Pharmaceutical Packaging Market Size by Material, Type, Packaging Type, Drug Delivery Mode, End Use, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

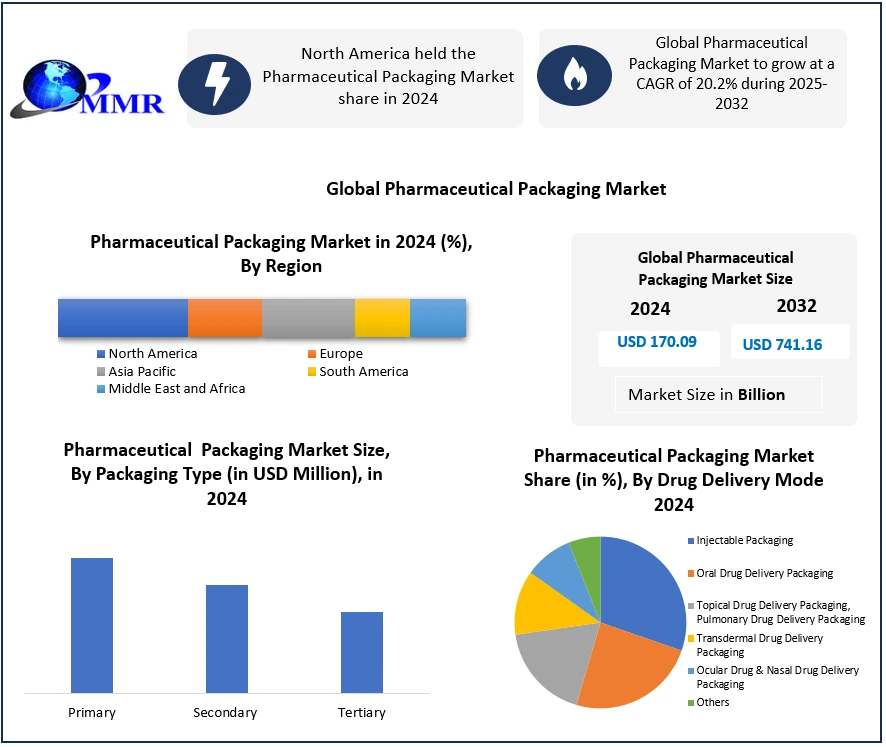

The Pharmaceutical Packaging Market size was valued at USD 170.09 Bn in 2024, reaching USD 741.16 Bn by 2032, and is growing at a CAGR of 20.2% from 2025 to 2032

Pharmaceutical Packaging Market Overview

Pharmaceutical packaging ensures the safety, integrity, and efficacy of medicines by protecting them from contamination, damage, and tampering. It includes materials such as blister packs, bottles, and eco-friendly alternatives. Driven by regulations, technological advancements, and sustainability trends, the market supports patient safety, supply chain efficiency, and evolving healthcare needs globally. The increasing demand for innovative, safe, and sustainable packaging solutions that meet the evolving needs of the healthcare industry. With the expansion of the pharmaceutical sector, increased prevalence of chronic diseases, advancements in biologics, and the growth of generic drugs, the need for reliable and high-quality packaging has intensified. The Pharmaceutical Packaging Market plays a critical role in protecting products from contamination, ensuring proper dosage, and maintaining the efficacy of medications throughout their shelf life.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The stringent regulatory requirements set through agencies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and other global bodies mandate strict compliance with quality and safety standards, further boosting the demand for advanced packaging solutions. Technological innovations, such as smart packaging, tamper-evident features, and track-and-trace systems, are gaining traction as they enhance patient safety, enable supply chain transparency, and address counterfeit drug concerns. The increasing trend toward personalized medicine and self-administration of drugs is creating demand for user-friendly, portable, and patient-centric packaging formats, driving Pharmaceutical Packaging Market growth.

