Global Processed Snacks Market Size by Product – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2032

Overview

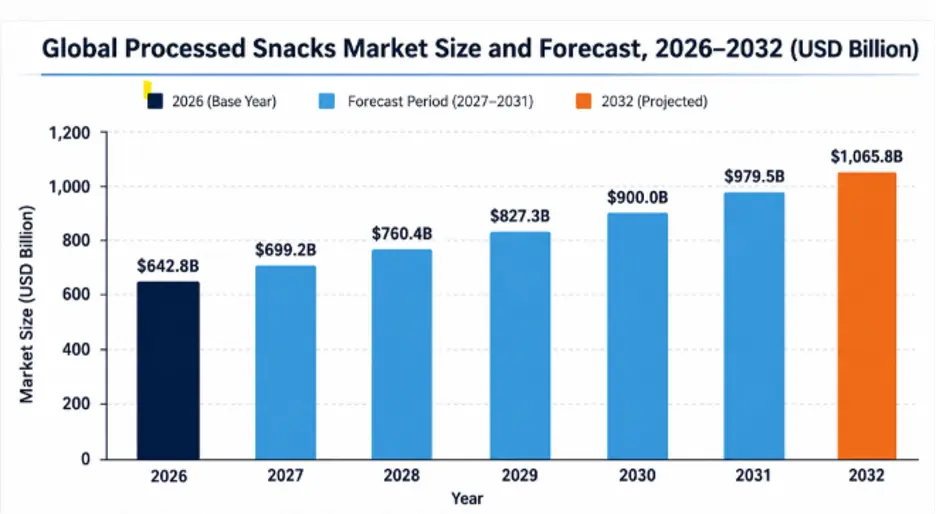

The Global Processed Snacks Market was valued at USD 642.8 billion in 2026 and is projected to reach USD 1,065.8 billion by 2032, expanding at a CAGR of 8.7% during the forecast period. The report provides an in-depth analysis of market size, regional dynamics, product segmentation, distribution channels, and emerging trends, including convenience-driven consumption and health-focused snacking innovations influencing industry growth.

| USD 642.8B 2026 Market Size |

8.7% CAGR 2026–2032 Growth Rate |

USD 1,065.8B 2032 Projected Size |

Key Market Highlights

- The Global Processed Snacks Market is estimated to grow from USD 642.8 Bn (2025) to USD 1,065.8 Bn by 2032 at an 8.7% CAGR. Growth is driven by increasing urbanization, rising dual-income households, evolving on-the-go consumption patterns, and continuous product innovation across better-for-you, premium, and indulgent snack categories.

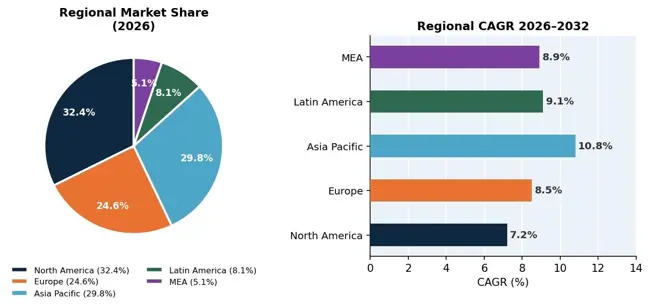

- Asia Pacific dominates the market with a 29.8% share and the highest CAGR of 10.8%. Growth is supported by expanding middle-class populations in China, India, Indonesia, and Vietnam, increasing penetration of modern retail formats, and localized flavor innovations.

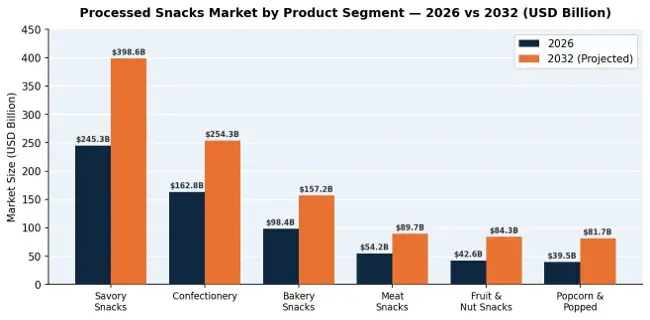

- Savory snacks accounted for approximately 38% of the market, making them the largest product segment. Meanwhile, fruit & nut snacks and popcorn/popped snacks are expected to witness the fastest growth, supported by health-oriented product reformulation and premium product positioning.

