a positive impact on the Silicone Market growth.

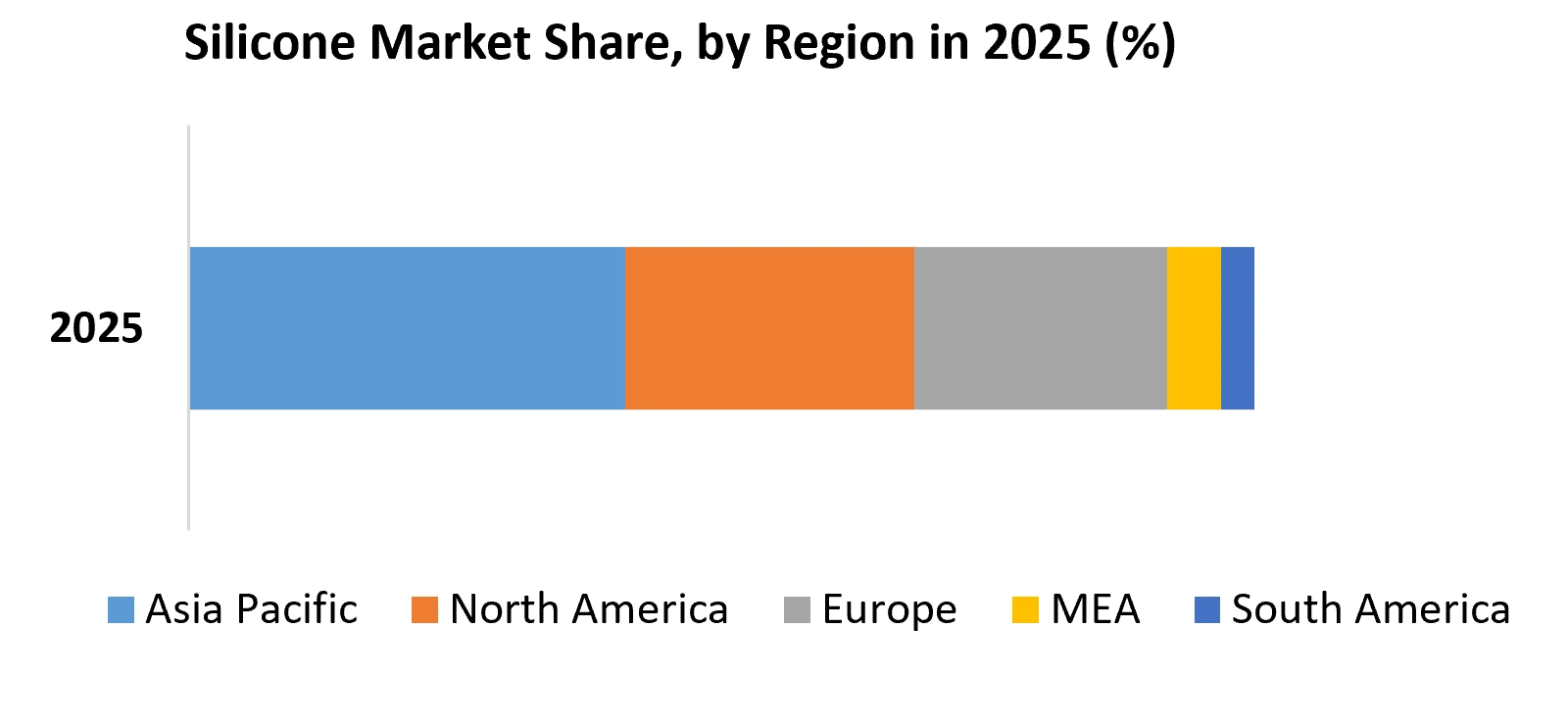

Silicone Market Regional Insights

The Asia Pacific area, notably China, has dominated the Silicone sector. China is a vital hub for electronics production, producing a significant share of the world's electronic devices. Silicone is a fundamental material in semiconductor manufacturing, and the demand for electronic gadgets in China has driven significant Silicone consumption. China's rapid industrialization and economic growth have increased the overall demand for Silicone across various sectors, including construction, automotive, and manufacturing.

Europe is anticipated to hold a significant market share. This is attributable to the increasing environmental regulations propelling the use of recyclable as well as sustainable silicone products. Similarly, the highly environmentally conscious population in European countries, fuelling the demand for electric vehicles, is anticipated to make a significant contribution to market progression.

Silicone Market Segment Analysis

Based on Type, the Elastomer Segment held a dominant position in the global silicone market in 2025. The dominance of the segment is driven by its versatile applications across various industries. Silicone elastomers are highly valued for their exceptional properties, including high thermal stability, flexibility, and resistance to UV radiation and extreme temperatures. These elastomers withstand temperature ranges from -60°C to 250°C, making them ideal for applications in the automotive, aerospace, electronics sectors, and the packaged food industry for safe and durable food contact materials. For instance, in the automotive industry, silicone elastomers are used in gaskets, seals, and hoses, where they must endure temperatures up to 200°C under the hood.

