Plastic Jar Packaging Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2029

Overview

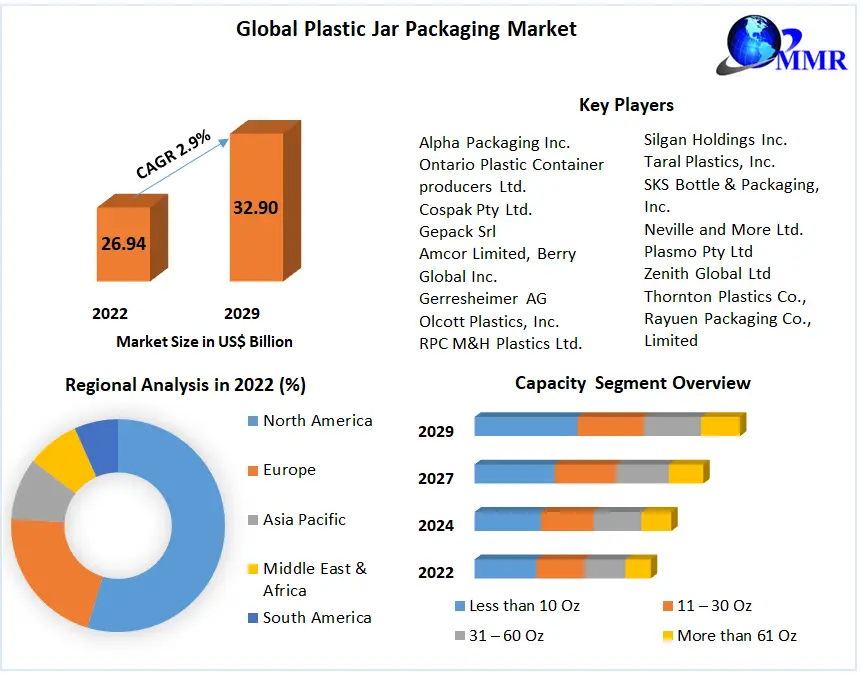

Plastic Jar Packaging Market is expected to reach US$ 32.90 Bn. by 2029 at a CAGR of 2.9% during the forecast period 2023-2029.

The report includes the analysis of impact of COVID-19 lock-down on the revenue of market leaders, followers, and disrupters. Since lock down was implemented differently in different regions and countries, impact of same is also different by regions and segments. The report has covered the current short term and long term impact on the market, same will help decision makers to prepare the outline for short term and long term strategies for companies by region.

Plastic Jar Packaging Market Snapshot

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

The demand for effective and budget-friendly packaging formats across many industries, particularly in the food and beverages sector, is expected to further fuel the plastic jar packaging market during the forecast period. Rapid urbanization and improving living standards of people will also growth the demand for plastic jar packaging in the upcoming years. However, the rising raw material prices of plastic jar packaging may hamper the plastic jar packaging market development on a global scale.

Plastic Jar Packaging Market Segment Analysis

The report covers a comprehensive overview, market shares, and growth opportunities of plastic jar packaging market by type, capacity, end use, key manufacturers and key regions and countries.

Food and beverages segment is dominating the plastic jar packaging market and valued nearby US$ xx Bn in 2022. Higher demand for flexible and functional packaging, largely for packaged food, frozen foods and beverages, is expected to positively impact segment growth in the near future.

In 2020, the APAC was the largest plastic jar packaging market owing to the rising use of plastic jar packaging in food and beverages, personal care and cosmetics, homecare, pharmaceuticals, and chemical industries. Additionally, the region is expected to be the fastest-growing market for plastic jar packaging in the years ahead, because of growing urbanization and industrialization in the region. China, India, Thailand, Indonesia, and South Korea are witnessing a steady growth in the use of plastic jar packaging across many end-user industries.

