Industrial Vehicles Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

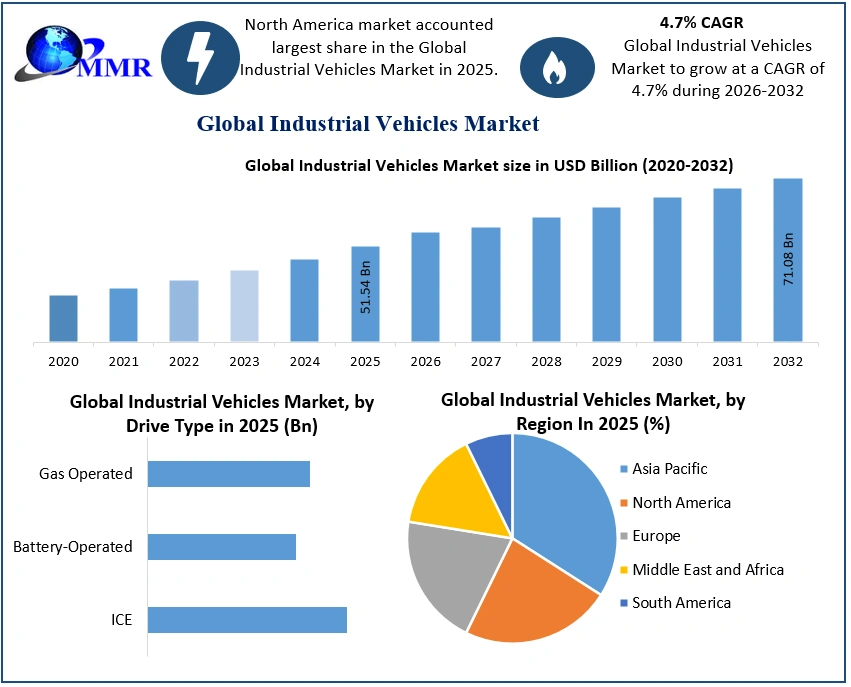

The Industrial Vehicles Market size was valued at USD 51.54 Billion in 2025 and the total Industrial Vehicles revenue is expected to grow at a CAGR of 4.7% from 2025 to 2032, reaching nearly USD 71.08 Billion by 2032.

Market Overview:

Industrial vehicles are designed to transport products and processing equipment to storage locations for raw materials and manufactured items as well as warehouse distribution centres. This industrial vehicle is designed to attach specialized heavy equipment vehicles and is available in a range of sizes. Due to their affordability, compactness, environmental friendliness, dependability, and efficiency, battery-operated industrial vehicles are now becoming more and more popular compared to those powered by internal combustion engines and gas.

As the need for battery-powered industrial vehicles increases and smart factories join the material handling sector, the industry is expected to have new growth opportunities. Companies in the industrial vehicle sector are concentrating on the development of innovative products, particularly electric industrial vehicles. For example, Clark expanded its selection of industrial lift trucks in February 2023 by introducing the new TWLi20 three-wheel electric lithium-ion driven lift truck.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Industrial Vehicles Market Dynamics:

e-commerce and warehouses facility

The number of warehouses per region is rising as a result of the expanding need for them to support hub and spoke models in a variety of industries, including e-commerce, the production of automotive components, consumer products, and electronics. Over the next five years, the warehousing and fulfillment industry is expected to rise by double percentages. In the US, the penetration of e-commerce increased from around 10% of total retail sales in 2019 to over 15% in 2020. Additionally, according to the US Bureau of Labor Statistics, there were 19,194 warehouses in the US in 2020 compared to 15,255 in 2011. Over the next five years, it is expected that worldwide online e-commerce sales would more than quadruple, adding over 28,500 new warehouses to the existing stock. According to the US Commerce Department, the US is ranked number two among the top ten e-commerce nations.

Over the next five years, it is expected that international online e-trade revenue will more than double, which will allow for the addition of around 28 thousand warehouses to the global stock. There will almost certainly be a rise in demand for commercial motors as a result of the expansion of the variety of warehouses. In turn, this is likely to increase sales for the industrial vehicle market over the forecast period.

Lack of R&D facilities and strict regulations

The lack of R&D facilities and strict regulations restrict the market's growth for industrial vehicles. Industrial vehicles require a lot of R&D and creativity. OEMs must make significant R&D investments to enhance industrial vehicles' capacity to lift heavy loads and boost productivity to speed up turnaround. To stop forklifts from toppling over, sliding sideways, or dumping their load, a leading R&D facility is required. Industrial vehicles also need a lot of maintenance to function effectively. Owners of industrial vehicles must do regular inspections and preventative maintenance as a result. In order to maintain industrial vehicles in a safe working environment, a competent maintenance worker should perform this.

