Pressure Sensitive Adhesives Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

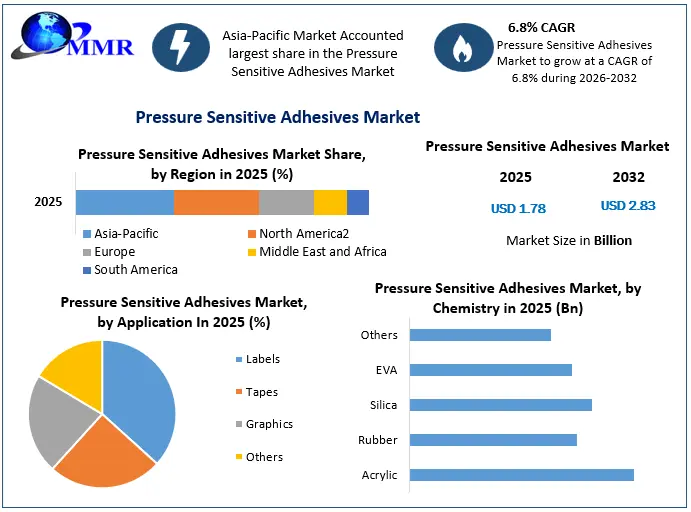

The Pressure Sensitive Adhesives Market size was valued at USD 1.78 Billion in 2025 and the total Pressure Sensitive Adhesives revenue is expected to grow at a CAGR of 6.8% from 2026 to 2032, reaching nearly USD 2.83 Billion.

Pressure Sensitive Adhesives Market Overview:

Pressure-sensitive adhesives (PSAs) are tacky (sticky) in their dry form at room temperature and form a bond through a combination of flow and resistance to flow. While other adhesives (sometimes collectively known as "structural adhesives") form an adhesive bond once they have hardened (via a chemical or physical process), PSAs are tacky (sticky) in their dry form at room temperature and form a bond through a combination of flow and resistance to flow.

To know about the Research Methodology :- Request Free Sample Report

PSAs are manufactured as emulsions, solutions, hot melts, ultraviolets, or as 100% solids. The most prevalent varieties of PSAs are emulsion and solvent-based adhesives; while solvent adhesives provide more strength and moisture resistance, emulsion adhesives are the most popular type of PSA used to manufacture adhesives for labels, packaging, and tapes.

Pressure-sensitive adhesives are used for a broad range of applications because of their ability to create a bond between a wide range of different materials (e.g. paper, wood, metals, plastics, and ceramics) and surface types. Pressure-sensitive labels, packaging, tapes, glue dots, note pads, post-it notes, vehicle trim, protective films, sound/vibration dampening films, masking tapes, price marking labels, promotional materials, and skin contact applications are all common applications.

The packaging industry's high need for pressure-sensitive tapes and labels is expected to increase the Pressure-sensitive adhesives market growth. Pressure-sensitive adhesives (PSAs) are simple to apply and may address adhesion issues in a wide range of substrates and coatings in the food packaging industry.

Packaging requirements are becoming increasingly complicated, especially in the food & beverages industry, due to product proliferation and rising competition. This would open up new opportunities for the industry, as PSAs provide the flexibility needed to satisfy these complicated needs. PSAs are also utilized in other sectors, such as automotive, where they are used in safety and warning labels as well as component identification labels throughout the supply chain.

However, rising raw material prices are a key concern influencing producers and may restrict the market growth. Acrylic polymers, rubber-based polymers, silicone polymers, tackifiers, and additives are the key raw ingredients utilized in the production of PSAs.

Pressure Sensitive Adhesives Market Dynamics:

Increasing Usage of Pressure-Sensitive Adhesives for Flexible Display Applications

The demand for thin and flexible displays is growing rapidly as interest in small and diverse designs grows. The intended purpose and function of flexible screens distinguish them. Pressure-sensitive adhesives (PSA) have rapidly gained popularity in electronics for applications such as shock absorption, thermal and electrical conductivity, electromagnetic shielding, and optical property. Optically clear adhesives (OCA) were utilized as a fundamental material for the display's optical performance. A substrate has needed dielectric constant, gap filling, and anticorrosion in addition to fundamental OCA features like adhesion strength, transmittance, haze, and dependability.

OCA is used to attach layers in a display, such as the cover window, touch panel, polarizers, and the light-emitting layer, to ITO (indium tin oxide) film, which generally requires high transmittance, low haze, and corrosion resistance. When OCA is directly bonded to ITO film, the acid component must be avoided to ensure the ITO film's endurance. Prolonged contact with acid can cause touch issues by interacting with metal, increasing surface resistance. It is also critical for OCA to eliminate air bubbles to reduce errors.

