Global Needles Market by Needle Type, Product Type, Delivery Site, End User, and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

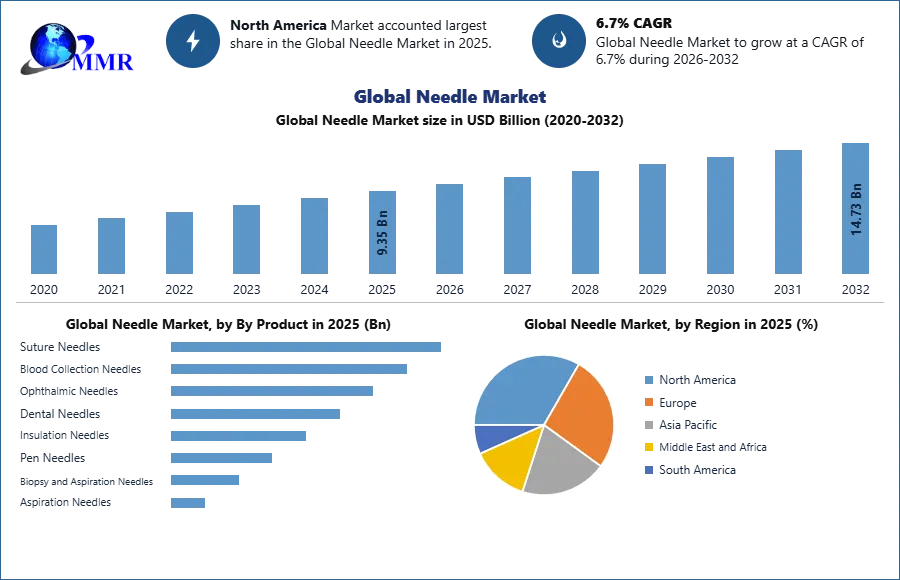

The Needle Market size was valued at USD 9.35 Billion in 2025 and the total Needle revenue is expected to grow at a CAGR of 6.7% from 2026 to 2032, reaching nearly USD 14.73 Billion.

Needle Market Overview

The global needles market has experienced steady growth, driven by factors such as the increasing prevalence of chronic diseases, the rise in geriatric population, and the expansion of healthcare infrastructure in emerging economies. The market scope includes a wide range of needle types, such as conventional needles for routine injections and safety needles designed to prevent needlestick injuries. These needles find applications in various medical procedures, including drug delivery, blood collection, and aesthetic procedures.

A key trend in the needles market is the growing demand for safety needles, particularly in regions with stringent regulations aimed at protecting healthcare workers from needlestick injuries. Another trend is the increasing adoption of needle-free technologies, driven by the need for more patient-friendly drug delivery methods. Besides, there is a rising focus on sustainability in needle manufacturing, with companies developing eco-friendly and recyclable needle products.

The needles market is primarily used by hospitals, clinics, diagnostic laboratories, ambulatory surgical centers, and home care settings. Hospitals are the largest end users, accounting for a significant portion of market revenue. Clinics and diagnostic laboratories also use needles for diagnostic procedures and sample collection. Ambulatory surgical centers are adopting advanced needle technologies for minimally invasive procedures. Home care settings are growing owing to self-administration of medications, particularly among patients with chronic conditions like diabetes.

Asia Pacific has been emerging as a leading region in the global needles industry, driven by factors such as the rise in per capita healthcare expenditure, increasing prevalence of chronic diseases, and expanding healthcare infrastructure. The region is witnessing a shift towards advanced needle technologies, leading to qualitative and quantitative growth in the market. Revenue trends indicate a significant rise in the demand for needles, particularly safety needles, in countries like China, Japan, and India. Inclusive, Asia Pacific's growing healthcare sector and rising disposable income are boosting the region to the forefront of the global needles market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Needle Market Dynamics

"Increasing prevalence of chronic diseases and rising geriatric population driving the needles market"

The needles market has experienced significant growth driven by several key factors. One of the primary drivers is the increase in sales volume, which is attributed to the expanding elderly population globally. As people age, the prevalence of chronic diseases increases, leading to a higher demand for medications that often require needle-based delivery methods. Additionally, the trend towards drug self-administration, driven by convenience and cost-effectiveness, is further boosting the demand for needles. Also, the market is witnessing an improvement in profit margins, largely owing to favorable regulatory policies for novel injectables. Regulatory bodies are increasingly approving new and advanced needle technologies, such as safety needles, which not only enhance patient safety but also provide companies with a competitive edge. This has led to increased adoption of these technologies, driving up profit margins for needle manufacturers.

• For example, Rhythmlink International, LLC's launch of a new product family, concentric needles, with various sizes and gauges tailored to accepted workflows, has enhanced sales volume and profitability in the market

• By 2030, approximately 1.4 billion worldwide are expected to be more than 60 years old, according to the World Health Organization (WHO)

Besides, strategic alliances between companies are playing a vital role in driving market growth. These alliances enable companies to combine their resources and expertise to develop innovative products and expand their market reach. By leveraging each other's strengths, companies introduce new and improved needle products, meeting the evolving needs of healthcare providers and patients alike.

