Polyvinyl Butyral Market by Type, Application, End-Use Industry, and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

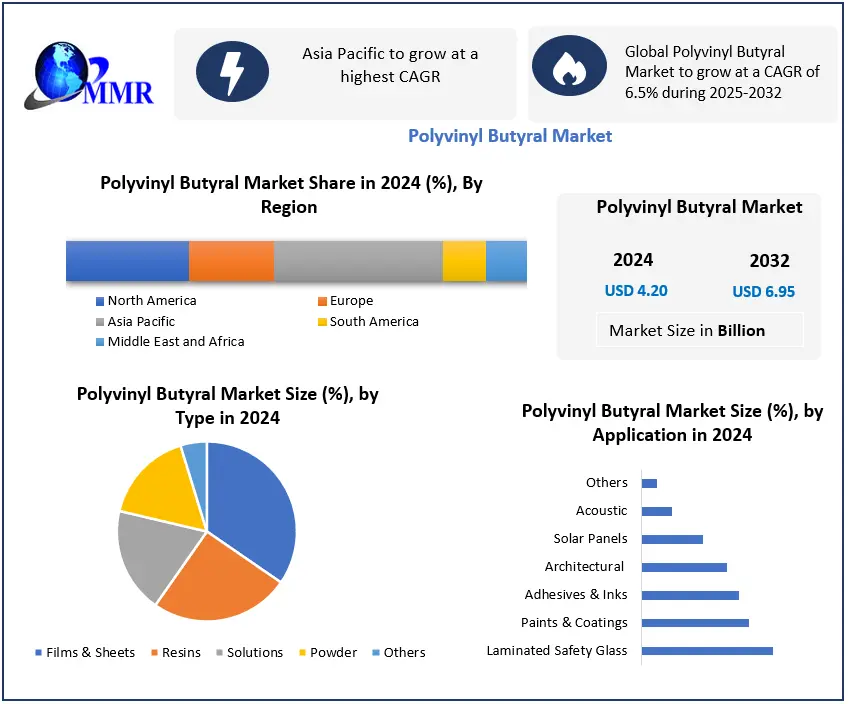

The Polyvinyl Butyral (PVB) Market size was valued at USD 4.20 Billion in 2024 and the total global market revenue is expected to grow at a CAGR of 6.5% from 2025 to 2032, reaching nearly USD 6.95 Billion, driven by the rising demand for laminated safety glass in automotive and construction industries.

Growing Applications and Demand for Laminated Glass, as well as the beneficial features of the resin-based product, are driving the Polyvinyl Butyral market growth. On the other hand, the influence of the COVID-19 pandemic on the growth of the different end-user sectors, as well as supply chain disruptions, hampered the market's growth. Kuraray Co. Ltd, Eastman Chemical Company, Sekisui Chemical Co. Chang Chun Group, and Kingboard (FoGang) Specialty Resins Co. Ltd are among the key competitors in the global Polyvinyl Butyral market. Polyvinyl butyral adhesive films led the market by type, accounting for almost 95% of total revenue in 2021. This trend is expected to continue through 2029, with adhesive films seeing the greatest growth rate of 5.48%.

In terms of end-user sectors, automotive and construction have the largest market shares in 2021, with 54.7% and 38.2%, respectively. The other sector is power generation, which includes polyvinyl butyral uses in PV cells, modules, and panels and was accounted for 4.9% of the market in 2020. This segment is expected to be the fastest-growing consuming industry during the forecast period. The Asia-Pacific region dominated the market analyzed in 2022, followed by Europe and North America. This pattern is expected to continue through 2026. During the projected period, Asia-Pacific is expected to be the fastest expanding region, with a CAGR of 5.7%. China is the largest consumer in 2020, followed by the United States.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Polyvinyl Butyral Market Dynamics

Growing Applications of Laminated Glass to Boost Market Growth

Polyvinyl butyral (PVB) is mostly utilised for laminated glasses due to its strong binding, optical clarity, adherence to numerous surfaces, durability, and flexibility. Laminated glass offers distinctive effects in home décor due to its numerous benefits. Frosted glass, for example, is commonly used in residential doors, particularly kitchen doors. Oily smoke may readily adhere to the surface in the kitchen. This issue may be avoided by using laminated glass instead of frosted glass. Furthermore, huge surface boundaries in the home might represent a safety danger to active children. Laminated glass may be utilised to improve everyone's safety at home.

