Hydrogen Storage Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

The Hydrogen Storage Market size was valued at USD 19.41 Billion in 2025 and the total Hydrogen Storage revenue is expected to grow at a CAGR of 7.97% from 2026 to 2032, reaching nearly USD 33.21 Billion.

Hydrogen Storage Market Overview:

Hydrogen is an energy carrier, not a fundamental source of energy. Hydrogen may be created using a wide range of fossil fuels and other main energy sources. Electrolysis may also be used to create hydrogen using electricity. Hydrogen can help to address a variety of key energy concerns since it is utilized to decarbonize a variety of industries including transportation, iron and steel, and chemicals. It can aid in the fluctuating production of renewables like solar photovoltaic and wind power. Hydrogen is one of the greatest solutions for storing renewable energy and is positioned to become the most cost-effective option for storing significant amounts of power over longer periods of time. Meanwhile, water electrolysis is the most adaptable and long-term alternative for storing renewable energy on a wide scale.

The increasing consumption of renewable energy to offset rising GHG emissions is expected to raise demand for an energy storage system. Additionally, favorable government regulations and initiatives aimed at reducing carbon emissions are expected to drive the hydrogen storage market throughout the forecast period. For example, on May 10, the United Kingdom government announced a $2.21 million investment to build an extra 100 hydrogen fuel cell vehicles and vans over the next few years. In addition, stringent pollution rules in China, South Korea, Japan, and India, as well as rising demand for ammonia and methanol, are expected to drive the hydrogen storage market growth. As a result, with increased government measures to promote the use of hydrogen storage technologies, the hydrogen storage market has a high growth potential during the forecast period.

One of the most recent trends in the hydrogen storage industry is an increased emphasis on research and development (R&D) for the development of hydrogen storage technology, as well as an increase in the use of hydrogen storage in solid form. The United States, the United Kingdom, India, and others have placed a high priority on R&D for technical improvements in hydrogen and fuel cell technology. The National Renewable Energy Laboratory (NREL), for example, is working with the US Department of Energy to develop cost-effective, high-performance fuel cells and hydrogen technologies for transportation and portable power applications.

In recent years, there has been a growth in the adoption of hydrogen storage in the transportation industry. This is due to its use in powering fuel cell cars due to its great storage performance and inexpensive cost. Additionally, according to the World Nuclear Association, the need for hydrogen in the generation of transport fuels from crude oil is expected to grow rapidly by 2032, driving the growth of the hydrogen storage market. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Hydrogen Storage Market Dynamics:

Large-scale applications of hydrogen across various industries

Hydrogen is widely utilized in many industrial sectors, including oil, chemicals, food, plastics, metals, electronics, glass, and power generation. However, with the increased need to minimize carbon emissions, hydrogen is being utilized in new and interesting ways to manufacture both old and new products. Hydrogen may also be utilized in large-scale energy conversion applications, such as direct combustion in internal combustion engines or fuel cells in the automotive industry. The major benefits of combustion engines over fuel cells are their lower cost and less severe purity requirements for hydrogen. Another potential new application is the production of concrete, which is a very carbon-intensive process that is ripe for decarbonization using hydrogen.

| Industry | Uses |

| Metals | Heat treatment to improve ductility and machining quality, increase the tensile strength, relieve stress, and harden, changing electrical or magnetic characteristics. Welding torches, Oxygen scavengers, The reductive atmosphere for the production of iron, molybdenum, etc. |

| Plastics | It is cracking used plastics to produce lighter molecules that can be recycled. Synthesize nylons, polyesters, polyurethane, and polyolefin. |

| Glass | Heat treatment of optical fibers.

The reductive atmosphere for the float glass process. High-temperature cutting torches, Glass polishing. |

| Electronics | Heat bonding materials.

Epitaxial growth of polysilicon. Manufacture of vacuum tubes. |

| Electric power | Nuclear fuel processing Coolant for large generation of motors. |

| Food | Conversion of edible oils to fats.

Conversion of tallow and grease to animal feed. Conversion of sugar to polyols. |

| Oil | Hydrocracking of large hydrocarbons to fuel distillates.

Removal of sulfur and other impurities. |

As the result, the increasing demand for hydrogen across various industries driving the hydrogen storage market during the forecast period.

Hydrogen as an alternative to Fossil Fuel

Global population growth and growing demand for clean energy, industrial outputs, and consumer use have resulted in a general increase in environmental and anthropogenically generated greenhouse gas emissions. Likewise, industrialized, advanced, and developing countries are looking for fossil fuel and petroleum resources to serve their aviation, electric utilities, industrial sectors, and consumer processing needs. As developing technology developments in clean energy technologies continue, there is a growing trend to overcome these challenging concerns. Hydrogen is expected to be used as a primary fuel in future energy carrier material research and manufacturing processes in a variety of production applications.

