Pre-shave Products Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

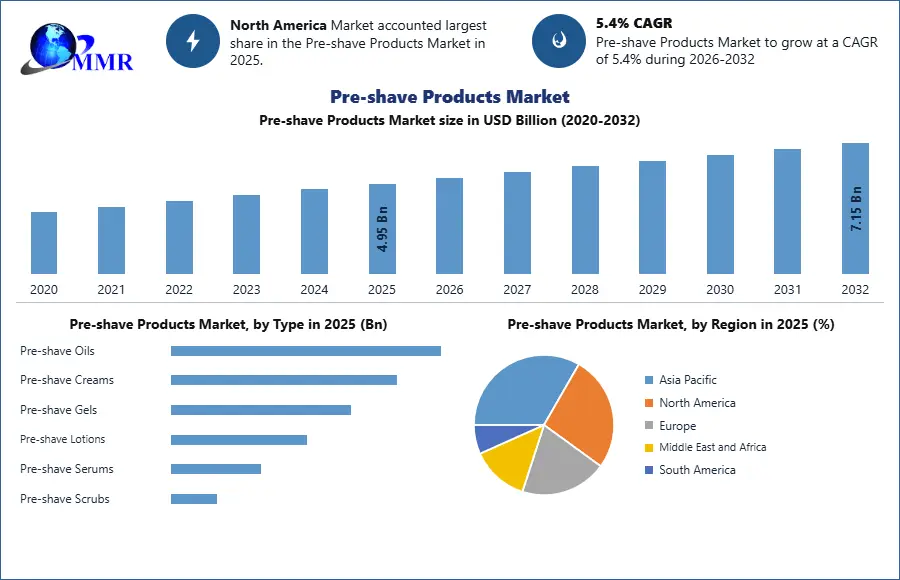

The Pre-shave Products Market was valued at USD 4.95 Billion in 2025 and is estimated to grow at a CAGR of 5.4% over the forecast period, reaching USD 7.16 Billion by 2032.

Global Pre-shave Products Market Overview

Global Pre-shave Products Market Overview

The Pre-shave Products Market comprises products applied before shaving to soften hair, improve razor glide, reduce friction, and create a protective interface between skin and blade. This includes pre-shave oils, creams, gels, lotions, scrubs, and treatment-led formulas designed for facial shaving, beard-line detailing, scalp shaving, and body shaving. In regulatory terms, shaving creams and related grooming products fall within the cosmetics and personal care framework in the United States, while the European cosmetics framework also explicitly covers shaving products such as creams, foams, lotions, gels, and oils. That regulatory inclusion is important because it confirms that pre-shave products are no longer treated merely as ancillary barbering aids; they are now part of the broader cosmetic compliance, safety, labeling, and ingredient-control landscape.

The growth foundation of the Pre-shave Products Market has strengthened because grooming consumption is becoming more skincare-led and less purely utility-driven. FDA notes that people use 6 to 12 cosmetic products daily, and shaving cream and other grooming products are explicitly included in that usage context. In parallel, the broader U.S. men’s grooming products market was estimated at USD 46.54 billion in 2023, indicating that pre-shave products are benefiting from a much larger premium personal-care ecosystem in which men are increasingly willing to spend on skin protection, appearance, and routine optimization. The category is also benefiting from rising awareness of razor burn, redness, dryness, ingrown hairs, and post-shave irritation, all of which make pre-shave skin preparation more commercially relevant than in traditional low-cost wet shaving routines.

Technology development is improving the commercial profile of the market. The innovation pipeline now extends beyond mineral-oil lubrication and basic emollients into silicone-free glide systems, botanical oils, aloe-based soothing blends, microbiome-conscious skin-prep treatments, fragrance-free sensitive-skin formulas, and hybrid products that combine pre-shave cushioning with moisturizer-like skin conditioning. These developments are especially important because buyers now evaluate pre-shave products not only on shaving performance but also on ingredient transparency, irritation control, beard-softening efficiency, and compatibility with premium razors and skincare routines. At the same time, e-commerce is making niche and specialist formulas more discoverable. The U.S. Census Bureau reported that retail e-commerce sales reached USD 1,233.7 billion in 2025, up 5.4% from 2024, with e-commerce accounting for 16.4% of total retail sales, which materially supports online discovery and direct-to-consumer growth for specialized grooming products.

