Physical Vapor Deposition (PVD) Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

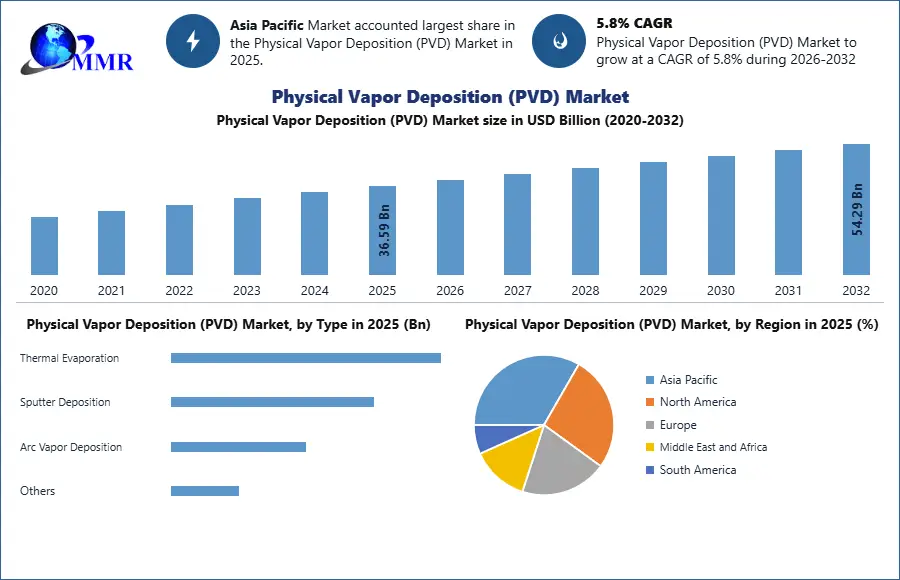

The Physical Vapor Deposition (PVD) Market size was valued at USD 36.59 Billion in 2025 and the total Physical Vapor Deposition revenue is expected to grow at a CAGR of 5.8% from 2026 to 2032, reaching nearly USD 54.29 Billion.

Physical Vapor Deposition (PVD) Market Overview

Physical Vapor Deposition (PVD) is a thin film deposition technique used in materials science and engineering to deposit thin films of various materials onto a substrate. It involves the physical vaporization of a material (usually in solid form) and its subsequent condensation onto a substrate in a vacuum environment. This process is typically carried out in specialized equipment known as PVD coating systems. In a typical PVD process, the material to be deposited is heated to a high temperature in a vacuum chamber, causing it to undergo physical vaporization or sublimation. The resulting vapor then condenses onto the surface of the substrate, forming a thin film. The substrate is held at a different temperature during deposition to control the properties of the deposited film.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The Physical Vapor Deposition (PVD) market has been experiencing steady growth driven by increasing demand across various industries such as electronics, automotive, aerospace, medical devices, and packaging. PVD is extensively used in the electronics industry for applications such as semiconductor manufacturing, data storage devices, and display technologies. Continuous innovations and technological advancements in PVD processes, equipment, and materials are driving market growth. Advancements such as magnetron sputtering, ion plating, and arc evaporation are enhancing the efficiency and capabilities of PVD systems. The Physical Vapor Deposition (PVD) Marketis witnessing significant growth in regions with strong manufacturing bases such as Asia-Pacific, particularly China, Japan, South Korea, and Taiwan. Emerging trends such as the integration of PVD with other deposition techniques and the development of novel coating materials are expected to further fuel Physical Vapor Deposition (PVD) Market growth.

Physical Vapor Deposition (PVD) Market Dynamics

Continuous innovation in PVD processes to boost Physical Vapor Deposition (PVD) Market growth

Continuous innovation in PVD processes, equipment, and materials plays a pivotal role in enhancing the efficiency, performance, and versatility of PVD coatings. Advancements such as magnetron sputtering, ion plating, and arc evaporation have revolutionized the capabilities of PVD systems, enabling the deposition of thin films with exceptional properties tailored to specific applications. The electronics industry stands as a major catalyst for the growth of the Physical Vapor Deposition (PVD) market. PVD coatings find extensive application in semiconductor manufacturing, where they are utilized for deposition on silicon wafers, photomasks, and other critical components. The proliferation of consumer electronics, including smartphones, tablets, and wearable devices, has driven the demand for PVD-coated components for improved performance, durability, and aesthetics.