Government regulation

Over the past few years, industrial vehicle safety and pollution requirements have gotten stricter and more complex. Occupational Safety and Health Administration (OSHA) estimates that 1 in 6 occupational fatalities in the US is attributable to forklift incidents. Over 100 people are killed in forklift accidents each year, which has a financial impact on the industry of $135 million. According to OSHA, standardized training and safety measures might have helped prevent almost 70% of forklift incidents. In order to assure safety, the Australian government has enacted a number of significant modifications to the forklift manufacturing business. For example, it has set a 5 km/h speed restriction for reaching trucks and counterbalance forklifts. Manufacturers of forklift trucks may have difficulties as a result of the stricter emission tier slabs since they will need significant R&D expenditures to alter the vehicles' emission systems.

Industrial Vehicles Market Segment Analysis:

Based on Drive Type, based on drive type battery-operated industrial vehicles held xx% of CAGR in 2025. Industrial vehicles that run on batteries are powered by rechargeable batteries. Business cars that run on batteries have recently gained a lot of popularity. Being eco-friendly is a benefit of battery-powered engines. These engines produce lower pollutants, which makes these commercial vehicles a very inexperienced tool for warehouse and company tasks. The majority of logistics service providers worldwide are concentrating on reducing their carbon footprint. Industrial automobile manufacturers have been focused on battery-operated motors to reduce CO2 emissions as well as other exhaust pollutants.

Commercial vehicles powered by batteries have advantages in terms of energy performance. These cars use fuel that is around 75% less expensive to operate than propane. About 70% of forklifts in use in Western Europe are electric. Additionally, there are fewer moving components to maintain and repair on battery-powered industrial vehicles.

Due to their improved performance levels and great productivity, battery-operated industrial vehicles have seen a growth in demand in recent years. Additionally, compared to ICE industrial vehicles, electric industrial vehicles offer superior pollution management and are more cost-effective. Due to its compliance with Tier 4 emission standards and lack of in-plant emissions, electric lift trucks are typically preferred by end users.

The performance difference between ICE and electric trucks is also getting smaller. Players are producing eco-friendlier industrial vehicles by manufacturing them in eco-friendly factories, driven by demands for emission and energy efficiency. For instance, Nissan Forklift Corporation (US) has cut its carbon dioxide emissions by 51% whereas Toyota Industrial Equipment Manufacturing Inc. (TIEM) (Japan) has decreased its energy use by 40%. The demand for electric industrial vehicles is rising globally as a result of their higher safety and better acceleration as compared to industrial vehicles powered by internal combustion engines (ICE). The demand for electric industrial vehicles has increased in developed nations like Europe and North America.

Electric forklift demand has increased in developed nations like Europe and North America. The majority of businesses, including Toyota Material Handling, KION GROUP AG, Jungheinrich AG, Hyster-Yale Group, Inc., and others, provide electric forklifts for a range of end uses. Additionally, businesses involved in the industrial vehicle industry are concentrating on the development of innovative products, particularly electric industrial vehicles. For example, Clark increased its range of industrial lift trucks in February 2023 by introducing the new TWLi20 three-wheel electric lithium-ion driven lift truck. The new XH series 2.0t-3.5t electric forklift truck from Hangcha Group Co., Ltd. was introduced in July 2022 and uses high-voltage lithium-ion batteries. With regard to productivity, efficiency, decreased noise, and zero emissions, this vehicle performs above average.

Based on Application Type, based on application warehousing held the highest CAGR in 2023. The automotive industry highly depends on OEM supply, therefore having a functional structure helps in creating and enhancing efficiency. The majority of us think of the auto industry as a single production line that produces vehicles. Given the different components, like steering wheels and infotainment systems, it is more complicated than that.

Thus, it becomes crucial to manage the supply chain in a way that reduces mistakes and increases cost-effectiveness. For example, having key suppliers close to the company warehouse can make more effective use of company drivers, tractors, and other pieces of equipment. Keeping the last site of storage components close by can also shorten lead times and keep inventory levels low. Because it directly affects the company warehouse's production and efficiency, a good warehouse plan is essential. maintaining a degree of consistency and error-proofing to guarantee that the correct part always arrives at the correct location exactly in time.

A warehouse management system is a software that directs and coordinates a warehouse's daily activities (WMS). The WMS helps in order selection, packing, and shipping as well as receiving, placing, and packing of goods. Warehouse management may be incorporated into the enterprise resource planning system (ERP) or may be created as a separate application. Initially, basic features like storage location information were available through warehouse inventory management systems. From straightforward pick, pack, and ship capability to complex programs that organize complex interactions with material-handling systems and yard management, modern WMS offers a wide range of capabilities. Warehouse automation trends and opportunities in industrial vehicles are covered in the report.

Based on the Aerial Work Platform, the Boom lifts segment held the largest market share in 2025. Boom lifts are frequently used in a variety of construction projects, including building roads, mines, irrigation systems, urban infrastructure, airports, railroads, and ports. Due to end users' increased focus on buying old boom lifts due to the high cost of new equipment, end users tend to retain their current boom lifts rather than invest in new lifts, and the boom lift market is constrained.

Based on the Aerial Work Platform, the Boom lifts segment held the largest market share in 2025. Boom lifts are frequently used in a variety of construction projects, including building roads, mines, irrigation systems, urban infrastructure, airports, railroads, and ports. Due to end users' increased focus on buying old boom lifts due to the high cost of new equipment, end users tend to retain their current boom lifts rather than invest in new lifts, and the boom lift market is constrained.

