Rigid Plastic Packaging Market by Type, Production Process, Material, Application and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

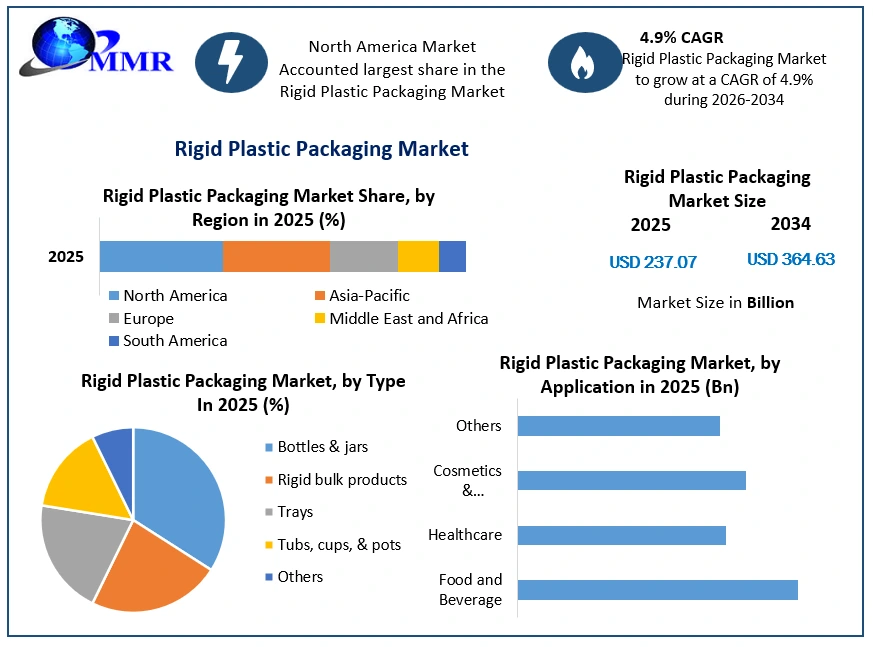

The Rigid Plastic Packaging Market size was valued at USD 237.07 Billion in 2025 and the total Rigid Plastic Packaging revenue is expected to grow at a CAGR of 4.9% from 2026 to 2034, reaching nearly USD 364.63 Billion.

Rigid Plastic Packaging Market Overview:

The Rigid Plastic Packaging Market is a dynamic and integral segment within the broader packaging industry. Rigid plastic packaging plays a pivotal role in providing robust and durable solutions for various products across multiple sectors. Rigid Plastic packaging market is characterized by its versatility, offering a wide range of packaging options, including bottles, jars, trays, tubs, cups, and pots, catering to the diverse needs of industries such as food and beverages, pharmaceuticals, healthcare, cosmetics, and toiletries. Driving the evolution of the market are key factors that underscore its significance in the packaging landscape.

The lightweight and durable properties of rigid plastic packaging make it an attractive choice, reducing transportation costs and ensuring the protection of products during transit. Moreover, its cost-effectiveness compared to alternative materials positions it as a preferred solution for manufacturers looking to balance quality and affordability.

Innovation is a hallmark of the Rigid Plastic Packaging Market, with continuous advancements in design and technology shaping the industry. This includes improvements in barrier properties, shelf life extension, and enhanced protection against external factors. The market is also witnessing a growing emphasis on consumer convenience, with packaging solutions offering features like easy-to-open mechanisms, resealability, and portion control. The detailed and constructive formation of key drivers, opportunities, and unique segmentation outputs structural and optimistic data. Validated using primary as well as secondary research methodology and scope of the Global market.

Rigid Plastic Packaging Market Growth Outlook

To know about the Research Methodology:-Request Free Sample Report

Rigid Plastic Packaging Market Dynamics

Lightweight and Durable Properties with Innovations in Design and Technology Boosting the Rigid Plastic Packaging Market Growth

The lightweight and durable properties of rigid plastic packaging drive its adoption in various industries, contributing to market growth and enhancing its potential. The cost-effectiveness of these features reduces transportation costs and ensures product protection, further solidifying the Rigid Plastic Packaging Market share in the packaging industry.

The cost-effectiveness of rigid plastic packaging positions it as a market leader, with the potential for increased penetration in industries looking for economical packaging solutions. Manufacturers are drawn to its cost advantages, making it a preferred choice and impacting the market share of alternative materials. Ongoing innovations in the design and technology of rigid plastic packaging fuel industry growth, leading to enhanced features and improved product capabilities. These innovations contribute to Rigid Plastic Packaging Market share expansion as manufacturers strive to stay at the forefront of emerging trends and consumer demands.