The report covers major players operating in the global market for plastic jar packaging like Alpha Packaging Inc., Cospak Pty Ltd., Gepack Srl, Olcott Plastics, Inc. and others. Alpha Packaging Inc manufactures high-quality bottles and jars prepared from polyethylene terephthalate (PET), high-density polyethylene (HDPE), polypropylene (PP) & polylactic acid (PLA) for the nutritional, personal care, pharmaceutical, consumer chemical and food and beverage markets.

Industry key players have been involved in mergers and acquisitions (M&A), and vertical integration across the value chain in order to strengthen their product portfolios and distribution network.

The objective of the report is to present a comprehensive assessment of the market and contains thoughtful insights, facts, historical data, industry-validated market data and projections with a suitable set of assumptions and methodology.

The report also helps in understanding Global Market dynamics, structure by identifying and analyzing the market segments and project the global market size. Further, the report also focuses on the competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence. The report also provides PEST analysis, PORTER’s analysis, and SWOT analysis to address the question of shareholders to prioritizing the efforts and investment in the near future to the emerging segment in Global Market.

Plastic Jar Packaging Market Scope: Inquire before buying

| Global Plastic Jar Packaging Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 26.94 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 2.9% | Market Size in 2029: | US $ 32.90 Bn. |

| Segments Covered: | by Material Type | Polyethylene Terephthalate (PET) Polyethylene (PE) Low-Density Polyethylene (LDPE) High-Density Polyethylene (HDPE) Polyvinyl Chloride (PVC) Polypropylene (PP) Polystyrene (PS) Others |

|

| by Capacity | Less than 10 Oz 11 – 30 Oz 31 – 60 Oz More than 61 Oz |

||

| by End Use | Food and Beverages Personal Care & Cosmetics Homecare Pharmaceuticals Chemicals Others |

||

Global Plastic Jar Packaging Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key players operating in the Global Plastic Jar Packaging Market

1. Alpha Packaging Inc.

2. Ontario Plastic Container producers Ltd.

3. Cospak Pty Ltd.

4. Gepack Srl

5. Amcor Limited, Berry Global Inc.

6. Gerresheimer AG

7. Olcott Plastics, Inc.

8. RPC M&H Plastics Ltd.

9. All American Containers, Inc.

10. Tim Plastics, Inc.

11. Pretium Packaging, LLC

12. Integrity Cosmetic Container Industrial Co., Ltd.

13. Silgan Holdings Inc.

14. Taral Plastics, Inc.

15. SKS Bottle & Packaging, Inc.

16. Neville and More Ltd.

17. Plasmo Pty Ltd

18. Zenith Global Ltd

19. Thornton Plastics Co.,

20. Rayuen Packaging Co., Limited

21. Berry Global Inc.

22. Maynard & Harris Plastics

23. Veritiv Corporation

24. Hangzhou Rayuen Packaging Co.,Limited

Frequently Asked Questions:

1. Which region has the largest share in Global Market?

Ans: Asia Pacific region held the highest share in 2022.

2. What is the growth rate of Global Plastic Jar Packaging Market?

Ans: The Global Market is growing at a CAGR of 2.9% during forecasting period 2023-2029.

3. What is scope of the Global Plastic Jar Packaging Market report?

Ans: Global Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Plastic Jar Packaging Market?

Ans: The important key players in the Global Market are – Alpha Packaging Inc., Ontario Plastic Container producers Ltd., Cospak Pty Ltd., Gepack Srl, Amcor Limited, Berry Global Inc., Gerresheimer AG, Olcott Plastics, Inc., RPC M&H Plastics Ltd., All American Containers, Inc., Tim Plastics, Inc., Pretium Packaging, LLC, Integrity Cosmetic Container Industrial Co., Ltd., Silgan Holdings Inc., Taral Plastics, Inc., SKS Bottle & Packaging, Inc., Neville and More Ltd., Plasmo Pty Ltd, Zenith Global Ltd, Thornton Plastics Co.,, Rayuen Packaging Co., Limited, Berry Global Inc., Maynard & Harris Plastics, Veritiv Corporation, Hangzhou Rayuen Packaging Co.,Limited.

5. What is the study period of this Market?

Ans: The Global Market is studied from 2022 to 2029.