In the automotive sector, the demand for PVD coatings is on the rise owing to their ability to enhance the durability and corrosion resistance of automotive components. PVD-coated parts, such as engine components, decorative trims, and wheels, offer superior performance and longevity, contributing to the overall quality and value proposition of automobiles. The automotive industry's shift towards lightweight materials and electric vehicles further accentuates the importance of PVD coatings for achieving optimal performance and efficiency. Medical devices represent another significant application area driving the growth of the Physical Vapor Deposition (PVD) Market. PVD coatings play a critical role in medical implants, instruments, and equipment by improving biocompatibility, wear resistance, and antimicrobial properties. As the global healthcare sector continues to expand, fueled by aging populations and advancements in medical technology, the demand for PVD-coated medical devices is expected to soar, driving Physical Vapor Deposition (PVD) Market growth.

Aerospace and defense industries rely on PVD coatings to enhance the performance and durability of critical components subjected to extreme conditions. PVD-coated aerospace components, such as turbine blades, bearings, and aircraft structural parts, benefit from increased surface hardness, reduced friction, and improved thermal protection. With escalating demands for fuel efficiency, safety, and reliability in the aerospace sector, the adoption of PVD coatings is projected to escalate in the coming years.

The complexity and cost associated with implementing PVD processes to limit Physical Vapor Deposition (PVD) Market growth

PVD equipment and facilities require significant capital investment, making it challenging for small and medium-sized enterprises (SMEs) to enter the market or upgrade their existing infrastructure. Moreover, the operation and maintenance of PVD systems entail substantial expenses, including energy consumption, consumables, and skilled labor, which pose financial barriers for businesses. Technological limitations represent another significant restraint in the Physical Vapor Deposition (PVD) Market. While PVD processes offer exceptional control over thin film deposition and enable the fabrication of coatings with tailored properties, certain limitations exist regarding the deposition of certain materials or complex structures. For instance, deposition of certain materials require high temperatures or specialized equipment, limiting the feasibility and scalability of PVD for specific applications.

Regulatory challenges and compliance requirements pose additional restraints on the Physical Vapor Deposition (PVD) Market. Environmental regulations, health and safety standards, and product certifications impose stringent requirements on PVD processes and coatings. Compliance with regulations such as REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) and RoHS (Restriction of Hazardous Substances) necessitates the use of environmentally friendly materials and processes, which increase operational costs and complexity for PVD manufacturers. The limited scalability and throughput of PVD processes compared to alternative thin film deposition techniques such as chemical vapor deposition (CVD). While PVD offers superior control over film properties and substrate compatibility, its batch processing nature and relatively slow deposition rates limit its suitability for high-volume production or applications requiring rapid throughput.