Because of its powerful anti-shocking and anti-break-in properties, laminated glass is used in most buildings in Europe and America to prevent accidents. Furthermore, StatCan estimates that the gross domestic product at basic prices for the construction industry in Canada in 2019 will be about CAD 141.22 billion, with an increase estimated during the forecast period. Furthermore, China is the world's largest construction market, accounting for 20% of all worldwide construction investment. By 2030, the country as a whole is estimated to spend over USD 13 trillion on construction.

China produced over 11 million square metres of laminated glass in August 2021, a 4.3% increase over the same time the previous year. In 2020, China's yearly manufacturing volume of laminated glass will exceed 114 million square metres. Furthermore, the advent of COVID-19 and its subsequent global spread halted certain development projects in the nation. Some projects are temporarily suspended because to government restrictions aimed at limiting the spread of COVID-19. This may have an influence on the Polyvinyl butyral market in the early years of the forecast period, but it is expected to rise in the later half of the forecast period. Such positive factors are expected to increase applications of laminated glass, which is further expected to increase the polyvinyl butyral market during the forecast period.

Increase in the Demand for PVB thanks to Growing Applications in Various Industries

Polyvinyl butyral has the ability to offer sound insulation, which is a key aspect in determining the quality of modern residential structures. Glass with Polyvinyl butyral interlayer coatings can suppress sound waves and keep an office atmosphere peaceful and comfortable. Its unique UV filtering capability protects human skin, prevents crucial and valuable furniture from fading, and keeps artworks from fading. It also inhibits light transmission and conserves refrigerating energy. Because polyvinyl butyral is used to make PV panels, the rising photovoltaic sector is expected to generate a large market for it. The building sector is a major consumer of polyvinyl butyral. Following COVID-19, the industry is rebounding at a reasonable rate in the Asia-Pacific area.

The Japanese construction industry is expected to expand quickly over the next five years as a result of increased expenditures in public and private infrastructure and commercial projects. Japan is a key region in the realm of skyscrapers and high-rise structures, making it a substantial market for polyvinyl butyral use. The country is home to about 290 high-rise buildings, with Tokyo serving as a key hub for such structures. As a result of the above factors, demand for PVB is expected to increase during the forecast period.

Other Alternatives of PVC and Disadvantages of PVC to Restraint Market Growth

Other alternatives, such as Ethylene Vinyl Acetate (EVA), are expected to act as a brake on the Polyvinyl butyral industry. EVA is now the most used PV cell panel sealant, with PVB as a thermoplastic substance coming in second. The chemical nature of EVA cross-linking allows interior molecules to establish three-dimensional linkages, providing extra protection for any architectural parts subjected to adverse circumstances such as high temperatures, high humidity, and extreme weather. As a result, EVA may also be used to replace PVB in the building sector. Another downside of PVB is its high water intake, which makes it particularly susceptible to hydrolysis. As a result, it cannot be utilised for crystalline Si solar modules based on glass/back sheets. It was utilised in glass-glass modules as well as thin-film solar panels. PVB is more sensitive and vulnerable to issues such as water intrusion in laminated glass corners. The market is also being influenced by a rise in the use of recycled polyvinyl butyral (PVB) due to environmental concerns, as well as the much higher manufacturing costs of purified PVB and virgin PVB.

Between 8 and 9 million automobiles are discarded in Europe each year. This figure approaches 800,000 automobiles each year in Spain, with a 6% yearly rise. As a result, scrap-derived laminated glass accounts for up to 3% of the total material in cars at the end of their useful life, which may be recycled to produce PVB for further usage. This laminated glass results in around 480,000 tonnes of residue in Europe each year, all of which originates from abandoned automobiles. Furthermore, as compared to standard latex, utilising recycled PVB reduces the carbon impact of the precoat by 80%. All regular micro tuft carpet tiles are now made using recycled PVB precoats, considerably lowering the environmental effect. The regular increase in the price of raw materials (polyvinyl alcohol and butyraldehyde), packaging, shipping, and logistics has resulted in an increase in manufacturing costs, which has subsequently influenced the price of finished polyvinyl butyral and related goods.

