Polystyrene Foam Market Size by Foam Type, End-User, Process Type, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

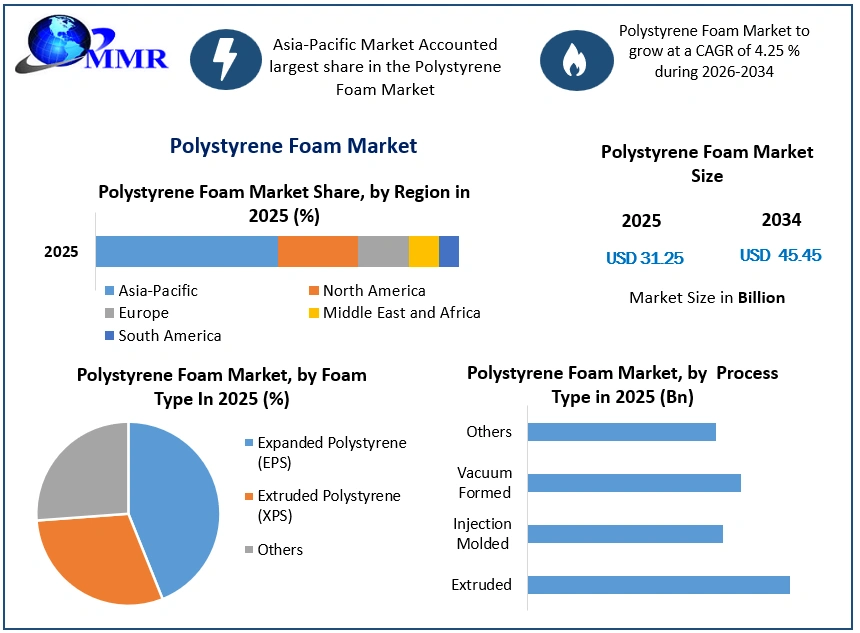

The Polystyrene Foam Market size was valued at USD 31.25 Billion in 2025 and the total Polystyrene Foam revenue is expected to grow at a CAGR of 4.25% from 2026 to 2034, reaching nearly USD 45.45 Billion.

Polystyrene foams (made up of 95-98% air) are excellent thermal insulators and are frequently used as building insulation materials, such as in insulating concrete forms and structural insulated panel construction systems. PS foams have strong damping qualities and are thus commonly utilised in packing. Non-weight-bearing architectural constructions are also made of foam (such as ornamental pillars).

In the medium term, the development of green building, together with rising demand for polystyrene foam in protective packaging applications in developed and emerging countries globally, are some of the key factors bolstering market expansion. However, unpredictability in raw material pricing is a crucial element that is expected to limit the Polystyrene Foam Market growth.

Furthermore, rigorous government regulations governing the usage of polystyrene foam, such as a prohibition on single-use foam products, may impede the growth of the researched industry. Nonetheless, new applications for polystyrene foam are emerging. Emerging Applications in marine floatation and floating decks are expected to generate profitable development opportunities for the global Polystyrene Foam Market.

The Asia-Pacific region is expected to dominate the Polystyrene Foam industry and have the fastest CAGR during the forecast period. This increase is due to an increase in polystyrene foam use in the infrastructure, building, and packaging industries in countries such as China, Japan, and India.

Polystyrene Foam Market Growth Outlook

To know about the Research Methodology :- Request Free Sample Report

Polystyrene Foam Market Trends in the Construction Industry

The usage of pre-fabricated Structural Insulated Panels is a major trend in the building business (SIPS). Many market participants are investing in research and development and providing polystyrene foam for prefabricated buildings. For example, DS Smith provides a variety of EPS blocks in various sizes and densities. Its EPS blocks are extensively used in the construction sector for wall and floor insulation, and basic designs may be hot wire cut to protect corners and edges. When shipping building components to construction sites, using polystyrene foam as part of a pre-fabricated building system can reduce CO2 emissions.