Physical Vapor Deposition (PVD) Market Segment Analysis

By Type Segment Analysis

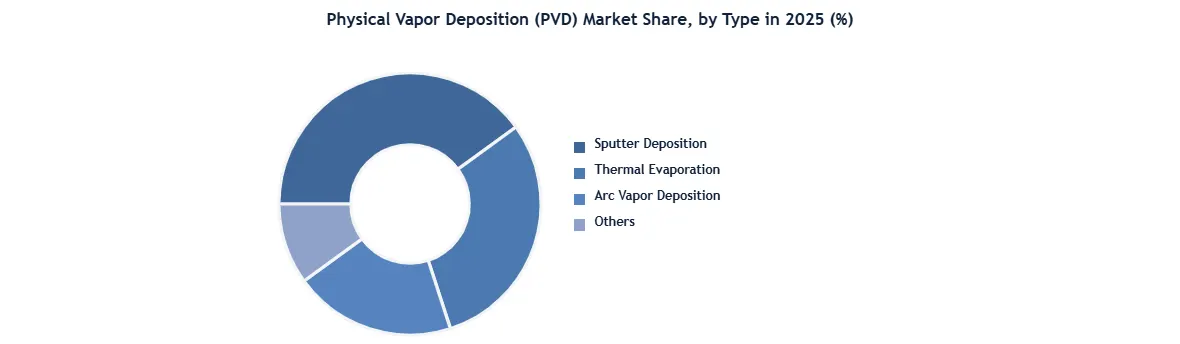

Among the type segments, Sputter Deposition dominated the global Physical Vapor Deposition (PVD) Market in 2025 due to its broad adoption in semiconductor fabrication, microelectronics, optical coatings, and solar applications. Sputter deposition is preferred for producing highly uniform thin films with excellent adhesion and precision, which is essential for advanced chipsets and display panels. The rapid expansion of semiconductor manufacturing in China, Taiwan, and South Korea significantly supported segment leadership. It is also increasingly used in automotive sensors, medical devices, and high-performance industrial coatings. Thermal evaporation maintained steady demand in cost-sensitive applications, while arc vapor deposition gained traction in specialized industrial surface treatments. The others segment includes advanced hybrid deposition methods used in research and niche manufacturing. Sputter deposition remained dominant due to its scalability, process control, and compatibility with next-generation electronics production.

By Category Segment Analysis

By category, PVD Equipment held the largest market share in 2025, supported by rising capital investments in semiconductor fabs, coating facilities, and industrial manufacturing plants. Demand for vacuum chambers, deposition systems, sputtering units, and coating tools increased significantly as industries upgraded production lines. Major manufacturers in the United States, Japan, and Germany expanded equipment development for precision coating processes. The equipment segment benefited from technological advancements in automated deposition systems and high-throughput manufacturing. PVD Services showed strong growth due to outsourcing of coating operations in automotive and aerospace sectors. PVD Materials, including target materials and coating compounds, also expanded with increasing demand for specialty thin films. However, equipment remained dominant because of high installation costs, long-term industrial use, and strong demand from electronics, healthcare, and energy industries.

Physical Vapor Deposition (PVD) Market Regional Insight

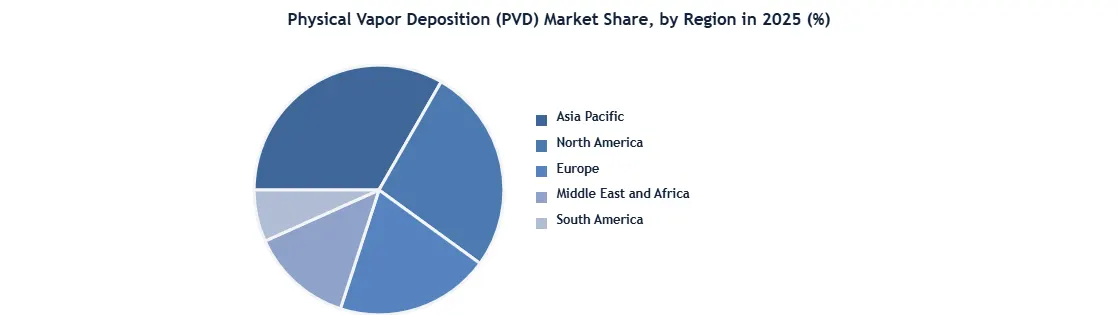

Robust manufacturing sector to boost Asia Pacific Physical Vapor Deposition (PVD) Market growth

Growing investments in research and development activities are driving advancements in PVD technology and expanding the application scope of PVD coatings in the Asia Pacific region. Collaborative efforts The Asia Pacific Physical Vapor Deposition (PVD) Market is the region's robust manufacturing sector, particularly in countries such as China, Japan, South Korea, and Taiwan. The rapid industrialization and economic growth in these nations have fueled the demand for advanced manufacturing technologies, including PVD processes, for improving product performance, quality, and competitiveness. The electronics industry, in particular, has been a major catalyst for the growth of the Physical Vapor Deposition (PVD) Market in Asia Pacific, with the production of semiconductors, displays, and electronic components driving the demand for PVD-coated materials and equipment. Technological advancements play a pivotal role in driving the Asia Pacific PVD market forward. The region is home to leading Physical Vapor Deposition (PVD) manufacturers and research institutions at the forefront of PVD technology development, driving innovations in deposition processes, equipment design, and coating materials. Advanced PVD techniques such as magnetron sputtering, ion beam deposition, and plasma-enhanced PVD are increasingly adopted in the region to meet the evolving requirements of industries such as electronics, automotive, aerospace, and healthcare.