Demand outlook remains favorable because the market now sits at the intersection of men’s grooming products, sensitive skin shaving solutions, premium shaving oils, barber-grade shave preparation, natural grooming products, and online grooming subscriptions. That combination gives the Pre-shave Products Market forecast stronger resilience than a purely commoditized shaving-accessory category, especially in North America, Europe, Japan, South Korea, and higher-income urban markets across Asia Pacific.

Pre-shave Products Market Growth Catalysts

Pre-shave Products Market Segments Analysis

Pre-shave Products Market Segmentation, by Type

TYPE

- Pre-shave Oils

- Pre-shave Creams

- Pre-shave Gels

- Pre-shave Lotions

- Pre-shave Serums

- Pre-shave Scrubs

In 2025, the Pre-shave Oils segment was the largest in the Pre-shave Products Market because it represented the most specialized and premium expression of pre-shave skin preparation. Oils dominated not because they were the cheapest format, but because they delivered the clearest value proposition in beard softening, blade glide, friction reduction, and visible protection against razor burn. They were heavily adopted by premium wet shavers, barbershop users, beard-line grooming consumers, and buyers with sensitive or dry skin who wanted more control than a standard foam or shave cream could provide. The segment also benefited from strong digital storytelling, since oils are easier to differentiate through ingredients such as jojoba, argan, castor, tea tree, sandalwood, or vitamin-rich blends. As the category became more skincare-oriented, oils gained share by aligning with both performance-led and natural-grooming positioning. Their dominance in 2025 therefore reflected a combination of premiumization, consumer education, sensory experience, and the market’s broader shift from commodity shave preparation toward treatment-led grooming.

Pre-shave Products Market Segmentation, by Ingredient Type

- Natural and Botanical Ingredients

- Synthetic and Performance Actives

- Hybrid Formulations

- Fragrance-Free Formulations

- Alcohol-Free Formulations

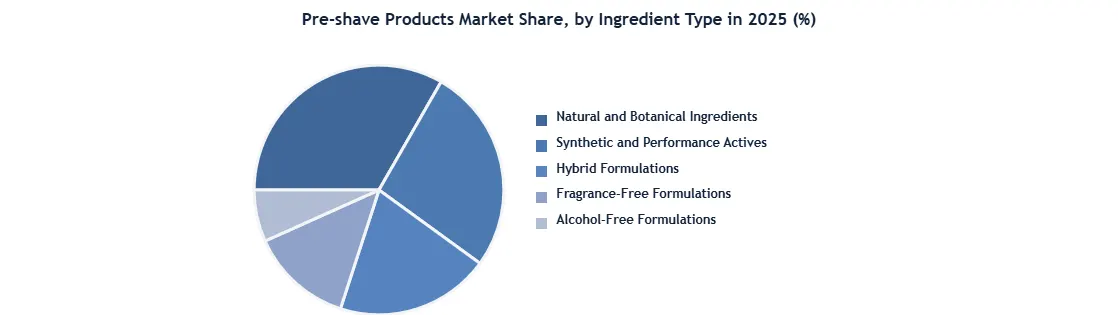

In 2025, the Natural and Botanical Ingredients segment led the Pre-shave Products Market because grooming consumers increasingly linked skin comfort with plant-based oils, soothing extracts, and perceived ingredient gentleness. The broader U.S. men’s grooming market explicitly highlights growing awareness of natural, organic, and herbal products, and that demand translated strongly into pre-shave categories where the consumer benefit is directly tied to skin feel. Natural-ingredient leadership was also reinforced by premium DTC and barber-led brands that positioned botanical formulas as more authentic, skin-friendly, and ritual-oriented than conventional lubricating products. For a market increasingly shaped by sensitive skin, grooming-as-self-care, and premium storytelling, botanical-led formulas held the strongest commercial advantage in 2025.