The acrylic PSA is widely used in display, mobile phones, and automotive applications due to its high transparency, weather resistance, heat resistance, and high adhesion strength. Additionally, due to the various acrylic monomers, the acrylic PSA can have a wide range of characteristics. Although the silicone PSA is not as general as the acrylic PSA, it has been utilized in certain applications that demand high dependability because of its great tolerance to high and low temperatures.

Rising demand for Water-based PSAs

Water-based technology is used in pressure-sensitive tapes, labels, adhesive dots, note pads, vehicle trims, films, and peelable, and specific applications in sectors such as packaging, electrical, electronics and telecommunications, medical and healthcare, and automotive. Despite the novel coronavirus outbreak, the market for water-based PSAs has grown because to demand from the medical and packaging industries. During the pandemic, the market for PSAs in packaging has been steadily increasing, as packaging is one of the primary sectors driven by FMCG and food items. People throughout the globe are purchasing just the necessities for survival during quarantines and lockdowns, resulting in increasing demand.

Growing focus on the development of self-adhesive medical products

The focus of self-adhesive medical product development is, on the one hand, customer-oriented criteria such as stickiness, biocompatibility, and permeability for water vapor or air. The user desires highly acceptable, breathable goods that also have excellent skin adhesion and release. On the other hand, medical product producers' economic goals must be considered. A typical element would be an increase in machine speed and a reduction in manufacturing costs, as well as the associated environmental issues of both the product and the process.

The three domains, namely raw materials, technology, and application, serve as the foundation for the development trends of adhesives for medical items. The major factor in raw materials is the use of highly tolerated chemicals with low allergenic potential. Additionally, additional external variables restrict the options. One example is arguments on the use of animal-derived raw materials in the manufacture of medicinal products.

Additionally, the criteria for raw materials in terms of finished product attributes and ease of processing are constantly increasing. Those technologies should be selected during process development if key products such as organic solvents are avoided. Hot-melt systems, water-borne adhesives, and solvent-free acrylic systems are common examples. Additionally, those systems where significant savings in process time and investment may be realized are prioritized.

New applications of self-adhesive acrylic medical items attempt to produce simpler handling or other distinctive selling points. There are medical systems, for example, in which medicine is obtained with the simple application of an island dressing. Acrylic pressure-sensitive adhesive medical grade is commonly used in plaster and pads, transdermal drug delivery systems (TDDS), OP tapes, biomedical electrodes, self-adhesive hydrogels, and surgical drapes. Thus the demand for PSAs offers lucrative potential in medical applications.

Pressure Sensitive Adhesives Market Segment Analysis:

Based on Chemistry, the Acrylic segment held the largest market share and dominated the market in 2025. This segment is further expected to be at a CAGR of 6.3% during the forecast period. Acrylic PSAs are more rigid and long-lasting than rubber PSAs.

Acrylics have outstanding environmental resistance, a fast drying duration, excellent durability against oxidation, temperature, and UV radiation, color stability, exceptional anti-aging qualities, a very good balance of adhesion and cohesiveness with exceptional water resistance, and high peel, tack, and shear. Because of their excellent temperature resistance and strong bonding with polar surfaces such as metal, glass, polyesters, and polycarbonates, they are suited for use in a wide range of applications, which explains their dominance in the pressure-sensitive adhesives industry.

The Rubber segment is expected to grow at a significant rate during the forecast period. Hot melt and solvent-based systems are commonly used in the manufacture of rubber-based goods. The ability of rubber-based goods to give rapid adherence on both rough and smooth surfaces drives their use in tapes. Rubber-based materials, as opposed to acrylic, are widely used on non-polar, low-energy surfaces. Additionally, they provide a more cost-effective option for tape manufacturers.

| Characteristic | Rubber | Acrylic | Silicone |

| Cost | Lowest | Med/High | Very High |

| Tack | Med/High | Med/Low | Low |

| Temp. Resistance | Low | High | Very High |

| Adhesion | Med/High | Moderate/High | Med/Low |

| Shear | Med/High | Moderate/High | Excellent |

| Solvent Resistance | Poor | Good | Excellent |

| UV Resistance | Poor | Excellent | Excellent |

| Plasticizer Resistance | Poor | Moderate/Good | Excellent |

| Low-surface energy materials | Excellent | Poor/Moderate | Poor |

| High-surface energy materials | Excellent | Excellent | Moderate |

Based on End-users, the Packaging industry dominated the market with the highest market share of about 38.4% in 2025 and is expected to maintain its dominance at the end of the forecast period. Adhesives play an essential role in keeping product packaging intact until it reaches the consumer. As the number of new items and product proliferation increases, packaging operations require a dependable adhesive to handle the increasingly complicated packaging demands.