Rigid plastic packaging's ability to offer consumer convenience is a significant driver, contributing to its market share and presenting growth opportunities. Features such as easy-to-open mechanisms and reseal ability enhance consumer satisfaction and contribute to the packaging market's continuous innovation. The increasing emphasis on environmental sustainability boosts the demand for recyclable and eco-friendly packaging solutions within the rigid plastic packaging market. Advancements in sustainable practices become opportunities for market players to innovate and capture a larger market share. The growth in end-use industries such as food and beverages, pharmaceuticals, and personal care presents opportunities in market to increase its share. The rising demand for reliable and versatile packaging solutions aligns with the market's potential for sustained growth.

Environmental Concerns and Volatility in Raw Material Prices Restraining the Rigid Plastic Packaging Market Growth

Environmental concerns pose challenges to the growth potential of the rigid plastic packaging market. Criticism and increased scrutiny due to the environmental impact of single-use plastics lead to potential restraints on market penetration and highlight the need for sustainable alternatives. Stringent government regulations aimed at reducing plastic waste and promoting recycling impact the market share of rigid plastic packaging. Compliance with these regulations becomes a key factor influencing market dynamics and pricing analysis within the industry. The shift in consumer preferences towards alternative packaging materials challenges the market penetration of rigid plastic packaging. Materials like glass, paper, and metal, perceived as more sustainable, create a competitive landscape that influences the market's share and pricing dynamics.

The Rigid Plastic Packaging Market faces fluctuations in raw material prices, particularly petrochemicals, impacting manufacturing costs and profit margins. Global Market players must conduct thorough pricing analyses to navigate these fluctuations and maintain cost-effectiveness. Negative public perception surrounding plastic waste influences consumer choices and creates opportunities for alternative materials, impacting on the rigid plastic packaging market share. Addressing these perceptions becomes essential for market players to seize opportunities and overcome restraints. Supply chain disruptions, such as those caused by natural disasters or global health crises like the COVID-19 pandemic, highlight vulnerabilities in the industry's operational resilience. Navigating these disruptions becomes crucial for maintaining market share and seizing opportunities in an evolving landscape.

Global Market Segment Analysis

Type:

Representing a substantial rigid plastic packaging market share, the bottles and jars segment is propelled by the escalating demand for convenient and sustainable packaging solutions. Industries spanning food and beverages, cosmetics, and healthcare prominently contribute to the segment's growth, making it a dominant segment. Targeting industries with requirements for robust packaging on a larger scale, rigid bulk products make a significant contribution to the market. Their durability and protective characteristics position them as pivotal players in safeguarding bulk quantities, establishing them as a booming segment.

Widely adopted in the food and healthcare sectors, trays offer a stable and organized platform for products. The market growth for trays is fuelled by the increasing demand for lightweight yet visually appealing packaging solutions, solidifying their status as a major segment in market. Addressing the demand for individual or small-quantity packaging, this segment caters to cosmetics and toiletries industries. The adoption of tubs, cups, and pots is driven by their convenience, ease of use, and shelf appeal, positioning them as an emerging segment rigid plastic packaging market.

Production Process:

The extrusion process is a significant contributor to the market, particularly in producing films, sheets, and profiles. It stands out for its cost-effectiveness and versatility in creating a variety of packaging formats, making it a dominant segment in the rigid plastic packaging market. Widely employed for intricate and detailed packaging components, injection molding is efficient in mass production and offers versatility in material usage. Its prominence contributes to the market's diversity, establishing it as a booming segment. Particularly prevalent in the production of bottles and containers, blow molding is characterized by advantages such as lightweight designs and cost efficiency.

Its adaptability to different shapes and sizes enhances its market presence, marking it as a major segment. Finding application in the production of trays, cups, and various packaging solutions, thermoforming stands out for its flexibility in design and cost-effectiveness for large-scale production, positioning it as an emerging segment in the rigid plastic packaging market.

Material:

With a rising emphasis on sustainability, bioplastics experience heightened demand. This eco-friendly material caters to environmentally conscious industries and consumers, significantly contributing to rigid plastic packaging market growth. Bioplastics are an emerging segment with immense market potential. Renowned for its durability and versatility, PE is widely utilized in various packaging applications, especially in bottles, containers, and films, making it a dominant segment. PET emerges as a preferred material for bottles, particularly in the beverage industry, owing to its clarity, lightweight nature, and recyclability. PET holds a major segment share in the market. Commonly used for packaging applications, PS offers insulation properties and finds application in trays, cups, and other disposable items. PS is a booming segment in the rigid plastic packaging market.

