Organic Food Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

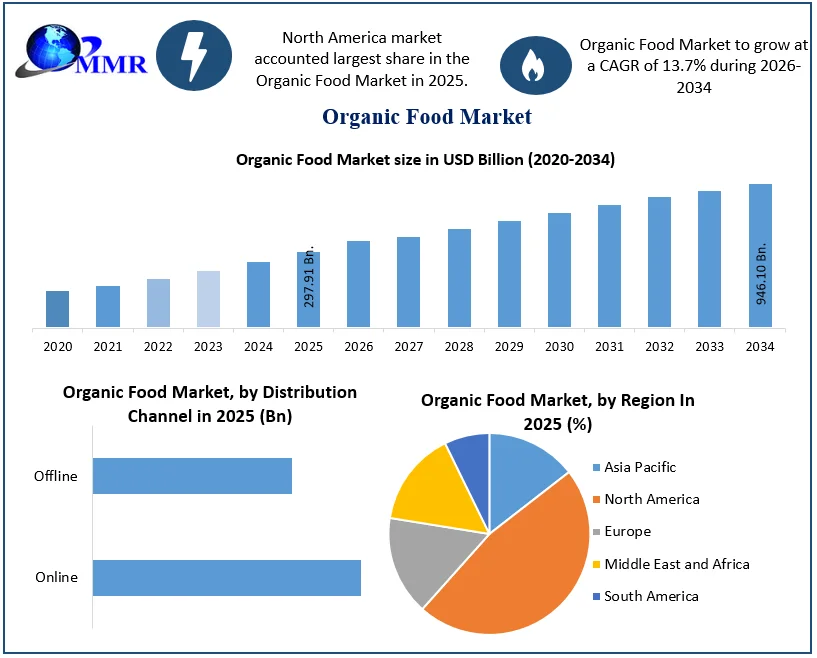

The Organic Food Market size was valued at USD 297.91 Billion in 2025 and the total Organic Food revenue is expected to grow at a CAGR of 13.7% from 2026 to 2034, reaching nearly USD 946.10 Billion.

Organic Food Market Overview

Organic Food is food grown without using any chemical fertilizers, hormones, pesticides, and antibiotics, which promotes ecological balance and conserves biodiversity. Organic food is not processed using irradiation, industrial solvents or chemicals, food preservatives, and synthetic food additives. Organic agriculture is emerging significantly in most countries across the globe. The rise in awareness regarding the advantages of organic food is expected to fuel the Organic Food Market growth during the forecast period.

Organic Food Market Dynamics: Drivers, Restraints, Trends and Opportunities.

Organic Food Market Growth Outlook

To know about the Research Methodology :- Request Free Sample Report

Increasing Health Consciousness to Drive the Market Growth

A significant driver for the organic food market is the growing awareness and prioritization of health among consumers. With rising concerns about the impact of conventional farming practices on health, such as pesticide residues and genetically modified organisms (GMOs), consumers are actively seeking safer and healthier food options. Organic food, which is produced without synthetic pesticides, fertilizers, or GMOs, is perceived as a healthier choice, leading to increased demand. Moreover, the rise in lifestyle-related diseases and health issues has fueled the demand for organic foods as consumers become more conscious of the relationship between diet and health outcomes. This trend is expected to continue as consumers increasingly prioritize natural, wholesome, and nutritionally dense foods, driving growth in the organic food market.

Organic farming has emerged as an efficient method to obtain organic food and act as an eco-friendly farming system. Organic farming prevents weed, disease, and pest effects of crop production along with retaining soil fertility. Thus, growing interest in organic farming is driving market growth across the globe. Currently, there are more than 0.0049 billion producers organically managing 0.0732 billion hectares of agricultural land and 0.0010 billion hectares of certified organic aquaculture across the globe.

Increasing demand for organic food such as organic crops, organic milk, organic dairy, and non-dairy products, organic meat, fish, and organic poultry products are fueling the market growth for organic food across the globe. For instance, Studies show that on average there is a 63% higher content of omega-3 fatty acids in organic milk over conventional milk. Organic food products are safer, and more nutritious as compared to conventional food items. These health benefits of organic foods encourage consumers to buy more organic products, resulting in the growth of the organic food market across the globe.

Sustainability as a Game-Changer in the Organic Food Market

The demand for the organic food market is driven by the concerns of people, towards personal health and the environment. The changing dietary habits of people and the awareness about the issues in conventionally farmed foods are expected to impact positively consumers' preference towards organic food. According to an UN report, around 200,000 people lose their lives every year due to the toxic effects of pesticides in food products. This factor also results in changing consumers' focus on organic food products.

