Fluoroscopy Equipment Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

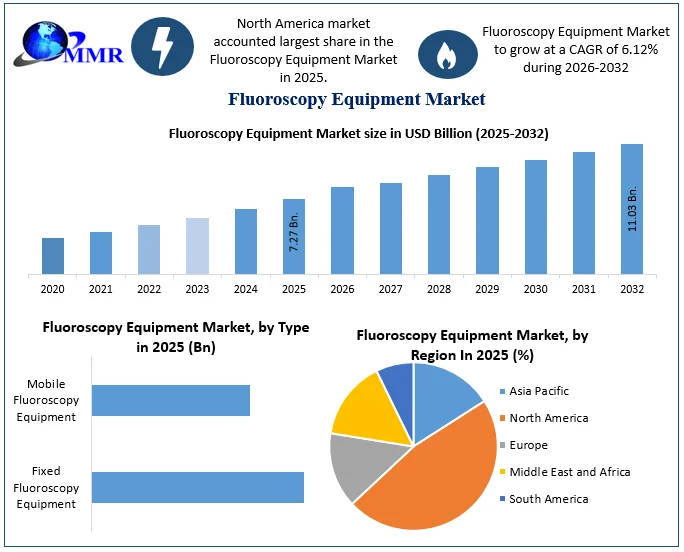

Global Fluoroscopy Equipment Market size was valued at USD 7.27 Bn in 2025 and Fluoroscopy Equipment market revenue is expected to reach USD 11.03 Bn by 2032, at a CAGR of 6.12% over the forecast period.

Fluoroscopy Equipment Market Overview:

Fluoroscopy tools are medical imaging systems that use continuous X-rays to generate real-time moving images of internal body structures, which are mainly used for clinical and traditional processes. Increasing demand for clinical and traditional processes in healthcare, which promotes the requirement of advanced imaging devices for aging population and increased prevalence of chronic diseases fuels demands for fluoroscopy. The expansion of healthcare infrastructure in emerging fluoroscopy equipment markets provides opportunities for the development of the fluoroscopy equipment, as these areas try to increase their medical abilities.

Excessive frequency of diseases such as heart issues, abdominal problems, and bone related injuries requires more sophisticated methods for diagnosis and treatment through imaging. Fluoroscopy is essential for diagnosis and treatment of these conditions, leading to high demand for fluoroscopy equipment and services. North America Fluoroscopy Equipment Market is dominant due its adequate health care expenses. GE Healthcare, Orthoscan Inc., Siemens Medical Solutions Inc., Philips Healthcare are the major fluoroscopy equipment companies. Hospitals account for 65% of use (complex intervention), while ASCS (25%) and diagnostic centres (10%) demand drive for mobile C-Arms, compact by the fluoroscopy equipment industry and supported by the cost-affected systems.

To know about the Research Methodology :- Request Free Sample Report

Fluoroscopy Equipment Market Dynamics:

Technological Advancements in Healthcare Sector to Boost the Fluoroscopy Equipment Market Growth

The fluoroscopy equipment market is experiencing a period of sustained growth driven by a confluence of factors that are shaping the landscape of medical imaging. As this sector of the healthcare industry continues to evolve, a range of drivers is propelling its expansion and adoption. These drivers are instrumental in enhancing diagnostic accuracy, minimizing radiation exposure, and supporting the trend toward minimally invasive medical procedures. Ongoing innovations in imaging technology have propelled the transition from traditional analog fluoroscopy to digital fluoroscopy.

This shift to digital formats has revolutionized the field by significantly enhancing image quality, allowing for real-time imaging with higher precision, and reducing radiation exposure. These technological advancements make fluoroscopy equipment more versatile, accurate, and efficient in its diagnostic and interventional capabilities. A key driving force behind the market's growth is the shifting paradigm toward minimally invasive medical procedures. This transformative trend is significantly altering the landscape of healthcare by offering patients less invasive treatment options with reduced risks and shorter recovery times. Fluoroscopy equipment plays an essential role in this shift. By providing dynamic, real-time imaging during minimally invasive surgeries and interventions, it enables healthcare professionals to navigate devices within the body with pinpoint accuracy. This enhances procedural precision, reduces complications, and expedites patient recovery.

The real-time, dynamic imaging capabilities of fluoroscopy are instrumental in enhancing diagnostic accuracy. The ability to observe the live movement of internal structures during procedures provides healthcare professionals with valuable insights. This dynamic imaging empowers them to make timely and precise diagnoses, thereby improving patient outcomes. As a result, the fluoroscopy equipment market remains buoyed by its indispensable role in increasing the accuracy of medical diagnoses. The expansion of healthcare infrastructure in emerging markets presents fertile ground for the growth of the fluoroscopy equipment market. These regions are actively enhancing their medical capabilities to meet the growing healthcare needs of their populations. As they invest in upgrading their healthcare systems, there is a burgeoning demand for advanced medical imaging equipment, including fluoroscopy systems. This growing market penetration in emerging economies is a notable driver of the fluoroscopy equipment market's overall expansion.