Global Pharmaceutical Packaging Market Dynamics

Increasing Demand for Smart and Sustainable Packaging Solutions to Drive Pharmaceutical Packaging Market Growth

The stricter global regulations, rising consumer awareness, and the industry’s ambitious environmental commitments. sustainable pharma packaging is no longer a niche initiative but a mainstream imperative, driven by the global push to reduce plastic use, ban single-use materials, and embrace the principles of a circular economy. Innovations such as biodegradable and compostable materials, such as cornstarch, mushrooms, sugarcane-based bioplastics, seaweed derivatives, and FSC-certified paper, to recyclable HDPE, PCR plastics, and high-quality Type I borosilicate glass vials, ampoules, syringes, and cartridges.

Smart packaging technologies, including QR codes, NFC tags, e-labeling, and sensor-embedded designs, are merging environmental stewardship with patient safety. These technologies enable reduced paper waste, enhanced product authentication, and real-time tracking. In the Pharmaceutical Packaging Market, flexible packaging, leveraging lightweight multi-layer barrier films, is gaining ground for its space efficiency, lower carbon footprint, and reduced transport costs, while 3D printing is opening doors to personalized, dosage-specific containers that minimize production waste.

Leading companies such as Amcor plc, Berry Global Inc., AptarGroup, Inc.,West Pharmaceutical Services, Inc., Becton, Dickinson and Company (BD) and global pharmaceutical giants are integrating renewable energy into manufacturing, optimizing fill-and-finish processes, and adopting waste-minimizing designs such as pre-filled, recyclable pen systems sycg as PenCycle. The collaborations, such as Schneider Electric’s Energize program, uniting major pharma brands to cut supply chain emissions, and nearly half the industry has joined the UN’s Race to Zero campaign, targeting a 45.8% reduction in Scope 1 and 2 emissions within 12 years. This momentum reflects a shift from compliance-driven sustainability to brand-defining strategy, where packaging is not only a protective medium but also a sustainability statement that meets patient expectations, regulatory mandates, and environmental imperatives.

Rapid growth of biologics and personalized Medicines to Create Market Opportunities

Biologics derived from living cells or organisms require far more stringent packaging, handling, and storage conditions than traditional small-molecule drugs, due to their heightened sensitivity to temperature, light, and environmental factors. Many advanced therapies, such as cell and gene treatments, demand cryogenic storage to maintain stability and efficacy, placing exceptional demands on primary and secondary packaging solutions.

The rise of personalized medicine, where treatments are tailored to an individual’s genetic profile, condition, or therapeutic response, is transforming packaging requirements Pharmaceutical Packaging Market. Precision dosing, patient-specific labeling, and highly customized container formats are becoming essential to ensure safety, accuracy, and regulatory compliance. This shift is driving innovation in labeling technologies, serialization, and tamper-evident features, alongside the use of smart packaging equipped with NFC, RFID, or IoT sensors to enable real-time tracking and authentication.

The Pharmaceutical companies and Contract Development and Manufacturing Organizations (CDMOs) are investing in advanced packaging capabilities, including temperature-controlled formats, specialized vial and syringe systems, and multi-layer labeling solutions tha accommodate extensive product information without sacrificing usability. Coupled with sustainability initiatives such as recyclable materials, biodegradable components, and energy-efficient production processes, these innovations are positioning the Pharmaceutical Packaging Industry for growth.

High Cost in Packaging Solutions to Create Restraint in the Drive Pharmaceutical Packaging Market

Pharmaceutical packaging adheres to stringent international regulations concerning safety, quality, and traceability, which require specialized materials, sterile environments, and complex production processes. These factors significantly increase manufacturing costs, particularly for small and mid-sized pharmaceutical companies that lack the infrastructure to support such investments. Also, the frequent updates to global compliance standards and the need for validation testing further add to operational and time-related costs. This financial burden limits innovation and slows down Pharmaceutical Packaging Market penetration, especially in price-sensitive or developing regions, posing a major restraint to the overall growth of the market.

