Green Data Center Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

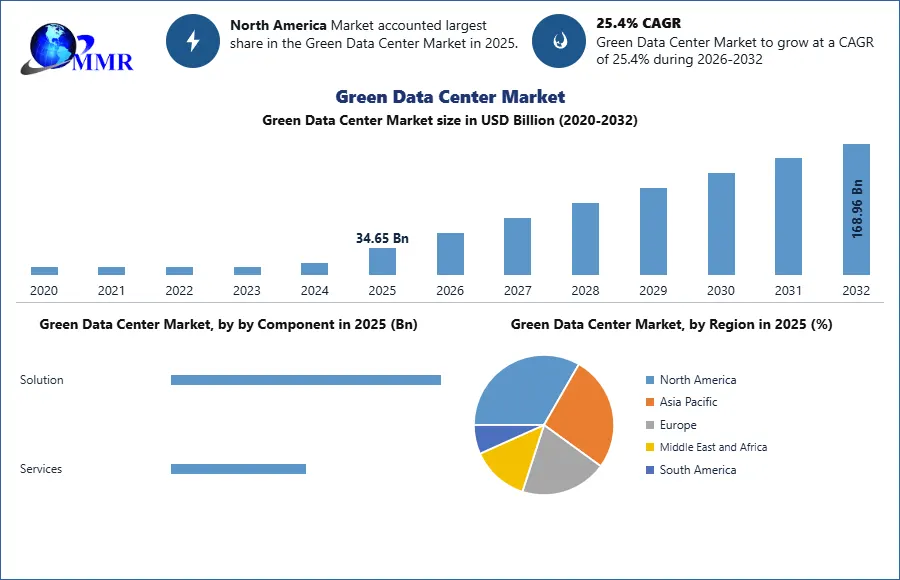

Global Green Data Center Market size was valued at USD 34.65 Bn. in 2025 and the total Green Data Center Market revenue is expected to grow by 25.4% from 2026 to 2032, reaching nearly USD 168.96 Bn.

Green Data Center Market Overview:

The Green Data Center Market is a rapidly evolving segment of the global data center industry, transforming how organizations address their environmental impact through enhanced energy efficiency, the adoption of renewable energy, and advanced cooling and power management solutions. This market emphasizes innovative approaches, including liquid cooling technologies, artificial intelligence (AI) for operational and energy optimization, and modular designs, to minimize carbon footprints and reduce operational costs.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The growth of the Green Data Center Market is driven by the surging demand for storage and processing capabilities fueled by cloud computing, the Internet of Things (IoT), and artificial intelligence applications. Rising energy costs, stringent sustainability regulations, and corporate carbon-neutrality targets have accelerated the adoption of solutions like free-air cooling in temperate climates and onsite solar or wind energy generation, achieving unprecedented Power Usage Effectiveness (PUE) levels compared to traditional data centers in North America and Europe.

The Green Data Center Market is also propelled by several key drivers, including the increasing demand for hyperscale and edge computing, advancements in renewable energy storage, and the enforcement of global green building standards such as LEED and BREEAM. Leading companies shaping the Green Data Center Market include Schneider Electric SE, Cisco Systems, Inc., Hewlett-Packard Enterprise (HPE), Dell Technologies, and Vertiv Holdings Co. These industry players focus on integrating AI capabilities, optimizing cooling technologies, procuring renewable energy sources, and aligning with environmental, social, and governance (ESG) principles to maintain competitiveness.

Emerging trends in the Green Data Center Market highlight the rapid expansion of modular green data centers, significant advancements in liquid immersion cooling, and the integration of energy storage systems to support grid stability. These developments are largely driven by regulatory mandates and global enterprise sustainability commitments. The Green Data Center Market is poised for substantial growth as data center operators continue to innovate and implement environmentally responsible solutions to meet rising global computing demands while reducing environmental impact.

Green Data Center Market Dynamics

Increased internet activity demands to Drive Green Data Center Market Growth

The green data center market is witnessing significant growth driven by a confluence of factors, primarily resulting from the substantial increase in internet usage. This surge in internet activity has amplified the energy consumption of data centers to ensure their efficient operation, subsequently leading to a significant environmental impact. This heightened power consumption by data centers is a primary driver of the green data center market, as organizations are seeking more sustainable and eco-friendly solutions to counteract this impact. Moreover, there is a growing awareness among individuals and enterprises regarding the environmental consequences of high energy usage by data centers. Governments are also taking proactive measures to address this issue through initiatives that encourage the adoption of green policies. As a result, more enterprises are aligning themselves with these green initiatives, which is further propelling the growth of the green data center market.