Silicone Market Competitive Landscape

The competitive landscape of the Silicone market is rapid and shaped by the presence of key players, their strategies, and the developing global demand for Silicone-based products. Asian companies, especially those in China and South Korea, have become major players in the market. Companies like China National Offshore Oil Corporation (CNOOC) and Samsung Electronics have a significant impact on the Silicone Industry growth. Companies are adopting environmentally friendly production practices, and some are investing in the development of sustainable Silicone alternatives, including for eco-friendly packaged food packaging.

Silicone Market Recent Industry Developments

• In September 2024, Wacker Chemie AG, a Silicone manufacturer, declared an investment of USD 160.34 million to increase its Silicone production facilities in China. The plant can produce Silicone fluids, Silicone emulsions, and Silicone elastomer gels suitable for food-safe packaged food applications.

| Date | Company | Development | Impact |

|---|---|---|---|

| 29 May 2026 | Univar Solutions B.V. | Expanded its strategic distribution agreement with Dow to supply advanced silicone additives for plastics and composites across Europe, the Middle East, and Africa (EMEA). | The collaboration optimizes manufacturer access to specialized technologies designed to enhance processing efficiency, material durability, and surface lubrication while supporting cross-regional sustainability goals. |

| 28 April 2026 | Wacker Chemie AG | Disclosed a solvent-free, gamma-sterilizable RTV-2 silicone pressure-sensitive adhesive (PSA) formulation engineered to retain functional integrity after intensive radiation exposure. | This development provides high-reliability performance solutions tailored specifically for the rigid quality demands of medical adhesive applications and wound care patches. |

| 20 April 2026 | Henkel AG & Co. KGaA | Launched a new line of silicone-based anti-fingerprint coatings engineered for advanced automotive displays without the use of per- and polyfluoroalkyl substances (PFAS). | The product addresses strict environmental compliance frameworks while providing high durability, heat cure cycle compatibility, and clean optics for automotive display manufacturers. |

| 16 April 2026 | Wacker Chemie AG | Expanded its biotechnology partnership with Amyris to develop scalable, bio-based functional ingredients for the personal care industry by combining biological building blocks with silicone specialties. | This integration allows cosmetic formulators to transition toward resource-efficient, sustainable formulations while maintaining the high performance and compatibility benchmarks of traditional silicone ingredients. |

| 17 February 2026 | Elkem ASA | Signed a definitive share purchase agreement to divest the majority stake of its Silicones division to Bluestar Elkem International Co. Ltd. S.A. in exchange for the redemption and cancellation of all Bluestar-held Elkem shares. | The transaction structurally refines the company into a pure-play metals and materials producer while substantially reducing operational complexity, lowering capital intensity, and improving long-term cash flow generation. |

| 09 January 2026 | Trelleborg Group AB | Acquired Austria-based Nexus Elastomer Molds to integrate specialized tooling systems and automated production cells for liquid silicone rubber (LSR) processing. | The strategic acquisition significantly reduces prototyping lead times and scales production capabilities for complex geometries in high-growth medical technology and advanced industrial sealing portfolios. |

Silicone Market Scope: Inquiry Before Buying

| Global Silicone Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 24.27 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 6.1% | Market Size in 2034: | USD 41.36 Bn. |

| Segments Covered: | by Type | Fluids Gels Resins Elastomers Others |

|

| by End Use Industries | Transportation Construction Materials Electronics Healthcare Industrial Processes Personal Care and Consumer Products Others |

||

| by Distribution Channel | Offline Online |

||

Silicone Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Silicone Market, Key Players

1. General Atomics

2. Safran SA

3. MacTaggart, Scott and Company Limited

4. Sojitz Aerospace Corporation

5. QinetiQ Group plc

6. Zodiac Aerospace

7. General Atomics

8. Runway Safe

9. SCAMA AB

10. Boeing

11. Atech Inc

12. A-Laskuvarjo

13. Curtiss-Wright Corp

14. Escribana Mechanical & Engineering S.L

15. Foster-Mille, Inc

16. General Atomics

17. Scama AB

18. Victor Balata Belting Company

19. Wire Rope Industries

20. WireCo WorldGroup

21. Aries S.A

22. Dow Silicones

23. Wacker Chemie AG

24. Momentive Performance Materials

25. Elkem Silicones

26. Shin‑Etsu Chemical Co., Ltd.

27. KCC Silicone (KCC Corporation)

28. Silicone Engineering Ltd

29. Simtec Silicone Parts, LLC

30. Genesee Polymers Corporation

FAQs:

1. What is the study period of the market?

Ans. The Global Silicone Market is studied from 2025-2034.

2. What is the growth rate of the Silicone Market?

Ans. The Silicone Market is growing at a CAGR of 6.1 % over the forecast period.

3. What is the market size of the Silicone Market by 2034?

Ans. The market size of the Silicone Market by 2034 is expected to reach USD 41.36 Bn.

4. What is the forecast period for the Silicone Market?

Ans. The forecast period for the Silicone Market is 2026-2034.

5. What was the Global Silicone Market size in 2025?

Ans: The Global Silicone Market size was USD 24.27 Billion in 2025.