- Among distribution channels, supermarkets and hypermarkets accounted for the largest revenue share, while e-commerce platforms and convenience stores are projected to register the fastest growth, supported by the expansion of direct-to-consumer (D2C) brands and increasing impulse purchases.

- Clean-label, reduced-sodium, high-protein, and plant-based snack formulations are reshaping the competitive landscape, compelling legacy manufacturers to accelerate R&D and reformulating product portfolios to maintain market competitiveness and strengthen shelf presence.

The Processed Snacks Market has changed dramatically over the last ten years, due to consumer preferences and innovations. What was once a marketplace dominated by traditional potato chips and candy is now a broad, multi-segment snack industry that includes better-for-you (BFY) snacks, premium and artisanal products, The market is expected to reach USD 1,065.8 billion by 2032, growing at a CAGR of 8.7% during the forecast period (2026-2032)

To know about the Research Methodology :- Request Free Sample Report

The structural drivers of market expansion are rooted in fundamental socioeconomic shifts. Urbanisation is accelerating in Asia Pacific, Africa and Latin America and producing large consumer populations with increasing disposable income and a desire for convenience food. In mature markets such as North America and Western Europe, premiumization and health-and-wellness trends are increasing average basket values and driving category innovation

Snack manufacturers are increasingly balancing two priorities: satisfying indulgent demand while simultaneously strengthening their better-for-you (BFY) portfolios. The response — higher-protein crisps, chickpea-based chips, freeze-dried fruit, air-popped grain snacks and probiotic-infused bars — highlights the industry's ability to address evolving consumer preferences. Digital-native direct-to-consumer (D2C) brands are reshaping traditional retail channels, accelerating product development cycles and forcing incumbents to acquire or partner with emerging snack innovators.

Regional market analysis highlights distinct growth patterns across key geographies. North America (32.4%) retains the largest absolute value position, anchored by strong brand equity, well-penetrated retail infrastructure, and a culture of persistent snack innovation. Europe (24.6%) follows, characterised by premium positioning, clean-label regulatory expectations, and a rapidly evolving plant-based snacking sub-category. Asia Pacific (29.8%) represents the fastest-growing regional market, where localised flavour development — from wasabi-seasoned snacks in Japan to chilli-lime formats in Southeast Asia — combined with expanding modern retail and food delivery ecosystems, is supporting robust market growth.

Innovation strategies across the market are evolving along two distinct directions. On one hand, global giants like PepsiCo, Mondelez International, and Nestlé are leveraging precision nutrition research, sustainable packaging initiatives, and digital commerce capabilities to strengthen their market position. On the other, a new cohort of specialty and clean-label brands is capturing premium shelf space and consumer mindshare through transparent labeling, ingredient traceability, and brand differentiation. The convergence of these forces is redefining competitive dynamics across all geographic markets.

Savory snacks account for the largest revenue segment (38.2%), underpinned by the global dominance of potato and corn-based products from legacy brands. Confectionery (24.6%) and bakery snacks (14.9%) follow as substantial volume contributors. Meat snacks (8.2%), fruit & nut snacks (6.4%) and popcorn & popped snacks (5.9%) are the highest-growth sub-segments, each benefiting from premiumisation and health-positioning tailwinds.

Competitive intensity is high. PepsiCo (Frito-Lay, Quaker) and Mondelez International hold dominant global positions in savory and confectionery snacks, respectively, while Kellanova (formerly Kellogg's snacks business), Campbell Soup (Pepperidge Farm, Snyder's-Lance), and Intersnack Group are key regional contenders. In the BFY and specialty space, emerging brands such as Kind Snacks, RXBar, SkinnyPop, PopCorners, and Hippeas are aggressively disrupting incumbent share.