Sustainability is emerging as a pivotal force within the organic food industry, transcending consumer preferences to become a key determinant of industry growth. Beyond consumer demand for healthier options, sustainability encompasses ethical considerations, environmental stewardship, and long-term viability. As climate change concerns intensify and consumers become more conscientious about their purchasing decisions, organic food producers have a unique opportunity to position themselves as champions of sustainability. This entails adopting regenerative agricultural practices, reducing carbon footprints, minimizing waste, and supporting local economies. By aligning with sustainable principles, organic food brands not only enhance their market appeal but also contribute tangibly to environmental preservation and social responsibility. Leveraging sustainability as a core value proposition differentiates brands, fosters consumer trust, and drive long-term growth in the increasingly competitive organic food market landscape. Embracing sustainability isn't just a trend; it's becoming a prerequisite for success in the organic food industry.

As India’s organic food sector undergoes this tech-driven metamorphosis, it is evident that technology is not just a tool but a catalyst for positive change. The unique dynamics of India’s agricultural landscape, coupled with the transformative power of technology, pave the way for a more sustainable and resilient future for the organic food industry in the country.

Table: The Symbiosis of Technology and Organic Farming in India:

| Unique Facets | Description |

| AgriTech Startups | The proliferation of AgriTech startups is providing Indian organic farmers with digital tools to enhance crop monitoring, supply chain optimization, and market access. |

| Mobile Technology for Farmer Outreach | Mobile technology disseminates real-time weather updates, market prices, and best organic farming practices directly to farmers, bolstering their knowledge base. |

| Organic Certification Platforms | Platforms like Jaivik Bharat streamline the organic certification process in India, reducing bureaucratic hurdles, and ensuring the credibility of organic products. |

| Solar-Powered Solutions | India integrates solar-powered solutions such as pumps and cold storage, addressing power supply challenges in remote areas and aligning with the sustainable ethos of organic farming. |

| Community-Supported Agriculture (CSA) Platforms | The rising popularity of CSA platforms connects Indian consumers directly with local organic farmers, facilitated by technology, fostering a robust farmer-consumer relationship. |

Cost Barrier Hindering Organic Food Market Growth

One key restraining factor in the organic food market is the higher cost compared to conventionally grown produce. This cost barrier limits the accessibility of organic products to a wider consumer base. Organic farming practices often require more labor-intensive methods, such as manual weeding and natural pest control, which contribute to increased production costs. Additionally, obtaining organic certification involves stringent standards and inspections, further adding to the expenses. As a result, organic foods typically command a premium price in the market.

While some consumers are willing to pay extra for the perceived health and environmental benefits of organic produce, many others are deterred by the higher prices, especially in regions where disposable income is limited. This pricing disparity creates a challenge for organic producers to compete with conventional counterparts on a larger scale. To address this issue and stimulate market growth, efforts are needed to reduce production costs through innovation, subsidies, and increased consumer education on the long-term benefits of organic farming practices.

Organic Food Market Segment Analysis

Based on product, the fruits and vegetables segment held the largest Organic Food Market share in 2025. Developed nations like Europe and North America exhibit maximal demand for organic fruits and vegetables, buoyed by substantial disposable incomes. Simultaneously, burgeoning economies such as China and India are witnessing an escalating appetite for organic produce. Furthermore, there's a noticeable uptick in the consumption of organic fish and poultry products, a trend poised to surge during the forecast period. The market's growth is propelled by mounting health consciousness and a deepening understanding of the benefits of organic food. The absence of preservatives aimed at extending shelf life enhances the appeal of organic vegetables and roots, auguring well for their future expansion.

By Distribution Channel: In 2025, the offline segment dominated the largest Organic Food Market share. Offline stores boast a diverse array of products, spanning domestic and branded offerings. Organic products are readily accessible through specialty stores, supermarkets, hypermarkets, and various general stores. While sales of organic food products thrive in developed nations, efforts are underway to bolster sales in developing nations by tailoring hypermarkets and supermarkets to favor organic food products. The offline channel remains instrumental in driving sales of these products, facilitating wider reach and accessibility to consumers across different regions.

Organic Food Market Regional Analysis

The North American region held the largest Organic Food Market share in 2025 and growth is driven by surging demand for organic produce, particularly from the United States. Australia is witnessing a similar trend, prompting the government to implement supportive policies for organic farming. Regulatory bodies are actively engaging in the formulation of policies conducive to organic farming, fostering market growth in developed nations like North America and Europe. Moreover, the increasing purchasing power in these regions is expected to further fuel market expansion. The rising popularity of vegan diets, accompanied by their associated benefits, is contributing to the heightened consumption of organic food products. Heightened awareness of the health risks associated with chemical exposure from preservatives, fertilizers, and pesticides used in conventional farming practices is also driving the demand for organic farming.

The Asia Pacific Organic Food Market is projected to experience robust growth, with a Compound Annual Growth Rate (CAGR) of 18.1% from 2026 to 2034. This growth is primarily fueled by the increasing popularity of ready-to-eat foods among the working-class demographic and the sizable millennial population, notably in countries like India. Major markets in terms of consumer spending on food include China, India, and Japan. Additionally, there's a notable surge in demand for frozen food due to time constraints for preparation and cooking, thus creating new opportunities for organic frozen food in the regional market.

