Lead Market by Type, Application and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

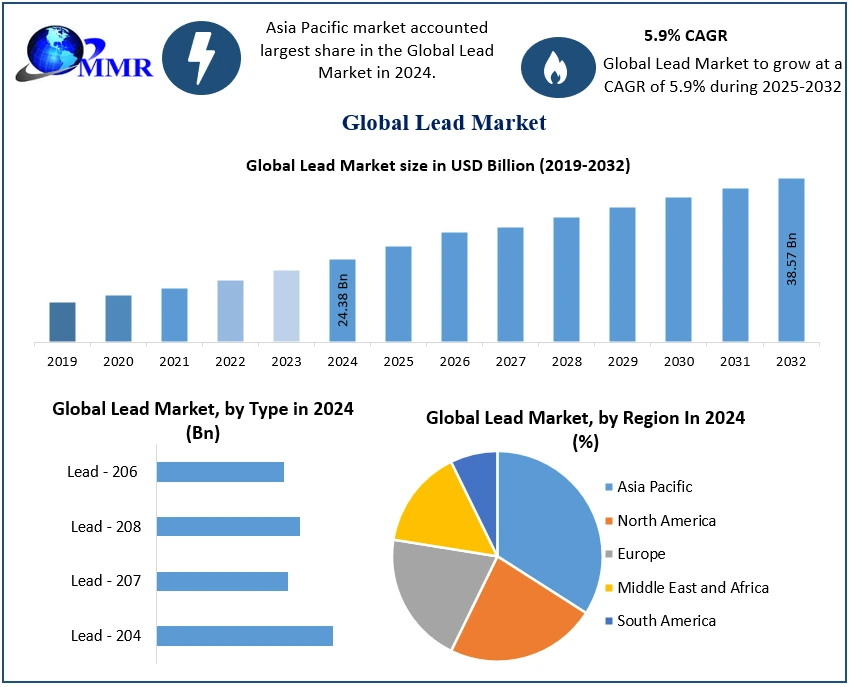

The Lead Market size was valued at USD 24.38 Billion in 2024 and the total Lead revenue is expected to grow at a CAGR of 5.9% from 2025 to 2032, reaching nearly USD 38.57 Billion.

Lead Market Overview:

Lead, is soft in nature is obtained naturally, and profusely originated from the earth. Lead is very dense, ductile, and flexible and is a poor conductor of electricity. Lead is documented as the oldest metal, also it is extremely long-lasting and owns the anti-corrosion property. Lead production, primarily sourced from lead ore and recycling, is essential for applications in the automotive sector, construction, ammunition, and electrical equipment. The automotive industry, relying heavily on lead-acid batteries, remains a dominant consumer of lead. The Lead Market faces ongoing challenges due to environmental and health concerns related to lead toxicity, leading to stringent regulations and a push for cleaner production methods and recycling. The shift towards electric vehicles (EVs) and the adoption of alternative battery technologies reshape the Lead Market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Lead Market Dynamics

Rising Battery Industry boosts the lead Market Growth

The surging battery industry is significantly influencing the lead market's growth. Lead-acid batteries, distinguished by their reliance on lead plates and sulfuric acid electrolytes, assume a pivotal role across various sectors, encompassing the automotive industry, renewable energy storage, and backup power systems. The burgeoning electric vehicle (EV) market, combined with the escalating requirement for efficient energy storage solutions within the automotive sector, has precipitated a notable surge in the demand for lead. Concurrently, renewable energy sources such as solar and wind power, characterized by their inherently intermittent nature, precipitate the imperative need for energy storage.

Within this context, cost-effective and dependable lead-acid batteries have effectively addressed the niche demand for surplus energy storage. The critical function of Uninterruptible Power Supplies (UPS) systems in providing backup power during outages relies on lead-acid batteries, further solidifying their importance. The lead industry's strong link to recycling serves as a strong driver of growth. The recycling of spent lead-acid batteries is integral to sourcing lead for the production of new batteries. Environmental regulations and the emergence of new markets are significant factors influencing the lead-acid battery demand. In regions where affordable energy storage solutions are imperative, this demand is on the rise.

Growth of the Automotive Industry Acts as a Prominent Driving Force for Increased Lead Market Demand.

The automotive industry, comprising the conception, manufacturing, and marketing of motor vehicles, which includes passenger cars, trucks, and commercial vehicles, holds a pivotal global economic position. It assumes a crucial role in diverse economies, contributing substantially to employment, financial gains, and technological progress on a worldwide scale. Significantly, the sector is presently undergoing a notable transformation, driven by several critical factors. Technological advancements have given rise to electric vehicles (EVs), autonomous driving technology, and heightened safety features, thereby instigating a revolution in our perception of transportation.

Simultaneously, concerns about environmental impacts have prompted a shift towards environmentally sustainable vehicles, compelling automobile manufacturers to invest in electric and hybrid alternatives. Supply chain disruptions, especially regarding semiconductor shortages, have impacted production capabilities. Changing consumer preferences have emphasized sustainability, connectivity, and advanced tech features. Government regulations around safety, emissions, and electrification are influencing automakers' strategies. Intense competition and mergers are reshaping the industry landscape. In essence, the automotive industry is evolving rapidly to meet these challenges and capitalize on opportunities for growth, innovation, and sustainability. For example, according to the MMR Study Report, the positive state and central government helped to accelerate the demand for E-cars in India in the year 2022.