High Initial Costs of Equipment to Restraint Fluoroscopy Equipment Market Growth

The foremost impediments encountered in the mobile fluoroscopy equipment market is the considerable initial investment associated with procuring and deploying these systems. In particular, the acquisition of cutting-edge digital mobile fluoroscopy equipment, equipped with advanced features, imposes a significant financial burden on healthcare facilities. These upfront expenses can be a deterrent, especially for smaller clinics and healthcare providers with budgetary constraints. Consequently, the adoption of mobile fluoroscopy equipment may proceed at a slower pace in resource-limited settings. Radiation exposure remains a persistent concern in the realm of medical imaging, and mobile fluoroscopy is no exception. Despite notable advancements aimed at reducing radiation doses, especially with the transition to digital mobile fluoroscopy, a certain level of risk persists. Medical professionals and patients understandably exhibit caution regarding radiation exposure. They often demand robust safety measures and clear communication pertaining to associated risks. Achieving a delicate balance between obtaining high-quality imaging and minimizing radiation exposure remains a complex challenge in mobile fluoroscopy.

Efficient operation of mobile fluoroscopy equipment hinges on the presence of skilled operators who can adeptly navigate the technology and accurately interpret real-time images. However, certain regions grapple with a shortage of adequately trained operators, limiting the optimal utilization of mobile fluoroscopy equipment. Addressing this constraint requires investments in training and education to ensure a proficient workforce capable of harnessing the full potential of mobile fluoroscopy systems. These educational endeavors may necessitate time and resources. The mobile fluoroscopy equipment market encounters competition from alternative imaging modalities, including computed tomography (CT) scans, magnetic resonance imaging (MRI), and ultrasound. Each of these alternatives boasts distinct advantages, and healthcare providers may opt for these technologies over mobile fluoroscopy based on specific clinical requirements and patient needs. The competition among various imaging modalities can impact the market's growth potential, underscoring the necessity for ongoing innovation and differentiation in mobile fluoroscopy offerings.

Fluoroscopy Equipment Market Segment Analysis:

Based on Type, the market is segmented into Fixed Fluoroscopy Equipment, and Mobile Fluoroscopy Equipment. Mobile Fluoroscopy Equipment dominated the market in 2025 and is expected to hold the largest Fluoroscopy Equipment Market share over the forecast period. Mobile Fluoroscopy Equipment is known for its flexibility and versatility. It empowers healthcare providers to transport the equipment swiftly to different locations within a healthcare facility. This adaptability is invaluable, facilitating a wide array of medical procedures. It allows for bedside imaging, seamless integration into operating rooms, and rapid deployment during emergency situations. The ability to bring fluoroscopy directly to the patient's bedside or into the surgical suite represents a substantial advantage that caters to the evolving needs of modern healthcare.

Resource optimization stands as a pivotal benefit of mobile fluoroscopy systems. By reducing the reliance on multiple fixed units dispersed across various procedure rooms, these mobile systems streamline costs and resource utilization. Healthcare facilities can invest in a singular mobile unit, which, in turn, efficiently serves multiple departments. This consolidation of resources is a strategic advantage that aligns with modern healthcare economics. Mobile Fluoroscopy Equipment manufacturers in the medical imaging industry have not remained static. They have consistently propelled the envelope of innovation in mobile fluoroscopy technology. These advancements manifest in improved image quality, precise dose management, and enhanced user-friendliness. Collectively, these technological strides have cemented the dominance of mobile fluoroscopy units in the market.

Based on Technology, the market is segmented into Analog Fluoroscopy Equipment, and Digital Fluoroscopy Equipment. Digital Fluoroscopy Equipment segment dominated the market in 2025 and is expected to hold the largest Fluoroscopy Equipment Market share over the forecast period. Digital fluoroscopy equipment provides superior image quality with high resolution and improved contrast. This enhanced image clarity allows for better visualization of anatomical structures and more accurate diagnoses. Digital systems typically require lower radiation doses to produce high-quality images, reducing the radiation exposure for both patients and healthcare professionals. This is a significant safety advantage. Digital fluoroscopy systems offer real-time image capture and immediate availability, allowing healthcare providers to view and analyse images quickly. This speed can be crucial in emergency situations and interventional procedures. The elimination of film and chemicals in digital fluoroscopy contributes to a more environmentally friendly imaging process.

