Inverter Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2034

Overview

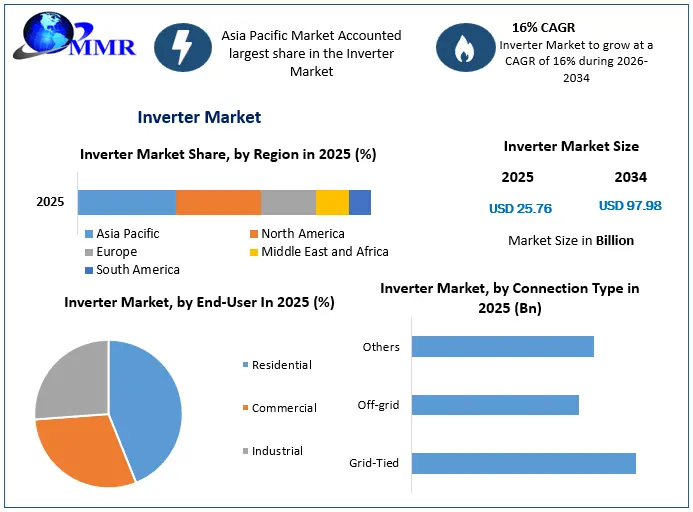

The Inverter Market size was valued at USD 25.76 Billion in 2025 and the total Inverter revenue is expected to grow at a CAGR of 16% from 2026 to 2034, reaching nearly USD 97.98 Billion.

Inverter Market Overview:

An inverter is a device that converts direct Current (DC) power into alternating contemporary (AC) energy. The conversion is critical in diverse programs, inclusive of renewable power structures, uninterruptible strength materials (UPS), and electric-powered automobile powertrains. The function of an inverter is to supply AC power. The need for uninterrupted and reliable power supply in residential, commercial, and industrial sectors boosts the Inverter Market. Technological advances such as the development of smart inverters with grid-support functionality and improved performance are driving the Inverter market growth. Key players in the inverter industry include SMA Solar Technology AG, ABB Limited, Huawei Technologies Co., Ltd., Enphase Energy, Inc. and others. A major focus of inverter manufacturers has been on increasing power density, which allows more power to be produced from a smaller, lighter device. It is achieved through improvements in switching topologies and semiconductor materials. Transistors have been primarily made of silicon MOSFET (metal oxide semiconductor field-effect transistor) and IGBT (insulated-gate bipolar transistor.) India exports most of its Inverter batteries to Bangladesh, Nigeria, and Lebanon and is the 2nd largest exporter of Inverter batteries in the World. The top 3 exporters of Inverter batteries are China with 3,160 shipments followed by India with 1,908 and Vietnam at the 3rd spot with 567 shipments.

1. Inverter exports in October 2023 were 3.1107 million units, down 28.7% YoY and 20.4% MoM. Conversely, imports hit 2.271 million units, up 0.7% YoY and 21.9% MoM. Cumulative exports from January to October 2023 rose 12.66% YoY.

2. In October 2023, inverters were exported to 184 countries. Europe received 539,800 units, 17.35% of total exports, down 43.86% MoM. Africa got 748,000 units, 24.05% of total exports, down 25.2% MoM. The top ten countries took in 1.2523 million inverters, 40.26% of total exports.

Inverter Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

Inverter Market Dynamics:

Renewable Energy, Technological Innovations, and Demand of the Inverter Market

Rising need for renewable energy, technological progress, and growing demand for uninterrupted power supply are fuelling the growth of the Inverter Market. Inverters are vital for the conversion of DC power from sources like solar panels and batteries into internal AC power for grid or standalone use. The commercial and industrial sectors are seeing a rise in the use of solar energy systems owing to the demand for dependable and effective energy management solutions.

Inverters used by automotive & residential end users are easy to use and install. The inverters procured are mostly installed by end users themselves. Factors like increasing global electric vehicle production & rise in the adoption of microinverters & hybrid inverters that are integrated with small or medium-sized rooftop solar installations by the residential and commercial end users contribute to the growth of the inverter market through the forecast period.

In addition, Government policies and incentives, such as updated standards such as IEEE 1547 and UL 1741, mandate the use of advanced inverters, increasing the demand. Various forms of energy are stored through power generation new hybrid systems that integrate multiple energy sources such as solar and wind. It is necessary to use an inverter with multiple-maximum-power-point monitors (MPPT) to monitor the inputs properly. Environmental benefits of renewable energy, such as reduced greenhouse gas emissions and air pollution, and decreased energy costs are factors that drive Inverter Industry growth. Renewable Energy System also improves independence, which makes it attractive for remote, coastal, or isolated communities.