From High Energy Costs to Eco-Friendly Solutions to Drive Green Data Center Market Growth

One of the key drivers is the high energy cost associated with traditional data centers. These expenses are prompting organizations to transition to more energy-efficient green data centers, resulting in significant cost savings. Additionally, government guidelines and regulations that advocate the adoption of green data centers are motivating organizations to invest in environmentally sustainable solutions. Environmental concerns and government regulations are pushing the market towards practices that reduce carbon emissions and environmental impact, making green data centers a more attractive and responsible choice. Furthermore, the advent of advanced technologies, such as economizers for cooling data centers, is driving the growth of the global green data center market by enhancing efficiency and reducing environmental impact. However, certain challenges exist that could hinder the growth of the green data center market. The rapid pace of research and development activities aimed at technological advancements can pose a challenge as it requires continuous adaptation and investment. Additionally, systems using green data centers may sometimes be underpowered compared to traditional counterparts, and the initial cost of implementing this technology can be a hindrance.

Renewable Energy Integration and Innovative Cooling Technologies to Create Green Data Center Market Opportunity

The seamless incorporation of renewable energy sources, by adding solar panels, wind turbines, and hydroelectric power, affords data centers a remarkable chance to prominently lower their environmental impact in the green data center market. By adapting harnessing clean, sustainable energy sources, data centers can reduce their dependence on fossil fuels, thus execution their operations more environmentally responsible while achieving substantial energy cost savings. Progressions in cooling technologies, such as liquid cooling, hot/cold aisle containment, and free cooling, present data centers with an opportunity to elevate their energy efficiency. These cooling solutions not only curtail the energy necessary for temperature management but also curbs the environmental repercussions associated with cooling processes. The ascendancy of edge computing, propelled by the demand for low-latency data processing and the burgeoning Internet of Things (IoT), generates opportunities for the establishment of smaller, decentralized data centers situated in closer proximity to end-users. This approach reduces the energy and resources required for long-distance data transmission, positioning data centers to adeptly meet the contemporary requirements of computing in the green data industry.

The continual evolution of energy-efficient server hardware, storage devices, and networking equipment affords data centers the prospect to optimize their energy consumption. High spending in these energy-efficient components can significantly provide the sustainability and cost-effectiveness of green data center operations. The adaptation of cloud-based software and services, incorporating public, private, and hybrid cloud, empowers firms to reduce their dependence on energy-intensive in-house data centers. This immigration to the cloud not only reduces energy utilization but also boosts scalability and flexibility. The deployment of advanced energy management and monitoring systems empowers data centers to monitor and optimize their energy consumption. These technologies furnish valuable insights into areas where enhancements in energy efficiency can be made, ensuring more sustainable and cost-effective operations.

Global Green Data Center Market Segment Analysis

Based on Data Center Size, The market is segmented into Large Data Centers and Small & Medium Data Centers. Large data centers, spanning over 25,000 square feet dominated the Green Data Center Market in 2025. They are equipped with high-energy-efficient Computer Room Air Handler (CRAH) and Precision Air Handling Unit (PAHU) systems, along with efficient liquid cooling technology to optimize performance and minimize energy losses. Due to their extensive infrastructure and complex networking equipment, large data centers consume significant power compared to mid-size and enterprise data centers. They are primarily utilized by large enterprises with a high density of cloud computing systems. These data centers play a crucial role in the green data center market by offering efficient power flow to both private and hybrid cloud environments, reducing capital and operational expenditures (CAPEX and OPEX), ensuring data protection, and driving the adoption of green data center solutions globally.

Based on Component, the Green Data Center Market is segmented into Hardware: Servers, Cooling Equipment, Power Units, Networking Components and Software. Among these the Hardware segment has dominated the market in 2025 and is expected to hold largest market share over forecast period because there is heavy reliance on capital investment because to set up and operate a green data center, organizations are required to make significant capital expenditures on physical components of the data center, such as servers, advanced cooling systems, energy-efficient power units, and high performance network components. These components are the primary building blocks of all data center operations, and have the most direct impact on energy efficiency and carbon footprint. Organizations are also increasingly looking to replace the hardware that they currently have with energy-efficient servers, module-style cooling systems, and renewable energy sourced power units, as they seek to reduce operational costs while pushing operations into the sustainability goals of carbon footprint emissions reduction. Operational changes are also seen as a vehicle to capitalize on reducing operational costs. To achieve meaningful and measurable efficiency improvements, hardware upgrades are necessary adjustments for organizations, while software is supportive to the actual optimization and management of energy efficiency and other operational parameters, and does hold significant market share compared to hardware.

Green Data Center Market Regional Insights

North America led the market with a substantial share of 37.50% in 2025. This prominent position can be attributed to various factors. Firstly, the region has seen the emergence of energy efficiency targets and regulatory demands, compelling businesses to embrace greener data center solutions. Moreover, there is a strong commitment to supporting sustainability efforts, both in terms of environmental responsibility and corporate ethics. The increasing adoption of eco-friendly practices across diverse North American industries reflects a growing environmental awareness, further driving green data center market expansion. The Asia Pacific region is anticipated to record the highest Compound Annual Growth Rate (CAGR) of xx% throughout the forecast period. This exceptional growth can be ascribed to several key drivers. The rapid economic development in this region has led to a substantial surge in data traffic and heightened energy demand. Consequently, there is a growing concern about the environmental consequences of this increased energy consumption, leading to heightened support for international sustainability programs and initiatives. Numerous countries in the Asia Pacific region are enforcing stricter regulations concerning energy consumption and emissions. Green data centers are playing a pivotal role in helping businesses adhere to these regulations, thus averting penalties and actively contributing to regional sustainability endeavor.