Based on End user, the market is segmented into Hospitals, Clinics and Diagnostic Centres, and Ambulatory Surgical Centres (ASCs). Hospitals segment held the largest Fluoroscopy Equipment Market share in 2025 and is expected to dominate the market over the forecast period. Hospitals are known for handling complex medical cases and providing specialized care. Patients with serious medical conditions and intricate diagnostic or interventional needs often seek treatment at hospitals. Fluoroscopy equipment is essential for diagnosing and treating such cases, ensuring accurate and real-time imaging guidance during procedures.

Hospitals have dedicated imaging suites or departments equipped with advanced fluoroscopy equipment. These imaging suites are staffed with specialized healthcare professionals, including radiologic technologists and physicians with expertise in various medical fields. These professionals operate fluoroscopy equipment for specific applications within the hospital. Many hospitals are affiliated with medical schools and research institutions. They provide a valuable environment for medical education and research. Fluoroscopy equipment is used for training future healthcare professionals and conducting research studies related to medical imaging and interventions.

Global Fluoroscopy Equipment Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 11 March 2026 | Noah Medical | The company announced the publication of its MATCH 2 study validating the reliability of real-time imaging guidance during robotic bronchoscopy. | The results confirm enhanced diagnostic precision and safer navigation paths during complex intraoperative fluoroscopic tracking. |

| 16 December 2025 | Philips | The company expanded the commercial rollout of its LumiGuide 3D navigation integrated with the Azurion fluoroscopy platform across the U.S. and Europe. | This integration provides AI-enabled, radiation-free solutions that offer real-time light-based guidance during intricate image-guided surgical therapies. |

| 10 October 2025 | Canon Medical Systems | The company secured U.S. FDA 510(k) clearance for its Alphenix interventional fluoroscopic X-ray systems featuring αEvolve Imaging technology. | The update implements Artificial Intelligence Denoising (AID) algorithms to drastically reduce visual noise in real-time fluoroscopic streams. |

| 21 July 2025 | Siemens Healthineers | The company obtained U.S. FDA clearance for its newly engineered Luminos Q. namix R and Luminos Q. namix T radiography and fluoroscopy platforms. | The systems drastically lower radiation exposure for patients while boosting operational workflow efficiency via remote and tableside controls. |

| 12 February 2025 | Konica Minolta Healthcare Americas | The company published clinical data establishing the efficacy of its Dynamic Digital Radiography (DDR) system for quantitative diaphragm motion assessments. | This deployment demonstrates the commercial viability of low-dose fluoroscopic motion analysis over standard static imaging alternatives. |

| 22 January 2025 | GE HealthCare | The company formed a strategic partnership with Medtronic to co-develop advanced AI-based fluoroscopic imaging solutions. | The collaborative initiative aims to achieve a significant reduction in occupational scatter radiation during complex interventional procedures. |

Fluoroscopy Equipment Market Regional Insight:

North America dominated the Fluoroscopy Equipment Market in 2025 and is expected to hold the largest market share during the forecast period (2026-2032)

The North American region stands at the forefront of technological innovations in the healthcare industry. The constant evolution of fluoroscopy equipment, with the integration of digital imaging, advanced software, and real-time visualization capabilities, has significantly boosted the adoption of fluoroscopy systems. North America is known for its substantial healthcare expenditure. The region's commitment to delivering advanced healthcare services is reflected in its substantial investments in medical equipment.

Healthcare facilities across North America are well-equipped and maintain advanced infrastructure, making it conducive for the adoption of fluoroscopy equipment, which is expected to boost the fluoroscopy equipment market growth. Stringent regulations and standards related to patient safety and radiation exposure have led to advancements in fluoroscopy equipment design. The compliance requirements have encouraged healthcare facilities to invest in modern fluoroscopy systems that offer lower radiation doses, precise imaging, and enhanced patient safety.

The utility of fluoroscopy equipment extends beyond traditional medical specialties. It finds applications in diverse fields such as interventional radiology, vascular surgery, pain management, and more. The continuous discovery of new applications and procedures has expanded the market's reach and driven adoption. North America has a thriving medical education system, and many healthcare facilities are affiliated with educational institutions. This has created a conducive environment for education and training in the use of fluoroscopy equipment. The emphasis on skill development and continuing education has contributed to the proficient operation of fluoroscopy systems.