Processed Snacks Market Segment Analysis

by Product Type: Savory Snacks (38.2%) includes potato chips, tortilla chips, pretzels, pork rinds, and grain-based extruded snacks. This segment benefits from strong brand recognition and extensive retail distribution worldwide, supported by continuous innovation in bold flavors, premium offerings, and better-for-you (BFY) formulations, including baked, reduced-fat, and air-popped products.

Confectionery Snacks (24.6%), encompassing chocolate, candy, gummies and sugar confectionery, is a high-value and high-impulse segment. Premium product offerings, including single-origin chocolate, reduced-sugar formulations, and plant-based confectionery, are supporting revenue growth despite moderating volume growth in mature markets.

Bakery Snacks (14.9%), including cookies, crackers, cereal bars and biscuits, straddle the boundary between snack and meal replacement. The segment is supported by high-protein formulations, whole-grain reformulations, and the growing popularity of on-the-go breakfast and mid-meal consumption,whole-grain reformulations, and the global expansion of on-the-go breakfast and mid-meal snacking occasions.

Meat Snacks (8.2%), Fruit & Nut Snacks (6.4%), and Popcorn & Popped Snacks (5.9%) are the fastest-growing sub-categories. Meat snacks benefit from high-protein, keto-aligned positioning; fruit & nut snacks from clean-label and natural credentials; and popcorn from both indulgent and BFY dual positioning that appeals to a uniquely broad demographic.

by Distribution Channel: Supermarkets & Hypermarkets (43.6%): Supermarkets and hypermarkets remain the leading distribution channel, offering extensive product assortments, strong promotional capabilities, and high consumer traffic. This channel continues to be the primary battleground for shelf space and new product launches by both legacy and challenger brands.

Convenience Stores (21.3%): A high-velocity impulse channel, particularly important for single-serve formats and new product trial. Growth is being fuelled by urban convenience store proliferation in Asia Pacific, and by the premiumisation of convenience store assortments in North America and Europe.

E-Commerce (17.8%): The fastest-growing distribution channel, enabling D2C brand scaling, subscription commerce, and data-driven personalisation. E-commerce is disproportionately important for premium, BFY, and niche flavour snack brands that have limited presence in traditional retail channels.

Strategic Input

1. Why the Processed Snacks Market Deserves Investor Attention

The processed snacks market represents one of the most resilient and innovation-oriented segments of the global food industry. Unlike discretionary premium food categories, snacking is deeply embedded in daily consumer behaviour across all income quintiles and geographies. This creates both a durable demand baseline and ongoing opportunity for value accretion through premiumisation, functional positioning, and geographic expansion.

The market is expected to exceed USD 1,065.8 billion by 2032 at ~8.7% CAGR, underpinned by structural trends that include urban population growth (particularly in Asia Pacific and Africa), increasing workforce participation and changing lifestyles are supporting demand for convenient meal and snack options and the continued proliferation of digital food commerce enabling brand access at unprecedented scale.

2. Key Growth Drivers and Market Momentum

The global trend toward on-the-go and convenience-first eating is the primary demand catalyst, amplified by post-pandemic shifts in work-from-home and hybrid working patterns that have structurally elevated in-home snacking occasions. Key growth vectors include:

• Better-for-you (BFY) Reformulation — reduced sodium, high-protein, high-fibre, plant-based, and allergen-free formats driving premiumisation and category expansion in health-conscious consumer segments

• Flavour Innovation & Global Fusion — consumers seeking novel taste experiences (Korean BBQ, Japanese miso, Indian masala) accelerating flavour proliferation and limited-edition launch cadence

• Sustainable Snacking — recyclable packaging, carbon-neutral production, upcycled ingredients, and regenerative agriculture sourcing gaining traction among younger consumers

• Digital & D2C Commerce — subscription snack boxes, DTC brand ecosystems, and social commerce (TikTok Shop, Instagram) enabling viral new product discovery and rapid scaling

• Functional Snacking — protein bars, nootropic-infused snacks, adaptogen crackers, and probiotic-enriched formats increasing the convergence between snacks and nutritional products

3. Regional Dynamics: Stability and High Growth

The geographic composition of the processed snacks market offers investors an attractive combination of stable earnings from mature markets and high-growth exposure from emerging economies:

• North America and Europe provide earnings stability via entrenched brand equity, sophisticated retail infrastructure, and premiumisation-led average selling price (ASP) growth.