Global Pharmaceutical Packaging Market Segment Analysis

Based on Material, the market is segmented into the Plastic & Polymers, Glass, Paper and paperboard and Others. Plastic & polymers hold the dominant share in the global pharmaceutical packaging market in 2024. Due to their versatility, cost-effectiveness, and compatibility with a wide range of drug formulations. They offer excellent barrier properties against moisture, oxygen, and contaminants, ensuring product stability and extended shelf life. Materials such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), and polyvinyl chloride (PVC) are widely used for bottles, blister packs, pouches, and caps. The lightweight nature of plastics reduces transportation costs and enhances ease of handling, while their moldability enables innovative, patient-friendly designs. Additionally, plastics support advanced features such as tamper-evidence, child resistance, and unit-dose packaging, improving patient safety and compliance. Recent innovations in biodegradable and recyclable plastics are boosting adoption, aligning with sustainability goals. Their compatibility with high-speed manufacturing lines and adaptability for sterile and non-sterile applications reinforce their leadership in the Pharmaceutical Packaging Market.

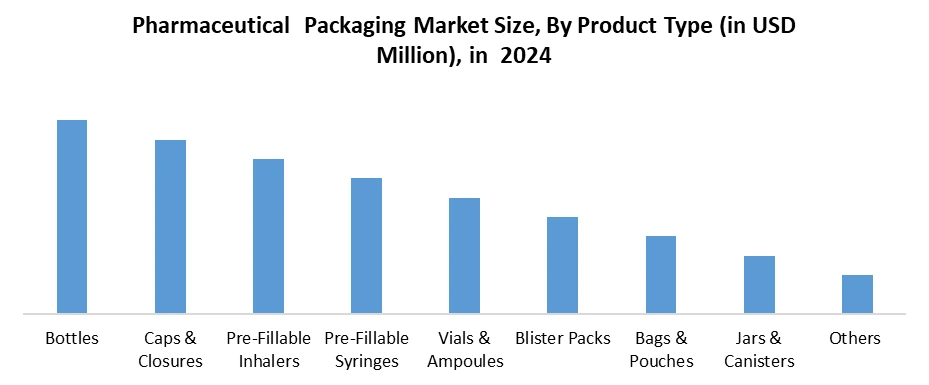

Based on Product Type, the market is categorized into Bottles, Caps & Closures, Pre-Fillable Inhalers, Pre-Fillable Syringes, Vials & Ampoules, Blister Packs, Bags & Pouches, Jars & Canisters and Others. Blister packs are the dominant packaging type in the pharmaceutical packaging market in 2024, widely used for solid oral dosage forms such as tablets and capsules. They offer an ideal combination of protection, dosage accuracy, and patient convenience. Made primarily from a combination of plastic films (such as PVC, PVDC, or PET) and aluminum foil, blister packs provide an effective moisture, oxygen, and light barrier, safeguarding drug stability and efficacy throughout its shelf life. The unit-dose format of blister packs minimizes contamination risks, ensures hygienic handling, and supports medication adherence by allowing patients to track dosage schedules easily. Regulatory bodies, including the FDA and EMA, favor blister packaging for its tamper-evident and child-resistant properties, which enhance safety and compliance. The format also facilitates product identification through clear labeling and transparent cavities, making it user-friendly for patients and caregivers. Blister packs are cost-effective for high-volume production and adaptable for various.

Pharmaceutical Packaging Market Regional Insights

North America held the largest Pharmaceutical Packaging Market Share in 2024. The strong pharmaceutical manufacturing base, a highly developed healthcare infrastructure, and strong adoption of cutting-edge packaging technologies drive the Pharmaceutical Packaging Market. The region’s market leadership is reinforced by stringent regulatory frameworks, significantly those implemented by the U.S. Food and Drug Administration (FDA), which enforce strict quality, safety, and compliance standards, ensuring that packaging solutions meet the highest global benchmarks. This regulatory environment fosters innovation while safeguarding patient health.

The increasing demand for specialized packaging solutions to accommodate the rising production of biologics, personalized medicines, and controlled-release drug formulations is further driving market expansion. Pharmaceutical companies and contract packaging organizations (CPOs) in the region are investing heavily in advanced materials, smart packaging systems, and sustainable solutions to address the evolving needs of healthcare providers, patients, and regulators. The growing emphasis on patient safety, product integrity, and supply chain traceability is encouraging the integration of features such as tamper-evident seals, child-resistant closures, and RFID-enabled tracking systems. Additionally, demographic trends, including an aging population and the increasing prevalence of chronic diseases, are driving the demand for reliable, convenient, and compliant packaging formats. Rising healthcare expenditure, strong R&D investments, and a focus on sustainability are influencing product development strategies, with companies increasingly adopting recyclable materials, reducing packaging waste, and optimizing transportation efficiency.