Environmental and Health Concerns Associated With Lead Exposure Limits the Lead Market Growth

Lead, recognized as a hazardous substance, has faced scrutiny for its utilization in various applications, particularly those entailing direct human interaction or environmental exposure. The potential detrimental consequences on health and the environment have prompted regulatory agencies and governments in numerous nations to enact rigorous regulations governing lead use. Consequently, certain applications have encountered restrictions and phase-out measures. Mandates requiring the diminution of lead content in diverse products and materials, including paints, pipes, and specific electronics, have been enforced to mitigate the potential hazards associated with lead poisoning and environmental contamination. The awareness of these risks and the associated legal restrictions have led to the development of lead-free alternatives and increased efforts in lead recycling and disposal management. These factors collectively serve as significant restraints on the lead market, affecting its growth and necessitating the industry's adaptation to evolving regulatory landscapes and consumer expectations.

Technological Advancement Creates Lucrative Growth Opportunities for the Market Growth

Technological advancements have significantly reshaped the lead market, offering a multitude of lucrative growth opportunities. Lead, a versatile metal, is benefiting from these advancements in several key ways. Battery technology, for instance, has witnessed substantial progress, with lead-acid batteries undergoing continuous improvements in energy density, cycle life, and charge/discharge efficiency. This progress makes them more competitive and appealing in various applications, including automotive, uninterruptible power supplies (UPS), and renewable energy storage.

Furthermore, the development of innovative recycling processes and automated sorting systems has made lead recycling more efficient and eco-friendly, aligning with the growing global focus on sustainability. Stringent environmental regulations have also driven the industry toward cleaner and more sustainable lead production and recycling methods. Beyond batteries, lead-based alloys have seen advancements tailored to specific applications, such as the automotive sector, where lead contributes to increased strength, corrosion resistance, and overall performance. In addition to these applications, the medical field benefits from lead's high density, which makes it ideal for X-ray shielding and radiation protection. The continued development of medical imaging technologies and radiation therapy is expected to drive the demand for lead-based products in healthcare.

The miniaturization of electronic devices continues to rely on lead, commonly used in solder for assembling microelectronic components. As technology evolves, demand for high-quality lead-based solders persists. The construction and infrastructure sectors also contribute to lead market growth, particularly in applications such as roofing and waterproofing. Research and development efforts have unveiled new applications for lead in advanced ceramics and superconductors, further expanding the scope of lead's use in specialized niches. The growth of data centers worldwide, driven by the demand for cloud computing and digital Applications, necessitates reliable backup power systems and UPS solutions, where lead-acid batteries play a pivotal role, thereby sustaining the demand for lead. In the automotive industry, lead remains relevant in the manufacturing of lead-acid batteries, especially for vehicles with start-stop systems and auxiliary power requirements, ensuring a consistent market demand. However, it's crucial to recognize that the lead industry must also address environmental concerns and regulatory challenges to secure long-term growth and sustainability.

Lead Market Segment Analysis:

Based on Application, The batteries segment dominated the Lead Market in the year 2024. Lead-acid batteries serve various purposes, including starting, lighting, and ignition applications, stationary uses such as telecom, UPS, and energy storage systems, portable devices including consumer electronics, and more. Sealed Lead-Acid (SLI) batteries play a pivotal role in automotive applications, where they are integrated with the vehicle's charging system, resulting in a continuous process of charging and discharging during the vehicle's operation.

The expansion of the SLI battery market is primarily steered by the increasing need for batteries that provide exceptional performance, extended lifespan, and cost efficiency, particularly to initiate engines, illuminating lights, powering ignition systems, or other internal combustion engines. In conventional combustion engine vehicles such as cars and trucks, lead-acid batteries remain the preferred technology for all SLI battery applications.

Lead Market Regional Insight:

Asia Pacific region dominated the global Lead Market in 2024. China stands as a global leader in both lead production and consumption, driven by its automotive industry and manufacturing sector. The United States follows suit, heavily reliant on lead-acid batteries in the automotive domain and influenced by stringent environmental regulations that promote recycling and emissions reduction.

In the European Union, environmental policies play an essential role, fostering a strong emphasis on sustainable lead production and responsible usage. India experiences a burgeoning lead market due to a growing automotive and construction sector, increasing the demand for lead-acid batteries. Australia contributes significantly to global lead supply as a producer and exporter of lead concentrates. Latin American countries, particularly Peru, hold prominence as vital contributors to the global lead production landscape. Recycling centers for lead-acid batteries, scattered worldwide, further underpin sustainability efforts.

Lead Market Scope: Inquiry Before Buying

| Lead Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 24.38 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.9% | Market Size in 2032: | USD 38.57 Bn. |

| Segments Covered: | by Type | Lead - 204 Lead - 207 Lead - 208 Lead - 206 |

|

| by Application | Bullets and Shots Ammunition Construction Plumbing Electronics Batteries Solders Marine Others |

||

Lead Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Lead Key Players

1. Gravita Metals

2. Glencore

3. Teck Resources Limited

4. Canada Metal North America Ltd.

5. KOREAZINC

6. Vedanta Resources

7. EnerSys Inc Global Metals

8. Johnson Control Inc

9. M.A. Metal

10. KOREAZINC

11. MMG

12. South32

13. Nyrstar

FAQs

1] What segments are covered in the Global Lead Market report?

Ans. The segments covered in the Lead Market report are based on Isotope, Application and Region.

2] Which region is expected to hold the highest share of the Global Lead Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Lead Market.

3] What is the market size of the Global Lead Market by 2032?

Ans. The market size of the Lead Market by 2032 is expected to reach USD 38.57 Bn.

4] What was the Global Lead Market size in 2024?

Ans: The Global Lead Market size was USD 24.38 Billion in 2024.

5] Who are the Key players in the Lead Industry?

Ans. Key players in the Global Lead Market are Gravita Metals, Glencore, Teck Resources Limited, Canada Metal North America Ltd., KOREAZINC, Vedanta Resources, and others.