Valued for its strength and heat resistance, PP finds suitability in applications across the food and healthcare industries, establishing itself as a dominant segment. Despite environmental considerations, PVC is still utilized, particularly in the healthcare sector where its clarity and barrier properties play a crucial role. PVC maintains a significant rigid plastic packaging market share as a dominant segment. Known for its lightweight and insulating properties, EPS is a preferred choice for protective packaging in various industries, positioning itself as a major segment.

Rigid Plastic Packaging Industry Ecosystem:

Rigid Plastic Packaging Market Regional Analysis

The Rigid Plastic Packaging Market is a dynamic industry with distinctive characteristics across various regions, each contributing to its overall dynamics. A comprehensive regional analysis sheds light on the market trends, challenges, and opportunities present in North America, Asia Pacific, Europe, and the Middle East and Africa (MEA).

North America, particularly the United States, plays a key role in the Rigid Plastic Packaging Market, driven by advanced packaging technologies and a robust industrial landscape. The region's dominance is underscored by the high adoption of sustainable packaging solutions and a growing preference for eco-friendly materials. The market in North America, including the US, demonstrates a significant market share in the global rigid plastic packaging sector. Key players in this region contribute to the regional growth, emphasizing recyclability, advanced production processes, and leveraging the market potential.

The Middle East and Africa represent a region with a growing presence in the Rigid Plastic Packaging Market. The market dynamics in MEA are shaped by enlarging consumer markets, increasing urbanization, and a rising demand for packaged goods. The Gulf Cooperation Council (GCC) countries, including a notable market share in countries like the UAE and Saudi Arabia, witness significant investments in packaging infrastructure and technologies. MEA is positioned as an emerging segment in the global market, showcasing potential for market expansion driven by economic development, changing consumer preferences, and a surge in manufacturing activities.

The Asia Pacific region, spearheaded by countries such as China and India, is experiencing robust growth in the Rigid Plastic Packaging Market. This growth is fuelled by rapid industrialization, urbanization, and a burgeoning middle-class population. China and Indonesia, in particular, showcase increased demand for rigid plastic packaging across diverse sectors, including food and beverages, healthcare, and cosmetics. This region stands out as a booming segment in the global market, with immense growth potential.

The rising Rigid Plastic Packaging Market share in these countries reflects their significant contribution to the overall market dynamics. Europe, a mature yet innovative market for rigid plastic packaging, distinguishes itself with a strong emphasis on sustainability and environmental consciousness. Countries like Germany, France, and the United Kingdom lead the way in adopting eco-friendly packaging materials, contributing significantly to the market's evolution. These nations hold a substantial market share in the global rigid plastic packaging sector. The European region is considered a major segment known for its technological advancements, focus on recyclability, and a well-established infrastructure supporting sustainable packaging practices.

Recent Advancements in the Rigid Plastic Packaging Sector:

The rigid plastic packaging sector is not only experiencing regional market performance but is also contributing significantly to the global rigid plastic packaging market growth rate. Technological advancements have been a driving force, propelling the industry forward. Innovations such as lightweight and cost-effective materials with superior barrier properties are reshaping the global market landscape. The market's response to consumer demand trends, particularly the emphasis on sustainability, has played a crucial role in shaping its trajectory. The integration of environmentally friendly processes, including the adoption of biodegradable plastics and recycling programs, reflects the industry's commitment to meeting consumer expectations and addressing environmental concerns.

The rigid plastic packaging market is constantly evaluating its environmental impact, conducting thorough environmental impact evaluations to ensure responsible practices. Regulatory influences are increasingly shaping themarket, with a focus on sustainability and waste reduction. The industry's response to regulatory measures is evident in the adoption of eco-friendly processes and materials. As the regulatory landscape evolves, the competitive landscape analysis becomes more critical, influencing business strategies and market positioning. Raw material availability and costs play a pivotal role in shaping the market's profit margins. The industry's ability to manage and navigate fluctuations in raw material prices directly impacts its profitability.

In this dynamic landscape, profit margin calculation becomes an essential aspect of strategic decision-making. Companies in the rigid plastic packaging sector are continually assessing their profit margins to ensure financial viability and sustainability. To stay competitive, the industry is adopting industry expansion strategies. These strategies encompass market diversification, geographic expansion, and the exploration of new applications for rigid plastic packaging. The industry's commitment to technological advancement rate is evident in the rapid adoption of advanced manufacturing techniques, such as blow molding and thermoforming. These techniques not only enhance product design and functionalities but also contribute to the rigid plastic packaging industry's efficiency and competitiveness.