Pre-shave Products Market Segmentation, by End User

END USER

- Men

- Women

- Unisex

- Professional Barbershops

- Salons

In 2025, Men remained the largest end-user segment in the Pre-shave Products Market because facial shaving frequency, beard styling culture, and premium wet-shaving adoption remained highest in male grooming routines. This dominance was supported by the scale of the men’s grooming market, the willingness of male consumers to experiment with specialized grooming products, and the increasing normalization of skincare-led shave routines. Professional barbering also reinforced male demand, especially for beard detailing, neckline definition, and razor-burn prevention. Although women’s shaving applications are rising, the male segment still dominated in 2025 due to higher category familiarity, higher branded assortment visibility, and deeper integration of pre-shave products into facial grooming rituals.

Pre-shave Products Market Segmentation, by Distribution Channel

DISTRIBUTION CHANNEL

- Online Retail

- Direct-to-Consumer Websites

- Supermarkets and Hypermarkets

- Pharmacies and Drugstores

- Specialty Grooming Stores

- Barbershop and Salon Retail

- Subscription Commerce

In 2025, Online Retail was the leading distribution channel in the Pre-shave Products Market because the category benefits disproportionately from education, comparison, reviews, influencer-led recommendations, and ingredient storytelling. The U.S. Census Bureau’s 2025 e-commerce growth data supports this structural shift, and men’s grooming market analysis also shows online as the faster-growing channel. Pre-shave products often require more explanation than basic razors or foams, which makes digital storefronts more effective for conversion. Consumers could compare oils, creams, and sensitive-skin formulas, read technique guidance, and access a wider assortment than most physical stores could offer. That is why online retail outperformed in 2025: it matched the decision-making behavior of the modern grooming buyer more closely than shelf-based retail.

Pre-shave Products Market Segmentation, by Skin Type

- Sensitive Skin

- Dry Skin

- Normal Skin

- Oily Skin

- Combination Skin

In 2025, the Sensitive Skin segment held the largest share in the Pre-shave Products Market because irritation reduction is one of the category’s clearest purchase triggers. Redness, razor burn, stinging, and post-shave discomfort are repeatedly cited as major user concerns, and these concerns are strongest among consumers who actively seek pre-shave protection rather than relying on a standard shave cream alone. Sensitive-skin formulations therefore benefited from both problem-solution relevance and premium willingness to pay.

Pre-shave Products Market Regional Analysis

In 2025, North America was the leading region in the Pre-shave Products Market because it combined high grooming expenditure, strong premium product adoption, advanced retail infrastructure, and a highly developed digital commerce ecosystem. The United States alone represented a large and fast-growing men’s grooming base, with the broader U.S. men’s grooming products market estimated at USD 46.54 billion in 2023 and expected to expand at 8.3% CAGR through 2030. That scale matters because pre-shave products are a premium subcategory that performs best where consumers already spend meaningfully on grooming and skincare. The region also benefited from policy and regulatory support in the sense that FDA’s MoCRA has pushed the cosmetics category toward stronger safety substantiation and more disciplined product stewardship, which tends to favor established premium operators and higher-quality formulations. From a technology leadership perspective, North America remained a center for DTC grooming brands, influencer-led launches, premium ingredient storytelling, and rapid omnichannel testing. Infrastructure was equally important: the region had deep pharmacy, supermarket, specialty retail, barber, and e-commerce networks, while total U.S. e-commerce sales reached USD 1.23 trillion in 2025. Taken together, industrial scale, consumer spending power, regulatory maturity, innovation capability, and retail infrastructure kept North America in the lead in 2025.

Recent Developments

June 2025: Unilever announced that it would acquire men’s personal care brand Dr. Squatch, describing it as a high-engagement men’s brand with a strong retail and direct-to-consumer model and a product portfolio built around natural, high-performance personal care. While the announcement was broader than pre-shave alone, it is strategically important for the Pre-shave Products Market because it confirms that large consumer groups are actively expanding into premium, digitally native, ingredient-led men’s grooming spaces. Pre-shave products benefit directly from this kind of portfolio move because the category relies on exactly the same commercial levers that made Dr. Squatch attractive: social-first marketing, high customer engagement, natural-performance positioning, and scalable omnichannel distribution. The transaction also signals rising investor confidence in men’s personal care adjacencies where skincare, beard care, shave preparation, and ritualized grooming routines increasingly overlap. In commercial terms, such acquisitions typically accelerate category education, raise innovation intensity, and lift merchandising visibility for premium grooming products across digital and physical channels.