Polyvinyl Butyral Market Segment Analysis

Based on Type, the Market is segmented into Films & Sheets, Resins, Solutions, Powder, and Others. The Films & Sheets segment dominated the market in 2024 and is expected to hold the largest market share during the forecast period. the PVB market, capturing more than 70% of the total revenue share. This dominance is mainly due to their wide application as an interlayer in laminated safety glass used in automotive windshields, architectural glazing, and high-rise building facades. Growing automotive safety regulations, rapid urbanization, rising demand for acoustic insulation, and UV-resistant glazing in construction are fueling the market growth. Films & Sheets are also preferred because of their superior optical clarity, strong adhesion, durability, and cost-effectiveness compared to other forms. As a result, leading manufacturers are heavily investing in PVB films for automotive and architectural applications, ensuring consistent innovation and supply.

Based on End-Use, the market is segmented into Automotive, Building and Construction, Solar Energy, Electrical & Electronics, and Defence. The Automotive segment dominated the market and is expected to hold the largest market share during the forecast period. The dominance of this segment is attributed to the extensive use of PVB films in laminated safety glass for automotive windshields, side windows, and sunroofs, which enhance passenger safety by preventing shattering during accidents. Stringent vehicle safety regulations across North America, Europe, and Asia-Pacific, coupled with the rising production of electric vehicles, have further accelerated demand for PVB in the automotive industry. Additionally, the growing consumer preference for noise reduction, UV protection, and advanced glazing technologies in modern vehicles continues to strengthen the leadership of the automotive end-use segment in the global PVB market.

The laminated glasses are most likely made of float or coloured glass. The strength of the layers of glass and PVB sheets can be improved. Car production in 2020 was reduced. Light vehicle production had been cut by 6.2% or 5.02 million units in 2021 and by 9.3% or 8.45 million units in 2022, to stand at 75.8 million units and 82.6 million units, respectively.

The forecast for 2023 has been reduced by 1.05 million units, or 1.1%, to 92.0 million units. Production in 2024 and 2025 is expected to be 97.3 million units in 2024, up 3.2% over the prior forecast, and 98.9 million units in 2025, up 2.4%. The major cause of the shortfall is a disruption in front-end wafer manufacture for microcontrollers (MCU), which has exacerbated challenges in the semiconductor industry's already tight supply chain.

Asia-Pacific, the world's largest car production area, saw a 10.2% fall in 2020. The output declined from 49.33 million in 2019 to 44.28 million in 2020. China, which was badly struck by the pandemic in the first three quarters of 2020, recovered fast. The Chinese reduction in production has been limited to only 2%.

Regional Insights

In terms of GDP, China has the largest economy in the Asia-Pacific region. Due to its trade battle with the United States, the country saw the slowest growth, totaling to 6.0% in 2019, compared to prior years. In the first half of 2021, vehicle manufacturing in the country reached 12,569,475 units, a 24% increase over 10,116,915 units in the same time in 2020. The polyvinyl butyral market is expected to benefit from this scenario. Furthermore, the Chinese government is encouraging the use of electric cars, which is favourably affecting the industry.

The People's Republic of China's Ministry of Finance released a notice in April 2020 on measures to enhance financial incentives for new electric cars. It is expected that new EVs acquired between January 1, 2021 and December 31, 2022 would be free from car purchase tax. The Chinese government intends to have 5,000 fuel cell electric vehicles by 2025 and one million by 2030. During the forecast period, the government's promotion of electric, hybrid, and fuel cell electric cars is likely to push the market researched.

The country's demographics are likely to drive continuous expansion in home building. Rising family income levels and a growing number of individuals relocating from rural to urban regions are expected to fuel demand for the country's residential building sector. The public and private sectors' greater emphasis on affordable housing may boost growth in the residential building sector. The abundant advancements in the residential and commercial building sectors, as well as the increasing economy, are driving China's growth. In China, the Hong Kong housing authorities announced a number of initiatives to jump-start the development of low-cost homes. By 2030, officials hope to have built 301,000 public housing units.