The rigid plastic packaging industry is navigating a complex landscape influenced by global market growth rates, regional market performance, technological advancements, consumer demand trends, raw material availability and costs, environmental impact evaluations, regulatory influences, competitive landscape analysis, profit margin calculations, and industry expansion strategies. The convergence of these factors shapes the industry's trajectory, and industry players must strategically align with these trends to thrive in an ever-evolving rigid plastic packaging market.

Rigid Plastic Packaging Market Scope: Inquire before buying

| Global Rigid Plastic Packaging Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 237.07 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.9% | Market Size in 2034: | USD 364.63 Bn. |

| Segments Covered: | By Type | Bottles & jars Rigid bulk products Trays Tubs, cups, & pots Others |

|

| By Production Process | Extrusion Injection molding Blow molding Thermoforming Others |

||

| By Material | Bioplastics Polyethylene (PE) Polyethylene Terephthalate (PET) Polystyrene (PS) Polypropylene (PP) Polyvinyl Chloride (PVC) ed Polystyrene (EPS) Others |

||

| By Application | Food and Beverage Healthcare Cosmetics & toiletries Others |

||

Rigid Plastic Packaging Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Rigid Plastic Packaging Market Key Players:

Competitive Dynamics in Rigid Plastic Packaging Industry is marked by robust brand competition and strategic investments aimed at market penetration. Companies are focusing on innovative product creation and manufacturing growth to enhance their competitive position. Key players are leveraging diverse distribution channels to optimize reach and improve market position. Competitive dynamics involve benchmarking against industry standards, fostering continuous improvement. As demand for sustainable and high-performance packaging rises, firms are investing in advanced technologies to differentiate their offerings, further shaping the industry's competitive dynamics and enhancing overall industry competitiveness.

Major Global Key Players:

1. Tetra Pak International S.A. (Switzerland) - Global Presence

2. Sealed Air Corporation (United States) - Global Presence

3. Reynolds Group Holdings Limited (New Zealand) - Global Presence

4. Bemis Company, Inc. (United States) - Global Presence

5. Coveris Holdings S.A. (Luxembourg) - Global Presence

Leading Key Players in North America:

1. T Amcor plc (Australia)

2. Berry Global Group, Inc. (United States)

3. Ball Corporation (United States)

4. Sonoco Products Company (United States)

5. Silgan Holdings Inc. (United States)

Market Follower key Players in Europe:

1. RPC Group Plc (United Kingdom)

2. ALPLA Werke Alwin Lehner GmbH & Co KG (Austria)

3. Gerresheimer AG (Germany)

4. Constantia Flexibles Group GmbH (Austria)

5. Coveris Holdings S.A. (Luxembourg)

Prominent Key player Asia Pacific:

1. Toyo Seikan Group Holdings, Ltd. (Japan)

2. Huhtamaki Oyj (Finland)

3. Cosmopak Pty Ltd (Australia)

4. Zhuhai Zhongfu Enterprise Co., Ltd. (China)

5. UFlex Limited (India)

Leading key player in Middle East & Africa:

1. Nampak Limited (South Africa)

2. Saudi Basic Industries Corporation (SABIC) (Saudi Arabia)

3. PACCOR (Germany) - has a significant presence in the Middle East

4. ALPLA Werke Alwin Lehner GmbH & Co KG (Austria) - with operations in Africa

5. BWAY Corporation (United States) - operates in the Middle East

Growing Companies in South America:

1. Graham Packaging Company (United States) - operates in South America

2. Plásticos Novel S/A (Brazil)

3. Rigolleau S.A. (Argentina)

4. Greif, Inc. (United States) - has a presence in South America

5. Embalagens Flexíveis Flexoprint Ltda. (Brazil)

Frequently Asked Questions:

1. What is Rigid Plastic Packaging?

Ans: Rigid plastic packaging refers to containers and packaging materials made from stiff and unyielding plastics, providing durability and protection to various products.

2. What Drives the Growth of the Rigid Plastic Packaging Market?

Ans: The market is driven by factors such as lightweight and durable properties, cost-effectiveness, innovations in design and technology, consumer convenience, recyclability, and growth in end-use industries.

3. Which End-Use Industries Contribute to the Demand for Rigid Plastic Packaging?

Ans: Rigid plastic packaging finds extensive use in industries like food and beverages, pharmaceuticals, healthcare, cosmetics, and toiletries.

4. What Are the Key Production Processes in Rigid Plastic Packaging?

Ans: Major production processes include extrusion, injection molding, blow molding, and thermoforming.

5. What was the Global Rigid Plastic Packaging Market size in 2025?

Ans: The Global Rigid Plastic Packaging Market size was USD 237.07 Billion in 2025.