Demand for expanded polystyrene is expected to rise as the number of construction projects in industrialised nations such as the United States increases. Among these projects is the USD 10,000 million expansion and modernization of the JFK Airport in Jamaica, New York. Furthermore, Germany has the continent's greatest building stock and is Europe's largest construction market. Annual investment in the country has been consistent in recent years, as the German government encourages energy-efficient repair and development. Asia-Pacific is a major user and producer of expanded polystyrene, with China accounting for the majority of global capacity. The big population and increasing building activity, particularly in residential and infrastructural projects across China, are leading to rising consumption.

Polystyrene Foam Market Dynamics

Increasing Demand of Expanded Polystyrene (EPS) from the Building and Construction Industry to Drive Polystyrene Foam Market

Expanded polystyrene (EPS) is employed in the building and construction industry due to its qualities such as lightweight, durability, thermal efficiency, shock absorption, moisture resistance, and use. It is a well-known insulation material that is utilised in a variety of applications because to its light yet firm foam that provides strong thermal insulation and great impact resistance.

As most ICF dwellings are now developed and sold by corporations, EPS shape-molders could expect a significant rise in production of Insulating concrete forms (ICFs). As a result, growing demand for ICF houses is expected to drive growth in the market for expanded polystyrene (EPS) materials. For decades, EPS has been the architect's preferred choice for economy, performance, and sustainability in a variety of applications.

The primary function of ornamental moulding is to improve a building's overall appeal by concealing transitions and gaps between surfaces. As seen in many locations in North America and other emerging nations where EPS is implanted with reinforcing mesh before polyurethane or polymer-modified cement coating is applied, EPS has supplanted stone as a material for ornamental moulding. Aside from that, there has been a significant demand in the Polystyrene Foam Market for EPS to be used as a thermal insulator in the building sector.

Rising Demand of Polystyrene Foam from the Packaging Industry to Drive Polystyrene Foam Market

Packaging foam is often used as a cushioning material for boxes, and it is noted for its versatility and ability to be tailored. Foams are utilised in a wide range of packaging applications where maximum protection and durability are required. In the building and food packaging sectors, polystyrene foam is primarily utilised as thermal insulation. In recent years, there has been a huge growth in demand for polystyrene foam. Online purchasing for items is gaining in popularity. For fragile objects, foam wrap has been utilised as an alternative to bubble wrap. Foam wrap is popular since it is thin, light, and easy to work with.

Regions, like North America, Asia-Pacific, and the Middle East, have seen a huge demand for cold-chain transport boxes, transport containers, and fastfood packaging. Furthermore, with the introduction of numerous meal delivery applications, the food delivery service has been steadily expanding over the years. Polystyrene foam or expanded polystyrene foams are commonly used as food packaging because they can keep food at a comfortable temperature and keep it fresh. With the e-commerce market rapidly expanding and individuals increasingly adopting and preferring online shopping for anything from FMCG items to medications, gadgets, and food, etc. Thus, the rise of e-commerce, the food packaging industry, and online commerce has resulted in the exponential growth of the packaging sector, with increased awareness and adoption of green packaging expected to have a potentially beneficial influence on the polystyrene foam market in the future years.

Growing Preference for Molded Pulp as a Green Alternative to Restraint Polystyrene Foam Market

The increased desire for eco-friendly products, along with the potential volatility of rising oil costs, has resulted in an increase in the usage of moulded fibre packaging. Polystyrene foam, sometimes known as EPS, is a kind of foam. Polystyrene foam, which is created from petroleum-based polystyrene and a blowing agent for fuel such as pentane or carbon dioxide, is not only hazardous to human health but also to the environment. However, because to its unique composition, EPS cannot always be easily recycled and, if not appropriately processed, might take up space in landfills. EPS, or expanded polystyrene packing, has long been a popular alternative for safeguarding goods in transit.