Boom lifts come in a variety of designs, including Articulating Boom Lifts, Telescopic Boom Lifts, Straight Boom Lifts, Genie Boom Lifts, and Towable Boom Lifts. They have characteristics like a 360-degree rotating turntable and a chassis width that makes it possible to reach crowded workspaces and small industrial aisleways. Boom lifts make it easy to guide and relocate machines from the work stage forward and backward.

Scissor lifts have low costs and a higher operating efficiency owing to the compact design and ability to perform repetitive loading tasks with high speed. They are commonly employed for the positioning work of materials and vertical lifting. Their ergonomic designs help improve the productivity of workers and reduce potential workplace injuries.

Vehicle-mounted platforms include scissors as well as boom lifts, which are mounted on the vehicles. The segment is expected to grow at a CAGR of 5.8% over the forecast period. Vehicle-mounted platforms are gaining more popularity owing to their impressive durability, better accessibility, and reach, and higher safety levels as compared to conventional methods to reach heights including ropes and ladders.

Industrial Vehicles Market Regional Insights:

As a result of the region's emerging countries' rapid expansion in the car industry, Asia-Pacific is expected to have the greatest share of the global industrial vehicle market. Due to the region's fast industrialization, there is a greater demand for industrial trucks to deliver completed items and raw materials to warehouses.

The Asia Pacific area includes both industrialized countries like Japan and South Korea and growing economies like China and India. The area, which includes China and India, has among of the world's fastest-growing economies and is a major manufacturer of industrial vehicles. Due to OEMs providing not only domestic but also international demand, industrial vehicle manufacturing volumes have increased throughout the years. In order to establish themselves in this local market, major industrial vehicle manufacturers are growing in the Asia Pacific region.

For instance, the German company KION Group constructed a new forklift truck manufacturer in China in December 2022. The company's product line will be able to expand in China, the material handling equipment market that is expanding the quickest. The number of warehouses in the area has increased as a result of the expanding need for them to support the hub and spoke model in many industries. Additionally, one of the markets for industrial vehicles that are expanding the quickest in the globe is being driven by China's expanding economy.

The objective of the report is to present a comprehensive analysis of the Industrial Vehicles Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

Industrial Vehicles Market Scope: Inquire before buying

| Industrial Vehicles Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 51.54 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.7% | Market Size in 2032: | USD 71.08 Bn. |

| Segments Covered: | by Drive Type | ICE Battery-Operated Gas Operated |

|

| by Application | Manufacturing Warehousing Freight & Logistics Others |

||

| by Aerial Work Platform | Boom Lifts Scissor Lifts |

||

| by Level of Autonomy | Non/Semi-Autonomous Autonomous |

||

Industrial Vehicles Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Industrial Vehicles Market, Key Players are:

1. Crown Equipment Corporation (US)

2. Hyster-Yale Materials Handling, Inc. (US)

3. Altec Industries (US)

4. CLARK MATERIAL HANDLING (US)

5. Lonking Forklift Co., Ltd. (China)

6. EP Equipment, Ltd. (China)

7. Hangcha Group Co. Ltd (China)

8. Noblelift Intelligent Equipment (China)

9. Anhui Heli Co., Ltd (China)

10. Liuzhou LiuGong Forklift Co.,Ltd (China)

11. Hubtex Maschinenbau GmbH & Co. KG (Germany)

12. Hubtex Maschinenbau GmbH & Co. KG (Germany)

13. Jungheinrich AG (Germany)

14. Kion Group AG (Germany)

15. Mitsubishi Nichiyu Forklift Co., Ltd. (Japan)

16. Toyota Industries Corporation (Japan)

17. Aichi Corporation (Japan)

18. MORITA HOLDINGS CORPORATION (Japan)

19. Komatsu Ltd. (Japan)

20. Doosan Corporation (South Korea)

21. Hyundai Heavy Industries (South Korea)

22. Action Construction Equipment Ltd. (India)

23. Godrej & Boyce Mfg. Co. Ltd. (India)

24. Cargotec Corporation (Finland)

25. Combilift (Ireland)

26. Goldbell Group (Singapore)

27. Motrec International Inc. (Canada)

28. Manitou (France)

Frequently Asked Questions:

1. What is the forecast period considered for the Industrial Vehicles Market report?

Ans. The forecast period for the Industrial Vehicles Market is 2026-2032.

2. Which key factors are hindering the growth of the Industrial Vehicles Market?

Ans. Government regulation hinders the market.

3. What is the compound annual growth rate (CAGR) of the Industrial Vehicles Market for the forecast period?

Ans. 4.7 % of CAGR is the annual growth rate of the industrial vehicle market

4. What are the key factors driving the growth of the Industrial Vehicles Market?

Ans. Wearhouse and e-commerce are driving factors of the industrial vehicle market.

5. Which are the worldwide major key players covered for the Industrial Vehicles Market report?

Ans. Anhui Heli Co., Ltd, Crown Equipment Corporation, Hangcha Group Co. Ltd, and Toyota Industries Corporation are some of the key players covered in the report.