Europe's organic food market is expected to grow at a CAGR of xx % from 2026 to 2034. This growth is attributed to a significant shift in consumer attitudes toward sustainability and ethical consumption, signaling a growing preference for organic products in the region. A sustainable food system is at the heart of the European Green Deal. Under the Green Deal’s Farm to Fork strategy, the European Commission has set a target of at least 25% of the EU’s agricultural land under organic farming and a significant increase in organic aquaculture by 2034’. The Commission has set out a comprehensive organic action plan for the European Union. Through it, the Commission will aim to achieve the European Green Deal target of 25% of agricultural land under organic farming by 2034. Organic farming is knowledge-intensive. However, there is still a clear need to further enhance the knowledge so that organic farming becomes even more sustainable and also more productive. To support the ambitions of the action plan, the Commission intends to dedicate at least 30% of the budget for research and innovation actions in the fields of agriculture, forestry and rural areas to topics specific to or relevant to the organic sector. This includes issues such as increased crop yields, genetic biodiversity and alternatives to contentious products. Such factors are expected to drive the regional Organic Food Market growth.

Organic Food Market Scope: Inquire before buying

| Organic Food Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 297.91 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 13.7% | Market Size in 2034: | USD 946.10 Bn. |

| Segments Covered: | by Product | Fruits and vegetables Dairy products Meat Fish and poultry Frozen foods Others |

|

| by Distribution Channel | Online Offline |

||

Organic Food Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Organic Food Market, Key Players

The Global Organic Food involves the trade and processing of natural, unprocessed foods free from any kind of chemicals or genetic modifications. The important sectors that have been identified to be driving this market are organic fruits and vegetables, dairy products, and beverages.

| Company Name | Headquarters | Core Competencies |

| General Mills, Inc. | Minneapolis, Minnesota, USA | Organic cereals, snacks, packaged organic foods (Annie's) |

| Cargill, Incorporated | Wayzata, Minnesota, USA | Organic grains, food ingredients, agricultural products |

| United Natural Foods, Inc. | Providence, Rhode Island, USA | Organic food distribution, natural foods, grocery supply |

| The Hain Celestial Group, Inc. | Hoboken, New Jersey, USA | Organic packaged foods, beverages, and personal care products |

| Dole plc | Dublin, Ireland | Organic fresh fruits and vegetables |

| Newman's Own, Inc. | Westport, Connecticut, USA | Organic salad dressings, sauces, snacks, beverages |

| The Hershey Company | Hershey, Pennsylvania, USA | Organic chocolate and confectionery products |

| Nature's Path Foods | Richmond, British Columbia, Canada | Organic cereals, granola, oatmeal, breakfast foods |

| Danone S.A. | Paris, France | Organic dairy products, plant-based foods, beverages |

| Arla Foods amba | Viby J, Denmark | Organic milk, cheese, butter, dairy products |

| HiPP GmbH & Co. Vertrieb KG | Pfaffenhofen, Germany | Organic baby food, infant nutrition, cereals |

| Amul | Anand, Gujarat, India | Organic milk, dairy products, organic ghee |

| Suminter India Organics | Mumbai, Maharashtra, India | Organic grains, spices, oilseeds, food ingredients |

| Sresta Natural Bioproducts Pvt. Ltd. | Hyderabad, Telangana, India | Organic packaged foods under the 24 Mantra Organic brand |

| Nature Bio-Foods Limited | Gurugram, Haryana, India | Organic grains, pulses, oilseeds, food ingredients |

| China Shengmu Organic Milk Limited | Hohhot, Inner Mongolia, China | Organic milk and dairy products |

| Tony's Farm | Shanghai, China | Organic fruits, vegetables, and fresh farm produce |

| Amy's Kitchen, Inc. | Petaluma, California, USA | Organic frozen meals, soups, pizzas, snacks |

| Eden Foods, Inc. | Clinton, Michigan, USA | Organic beans, grains, pasta, grocery products |

| Organic Valley/CROPP Cooperative | La Farge, Wisconsin, USA | Organic dairy products, eggs, meat, vegetables |

Frequently Asked Questions:

1] What is the growth rate of the Global Organic Food Market?

Ans. The Global Organic Food Market is growing at a significant rate of 13.7 % during the forecast period.

2] Which region is expected to dominate the Global Organic Food Market?

Ans. North America is expected to dominate the Organic Food Market during the forecast period.

3] What is the expected Global Organic Food Market size by 2034?

Ans. The Organic Food Market size is expected to reach USD 946.10 Bn by 2034.

4] Which are the top players in the Global Organic Food Market?

Ans. The major top players in the Global Organic Food Market are Cargill Inc., Amul and others.

5] What are the factors driving the Global Organic Food Market growth?

Ans. The increasing health consciousness among the population is expected to drive the Organic Food Market growth.

6] What was the Global Organic Food Market size in 2025?

Ans: The Global Organic Food Market size was USD 297.91 Billion in 2025.