Pharmaceutical Packaging Market Competitive Landscape

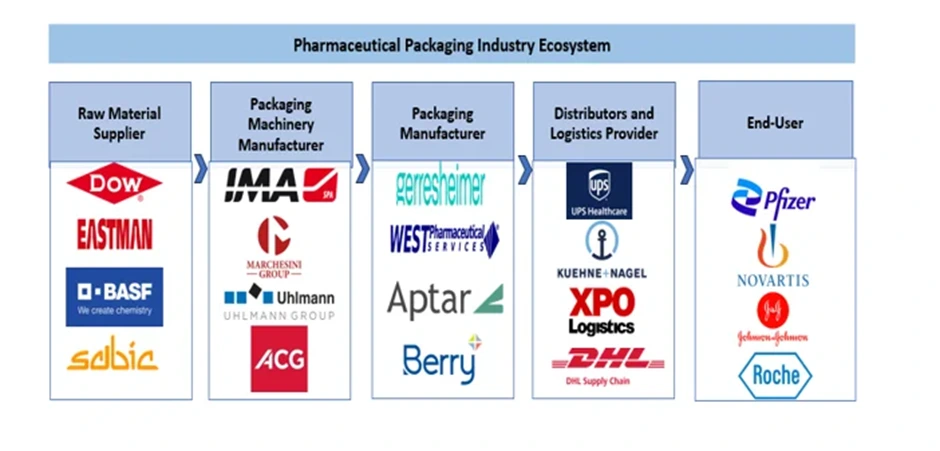

The Pharmaceutical Packaging Market is highly competitive, driven by innovation, regulatory compliance, and the growing demand for sustainable, high-performance solutions. Global leaders such as Amcor plc, Berry Global Inc., Gerresheimer AG, SCHOTT Pharma, West Pharmaceutical Services, AptarGroup, Catalent, and Constantia Flexibles dominate through diversified portfolios that cater to every stage of pharmaceutical distribution from sterile primary packaging like vials, syringes, and blister packs to secondary cartons and tamper-evident closures. In North America, players like such as e Amcor, Berry Global, WestRock, and BD excel in advanced manufacturing and FDA-compliant solutions for biologics and specialty drugs. Europe stands out for precision glass and eco-friendly packaging, with Gerresheimer, SCHOTT, Stevanato Group, and SGD Pharma leading in premium quality and sustainable innovation. Meanwhile, the Asia-Pacific region is emerging as a growth powerhouse, driven by cost-efficient manufacturing, expanding pharmaceutical exports, and investments from both local champions such as Piramal Glass and global giants.

Key Development in the Pharmaceutical Packaging Market

• On April 2025, Amcor completed construction of an advanced healthcare packaging coating facility in Selangor, Malaysia, marking the first in Asia to feature state-of-the-art air knife coating technology. This advancement enables local production of both top and bottom substrates for medical device packaging, significantly reducing lead times and enhancing supply security. The facility incorporates water-based coating systems, online inspection mechanisms, and precision air knife technology to boost operational efficiency while minimizing waste. Alongside this milestone, Amcor expanded its Asia Pacific presence through strategic acquisitions, including MDK in China, a grid lacquer paper unit in India, and a co-extrusion blown film and printing plant in Singapore.

• On October 31, 2024 – Berry Global launched its ClariPPil™ range of clarified polypropylene (PP) bottles for healthcare applications, offering enhanced sustainability, improved recyclability, and superior product protection compared to traditional PET bottles. Certified RecyClass A, these bottles deliver up to 84% better moisture ingress protection and approximately 71% lower CO₂ emissions than PET manufacturing. Available in various sizes and colors, including customizable options, they are compatible with standard closures and meet diverse product needs such as vitamins, nutraceuticals, and OTC treatments. Berry will showcase these innovations, alongside its CDMO services, at Pharmapack 2025 in Paris, reinforcing its commitment to advancing sustainable, high-performance solutions in the Pharmaceutical Packaging Market.