The Asia Pacific region is home to some of the world's most highly populated countries and the fastest-growing economies in the green data center market. Hence Asia-Pacific region has become a focal point for sustainable energy practices and the adoption of green data center technologies. With the increasing surge for electricity, there is an intensive effort to boost energy efficiency and implement eco-friendly measures to manage energy costs. The convergence of these factors positions the Asia Pacific region as a vibrant hub for the growth of green data centers, where sustainability and efficiency stand as cornerstones of modern business strategies.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 24 February 2026 | Google / Xcel Energy | The companies finalized a Clean Energy Accelerator Charge (CEAC) agreement to fund 1,400MW of wind and 200MW of solar power for a Minnesota data center. | This regulatory tariff allows Google to directly fund and bring new carbon-free energy online to achieve 24/7 carbon-free energy goals. |

| 06 March 2026 | The company finalized a $4.8 billion deal for Intersect Power and launched a new coalition named Utilize alongside Tesla. | The acquisition secures large-scale renewable energy assets to support the massive power requirements of AI-driven green data centers. | |

| 19 June 2025 | Schneider Electric / NVIDIA | The firms introduced a co-developed AI-ready infrastructure platform at GTC Paris 2025, integrating liquid cooling and OCP racks. | The solution optimizes energy efficiency for high-density AI workloads, supporting the AI Continent Action Plan across Europe. |

| 10 June 2025 | Oklo Inc. / Vertiv | Oklo and Vertiv signed a partnership to co-develop advanced nuclear-powered thermal and power management solutions for hyperscale facilities. | By utilizing advanced fission, the collaboration aims to provide a reliable, carbon-free baseload power source for sustainable data center campuses. |

| 13 March 2025 | Schneider Electric | The company secured $1 billion in funding specifically dedicated to expanding its Green Data Center Solutions business unit. | This capital injection accelerates the commercialization of energy-efficient hardware and microgrid technologies for global cloud providers. |

| 15 January 2025 | Amazon (AWS) | AWS officially launched its first cloud region in Thailand, part of a long-term $5 billion investment in local sustainable infrastructure. | The expansion strengthens green computing availability in Southeast Asia while meeting strict energy efficiency standards for new builds. |

Green Data Center Market Scope: Inquiry Before Buying

| Green Data Center Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 34.65 USD Billion |

| Forecast Period 2026-2032 CAGR: | 25.4% | Market Size in 2032: | 168.96 USD Billion |

| Segments Covered: | by Component | Solution Monitoring & Management System Cooling System Networking System Power Systems Others Services Installation & Deployment Consulting Support & Maintenance |

|

| by Enterprise Size | Large Enterprises SMEs |

||

| by Data Center Size / Capacity | Edge & Micro Data Centers (1–5 MW) Medium Data Centers (5–15 MW) Large & Hyperscale Data Centers (50 MW & above) |

||

| by Data Center Type | Cloud & Hyperscale Data Centers Colocation Data Centers Enterprise Data Centers |

||

| by End-User Industry | Manufacturing Energy & Utilities Retail & E-commerce Technology & Software Telecommunications Media & Entertainment BFSI Healthcare & Life Sciences Others |

||

Green Data Center Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitores Proflies Coverd Green Data Center Market Report in Strategic Perspective

North America

1. Cisco Systems Inc. (USA)

2. International Business Machines (IBM) Corporation (USA)

3. Hewlett Packard Enterprise Company (USA)

4. Dell Inc. (USA)

5. Equinix, Inc. (USA)

6. Eaton Corporation Plc (USA)

7. EcomNets Inc. (USA)

8. Vertiv (USA)

9. Midas Green Technologies (USA)

10. Nortek Air Solutions (USA)

11. Asetek (USA)

12. Airedale (USA)

13. Lenovo (USA)

14. Cyber Power Systems (USA)

15. Super Micro (USA)

16. Tripp Lite (USA)

17. CDP Energy (USA)

18. Bxterra Power Technology (USA)

19. Green Revolution Cooling (USA)

Europe Green

1. Ericsson Inc. (Sweden)

2. Fujitsu Ltd. (UK)

3. Schneider Electric (France)

4. Delta Electronics (Netherlands)

5. Rittal (Germany)

6. Airedale (UK)

Asia Pacific

1. Fujitsu Ltd. (Japan)

2. Tech Mahindra Ltd. (India)

3. Delta Electronics (Taiwan)

4. Lenovo (China)

5. Cyber Power Systems (Taiwan)

6. Inspur (China)