Robotic Welding Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

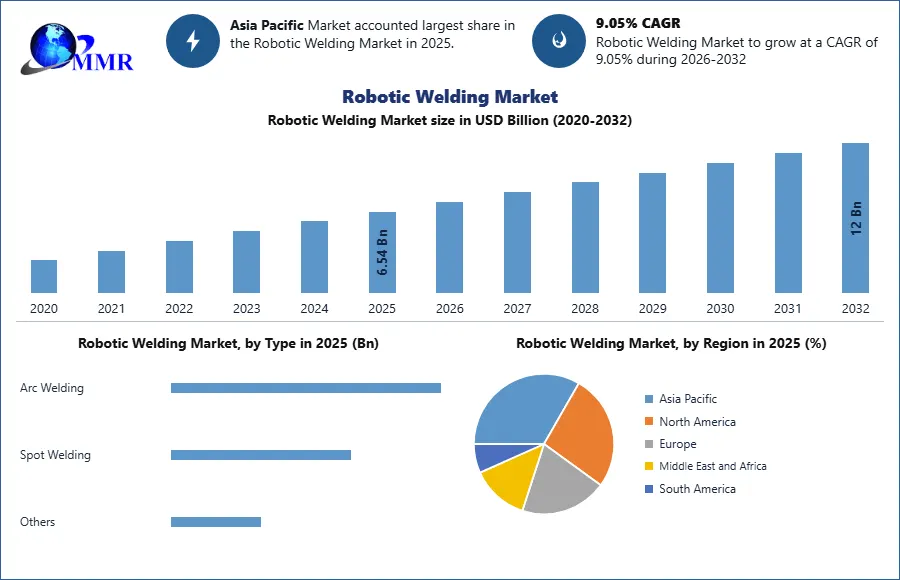

Robotic Welding Market was valued US$ 6.54 Bn in 2025 and is expected to reach US$ 12 Bn by 2032 , at a CAGR of 9.05 % during a forecast period.

Robotic Welding Market Overview:

The increasing industrial automation, rising demand for precision manufacturing, and growing adoption of smart factory technologies across automotive, aerospace, heavy machinery, and metal fabrication industries. Robotic welding systems improve production efficiency, welding consistency, operational safety, and product quality while reducing labor dependency and manufacturing errors. Industries are increasingly deploying robotic welding solutions for high-volume production processes requiring speed, repeatability, and precision. Advancements in artificial intelligence, machine vision, IoT integration, and collaborative robotics are enhancing welding automation capabilities globally. Asia-Pacific dominates the market due to strong manufacturing activity and rising industrial robotics adoption in China, Japan, South Korea, and India. Continuous innovation in automated welding systems and Industry 4.0 implementation is expected to create significant growth opportunities for the Robotic Welding Market during the forecast period.

To know about the Research Methodology :- Request Free Sample Report

Robotic Welding Market Dynamics:

Trend – Integration of AI and Smart Welding Automation

One of the major trends shaping the Robotic Welding Market is the increasing integration of artificial intelligence, machine vision, and smart automation technologies into robotic welding systems. Manufacturers are increasingly adopting AI-powered robotic welding solutions capable of real-time seam tracking, adaptive welding control, predictive maintenance, and automated quality inspection. Smart robotic welding systems improve welding precision, reduce material waste, and enhance production flexibility across high-volume manufacturing environments. Industries such as automotive, shipbuilding, aerospace, and heavy equipment manufacturing are rapidly implementing intelligent robotic welding technologies to support Industry 4.0 transformation initiatives. Additionally, collaborative welding robots (cobots) are gaining popularity due to their ability to safely operate alongside human workers and support flexible production processes. Advancements in sensor technologies, cloud-based analytics, digital twins, and IoT-enabled monitoring systems are further improving robotic welding efficiency and operational reliability. The growing demand for automated, high-precision manufacturing continues to accelerate smart robotic welding adoption globally.