Advancements in drug delivery devices

The needle market has been experienced significant growth owing to advancements in drug delivery devices. The pharmaceutical industry is prioritizing patient-centric designs, with auto-injectors, pen injectors, and advanced syringes influencing demand. Auto-injectors are popular for chronic diseases, while pen injectors simplify insulin delivery. Safety syringes and prefilled syringes offer convenience and reduced medication waste. The growth of drug delivery devices for biologics and the biosimilars market is driven by the demand for specialized needles for high-viscosity formulations. Public-private financing for targeted research activities is expected to drive innovation and product development, leading to increased market revenue. Additionally, the growth of hospitals and laboratories is likely to boost production capacity, further fueling market growth.

• For instance, Roche Diabetes Care's launch of Accu-Fine quality pen needles, aimed at improving insulin delivery and diabetes management, thus it is expected to drive market revenue growth.

Trends in Needle Technology

Progressions in needle technology are driving market growth, with a key trend being the development of needle-free technologies.

• For example, Vaxxas was awarded $3.7 million from the Wellcome Foundation for the development of needle-free typhoid vaccine technology, highlighting the industry's shift towards innovative needle alternatives.

Other trends include the development of smaller, more precise needles for minimally invasive procedures, as well as the integration of digital technologies for enhanced monitoring and control. These trends are expected to drive further market growth in the coming years.

Transition towards single-use needles

The healthcare sector is transitioning towards single-use needles, which are disposable and disposable, reducing cross-contamination and infectious disease transmission. These needles offer higher infection control standards, preventing the spread of diseases like HIV, hepatitis B, and hepatitis. Global healthcare regulations mandate the use of single-use needles for medical procedures, improving patient safety. Despite the need for repeated purchases, single-use needles can be cost-effective due to the long-term costs associated with sterilizing reusable needles and treating needle stick injuries or infections.

• On 7th March 2024, Hindustan Syringes and Medical Devices (HMD) has launched Dispojekt single-use with safety needle, which further which further strengthens India's position in medical devices.

Needle Market Segment Analysis

Based on Needle Type, the conventional needles segment held the largest market share in 2025. This is primarily owing to the longstanding use and familiarity of conventional needles in medical procedures worldwide. Healthcare professionals are accustomed to conventional needles, which are often perceived as reliable and cost-effective. While safety needles are gaining traction owing to growing concerns about needlestick injuries, the transition to safety needles is gradual. Factors such as the perceived higher cost of safety needles and the need for training on their proper use contribute to the continued dominance of conventional needles. Additionally, in regions with limited healthcare infrastructure or resources, conventional needles remain the preferred choice. However, with increasing awareness and regulatory initiatives promoting the use of safety devices, the market share of safety needles is expected to grow steadily in the coming years.

Based on Product, the suture needles segment has been expected to dominate the global needles market during the forecast period 2032. This dominance is attributed to several factors, including the increasing incidence of chronic diseases worldwide. As the prevalence of chronic conditions rises, the demand for surgical procedures, including those requiring suture needles, also increases. Additionally, the segment is experiencing growth thanks to the rising support from private and public healthcare organizations. These organizations are investing in healthcare centers and facilities, which is leading to an increased use of suture needles in various medical procedures. Moreover, advancements in suture needle technology, such as the development of more precise and efficient needles, are further driving the growth of this segment.

Needle Market Regional Insights

North America has been dominated the global needle market, driven by robust import-export activities and a well-established supply chain. The region's dominance is attributed to factors such as a high prevalence of chronic diseases, advanced healthcare infrastructure, and strong regulatory frameworks promoting the adoption of innovative medical technologies. North America boasts a strong import-export network, facilitating the efficient flow of needles and related products across borders. The region's strategic geographical location and extensive trade partnerships further bolster its position as a key player in the global needle market.

Also, North America's well-developed supply chain ensures timely delivery of needles to healthcare facilities, contributing to the region's market leadership. The presence of major needle manufacturers and distributors in North America also plays vital role in driving market growth. Furthermore, the region's focus on research and development in the healthcare sector fosters innovation and drives demand for advanced needle technologies. Overall, North America's leading position in the needle market is characterized by its strong import-export activities, robust supply chain, and commitment to innovation in healthcare.

• The top 3 importers of Needles, North America are India with 1,094,911 shipments followed by Vietnam with 585,748 and United States at the 3rd spot with 210,146 shipments.

• Mexico exports most of its Needles, North America to India, Germany and Argentina.

• The top 3 exporters of Needles, North America are India with 702,886 shipments followed by China with 635,526 and Germany at the 3rd spot with 505,913 shipmen In the Europe region, the needle type segment is dominated by conventional needles for subcutaneous and intramuscular injections. These needles account for over 75% of the total needle market owing to their low cost and widespread adoption in routine healthcare procedures. Several European countries heavily rely on conventional disposable needles for delivering common vaccines and medications. For instance, in May 2021, public health authorities in Italy released data showing that over 95% of vaccine doses from 2018-2020 were administered using conventional needles. This preference is primarily because conventional needles are inexpensive and can be produced at large volumes, making them the preferred option for cash-strapped public health systems.