As a result, an increase in the adoption of hydrogen storage as a substitute for fossil fuels among a wide range of end-users is expected to drive the hydrogen storage market during the forecast period. This is due to the fact that hydrogen storage provides various benefits that fossil fuel does not. This is going to be a key factor driven by a rise in the consumption of hydrogen storage as a substitute for the use of fossil fuels. Besides that, rising energy demand, volatile fossil fuel prices, and massive greenhouse gas (GHG) emissions from fossil-fuel-powered automobiles and industries are expected to be major drivers for the adoption of hydrogen storage as an alternative to fossil fuel, driving the hydrogen storage market during 2025-2032.

High demand for Environmentally Friendly Power Sources

High demand for Environmentally Friendly Power Sources

The increased awareness of sustainable energy services is also a driving factor for hydrogen storage industrial growth. This is due to the growing popularity of renewable energy around the world. Hydrogen energy may improve the electrical grid and the transportation sector in the long term. The growing focus that governments across the world are placing on environmentally friendly electricity generation is expected to drive the hydrogen storage market growth during the forecast period. This is because governments in every part of the world are actively attempting to reduce their environmental effect by emitting carbon dioxide. Several reasons, including this, are driving the market's rise significantly during the forecast period.

Rising governmental initiatives around the world

The Energy Storage Organisation, the United States national trade association for the energy storage industry, submitted the Energy Storage Tax Incentive and Deployment Act in . The purpose of this measure is to increase the adoption of energy storage technology. The bill's sponsors want to encourage and make more accessible the usage of energy storage technology. The bill's supporters have stated that they expect it would stimulate and facilitate the use of different energy storage technologies. This act states that regardless of the type of energy stored, any technique of storing energy, including hydrogen storage, shall be eligible for financial incentives. These requirements apply to all energy storage methods, including hydrogen storage. These restrictions apply to all energy storage methods, including hydrogen storage. As a result of their respective impacts, recent developments, and rising government initiatives are expected to result in the emergence of new market opportunities for the hydrogen storage market during the forecast period.

High Capital Cost of keeping the liquid from vaporizing

The total amount of energy that fuel cells can produce from hydrogen and then use to meet the needs of commercial and residential buildings is extremely low. The energy source for fuel cells is hydrogen. However, due to the high insulation costs necessary to avoid vaporization, the market for storing hydrogen energy in liquid form has significant capital costs. These expenses are required to keep the liquid from vaporizing. These expenses are required to keep the liquid from evaporating, which would be undesirable. For example, according to the Department of Energy in the United States, the cost of storing hydrogen of the solid kind is USD 2.1/kg for a flow rate of 10 kg/hr. This pricing includes a storage capacity of 10 kilos per hour. Even at a flow rate of 10,000 kg per hour, the cost of storing hydrogen in solid form remains around USD 2.1/kg. Even though there is a decrease in flow rate, this is still the case. As a result, the high capital cost of keeping the liquid from vaporizing is expected to restrict market growth.

Hydrogen Storage Market Segment Analysis:

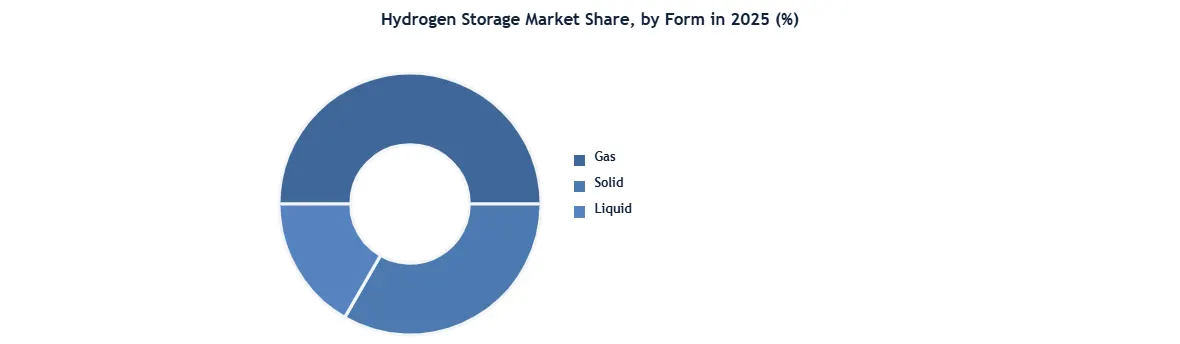

Baseb On Form :The gas segment dominates the global hydrogen storage market, driven by its widespread use in industrial applications, transportation, and energy storage systems. Compressed gaseous hydrogen is the most commercially adopted storage form because it offers easier handling, established infrastructure, and compatibility with fuel cell vehicles and refueling stations. High-pressure tanks ranging from 350 to 700 bar are extensively used across automotive, aerospace, and industrial sectors. In 2025, gaseous storage held the largest market share due to strong deployment in hydrogen-powered mobility projects and government investments in clean fuel infrastructure. Its lower conversion cost compared with liquefaction also supports broad adoption.

