Metal Pipe Market Size by End Use Industry, Material, Diameter, Pressure Ratings, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2034

Overview

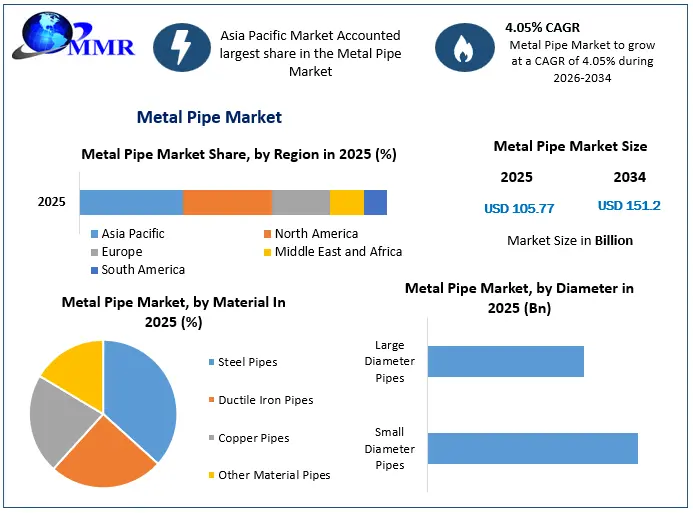

Metal Pipe Market is expected to reach US$ 151.2 Bn. in 2034, with a CAGR of 4.05% for the period 2026-2034, because of the growing demand from oil & gas industry.

Metal Pipe Market Overview:

One of the major development drivers for the market is the increase in oil & gas production due to demand from the transportation industry. Steel pipes and tubes are mostly used in the oil & gas industry. In this industry, steel pipes are utilised to transfer gas and liquid. Low alloy or carbon steel is commonly used in pipe construction. When choosing pipes for specific purposes, inner diameter, ductility, yield strength, and pressure rating are some of the most important elements to consider. Steel pipes and tubes are used extensively in the oil & gas business in the United States. The product is utilised in crude oil processing upstream, midstream, and downstream. Due to changes in the oil & gas industry in the United States, the market is expected to rise steadily over the forecast period.

Metal Pipe Market Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Latest Pipe Support Trends and the Industry’s Top Innovations:

Advances in Composite Pipe Supports

Dissimilar Metal Corrosion: Galvanic corrosion can be accelerated and pipes can be destroyed when two dissimilar metals with distinct chemical characteristics are linked. Manufacturers can isolate metals that would otherwise create destructive reactions by lifting pipes off metal surfaces using a nonmetallic support, such as a composite pipe shoe.

Surface Abrasion: Abrasion damage can now be reduced by using advanced composite pipe supports. They elevate pipes off hard surfaces and cushion hefty pipes while they move. ProTek Composite Wear Pads, which lie directly on a pipe and protect its surface, are one popular trend. At the same time, composite pipe shoes, such as ProTek Composite Pipe Shoes and CryoTek Pipe Shoes, expand on this concept. These pipe shoes are designed to withstand heavy weights and elevate pipes without the need of metal.

A Renewed Focus on Corrosion Resistance

Corrosion is not a new issue. Pipeline corrosion costs $9 billion a year in North America, according to the American Galvanizers Association. Manufacturers, on the other hand, are coming up with new ways to combat corrosion.

Advances in Friction Reduction: Corrosive compounds can take advantage of even minor scratches on metallic surfaces to slip in, cause damage, and spread. Advanced manufacturers are employing cutting-edge technologies to prevent these issues from occurring in the first place. Supports, for example, are treated with thermoplastic coatings or sophisticated linings to reduce friction, wear, and corrosion.

Controlling Movement : Because the pipes are loaded with rushing gases and liquids, movement is unavoidable. Pipes can collide with objects, rupture, or erode if they are not properly regulated. This undesirable movement is being stopped by innovative pipe restrictions. For example, VibraTek Hold Down Clamps, allow pipes to move naturally along an axis without jumping up and down. This not only decreases the risk of fractures, but it also prevents point-loading by dispersing stress.

Protective Coatings : Pipes must still contend with tough environmental conditions even when there is no friction or worn patches. Pipes can be corroded by salty air, chemicals, moisture, and bacteria. Thus, manufacturers are using chemical-resistant finishes, improved sealants, and waterproof coatings to protect metals from corroding.

Oil & Gas segment led the Metal Pipe Market

In 2025, the oil & gas segment dominated the market, accounting for almost 52% of global revenue. Because of the varied applications of the goods in the oil & gas sector, spanning from OCTG, transportation, and process pipes for refining crude oil into petroleum products, the segment is expected to maintain its leadership position during the estimated period (2026-2034).