In the Europe region, the needle type segment is dominated by conventional needles for subcutaneous and intramuscular injections. These needles account for over 75% of the total needle market owing to their low cost and widespread adoption in routine healthcare procedures. Several European countries heavily rely on conventional disposable needles for delivering common vaccines and medications. For instance, in May 2021, public health authorities in Italy released data showing that over 95% of vaccine doses from 2018-2020 were administered using conventional needles. This preference is primarily because conventional needles are inexpensive and can be produced at large volumes, making them the preferred option for cash-strapped public health systems.

Needle Market Competitive Landscapes

The global needles market is relatively fragmented, with a high level of competition. The prominent players operating in the market are constantly adopting various growth strategies to stay afloat in the market. Product launches, innovations, mergers, and acquisitions, collaborations and partnerships, and intensive R&D are some of the growth strategies that are adopted by these key companies to thrive in the competitive market. The key market players are also constantly focused on R&D to supply industries with the most efficient and cost-effective solutions.

• In September 2022, Serpex Medical announced U.S. FDA 510(k) clearance of its Compass Steerable Needless – steerable biopsy needles that enable precise access to lung nodules in the intrapulmonary region to improve the diagnosis and treatment of lung cancer. The clearance of the compass steerable needles follows the clearance of Serpex's Recon Steerable Sheath.

• On September 26, 2023, Sharps Technology, Inc., an innovative medical device and pharmaceutical packaging company and Nephron Pharmaceuticals Corporation, a privately owned U.S. leader in contract manufacturing and 503B outsourcing, announce the signing of an Asset Purchase Agreement (APA) to acquire Nephron’s InjectEZ specialty syringe manufacturing facility. This includes a purchase agreement for over US$ 400 Mn from Nephron Pharmaceuticals for next-generation copolymer prefillable syringe systems.

• In January 2022, ICU Medical Inc., a medical device company, announced acquisition of Smiths Medical, a medical device company. Smiths Medical business includes syringe and ambulatory infusion devices, vascular access, and vital care products.

Recent Developments

- In May 2021, Olympus Corporation (US) introduced the FDA-approved BF-UC190F endobronchial ultrasound (EBUS) bronchoscope for minimally invasive lung cancer detection and staging by needle biopsy.

- In June 2022, Wuxi Biologics, a worldwide contract research, development, and manufacturing organization (CRDMO), has begun GMP operations at its new drug product facility DP5 in Wuxi, China. For pre-filled syringes (PFS), the facility provides many volume delivery choices.

- On October 13, 2023, Rhythmlink International, LLC, a medical device company, launched a new product family, concentric needles. The concentric needle is offered in four sizes or gauges, which also vary in needle diameter, length and color, matching the accepted workflows.

- In May 2022, Roche Diabetes Care, a global leader in integrated personalized diabetes management (iPDM), launched Accu-Fine, quality pen needles to make the process of insulin delivery smoother and virtually painless for people with diabetes. This latest innovation from (Roche Diabetes Care, maker of Accu-Chek) the house of Accu-Chek aims to make the process of insulin delivery easier thereby leading to better diabetes management for people with diabetes.

-

| Global Needle Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 9.35 USD Billion |

| Forecast Period 2026-2032 CAGR: | 6.7% | Market Size in 2032: | 14.73 USD Billion |

| Segments Covered: | By Product | Suture Needles Blood Collection Needles Ophthalmic Needles Dental Needles Insulation Needles Pen Needles Standard Needle Safety Needles Biopsy and Aspiration Needles Biopsy Needles Core Biopsy Needles Vacuum Assisted Needles Aspiration Needles |

|

| By Type | Conventional Needles Bevel Needles Blunt Fill Needles Filter Needles Vented Needles Safety Needles Active Needles Passive Needles |

||

| By Delivery Mode | Hypodermic Needles Intravenous Needles Intramuscular Needles Subcutaneous Needles |

||

| By Material | Glass Needles Plastic Needles Stainless Steel Medical Needles Polymer/Polyetheretherketone (PEEK) Needles |

||

| By Application | Diagnostic Applications Therapeutic Applications |

||

| By End User | Hospitals & Clinics Diagnostic Centers Home Healthcare Other End Users |

||

- Needle Market, by Region

- North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America) - Needle Market, Key Players

- Becton, Dickinson and Company

- Braun Melsungen AG

- Terumo Corporation

- Nipro Corporation

- Cardinal Health

- Smiths Medical

- Medtronic

- Novo Nordisk

- Johnson & Johnson

- Boston Scientific

- Stryker Corporation

- Cook Medical

- Teleflex Incorporated

- ICU Medical

- Ypsomed Holding AG

- WEGO Group

- KDL Group (Kangde Lai Medical Devices)

- Artsana Group

- Hamilton Company

- Retractable Technologies

- Owen Mumford Ltd

- Vygon Group

- Baxter International

- Olympus Corporation

- Thermo Fisher Scientific

- Embecta Corp.

- SOL‑Millennium Medical Group

- UltiMed Inc.

- Hindustan Syringes & Medical Devices

- Argon Medical Devices