Driver – Increasing Demand for Industrial Automation and Labor Efficiency

The increasing demand for industrial automation and improved labor efficiency is a major driver fueling the growth of the Robotic Welding Market. Manufacturing industries are rapidly adopting robotic welding systems to improve productivity, reduce operational costs, and address labor shortages in skilled welding operations. Robotic welding solutions deliver consistent weld quality, higher production speed, and greater precision compared to manual welding processes. Industries such as automotive, construction equipment, railways, and metal fabrication increasingly rely on robotic welding systems for repetitive and high-volume manufacturing applications. In addition, robotic welding improves workplace safety by minimizing worker exposure to hazardous fumes, heat, and repetitive physical strain. Rising labor costs and increasing quality standards are further encouraging manufacturers to automate welding operations. Government support for smart manufacturing and industrial modernization initiatives is also accelerating robotic adoption globally. Continuous advancements in AI, machine vision, and robotic motion control technologies are further strengthening market growth across developed and emerging industrial economies.

Restraint – High Initial Investment and System Integration Complexity

High initial investment and system integration complexity remain major restraints affecting the growth of the Robotic Welding Market. Advanced robotic welding systems require substantial capital expenditure for robotic arms, welding power sources, sensors, machine vision systems, programming software, and automation infrastructure. Small and medium-sized enterprises often face financial challenges in implementing robotic welding technologies due to high setup and maintenance costs. Additionally, integrating robotic welding systems with existing manufacturing lines can be technically complex and time-consuming, requiring specialized expertise and workforce training. Companies may also encounter operational disruptions during installation and calibration processes. Inconsistent production environments, material variations, and complex welding geometries can create programming and operational challenges for automated systems. Furthermore, maintenance requirements, software upgrades, and cybersecurity concerns related to connected industrial automation platforms can increase long-term operational costs.

Robotic Welding Market Segment Analysis

By Type , The Arc Welding segment dominates the Robotic Welding Market due to its widespread use across automotive, construction, shipbuilding, heavy machinery, and metal fabrication industries. Robotic arc welding systems are highly preferred for applications requiring strong, precise, and continuous welds in high-volume production environments. These systems improve welding consistency, reduce material waste, and enhance operational efficiency while minimizing human error and labor dependency. Industries increasingly adopt robotic arc welding solutions for complex welding tasks involving steel structures, automotive frames, pipelines, and industrial equipment manufacturing. Additionally, advancements in AI-enabled seam tracking, automated torch positioning, and adaptive welding technologies are significantly improving robotic arc welding precision and productivity. The growing implementation of smart manufacturing and Industry 4.0 technologies is further accelerating demand for robotic arc welding systems globally. Their ability to support flexible production, improve workplace safety, and deliver high-quality weld performance continues to strengthen the dominance of the arc welding segment.

By Payload , The 50–150 kg payload segment dominated the Robotic Welding Market in 2025 due to its versatility and suitability for a wide range of industrial welding applications. Robots within this payload capacity range are extensively used in automotive manufacturing, metal fabrication, heavy equipment production, and industrial machinery assembly where moderate to heavy welding tools and components are handled efficiently. These robotic systems offer an optimal balance between flexibility, operational reach, payload strength, and welding precision, making them highly preferred across medium- and large-scale manufacturing facilities. Manufacturers increasingly deploy 50–150 kg robotic welding systems for arc welding, spot welding, and multi-axis automated welding applications requiring high productivity and operational stability. Additionally, advancements in servo motors, motion control systems, and AI-powered robotic programming are improving welding efficiency and process adaptability. The growing demand for automated high-volume manufacturing and flexible welding automation solutions continues to strengthen the dominance of the 50–150 kg payload segment globally.