Consumers are progressively preferring cleaner, more natural packaging with an aesthetically beautiful alternative. Molded fibre, also known as moulded pulp, is a 100% recycled and recyclable packaging alternative to EPS. Molded pulp packaging solutions are a clean, easy, and ecologically responsible packaging option. The increased focus of sustainability has also contributed to the popularity of pulp packaging in recent years. As the globe starts to urbanise, the need for packaging is expected to expand tremendously, necessitating the development of an effective recycling system. The growth of e-commerce will create a demand for consistent package sizes. Customers will place a higher priority on lifestyle trends such as comfort, wellness, and environmental awareness. In the foreseeable future, the growing green alternate replacements markets are likely to reduce demand for EPS foams.

Polystyrene Foam Market Segment Analysis

Polystyrene Foam Industry Based on Foam Type, EPS resin segment accounts for the largest share in the Polystyrene Foam market. EPS is a lightweight thermoplastic material with unique capabilities due to its structure, which aids in the protection of the product. Because it is lightweight yet stiff foam with outstanding thermal insulation and great impact resistance, EPS is a suitable material for various purposes. However, crude oil price volatility and the availability of high-performance replacements are limiting market growth. During the forecast period, the simple recyclability of polystyrene products is likely to provide chances for the growth of the EPS market.

Polystyrene Foam Industry Based on End-User, Building and construction are expected to have the highest volume growth in the Polystyrene Foam market during the forecast period. APAC is expected to be the largest and fastest-growing market in the Building & Construction end-use industry. Because of its closed-air low-thermal conductivity, lightweight (easy of handling), mechanical resistance (insulation in the wall structure and roofing & flooring), low water absorption (to avoid humidity), and sound resistance, EPS is widely employed in the building sector (in office and rooms). It has evolved into a strong design feature and an excellent alternative for green architecture. EPS provides substantial environmental benefits by increasing energy efficiency, improving indoor environmental quality, and increasing the longevity of buildings and packaged items.

Polystyrene Foam Market Regional Insights

The Asia-Pacific region dominated the global polystyrene foam market in 2025, accounting for a sizable revenue share, and is likely to retain its dominance during the forecast period. Growing demand for polystyrene foam in packaging, building and construction, automotive, and electronics appliance uses throughout Asian nations is the key reason driving growth in the Asia Pacific target industry. Aside from architecture and construction, polystyrene foam is used in the food and industrial packaging sectors to protect consumer items and provide safety during transit and handling.

Because of its shock-absorbing properties, it is commonly used in the packaging of fragile electronic components, medical equipment, electrical consumer goods, horticultural products, and consumables like as fruit, vegetables, and seafood. Additionally, the substance is utilised in a variety of automotive applications, including car components, trims, knobs, instrument panels, sound dampening foam, and energy absorbing door panels. It is commonly used in the production of child safety seats. Rapidly developing construction, packaging, and automotive sectors in India, China, and Japan are driving demand for polystyrene foam, which will boost polystyrene foam market development.

China has one of the world's fastest growing economies. In 2025, the country accounted for a sizable portion of global demand for EPS. The rising number of infrastructure development projects, as well as the growing packaging sector, are likely to drive polystyrene foam indusrty growth over the forecast period. Government programmes such as the 13th Five-Year Plan for Building Energy Efficiency and Green Building Development and the State Council Green Building Action Plan are promoting green building development in China, which may contribute to the country's EPS market growth.

Because of the region's economic growth, the South American building and construction industry is expected to grow significantly over the forecast period which is estimated to drive the growth of polystyrene foam market. The region's residential, commercial building, and infrastructure sectors are likely to recover, boosting demand for polystyrene foam in the construction industry.

Significant new expenditures in public works and housing by the South American government, supported by construction programmes to encourage green building construction, are likely to fuel infrastructure growth in South America, consequently boosting polystyrene foam demand during the forecast period. In 2025, Brazil dominated the South American polystyrene foam market, and this trend is expected to continue during the forecast period. The recovery of the economy, together with rising demand for green building development, is expected to promote the growth of the construction sector, which is likely to increase demand for polystyrene foam in the country.