Government policies and initiatives aimed at promoting innovation, industrial development, and technological advancement are further bolstering the growth of the Asia Pacific PVD market. Various countries in the region offer incentives, subsidies, and tax breaks to encourage investment in research and development, manufacturing infrastructure, and high-tech industries, fostering a conducive environment for PVD technology adoption and expansion. Growing investments in research and development activities are driving advancements in PVD technology and expanding the application scope of PVD coatings in the Asia Pacific region. Collaborative efforts between academia, industry, and government institutions are facilitating knowledge transfer, technology transfer, and skill development, driving innovation and competitiveness in the Physical Vapor Deposition (PVD) Marketcan. Research focus areas include the development of novel coating materials, process optimization, and sustainability initiatives aimed at reducing environmental impact and improving resource efficiency.

Physical Vapor Deposition (PVD) Market Scope: Inquire before buying

| Physical Vapor Deposition (PVD) Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 36.59 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.8% | Market Size in 2032: | 54.29 USD Billion |

| Segments Covered: | by Type | Thermal Evaporation Sputter Deposition Arc Vapor Deposition Others |

|

| by Category | PVD Equipment PVD Services PVD Materials |

||

| by Application | Microelectronics Data Storage Solar Products Medical Equipment Cutting Tools Architectural Glasses Others |

||

Physical Vapor Deposition (PVD) Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Physical Vapor Deposition (PVD) Market, Key Players

PVD Equipment Manufacturers & Vacuum Technology Providers

These companies develop PVD deposition systems, vacuum chambers, sputtering equipment, evaporation systems, and advanced thin-film processing technologies.

1. Canon Inc. – Japan

2. ULVAC, Inc. – Japan

3. Tokyo Electron Limited (TEL) – Japan

4. Denton Vacuum LLC – United States

5. Plasma-Therm LLC – United States

6. Shinkong Co., Ltd. – Taiwan

7. Leybold GmbH – Germany

8. Bühler AG – Switzerland

9. Von Ardenne GmbH – Germany

10. Pfeiffer Vacuum GmbH – Germany

11. Kurt J. Lesker Company – United States

12. Applied Materials, Inc. – United States

13. Veeco Instruments Inc. – United States

14. Semicore Equipment, Inc. – United States

15. AJA International, Inc. – United States

16. Mustang Vacuum Systems, Inc. – United States

17. PVD Products, Inc. – United States

18. Angstrom Engineering, Inc. – Canada

19. Singulus Technologies AG – Germany

PVD Coating & Surface Engineering Solution Providers

These companies specialize in industrial PVD coating services, hard coatings, decorative coatings, and surface treatment technologies.

1. Oerlikon Balzers Coating AG – Liechtenstein/Switzerland

2. CemeCon AG – Germany

3. Hauzer Techno Coating B.V. – Netherlands

4. Impact Coatings AB – Sweden

5. HEF Groupe – France

6. Inorcoat – Spain

7. PLATIT AG – Switzerland

8. Voestalpine AG – Austria

Industrial & Engineering Companies with PVD Capabilities

These companies participate in the PVD ecosystem through advanced materials, industrial equipment, and engineering solutions.

1. NISSIN ELECTRIC Co., Ltd. – Japan

2. Kobe Steel, Ltd. – Japan

Frequently Asked Questions:

1. What is the current size of the Physical Vapor Deposition (PVD) market?

The global Physical Vapor Deposition (PVD) Market is growing steadily due to rising use in semiconductor, electronics, medical devices, and industrial coating applications. Market size estimates vary by source and methodology, but the sector is expanding as advanced surface coating demand increases across manufacturing industries.

2. What is driving growth in the Physical Vapor Deposition (PVD) market?

Key growth drivers include increasing semiconductor production, rising demand for wear-resistant coatings, expansion of solar electronics, and growing use of PVD in automotive, aerospace, and healthcare industries. Adoption of precision manufacturing and nanotechnology also supports demand.

3. Which type segment leads the PVD market?

The sputter deposition segment holds a significant share due to its broad application in semiconductor wafers, optical coatings, and electronic devices. Thermal evaporation and arc vapor deposition are also important technologies.

4. Which application dominates the PVD market?

Semiconductor manufacturing remains the leading application, followed by cutting tools, medical equipment, decorative coatings, and solar panel production.

5. Which region dominates the global PVD market?

Asia-Pacific leads the market, supported by strong electronics manufacturing in China, Japan, South Korea, and Taiwan.

6. Which companies are key players in the PVD market?

Major companies include Applied Materials, Lam Research, AIXTRON, ULVAC, and Veeco Instruments.