August 2025: Edgewell highlighted the launch of Progista by Schick Japan, describing it as the first premium total grooming care brand for men endorsed by professionals and built around an integrated system covering pre-shave skin protection, razor performance, and after-shave skin care. This was one of the clearest 2025 developments directly tied to the Pre-shave Products Market because it explicitly repositioned pre-shave care as a strategic part of a full grooming architecture rather than an optional accessory. Edgewell also noted that razor burn, stinging, and redness remained leading skin concerns among men in Japan, which is commercially significant because it validates irritation management as a core demand driver for pre-shave products. The launch reinforces three broader market signals at once: first, dermatologist-backed and professional-endorsed shave preparation is gaining traction; second, premium male grooming continues to move closer to skincare; and third, companies increasingly see pre-shave care as a gateway category that can raise attachment rates across razors, shave products, and post-shave treatments.

October 2025: Henkel Beauty Care’s STMNT Grooming Goods announced its expansion into shaving with two new products, including a transparent non-foaming Shaving Gel described as ideal for pre-shave, full shave, and contouring, and designed to create a protective barrier between blade and skin while softening beard stubble for a precise, smooth shave. This development is particularly relevant to the Pre-shave Products Market because it reflects the increasing commercial value of hybrid formulations that function across multiple steps of the shave ritual. Rather than offering a basic mass-market foam, the brand introduced a professional-style gel built for visibility, beard-line precision, and skin protection, which aligns with the premium barber-led direction of the category. The launch also confirms that barbershops and salons are becoming more important innovation filters for shave preparation products. Strategically, this kind of product expansion supports category premiumization by shifting consumer attention from low-cost shave lubrication toward high-performance preparation systems linked to technique, artistry, and skin comfort.

Global Pre-shave Products Market Scope: Inquire before buying

| Pre-shave Products Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 4.95 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.4% | Market Size in 2032: | 7.15 USD Billion |

| Segments Covered: | by Type | Pre-shave Oils Pre-shave Creams Pre-shave Gels Pre-shave Lotions Pre-shave Serums Pre-shave Scrubs |

|

| by Ingredient Type | Natural and Botanical Ingredients Synthetic and Performance Actives Hybrid Formulations Fragrance-Free Formulations Alcohol-Free Formulations |

||

| by Distribution Channel | Online Retail Direct-to-Consumer Websites Supermarkets and Hypermarkets Pharmacies and Drugstores Specialty Grooming Stores Barbershop and Salon Retail Subscription Commerce |

||

| by Skin Type | Sensitive Skin Dry Skin Normal Skin Oily Skin Combination Skin |

||

| by End User | Men Women Unisex |

||

Global Pre-shave Products Market by Region

North America (United States, Canada, Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Poland, Belgium, Netherlands, Rest of Europe)

Asia Pacific (China, South Korea, India, Japan, Australia, Indonesia, Malaysia, Philippines, Thailand, Vietnam, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Rest of South America)

Key Players/Competitors Profiles Covered in the Pre-shave Products Market Report in Strategic Perspective

- Procter & Gamble

- Edgewell Personal Care

- Unilever

- Beiersdorf

- L'Oréal Groupe

- Shiseido

- Kao Corporation

- Colgate-Palmolive

- Church & Dwight

- Reckitt

- Harry’s Inc.

- The Art of Shaving

- Pacific Shaving Company

- Proraso

- Taylor of Old Bond Street

- Geo F. Trumper

- Edwin Jagger

- Captain Fawcett

- Cremo Company

- Jack Black

- Baxter of California

- Bombay Shaving Company

- The Real Shaving Company

- Phoenix Artisan Accoutrements

- Murphy and McNeil