From 2025 to 2034, the chemicals & petrochemicals segment is expected to grow at a CAGR of 5.01 percent in terms of volume. Steel pipes and tubes are increasingly being used in petrochemical plants for process refining because of their properties such as high corrosion and oxidation resistance. They can also endure varied levels of pressurisation.

Rapid industrialization and urbanization, rising population, and manufacturing sector expansion, particularly in emerging countries, are expected to boost the construction industry's growth. Therefore, product demand is expected to rise. The global top construction markets are China, India, and the United States.

Indian Steel Pipe Market Outlook

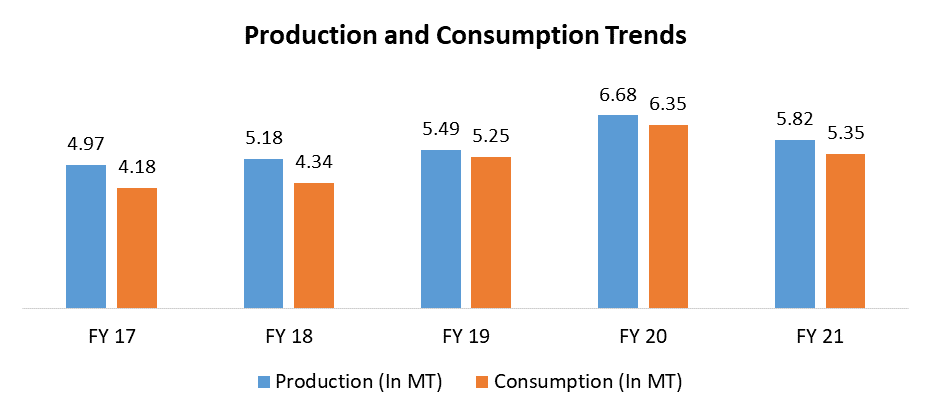

With a market value of approximately Rs.60, 000 crore, India's iron and steel pipe and tube business accounts for roughly 8% of the worldwide steel pipe market. Production increased at a CAGR of 7.7 percent for 6.68 million tonnes in FY20, because of increased demand from Jal Jeevan Mission-driven domestic water infrastructure, oil exploration, construction, infrastructure, and gas pipeline developments such as national gas grid and city gas distribution. Therefore, consumption growth exceeded output growth, growing at an annual rate of 11.03 percent in FY20.

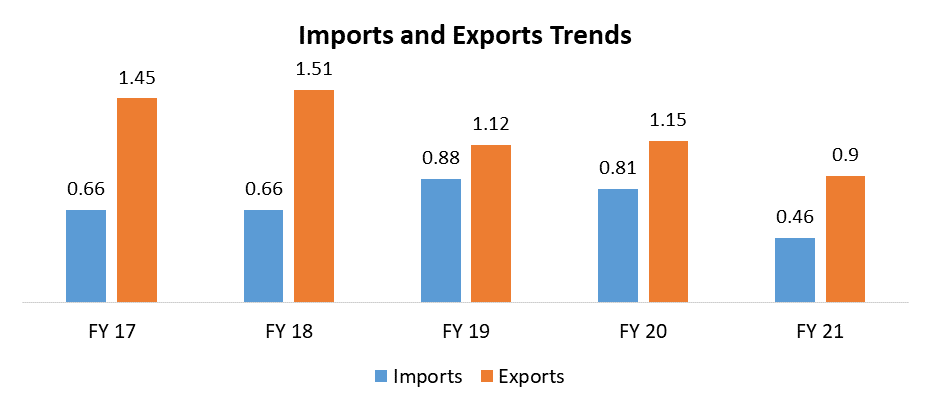

In response to rising demand and capital investment for modernization and capacity creation in end-user industries, Indian pipe and tube producers have evolved during the previous decade. Thus, steel pipe and tube producers have successfully scaled their operations to match the size of the global economy. Despite a contraction in FY20 due to reduced metal prices and volume losses because of the worldwide pandemic, domestic players' overall revenues have nearly doubled in the recent decade. India's manufactured pipes are in high demand in Europe, Thailand, Malaysia, the Middle East, and Indonesia because of their reasonable pricing, good quality, and location advantages. But, as domestic consumption grew rapidly, export volumes decreased, and the difference between exports and imports reduced over time. Moreover, Indian industry has limited capacity for high-temperature-resistant pipes needed in drilling and oil exploration, which are often imported by India's oil refineries. Pipe imports increased in FY19 and FY20 due to increased refining capacity and a renewed focus on oil exploration by the government of India to cut the country's crude oil import bill.