The liquid segment is witnessing strong growth due to increasing use in long-distance transportation, aerospace, and large-scale energy storage. Liquid hydrogen offers higher energy density than compressed gas, making it suitable for applications requiring bulk storage and efficient transport. Demand is rising in space exploration, shipping, and export-based hydrogen supply chains. However, the need for cryogenic temperatures and higher storage costs limits faster adoption.The solid segment includes metal hydrides, chemical hydrides, and advanced material-based storage systems. This segment remains emerging but is gaining attention due to its safety, compactness, and ability to store hydrogen at lower pressures. Growing research in stationary storage and next-generation fuel systems is expected to drive future adoption, particularly for renewable energy integration and decentralized storage applications.

Based on Application, the Chemical industry segment dominated the global hydrogen storage market with the highest market share of about 42% in 2025. The segment is further expected to grow at a CAGR of about 7.85% and maintain its dominance at the end of the forecast period. The chemical industry is crucial in generating innovative solutions to allow the transition to a sustainable and circular economy, but it has a significant challenge to achieve net zero emissions. Only a fraction of the net-zero aim can be met by energy efficiency, bio-based feedstock, and material loop closure, emphasizing the importance of alternative technologies such as hydrogen, carbon capture, and electrification in the chemical industry.

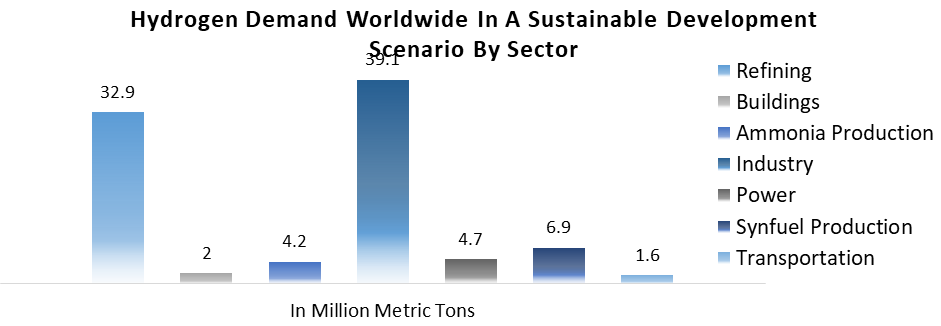

Approximately 10 million tonnes of hydrogen are already utilized in the EU industry, mostly as a fuel for ammonia production and in the refining industry. Blue and green hydrogen are the two main low-CO2 alternatives to grey hydrogen, which now account for 95% of hydrogen generation. The energy revolution and path to net-zero have also resulted in new potential roles for low-CO2 hydrogen, and the hydrogen market and hydrogen storage market is expected to grow considerably by the end of the forecast period, with hydrogen becoming the primary energy carrier of the future EU energy system. Industry (heat, steam, reducing agent in the steel industry), sustainable fuels for transportation (primarily shipping, long-distance road transport, and aviation), sustainable chemical feedstock (methanol, ammonia), and, to a lesser extent, hydrogen as a storage medium to enable the transition to renewable energy, are the three major demand drivers and expected to drive the global hydrogen storage market.

The emerging hydrogen economy is supported by global and regional governmental efforts, with a USD 450 billion investment required by 2032. The growing number of hydrogen projects being started or announced in the chemical sector demonstrates the industry's interest in hydrogen and emphasizes the need to move quickly. Countries outside of Europe are also formalizing hydrogen policies and initiatives, with China's need for hydrogen expected to reach 60 million tonnes per year by 2050. Chemical businesses are particularly positioned to capitalize on the potential of the burgeoning hydrogen economy, and by doing so, they may gain a competitive edge.

A collection of strategic decisions cascading down from "aspiration" to "where to play" to "how to win" to "how to configure" aids in the systematic and intentional establishment of the proper business direction and strategy. Hydrogen is not only a critical enabler for the industry to achieve net-zero emissions, but it is also an essential potential for chemical businesses to establish new sustainable revenue streams. New business and pricing models may be economically adopted by making informed decisions based on the potential and willingness to pay for diverse markets, as well as by concentrating on client centricity. Chemical businesses may use their strong global assets, interconnected supply networks, current sales and distribution, hands-on technical experience, and so on to jumpstart their future position in the hydrogen economy and make the profitable change to a more sustainable portfolio.