Pressure-sensitive adhesives (PSAs) in particular provide various benefits to the packaging sector, including:

Rapid reworks: Reworking or repackaging induces additional charges. PSAs provide a fast and simple solution to make items compliant and shelf-ready. Pressure-sensitive adhesives are more discreet than standard tape and safer than glue sticks. Pressure-sensitive adhesives, unlike glue sticks, do not require heat to be applied. The lack of heat prevents burns and promotes worker safety. Additionally, PSAs are less invasive on package visuals, giving the necessary adherence without jeopardizing the brand image. Pressure-sensitive adhesives are less apparent packaging options that help to retain and optimize the brand's impression.

Immediate bonding: Using pressure-sensitive adhesives saves time because there is no need to wait for them to cure. They compress the substrate as soon as they are placed, just as adhesion takes place. Instant bonding boosts processing speed and increases output.

Maintaining brand reputation: The appearance of the package greatly influences brand reputation. PSAs create a binding that is easily removed without destroying the packaging or leaving residue behind. Maintaining brand image increases its customer attractiveness.

Meanwhile, the packaging business has been through a transformation in recent years, with the manufacturing and industrial sectors adapting to flexible packaging. Packaging is popular due to features such as lightweight, simple handling, reduced space consumption, longer shelf life, easy transit, damage resistance, and greater printability. Such factors are expected to increase demand for pressure-sensitive adhesives throughout the forecast period.

PSAs are also utilized in the building and construction industries for flooring, vapor barriers, roofing linings, masking, insulation, and interior design. Several techniques are being implemented by businesses to discover and investigate the prospects for specialty tapes in the construction sector. For example, in May , the Pressure Sensitive Tape Council (PSTC) held a symposium in Baltimore regarding the usage of PSAs in the building and construction business.

Pressure-sensitive adhesives provide automobile manufacturers with a low-cost method for increasing the speed and efficiency of assembly processes. Besides that, they increase productivity in difficult manufacturing activities. PSAs help to keep automobiles light, which improves crash performance and provides a great counterbalance. Likewise, eco-friendly and efficient electric automobiles are expected to replace combustion engines and alter vehicle production needs. This is expected to aid the industry during the forecast period.

Pressure Sensitive Adhesives Market Recent Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 13 February 2026 | Sika AG | Sika AG signed a definitive agreement to acquire Akkim, a prominent manufacturer of adhesives and sealants based in Turkey that generated net sales of approximately CHF 220 million in 2025. | The transaction accelerates Sika's global market presence by expanding its distribution channels and production capacity across high-growth pressure-sensitive adhesive and construction markets in Eastern Europe, Central Asia, and North Africa. |

| 16 January 2026 | Henkel AG & Co. KGaA | Henkel AG & Co. KGaA officially finalized the acquisition of Switzerland-based ATP Adhesive Systems Group, a leader specializing in water-based pressure-sensitive adhesive tapes. | The acquisition strengthens Henkel's specialty tapes portfolio, boosting its production scale and capabilities for high-performance, sustainable engineered bonding systems targeting the electronics and medical industries. |

| 12 January 2026 | APPLIED Adhesives | APPLIED Adhesives acquired the United Kingdom-based Interlock Adhesives Limited to incorporate its structural and packaging formulation portfolio. | This acquisition significantly broadens APPLIED Adhesives' geographic footprint outside North America, scaling up its capability to deliver customized industrial pressure-sensitive adhesives (PSAs) for labeling and graphic arts across the UK market. |

| 30 March 2026 | TruArc Partners | TruArc Partners successfully closed the acquisition of Matrix Adhesives Group, a North American formulator and packaging specialist of adhesive solutions, from Goldner Hawn. | The investment provides Matrix Adhesives Group with enhanced capital resources to support operational scale, advanced R&D technology expansion, and broader product diversification in regional industrial and specialty markets. |

Pressure Sensitive Adhesives Market Regional Insights:

The Asia-Pacific market dominated the Pressure Sensitive Adhesives market with the highest market share of about 40% in 2024 and is expected to maintain its dominance at the end of the forecast period. This dominance is attributed to the region's rapidly growing industrial sector, rising foreign investment, and rising demand for tapes and labels. Over 80% of the demand for pressure-sensitive adhesives is supplied by China, India, Japan, and South Korea.