Polystyrene Foam Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 27 July 2026 | Supreme Petrochem | The company board approved a ₹325 crore capital investment to build a new 80,000 TPA polystyrene line at its Amdoshi plant. | This strategic expansion scales total nameplate capacity to 380,000 TPA to capture rising domestic packaging and insulation demand. |

| 23 June 2026 | INEOS Styrolution | The corporation announced the permanent closure of its 400,000 metric tons per year polystyrene plant in Channahon, Illinois, slated for completion in Q4 2026. | This major regional restructuring addresses oversupply and weak profit margins, tightening the North American polystyrene foam supply framework. |

| 18 June 2026 | Sulzer | Commercialized industrial-scale deliveries of styrene monomer produced via the EcoStyrene pyrolysis line. | Proves that recycled polystyrene streams can successfully meet food-contact purity thresholds to comply with strict circular economy regulations. |

| 17 January 2025 | Styrenix Performance Materials | Successfully completed the acquisition of INEOS Styrolution Thailand Co. Ltd. alongside brownfield debottlenecking projects. | Expanded regional manufacturing footprint and boosted production output to meet growing styrenics and polymer foam consumption across Asia. |

Polystyrene Foam Market Scope: Inquire before buying

| Global Polystyrene Foam Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 31.25 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.25% | Market Size in 2034: | USD 45.45 Bn. |

| Segments Covered: | by Foam Type | Expanded Polystyrene (EPS) Extruded Polystyrene (XPS) Others |

|

| by End-User | Building & Construction Packaging Construction & Industrial Insulation Others |

||

| by Process Type | Extruded Injection Molded Vacuum Formed Others |

||

Polystyrene Foam Market, Key Players are:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

1. DowDuPont Inc. (US)

2. Drew Foam (US)

3. Flint Hills Resources (US)

4. AFP-sealed air (US)

5. Alpek (Mexico)

6. Carpenter Co. (US)

7. Dart Container Corporation (US)

8. Nova Chemicals Corp (Canada)

9. Jiangsu Leasty Chemicals Co., Ltd. (China)

10.Wuxi Xingda New Foam Plastics Materials Co., Ltd. (China)

11.Taita Chemical Co., Ltd. (Taiwan)

12.Kaneka Corporation (Japan)

13.JSP Corporation (Japan)

14.BASF SE (Germany)

15.Xella International (Germany)

16.Synthos S.A (Poland)

17.Sunpor Kunststoff GmbH (Austria)

18.SUNPOR Kunststoff GmbH (Austria)

19.Versalis S.p.A (Italy)

20.ChovA (Spain)

21.Knauf Insulation (Belgium)

22.SABIC (Saudi Arabia)

23.Arkema S.A. (France)

24.Kingspan Group (Ireland)

25.O. N. Sunde AS (Norway)

26.Ravago Group (Belgium)

Frequently Asked Questions:

1] What was the Polystyrene Foam Market size in 2025?

Ans: The Polystyrene Foam Market size was USD 31.25 Billion in 2025.

2] What are the major players currently dominating the global Polystyrene Foam market?

Ans. DuPont (U.S.), The Dow Company (US), Loyal Group (China), Jiangsu Leasty Chemicals Co., Ltd. (China), Wuxi Xingda New Foam Plastics Materials Co., Ltd. (China), BASF SE (Germany), Synthos S.A (Poland), Total SE (France) and SABIC are among the major players currently dominating the global Polystyrene Foam market.

3] Which Polystyrene Foam market segment has the potential to register the highest market share during the forecast period?

Ans. The Building & Construction end-user segment has the potential to generate highest revenue share of the Polystyrene Foam market, in terms of volume and value, during the forecast period.

4] Which is the dominating region in the global Polystyrene Foam market?

Ans. Asia Pacific region is the dominating region in the global Polystyrene Foam market. Countries like China, India, Taiwan, Japan, Malaysia, Thailand, South Korea are emerging economies with fastest-growing market share of the region.

5] What is the major factor driving the growth of Polystyrene Foam market in the Asia Pacific region?

Ans. The easy availability of raw materials and high demand from end-use industries are factors driving the growth of Polystyrene Foam market in Asia Pacific region.