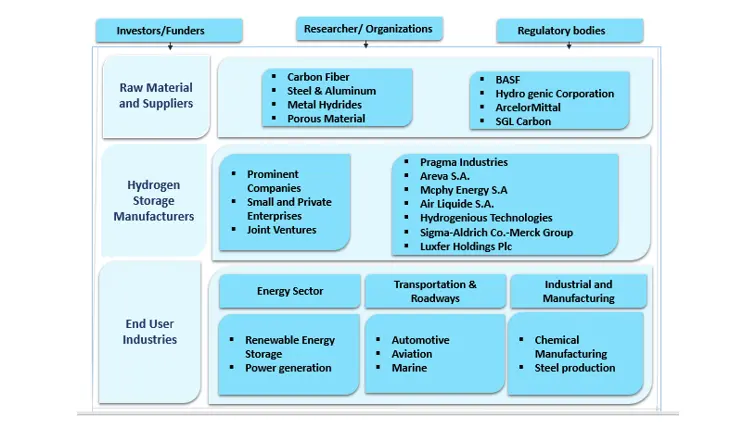

Hydrogen Storage Industry Ecosystem:

Hydrogen Storage Market Regional Insights:

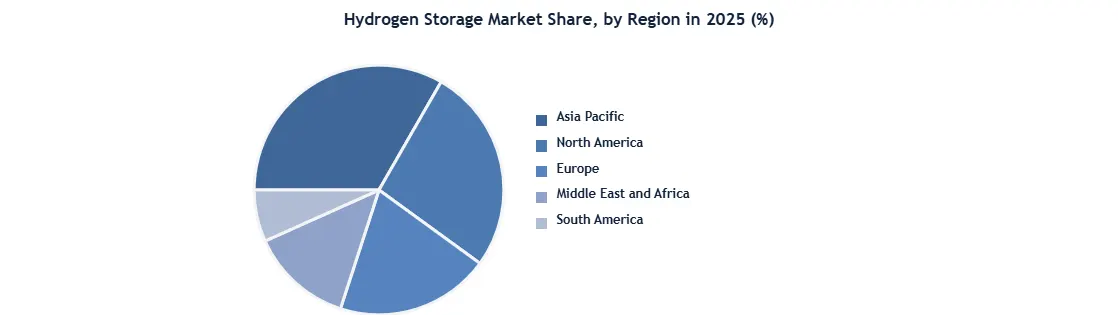

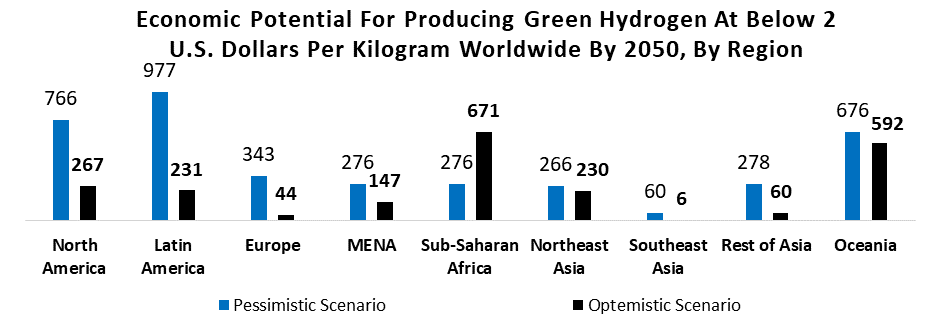

The Asia-Pacific region held the largest market share of the hydrogen storage market in 2025. The region is expected to be at a CAGR of about 7.89% and dominated the market at the end of the forecast period. An increasing population, rising energy needs, growing industrial sectors, manufacturing plants, and rapid economic development are expected to be the key factors driving the Asia-Pacific hydrogen storage market during the forecast period. By 2050, hydrogen will be a key component of energy markets across the world, allowing many countries to maximize their natural resources and lessen their dependency on imported oil and gas while opening up new opportunities for others to import energy.

China, as the world's largest primary energy consumer, is expected to be the largest single market for clean hydrogen by 2050, with a demand for 200 million tonnes (MT) of clean hydrogen, followed by Europe and North America, each with a demand for 100 MT of clean hydrogen, India with 55 MT, and Japan and South Korea with 35 MT. By 2050, the rest of the world, including Latin America, the Middle East, Oceania, and Southeast Asia, will account for approximately 175 MT of total hydrogen demand and drive the global hydrogen storage market. Most government programs are aimed at creating low-carbon hydrogen. Measures to boost demand are getting less attention. Japan, Korea, France, and the Netherlands have set FCEV deployment goals.