Key Trends of the Pharmaceutical Packaging Market

| Trend | Description | Impact on Market |

| Sustainable & Eco-Friendly Packaging | Growing shift towards biodegradable, recyclable, and plastic-free materials to meet environmental regulations and consumer preferences. | Drives innovation in packaging materials and boosts adoption of green solutions. |

| Smart & Connected Packaging | Integration of QR codes, NFC tags, and sensors for authentication, patient engagement, and supply chain tracking. | Enhances patient safety, combats counterfeiting, and improves traceability. |

| Rise in Biologic & Injectable Drugs | Increased demand for pre-filled syringes, vials, and advanced containment solutions to support biologics. | Spurs growth in specialized, high-barrier, and sterile packaging formats. |

Pharmaceutical Packaging Market Scope: Inquire before buying

| Global Pharmaceutical Packaging Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 170.09 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 20.2% | Market Size in 2032: | USD 741.06 Bn. |

| Segments Covered: | by Material | Plastic & Polymers Polyvinyl Chloride (PVC) Polypropylene (PP) Polyethylene Terephthalate (PET) Polyethylene (PE) HDPE LDPE LLDPE Polystyrene (PS) Others Glass Paper and paperboard Others |

|

| by Type | Bottles Caps & Closures Pre-Fillable Inhalers Pre-Fillable Syringes Vials & Ampoules Blister Packs Bags & Pouches Jars & Canisters Others |

||

| by Packaging Type | Primary Secondary Tertiary |

||

| by Drug Delivery Mode | Injectable Packaging Oral Drug Delivery Packaging Topical Drug Delivery Packaging, Pulmonary Drug Delivery Packaging Transdermal Drug Delivery Packaging Ocular Drug & Nasal Drug Delivery Packaging Others |

||

| by End Use | Pharmaceutical Manufacturing Companies Contract Packaging Organizations (CPOs) Contract Manufacturing Organizations (CMOs) Hospitals & Clinics Retail Pharmacies Others |

||

Pharmaceutical Packaging Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Pharmaceutical Packaging Key Players

North America

1. Amcor plc

2. Berry Global Inc.

3. AptarGroup, Inc.

4. West Pharmaceutical Services, Inc.

5. Becton, Dickinson and Company (BD)

6. Corning Inc.

7. Catalent, Inc.

8. WestRock Company

9. Sonoco Products Co.

10. Winpak Ltd.

Europe

1. Gerresheimer AG

2. SCHOTT Pharma

3. Constantia Flexibles

4. Stevanato Group

5. Vetter Pharma

6. August Faller GmbH & Co. KG

7. Romaco Group

8. GEA Pharma Systems

9. Erweka GmbH

10. SGD Pharma

Asia-Pacific

1. Piramal Glass Private Limited

2. Schott AG

3. Gerresheimer AG

4. Stevanato Group

5. Vetter Pharma

6. Constantia Flexibles

7. SGD Pharma

8. Corning Inc.

9. Catalent, Inc.

10. AptarGroup, Inc.

Frequently Asked Questions:

1. Which region has the largest share in the Global Pharmaceutical Packaging Market?

Ans: The North America region held the highest share in 2024.

2. What is the growth rate of the Global Pharmaceutical Packaging Market?

Ans: The Global Pharmaceutical Packaging Market is growing at a CAGR of 20.2% during the forecasting period 2025-2032.

3. What is the scope of the Global Pharmaceutical Packaging Market report?

Ans: The Global Pharmaceutical Packaging Market report helps with the PESTEL, PORTER, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in the Global Pharmaceutical Packaging Market?

Ans: The key players in the Global Pharmaceutical Packaging Market are Amcor plc, Berry Global Inc., AptarGroup, Inc.,West Pharmaceutical Services, Becton, Dickinson and Company (BD) and Others.

5. What is the study period of this Market?

Ans: The Global Pharmaceutical Packaging Market is studied from 2024 to 2032.