• Asia Pacific is the structural growth engine, with China and India projected to individually surpass USD 100 billion in snack market size by 2030, driven by expanding middle-class snack adoption and rapid modern trade development.

• South America and MEA represent frontier growth opportunities, particularly in urban convenience-store snacking, flavoured corn snack formats, and the emerging D2C digital snack channel.

4. Innovation and Competitive Intensity

The competitive landscape is evolving rapidly from traditional competition based on scale and market share toward innovation-led differentiation. Key investment areas include:

• Precision Formulation — leveraging food science, AI-assisted flavour development, and consumer sensory data to accelerate product development cycles from concept to shelf

• Sustainable Packaging Innovation — moving from linear to circular packaging models including compostable films, deposit-return systems, and concentrated/refillable snack formats

• Supply Chain Localisation — reducing import dependency and building regional ingredient sourcing networks to mitigate FX volatility and improve freshness profile

• Retail Media & Digital Commerce — deploying first-party data assets for targeted digital activation, loyalty programme integration, and personalized promotions and demand forecasting

5. Where the Real Opportunities Lie

The highest-conviction growth opportunities in the processed snacks market are concentrated in the following areas:

• BFY & functional snack expansion across protein, fibre, and gut-health positioning in North America and Europe

• Premiumisation of savory and confectionery categories in Asia Pacific tier-1 and tier-2 cities

• Meat snacks global rollout beyond North America, where jerky and biltong formats are gaining rapid traction in European and Australian markets

• Popcorn and popped snack category development in Asia Pacific where the format is characterized by relatively low market penetration

• E-commerce and D2C snack brands targeting subscription loyalty, trial-and-discovery mechanics, and personalised snack curation

Investor Takeaway

The processed snacks market combines the stability of a staple consumer category with the strong growth potential of an innovation-intensive, premiumisation-driven sector. The combination of durable structural demand, expanding addressable markets in Asia Pacific and emerging economies, and a relentless product innovation cycle makes the segment attractive across both growth-equity and strategic M&A investment contexts. For investors seeking exposure to consumer staples with above-average organic growth potential and significant digital commerce optionality, the processed snacks market offers attractive long-term opportunities supported by diversified revenue streams

Processed Snacks Market Scope: Inquire before buying

| Report Title | Global Processed Snacks Market Size, Share, Growth, Trends & Forecast 2026–2032 |

| Base Year | 2025 |

| Forecast Period | 2026–2032 |

| Market Size in 2025 | USD 642.8 Billion |

| Projected Market Size (2032) | USD 1,065.8 Billion |

| CAGR (2026–2032) | 8.7% |

| Largest Product Segment | Savory Snacks (38.2% share) |

| Fastest Growing Segment | Fruit & Nut Snacks and Popcorn & Popped Snacks |

| Largest Application Channel | Supermarkets & Hypermarkets (43.6% share) |

| Fastest Growing Channel | E-Commerce (14.6% CAGR) |

| Dominant Region | North America Processed Snacks Market (32.4% share) |

| Fastest Growing Region | Asia Pacific Processed Snacks Market (10.8% CAGR) |

| Major Players | PepsiCo, Mondelez International, Nestlé, Mars, Kellanova, Campbell Soup, Intersnack, Calbee, ITC Limited |

Leading Companies in the Processed Snacks Market

1. PepsiCo, Inc.

2. Mondelez International

3. Nestlé S.A.

4. Mars, Incorporated

5. Kellanova

6. Campbell Soup Company

7. Intersnack Group

8. Calbee Inc.

9. ITC Limited

Premium and Better-for-You Brands

1. Kind LLC

2. Clif Bar & Company

3. General Mills

4. SkinnyPop

5. Hippeas

6. Pipers Crisps

7. Tyson Foods

Specialty and Clean-Label Brands

1. Chomps

2. Outstanding Foods

3. LesserEvil

4. Hu Kitchen

5. Siete Family Foods

6. Real Turmat

Emerging and Direct-to-Consumer Brands

1. Graze

2. NatureBox

3. The Nosh

4. SnackNation

5. Bokksu

6. Amorepacific Foods