operational Challenges and Economic Barriers in the Inverter Market

Regular maintenance and scheduled replacements are essential to guarantee that these systems operate correctly, leading to higher overall operating expenses. Proficient technicians are needed to address all technical issues that arise, as any error leads to extensive periods of inactivity, impacting energy generation and financial success, and hindering the growth of the Inverter Market. Ensuring that all components, such as solar panels and air conditioners, work harmoniously with a sophisticated inverter in renewable energy systems involves thorough testing and adjustment, which is both expensive and time-consuming. Additionally, longer payback periods affect the adoption rate among residential and small commercial users.

| Emerging Opportunities in the Inverter Market Amidst Renewable Energy Growth |

| The increasing use of battery storage systems in renewable energy setups presents opportunities for inverters that efficiently manage and convert stored energy. |

| The continuous increase in solar and wind energy projects provides significant opportunities for inverter manufacturers to supply essential components for these installations. |

| Development of new inverter technologies, such as multi-level inverters, improve efficiency and reliability, attracting more customers. |

| The growing trend of smart grid technology offers opportunities for inverters with advanced communication and control features. |

| The rapid increase in electric vehicle adoption creates a growing need for inverters in EV charging stations. |

| Inverters enable V2G technology, allowing EVs to supply power back to the grid, creating new revenue streams. |

| Supportive policies and incentives for renewable energy adoption in various countries boost the demand for inverters. |

Inverter Market Segment Analysis:

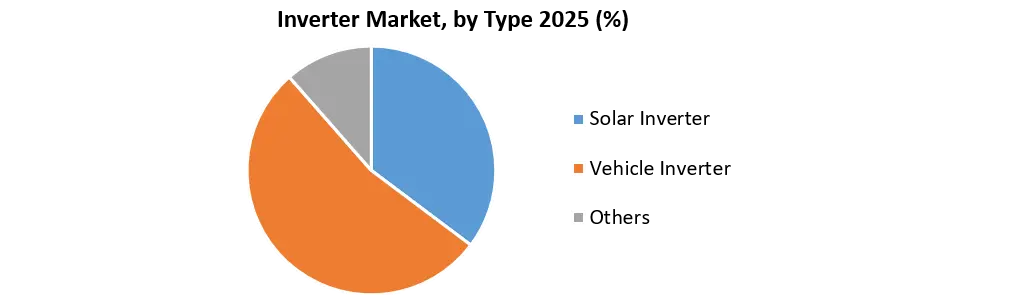

Based on the Type, the market is segmented into the Solar inverter, Vehicle Inverter and Others. Solar inverter is expected to dominate the inverter Market during the forecast period. Solar Inverters are further categorized into String Inverters, Central Inverters Microinverters and Others. As the world increasingly holds solar energy to mitigate climate change and reduce reliance on fossil fuels, the demand for solar power systems has increased, resulting in a corresponding increase in the need for efficient solar inverters. These help to convert the direct current (DC) generated by solar panels into alternating current (AC), which is compatible with the electrical grid and power homes, businesses, and industries. Their significance is improved by technological advancements that have enhanced efficiency, reliability, and cost-effectiveness, making solar inverters more available to a broader range of consumers.

The government incentives and policies encouraging renewable energy adoption have catalyzed the Inverter Market growth. Many countries are implementing subsidies, tax credits, and feed-in tariffs to promote solar installations, thereby increasing the demand for solar inverters. The increase in smart grid technology and energy management systems has also contributed to the prominence of solar inverters, as these devices integrate seamlessly with smart technologies, enabling better energy management and consumption tracking.

Inverter Market Regional Insight:

Asia Pacific held the largest market share in 2025 for the Inverter Market. The rapid growth of industries and urban areas in nations such as China, India, Japan, and South Korea is increasing the need for energy, leading to a required transition to more effective and eco-friendly energy choices. China's substantial investments in renewable energy have propelled it to become the world's leading producer of solar panels and wind turbines.

The Asia Pacific's domination has been strengthened by advancements in technology and the participation of Inverter market leaders. The area houses numerous top inverter manufacturers that continuously innovate, providing affordable solutions to match Inverter market demands. The area earns the advantages of economies of scale, such as extensive manufacturing and cost-efficient exports, that fuel the growth of the Inverter Market. Advancements in smart grid technology and energy storage investments in nations like South Korea and Australia drive the demand for advanced inverters, as well as enhance solar inverters Industry share through favourable weather conditions like sunlight. The domestic market for solar inverters has been growing with the rapid rise in solar deployment across all end-user segments. As domestic electricity prices have risen, many consumers in off-grid or remote areas with unreliable electricity supply have opted for solar inverters for backup. India has set a target of 175 GW of non-fossil fuel capacity by 2022 and a target of 500 GW of non-fossil fuel capacity by 2032; the government has been rapidly increasing the installed capacity base, especially solar.