After China, the United States is the world's second-largest automaker, producing 10.89 million vehicles in 2019. Despite the automobile industry's constant expansion over the last decade, the sector has been experiencing a steep decrease since the beginning of 2019 owing to a variety of issues, including the trade war between China and the United States, as well as COVID-19. In 2020, the country produced 8.82 million automobiles, a 19% decrease from the 10.89 million vehicles produced in 2019. Automotive sales fell 15.2% to 14.45 million vehicles in 2020, down from 17.03 million vehicles delivered in 2019. However, the automobile sector grew by 17% in the first half of 2021 compared to the same time in 2020. In the first half of 2021, automobile output was 4,732,820 units, up 36% from 3,484,169 vehicles in 2020.

Furthermore, sales of plug-in cars in the United States grew to 328,000 vehicles in 2020, representing a 4% rise over 316,000 vehicles sold in 2019. This is expected to increase demand for polyvinyl butyral in the market. The construction industry in the United States is one of the largest in the world, with a value of USD 1,469.15 billion in 2020, up from USD 1,391.04 billion in 2019.

According to the US Census Bureau, the annual value of residential building in the United States is expected to reach USD 6,38,088 million in 2020, representing a 13% increase from USD 5,53,442 million in 2019. According to the Federal National Mortgage Association (Fannie Mae), residential house construction was estimated to jump 10% across 2020, with 1 million new homes expected to hit the market by the end of 2021. Even though the United States construction sector declined in 2020, the industry is expected to start recovery by 2021, thereby, increasing the demand for polyvinyl butyral during the forecast period.

Polyvinyl Butyral Market Scope: Inquire before buying

| Polyvinyl Butyral Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024 : | USD 4.20 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 6.5% | Market Size in 2032 : | USD 6.95 Bn. |

| Segments Covered: | by Type | Films & Sheets Resins Solutions Powder Others |

|

| by Application | Laminated Safety Glass Paints & Coatings Adhesives & Inks Architectural Solar Panels Acoustic Others |

||

| by End Use | Automotive Building and Construction Solar Energy Electrical & Electronics Defence |

||

Polyvinyl Butyral Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Polyvinyl Butyral Market, Key Players are:

1. Chang Chun Group(Taiwan)

2. Hui Da Chemical (US)

3. DuLite PVB FILM(US)

4. Eastman Chemical Company(US)

5. WMC GLASS(US)

6. Eastman (Solutia)(US)

7. Everlam (Belgium)

8. Huakai Plastic (Chongqing) Co. Ltd(China)

9. Kingboard (FoGang) Specialty Resins Co. Ltd(China)

10.Anhui WanWei Bisheng New Material Co., Ltd.(China)

11.RongXin New Materials(China)

12.Xinfu Pharm(China)

13.Guangda Bingfeng(China)

14.Longcheng High-tech Material (China)

15.Sichuan EM Technology(China)

16.Kuraray Co. Ltd (Japan)

17.Sekisui Chemical Co. Ltd.(Japan)

18.Hubergroup(Germany)

19.Tridev Resin Pvt. Ltd.(India)

20.Genau Manufacturing Company LLP (GMC LLP)(India)

Frequently Asked Questions:

1] What segments are covered in the Global Polyvinyl Butyral Market report?

Ans. The segments covered in the Polyvinyl Butyral Market report are based on Type and End-User.

2] Which region is expected to hold the highest share in the Global Polyvinyl Butyral Market?

Ans. The Asia Pacific region is expected to hold the highest share in the Polyvinyl Butyral Market.

3] What is the market size of the Global Polyvinyl Butyral Market by 2032?

Ans. The market size of the Polyvinyl Butyral Market by 2032 is expected to reach USD 6.95 Bn.

4] What is the forecast period for the Global Polyvinyl Butyral Market?

Ans. The forecast period for the Polyvinyl Butyral Market is 2025-2032.

5] What was the market size of the Global Polyvinyl Butyral Market in 2024?

Ans. The market size of the Polyvinyl Butyral Market in 2024 was valued at USD 4.20 Bn.