China is a significant supplier of adhesive goods (tapes, labels, etc.), and the majority of its clients are concerned with the product's quality, the vendor's product selection, and lowering adhesive dosage and wastage. As a result, multinational firms now dominate the Chinese market for pressure-sensitive adhesives. The same motive pushes local producers to spend on R&D to get a significant portion of the national market.

The pressure-sensitive adhesives market in India is expected to grow faster, and its applications have increased to include transparent and filmic labels, shrink-wrap labels for fast-moving consumer goods (FMCG) makers, flexible labels, and multicolor wrap-around labels. The pressure-sensitive adhesives market is still in its early stages of development, and it has a greater potential for growth in the future. The vast market size, along with Asia-rapid Pacific's growth, is assisting in the advancement of the pressure-sensitive adhesives market. The North American market is expected to register a significant growth rate during the forecast period. PSAs based on UV/EB technology are expected to increase rapidly in North America, owing to rising corporate and government investment in new technologies, innovation, innovative materials, and sustainability. Additionally, the European market is expected to rise at a significant CAGR during the forecast period. The market is distinguished by the existence of severe REACH rules, which have hampered regional market growth. In terms of product consumption, Germany, France, and the United Kingdom topped the European market in 2024.

The North American market is expected to register a significant growth rate during the forecast period. PSAs based on UV/EB technology are expected to increase rapidly in North America, owing to rising corporate and government investment in new technologies, innovation, innovative materials, and sustainability. Additionally, the European market is expected to rise at a significant CAGR during the forecast period. The market is distinguished by the existence of severe REACH rules, which have hampered regional market growth. In terms of product consumption, Germany, France, and the United Kingdom topped the European market in 2024.

Pressure Sensitive Adhesives Market Ecosystem

Pressure Sensitive Adhesives Market Scope: Inquire before buying

| Pressure Sensitive Adhesives Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 1.78 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.8% | Market Size in 2032: | USD 2.83 Bn. |

| Segments Covered: | by Chemistry | Acrylic Rubber Silica EVA Others |

|

| by Technology | Water-based Solvent-based Hot Melt Radiation |

||

| by Application | Labels Tapes Graphics Others |

||

| by End-User | Packaging Electronics Automotive & Transportation Medical & Healthcare Others |

||

Pressure Sensitive Adhesives Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Pressure Sensitive Adhesives Market, Key Players are:

Pressure-sensitive adhesives (PSAs) are recognized for their tackiness at room temperature, enabling bonding through flow dynamics. Various manufacturing methods, including emulsions and hot melts, highlight the industry's versatility. Emulsion adhesives dominate applications such as labels and packaging due to their efficacy across diverse materials. The growing demand in the packaging sector, particularly within food and beverages, drives market expansion. However, challenges like rising raw material prices, including acrylic and rubber-based polymers, may hinder growth. The analysis emphasizes PSAs' broad applications across automotive and consumer products, indicating a robust market landscape despite potential cost pressures.

1. Henkel AG & Co. KGaA

2. 3M

3. Avery Dennison Corp.

4. H.B. Fuller

5. Arkema Group

6. Sika AG

7. RPM International Inc.

8. LINTEC Corp.

9. Illinois Tool Works Inc.

10.Huntsman Corp.

11.DuPont

12.Wacker Chemie AG

13.Berry Global Inc.

14.Pidilite Industries Ltd.

15.Nan Pao Resins Chemical Co., Ltd.

16.Jowat SE

17.Mactac

18.Ashland Performance Adhesives

19.DELO Industrial Adhesives

20.General Sealants, Inc.

21.The DOW Chemical Company

22.Scapa Group PLC

23.Additional Companies

24.LG Chem

25.SABIC

FAQs:

1. What are the growth drivers for the market?

Ans. Increased construction activity in emerging nations, great features of high-performance coatings, and increasing end-user demand for high-performance coatings are expected to be the major driver for the pressure-sensitive adhesives market.

2. What is the major restraint for the Pressure Sensitive Adhesives market growth?

Ans. The rising raw material prices are expected to be the major restraining factor for the pressure-sensitive adhesives market growth.

3. Which region is expected to lead the global Pressure Sensitive Adhesives market during the forecast period?

Ans. The Asia-Pacific market is expected to lead the global Pressure Sensitive Adhesives market during the forecast period due to the region's rapidly growing industrial sector, rising foreign investment, and rising demand for tapes and labels.

4. What was the Global Pressure Sensitive Adhesives Market size in 2025?

Ans: The Global Pressure Sensitive Adhesives Market size was USD 1.78 Billion in 2025.

5. What segments are covered in the Pressure Sensitive Adhesives Market report?

Ans. The segments covered are Chemistry, Technology, Application, End-User, and Region.