North America held xxx% share in 2025 for the Inverter Market. In the region, the government has introduced several new incentive programs to encourage the use of solar and other renewable technologies. In August 2022, the U.S. government initiated the Inflation Reduction Act, dedicating USD 369 billion to support the renewable energy industry. Numerous companies are now building new solar photovoltaic plants and expanding the capacities of their current plants. In February 2023, Silicon Ranch declared its plans to boost the energy generation capacity of its solar power plant. First Solar has secured a deal to provide 1.5 GW of innovative American thin-film solar modules, on top of existing contracts totaling 4 GW of solar PV panels to be installed by 2027.

1. The top 3 importers of Power inverters are Vietnam with 21,276 shipments followed by Russia with 7,989 and India at the 3rd spot with 7,799 shipments.

2. India imports most of its Power inverters from China, Germany, and Japan and is the 3rd largest importer of Power inverters in the World.

Inverter Market Recent Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 12 January 2026 | Enphase Energy | The company officially began U.S. production shipments of its IQ9N-3P™ Commercial Microinverter using gallium nitride (GaN) technology. | Delivers industry-leading 97.5% efficiency and simplifies 480V commercial project installations without requiring external transformers. |

| 28 January 2026 | SMA Solar Technology | Expanded its partnership with CEP to enable domestic integration of Medium Voltage Power Station (MVPS) solutions in the United States. | Accelerates utility-scale project timelines and supports increased domestic content by localizing assembly in Little Rock, Arkansas. |

| 13 April 2026 | Enphase Energy | Announced expanded deployments of its IQ9N-3P and IQ8P-3P commercial microinverters across the United States. | Provides a scalable, all-AC architecture that eliminates high-voltage DC risks, driving adoption in commercial solar retrofitting. |

| 22 June 2026 | Huawei | Launched and received the Smarter E AWARD for its 506 kW SUN2000-506KTL Smart String Inverter at Intersolar Europe 2026. | Introduces the industry’s first 1000Vac string inverter with grid-forming capabilities to maximize power density for utility-scale solar. |

Inverter Industry Ecosystem

Global Inverter Market Scope: Inquire before buying

| Global Inverter Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 25.76 Billion |

| Forecast Period 2026 to 2034 CAGR: | 16% | Market Size in 2034: | USD 97.98 Billion |

| Segments Covered: | by Types | Solar Inverter String Inverters Central Inverters Microinverters Others Vehicle Inverter Others |

|

| by Output Power Rating | Below 10 kW 10–50 kW 51–100 kW Above 100 kW |

||

| by Connection Type | Grid-Tied Off-grid Others |

||

| by End-User | Residential Commercial Industrial |

||

Global Inverter Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Inverter Market, Key Players:

1. Solar Edge Technologies (Milpitas, California, USA)

2. SunPower Corporation ( San Jose, California, USA)

3. Schneider Electric (Andover, Massachusetts, USA)

4. General Electric (GE Renewable Energy)

5. TBEA Sunoasis Co., Ltd. (Urumqi, China)

6. Sungrow Power Supply Co., Ltd. v Hefei, China)

7. Huawei Technologies (Shenzhen, China)

8. SMA Solar Technology AG (Niestetal, Germany)

9. Fronius International GmbH (Pettenbach, Austria)

10. ABB (Zurich, Switzerland)

11. Ingeteam (Zamudio, Spain)

12. Siemens (Munich, Germany)

13. Kostal Solar Electric (Freiburg, Germany)

14. FIMER (Terranuova Bracciolini, Italy)

15. Delta Electronics (Hoofddorp, Netherlands)

16. Kaco New Energy (Neckarsulm, Germany)

17. Enphase Energy (Petaluma, California, USA)

18. Trina Solar Limited (Changzhou, China)

19. Risen Energy Co., Ltd. (Ningbo, China)

20. GCL-Poly Energy Holdings Limited (Jiangsu, China)

21. Victron Energy (Almere, Netherlands)

FAQs:

1] What is the growth rate of the Inverter Market?

Ans. The Global Inverter Market is growing at a significant rate of 16 % during the forecast period.

2] What is the expected Inverter market size by 2034?

Ans. The Inverter Market size is expected to reach USD 97.98 Billion by 2034.

3] What segments are covered in the Inverter Market report?

Ans. The segments covered in the market report are Types, Connection Types, and End-users.

4] What are the factors driving the Inverter Market growth?

Ans. Rising need for renewable energy, technological progress, and growing demand for uninterrupted power supply are fuelling the growth of the Inverter Market.

5]Which are the top Key Players in the Inverter Market?

Ans. The major players in the Inverter market are Huawei Technologies Co., Ltd. (China), SUNGROW (China), SMA Solar Technology AG (Germany), Power Electronics S.L. (Spain), and Fimer Group (Italy).