Robotic Welding Market Regional Analysis

Asia-Pacific dominated the Robotic Welding Market in 2025 due to rapid industrialization, strong automotive manufacturing activity, and increasing investments in industrial automation across China, Japan, South Korea, and India. China remains the largest regional market driven by large-scale manufacturing expansion, smart factory initiatives, and rising deployment of industrial robots in automotive and electronics production facilities. Japan and South Korea are global leaders in robotics innovation and robotic welding technologies, supported by the presence of major robotics manufacturers such as FANUC, Yaskawa, Kawasaki Robotics, and Panasonic. The region is witnessing significant adoption of robotic welding systems across automotive assembly, shipbuilding, heavy machinery, and metal fabrication industries. Rising labor costs, increasing focus on manufacturing efficiency, and government initiatives promoting Industry 4.0 transformation are accelerating demand for automated welding solutions. Additionally, expanding electric vehicle production and infrastructure development projects are further supporting market growth. Strong industrial infrastructure and continuous advancements in robotic automation technologies continue to strengthen Asia-Pacific’s dominance in the global robotic welding market.

Recent Developments

March 2025: Kawasaki Heavy Industries, Ltd. expanded its robotic welding portfolio through advanced AI-enabled arc welding robots designed for automotive, shipbuilding, and heavy industrial manufacturing applications. The company introduced upgraded welding automation systems with real-time seam tracking, adaptive motion control, and intelligent welding parameter optimization technologies. Kawasaki also focused on improving robotic precision, operational flexibility, and collaborative welding capabilities for smart factory environments. The development supports increasing global demand for high-speed, high-accuracy robotic welding systems capable of reducing labor dependency and improving production efficiency across large-scale industrial manufacturing facilities implementing Industry 4.0 automation strategies.

February 2025: Nachi-Fujikoshi Corp. strengthened its intelligent robotic welding systems through the launch of advanced AI-powered welding robots equipped with machine vision and autonomous path correction technologies. The company enhanced robotic welding accuracy, operational consistency, and multi-axis motion control capabilities for automotive and metal fabrication industries. Nachi-Fujikoshi also focused on integrating predictive maintenance and smart monitoring systems into robotic welding operations to improve manufacturing efficiency and reduce downtime.

Global Robotic Welding Market Scope : Inquire before buying

| Robotic Welding Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 6.54 USD Billion |

| Forecast Period 2026-2032 CAGR: | 9.05% | Market Size in 2032: | 12 USD Billion |

| Segments Covered: | by Type | Arc Welding Spot Welding Others |

|

| by Payload | <50 kg 50–150 kg >150 kg |

||

| by End User | Automotive & Transportation Electricals & Electronics Aerospace & Defense Metals & Machinery Others |

||

Global Robotic Welding Market, By Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/Competitors profiles covered in the Robotic Welding Market report in strategic perspective

- Kawasaki Heavy Industries, Ltd. (Japan)

- Nachi-Fujikoshi Corp. (Japan)

- Daihen Corporation (Japan)

- Denso Corporation (Japan)

- ABB Ltd. (Switzerland)

- Yaskawa Electric Corporation (Japan)

- Panasonic Corporation (Japan)

- KUKA AG (Germany)

- FANUC Corporation (Japan)

- Siasun Robot & Automation Co., Ltd. (China)

- Comau S.p.A. (Italy)

- IGM Robotersysteme AG (Austria)

- Carl Cloos Schweißtechnik GmbH (Germany)

- Hyundai Robotics Co., Ltd. (South Korea)

- Welding Engineering 101 (U.S.)

- Lincoln Electric Holdings, Inc. (U.S.)

- Affordable Robotic & Automation Pvt. Ltd. (India)

- BTD Manufacturing, Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Omron Corporation (Japan)

- Universal Robots A/S (Denmark)

- Epson Robots (Japan)

- Genesis Systems Group LLC (U.S.)

- Miller Electric Mfg. LLC (U.S.)

- CLOOS Robotic Welding Inc. (U.S.)

- Robotic Welding Solutions, Inc. (U.S.)

- OTC Daihen Inc. (Japan)

- Acieta LLC (U.S.)