Fluoroscopy Equipment Market Competitive Landscape:

Major key players in the Fluoroscopy Equipment Market are GE Healthcare (US), Orthoscan Inc. (US), Varex Imaging Corporation (US) and Varian Medical Systems Inc. In 2025, Varian Medical Systems Inc. maintains a strong but special position in the Fluoroscopy Equipment market, mainly focusing on oncology and image-directed radiation therapy (IGRT) rather than traditional fluoroscopy. The company holds an estimated 5–7% market share in a high-end fluoroscopy system, integrating advanced imaging for accurate radiotherapy with its TrueBeam and Ethos platforms. While Siemens dominates the broader fluoroscopy market (22% shares), Varian's technology excels in a combination of fluoroscopy with linear accelerator (LINACS) in the hybrid system, leading to an increase in cancer care. However, its limited appearance in general radiography and mobile C-arms restricts its competition against pure-play fluoroscopy leaders such as GE Healthcare and Philips. Varian's R&D focus lives on AI-powered adaptive radiotherapy, but its fluoroscopy equipment growth depends on the broad distribution network of Siemens, especially in North America (15% regional stake in oncology imaging) and in Europe (10%), where its systems are preferred in academic and special cancer centres.

Fluoroscopy Equipment Market Key Trends:

| Trends | Description | Example |

| Real-time AI enhancements | AI flags vascular blockages or device malposition in real-time | Siemens Healthineers ARTIS icono with syngo AI-Rad Companion |

| Predictive maintenance | Sensors predict X-ray tube/GPU failures before they occur | Philips Azurion with SmartConnect |

| Pulsed fluoroscopy | 80% of new systems now use pulsed mode to meet FDA/EC dose limits | Ziehm Vision RFD 3D |

Fluoroscopy Equipment Market Scope: Inquire before buying

| Fluoroscopy Equipment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 7.27 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.12% | Market Size in 2032: | USD 11.03 Bn. |

| Segments Covered: | by Type | Fixed Fluoroscopy Equipment Mobile Fluoroscopy Equipment |

|

| by Technology | Analog Fluoroscopy Digital Fluoroscopy |

||

| by End User | Hospitals Clinics and Diagnostic Centres Ambulatory Surgical Centres (ASCs) Others |

||

Fluoroscopy Equipment Market by Region

North America (United States, Canada and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam, Indonesia, Philippines, Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America)

Fluoroscopy Equipment Key Players include

North America

1. General Electric Company (US)

2. GE Healthcare (US)

3. Orthoscan Inc. (US)

4. Varex Imaging Corporation (US)

5. Xoran Technologies LLC (US)

6. Thermo Fisher Scientific Inc. (US)

7. Varian Medical Systems Inc. (US)

8. Omega Medical Imaging, Inc. (US)

9. Carestream Health (US)

10. Hologic Inc. (US)

Europe

11. Siemens Medical Solutions, Inc. (Germany)

12. Ziehm Imaging GmbH (Germany)

13. Xcelsitas AG (Germany)

14. Philips Healthcare (Netherlands)

Asia Pacific

15. Shimadzu Analytical India Pvt. Ltd. (Japan)

16. Fujifilm Corporation (Japan)

17. Lepu Medical Tech Co. Ltd. (China)

18. Mindray Medical International (China)

19. Canon Medical Systems (Japan)

20. Allengers Medical Systems Ltd. (India)

21. Samsung Medison (South Korea)

Frequently Asked Questions

1. What is fluoroscopy equipment, and how does it work?

Ans: Fluoroscopy equipment is a modern medical imaging technology that provides real-time, dynamic views of the human body's internal structures using X-rays. It involves the use of X-rays that interact with the patient's body, and the resulting radiation is captured and converted into visible images for diagnostic and interventional purposes.

2. What are the key drivers behind the growth of the fluoroscopy equipment market?

Ans: The growth of the fluoroscopy equipment market is driven by factors such as ongoing technological advancements, the shift from analog to digital fluoroscopy, increased demand for diagnostic and interventional procedures, and the expansion of healthcare infrastructure, especially in emerging markets.

3. How has the commitment to healthcare expenditure and patient safety regulations in North America influenced the adoption of fluoroscopy equipment in the region?

Ans: The commitment to healthcare expenditure and stringent patient safety regulations in North America has driven the adoption of fluoroscopy equipment, leading to the integration of advanced technologies and ensuring compliance with radiation safety standards. These factors have positively influenced the growth of the fluoroscopy equipment market in North America.

4. Which segment of fluoroscopy equipment is expected to dominate the market, and why?

Ans: The mobile fluoroscopy equipment segment is anticipated to dominate the market due to its flexibility, versatility, resource optimization, and continuous technological advancements, making it invaluable for modern healthcare needs.

5. How do technological advancements in healthcare impact the fluoroscopy equipment market?

Ans: Technological advancements have led to the transition from traditional analog fluoroscopy to digital fluoroscopy, improving image quality, reducing radiation exposure, and making fluoroscopy equipment more versatile and efficient. These advancements play a pivotal role in enhancing diagnostic accuracy and supporting minimally invasive medical procedures.