India's manufactured pipes are in high demand in Europe, Thailand, Malaysia, the Middle East, and Indonesia because of their reasonable pricing, good quality, and location advantages. But, as domestic consumption grew rapidly, export volumes decreased, and the difference between exports and imports reduced over time. Moreover, Indian industry has limited capacity for high-temperature-resistant pipes needed in drilling and oil exploration, which are often imported by India's oil refineries. Pipe imports increased in FY19 and FY20 due to increased refining capacity and a renewed focus on oil exploration by the government of India to cut the country's crude oil import bill. The objective of the report is to present a comprehensive analysis of the global Metal Pipe market to the stakeholders in the Process. The past and current status of the Process with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the Process with a dedicated study of key players that include market leaders, followers, and new entrants.

The objective of the report is to present a comprehensive analysis of the global Metal Pipe market to the stakeholders in the Process. The past and current status of the Process with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the Process with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the Process to the decision-makers.

The report also helps in understanding the Metal Pipe dynamics, structure by analyzing the market segments and projecting the Metal Pipe size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the global Metal Pipe market make the report investor’s guide.

Metal Pipe Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 June 2025 | GAIL (India) Limited | Approved an investment of USD 100 million to expand the Dahej–Uran–Dabhol–Panvel natural gas pipeline. | Strengthens gas transmission networks and enhances national energy security in India. |

| 12 July 2026 | ArcelorMittal | Announced a price increase of €50 per tonne for rolled steel products across Europe. | Reflects rising operational costs and aims to preserve margins amidst market volatility. |

| 24 February 2026 | BS Pipe | Expanded manufacturing capacity for premium MS pipe products in Chhattisgarh. | Enhances local supply chain efficiency and meets rising demand from regional industrial sectors. |

| 01 June 2026 | Salzgitter AG | Reached a definitive agreement to acquire full control of Hüttenwerke Krupp Mannesmann. | Consolidates market position and streamlines production of high-quality pipe-grade steel. |

Metal Pipe Market Scope: Inquire before buying

| Metal Pipe Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 105.77 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.05% | Market Size in 2034: | US $ 151.2 Bn. |

| Segments Covered: | by End Use Industry | Oil and Gas Potable Water Wastewater Power Generation Automotive HVAC and Electrical Others |

|

| by Material | Steel Pipes Ductile Iron Pipes Copper Pipes Other Material Pipes |

||

| by Diameter | Small Diameter Pipes Large Diameter Pipes |

||

| by Pressure Ratings | Less than 300 psi Pressure Pipes 300-1000 psi Pressure Pipes 1000-3000 psi Pressure Pipes More than 3000 psi Pressure Pipes |

||

Metal Pipe Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Metal Pipe Market, Key Players are:

1. Tenaris

2. Vallourec

3. TMK Group

4. ArcelorMittal

5. Nippon Steel Corporation

6. JFE Steel Corporation

7. Salzgitter Mannesmann

8. United States Steel Corporation

9. Tata Steel

10. JSW Steel

11. Steel Authority of India Limited (SAIL)

12. Jindal SAW Ltd

13. APL Apollo Tubes Ltd

14. Maharashtra Seamless Ltd

15. Mueller Industries

16. Kaiser Aluminum

17. Amiantit

18. Northwest Pipe Company

19. POSCO

20. SeAH Steel

21. Man Industries (India) Ltd

22. Surya Roshni Ltd

23. Zenith Steel Pipes & Industries Ltd

24. Hi-Tech Pipes Ltd

25. Jindal Stainless Limited (JSL)

26. Benteler Steel/Tube

27. H. Butting GmbH & Co. KG

28. Voestalpine Tubulars

29. Baoshan Iron & Steel Co., Ltd. (Baosteel)

30. Zhejiang Jiuli Hi-Tech Metals

Frequently Asked Questions:

1. Which region has the largest share in Metal Pipe Market?

Ans: The Asia Pacific held the largest share in 2025.

2. What is the growth rate of the Metal Pipe Market?

Ans: The Metal Pipe Market is growing at a CAGR of 4.05% during the forecasting period 2026-2034.

3. What segments are covered in the Metal Pipe Market?

Ans: Metal Pipe Market is segmented into Mesh Size, Material, Application, Process, and Region.

4. Who are the key players in the Metal Pipe Market?

Ans: The important key players in the Metal Pipe Market are – ArcelorMIttal S.A., Compagnie de Saint-Gobain SA, Kaiser Aluminum Corporation, Northwest Pipe Company, Saudi Arabian Amiantit Company, Muller Industries, Inc., Narsk Hydro ASA, Nippon Steel and Sumitomo Metals, TMK Group, Tenaris SA, Hebei Iron & Steel Group, Baosteel, Wuhan Iron & Steel Group, Vallourec, United States Steel Corporation, Amiantit, and Others.

5. What is the study period of this Market?

Ans: The Metal Pipe Market is studied from 2020 to 2034.