However, increasing the importance of low-carbon hydrogen in clean energy transitions necessitates a significant shift in sales. Governments are starting to declare a wide range of policy tools, such as carbon pricing, auctions, quotas, mandates, and public procurement requirements. The majority of these policies have not yet taken effect. Their swift and broad implementation might pave the way for new projects to ramp up hydrogen consumption and propel the hydrogen storage market throughout the forecast period.

Green hydrogen is the most competitive kind of hydrogen in the long term due to India's specific edge in low-cost renewable energy generation. As a result, India has the potential to be one of the world's most competitive producers of green hydrogen. Green hydrogen has the potential to reach cost parity with natural gas-based hydrogen (grey hydrogen) by 2032, if not before. Aside from the cost, because hydrogen is only as clean as the source from which it is produced, green hydrogen will be required to build a genuinely low-carbon economy. It will also allow for the development of a domestically generated energy carrier, which would minimize reliance on imports for essential commodities such as natural gas and petroleum. Hydrogen demand in India could grow more than fourfold by 2050, representing almost 10% of global hydrogen demand. Initial demand growth is expected from existing sectors such as refineries, ammonia, and methanol, which currently use hydrogen as a feedstock and in chemical processes. Steel and heavy-duty transportation are expected to generate the majority of demand increase, in the long run, accounting for over 52% of total demand by 2050.

Green hydrogen is the most competitive kind of hydrogen in the long term due to India's specific edge in low-cost renewable energy generation. As a result, India has the potential to be one of the world's most competitive producers of green hydrogen. Green hydrogen has the potential to reach cost parity with natural gas-based hydrogen (grey hydrogen) by 2032, if not before. Aside from the cost, because hydrogen is only as clean as the source from which it is produced, green hydrogen will be required to build a genuinely low-carbon economy. It will also allow for the development of a domestically generated energy carrier, which would minimize reliance on imports for essential commodities such as natural gas and petroleum. Hydrogen demand in India could grow more than fourfold by 2050, representing almost 10% of global hydrogen demand. Initial demand growth is expected from existing sectors such as refineries, ammonia, and methanol, which currently use hydrogen as a feedstock and in chemical processes. Steel and heavy-duty transportation are expected to generate the majority of demand increase, in the long run, accounting for over 52% of total demand by 2050.

Hydrogen Storage Market Recent Developments:

Hydrogen Storage Market Scope: Inquire before buying

| Hydrogen Storage Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 19.41 USD Billion |

| Forecast Period 2026-2032 CAGR: | 7.97% | Market Size in 2032: | 33.21 USD Billion |

| Segments Covered: | by Form | Solid Liquid Gas |

|

| by Technology | Liquid Hydrogen Storage Material-Based Storage Underground Bulk Storage |

||

| by Component | Pipe Valve Pump Tank Type I Type II Type III Type IV Others |

||

| by Material | Metal Hydrides Chemical Hydrides Carbon-based Materials |

||

| by Type of Storage | Cylinder Merchant On-Site On-Board |

||

| by Application | Utilities and Grid Operator Industrial Transportation Others |

||

Hydrogen Storage Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Hydrogen Storage Market, Key Players are:

- Linde plc

- Air Liquide SA

- Air Products and Chemicals, Inc.

- Worthington Enterprises

- Hexagon Composites ASA / Hexagon Purus

- Luxfer Holdings PLC

- Quantum Fuel Systems LLC

- Faber Industrie S.p.A.

- NPROXX Gmbh

- McPhy Energy S.A.

- Nel ASA

- Plug Power Inc.

- Chart Industries, Inc.

- SFC Energy AG

- Hyto Energy Company Limited

- Hydrogenious LOHC Technologies

- H2Go Power

- Hydrexia

- GRZ Technologies

- Noble Gas Systems

- HDF Energy

- H2Gremm

- Vortex Energy

- GreenHy2

- Tenaris

- Steelhead Composites Inc.

- Coolergy

- Iwatani Corporation

- Engie

- Inoxcva

- Cryofab

- Everest Kanto Cylinder Ltd.

- OPMobility

- Umoe Advanced Composites

- CIMC Enric Holdings Limited

- Doosan Mobility Innovation

- BNH Gas Tanks

- Calvera Hydrogen

- Bayotech

- ECS Composite

- Vako GmbH & Co. KG

- Johnson Matthey Plc

Others