Ferrochrome Market Insights: Growth Drivers, Challenges, and Key Trends by Product Type, End-Use Industry, and Region, Forecast (2026-2032)

Overview

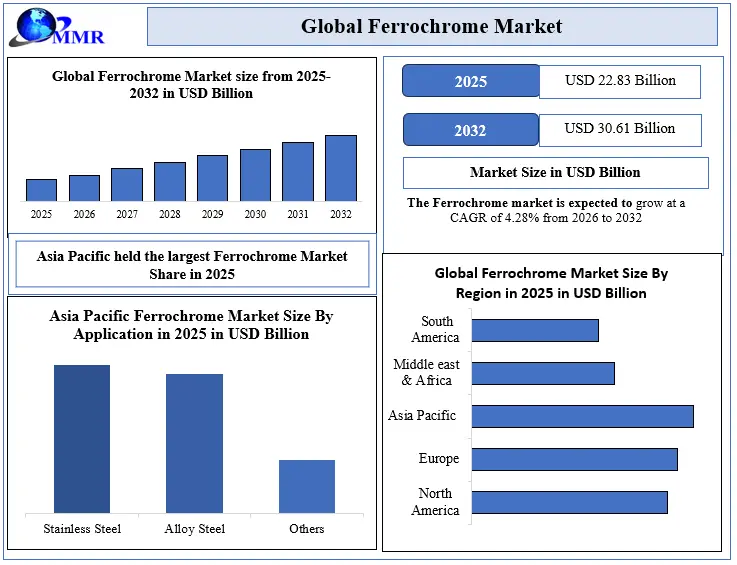

The Ferrochrome Market was valued at USD 22.83 Billion in 2025 to reach USD 30.61 Billion by 2032, growing at a CAGR of 4.28%. The Ferrochrome Market is driven by the increasing demand for stainless steel across industries such as automotive, construction, and consumer goods. The need for corrosion-resistant materials and high-strength alloys fuels ferrochrome consumption.

Ferrochrome Market Overview

Ferrochrome (FeCr) is a crucial ferroalloy composed primarily of chromium and iron. It plays a vital role in the production of stainless steel, contributing significantly to the global manufacturing industry. The Ferrochrome Market has seen substantial growth due to its increasing demand, driven by the stainless-steel sector. Ferrochrome's versatility in steelmaking is evident, especially in the production of stainless steel, where chromium content ranges between 10% to 20%. Countries such as South Africa, Kazakhstan, Turkey and India are the major producers of this alloy due to their vast chromite reserves. Over 80% of the world’s ferrochrome production is consumed in stainless steel production with China accounting for the highest consumption, underlining the alloy's significant role in the global economy.

Ferrochrome Market Key Highlights

• Technological Advancements: The adoption of electric arc furnaces (EAF) has improved production efficiency by 12%. The carbon-neutral technologies have significantly reduced CO₂ emissions by up to 67% in 2025, making production more sustainable and cost-effective.

• Asia-Pacific Dominance: Asia-Pacific remains the largest producer and consumer of ferrochrome, with China, India, and Japan collectively contributing over 60% of global demand. The region’s industrial growth, particularly in automotive and construction, continues to drive ferrochrome consumption.

• Sustainability Initiatives: Leading companies like Outokumpu are prioritizing sustainability with investments such as USD 45 million in a low-carbon ferrochrome pilot plant. This aligns with the global push for eco-friendly manufacturing and meeting environmental regulations.

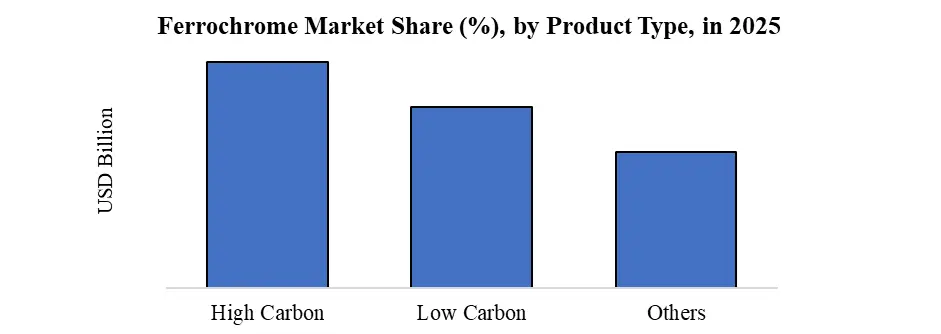

• High Carbon Ferrochrome (HC FeCr): HC FeCr remains the dominant product type, representing over 70% of global ferrochrome production. This product is vital in producing high-strength stainless steel used in the automotive and construction industries.

• Rising Energy Costs: Despite growth, the ferrochrome industry faces challenges due to high energy costs. Electricity consumption remains a significant factor, as ferrochrome production requires 2,800°C temperatures, making energy-efficient innovations crucial for future growth.

• In 2024, South Africa supplied nearly 3.3 Mt of the world’s total ferrochrome production of 17.5 Mt. The country holds over 72% of global chrome reserves, making it the largest chrome reserve holder worldwide.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Trend: Increasing Demand for Stainless Steel

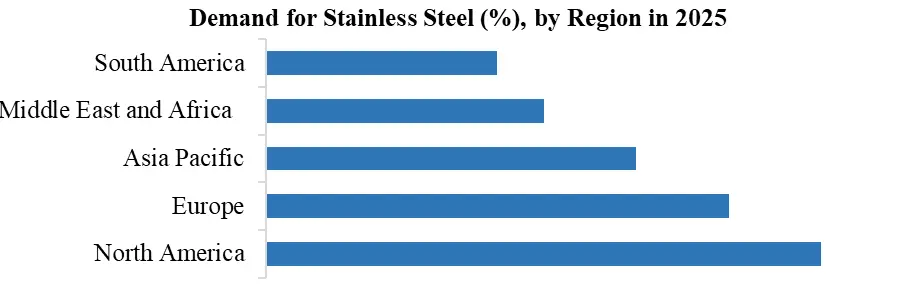

The automotive, construction, and consumer goods sectors are major consumers of stainless steel, which in turn drives the demand for ferrochrome. Stainless steel’s corrosion-resistant properties make it a preferred material for high-performance applications. In 2024, global stainless-steel production was 50 million tons, with the demand for stainless steel growing at a rate of 3-4% annually in emerging economies. As the demand for durable and sustainable materials continues to rise, particularly in regions like Asia-Pacific and south America, the need for stainless steel and, consequently, ferrochrome is projected to grow in tandem. The automotive industry alone accounted for around 10 million tons of stainless steel in 2024, with a projected increase of 5% annually through 2027, which will directly impact ferrochrome demand.

Around 90% of global ferrochrome production is consumed in the manufacture of stainless steel and speciality steels, underlining its critical role in the chromium supply chain. In 2024, global ferrochrome output was approximately 16–17 million tonnes, closely aligned with rising stainless-steel demand. China remains the dominant stainless-steel producer, increasing its output to 40.7 million tonnes (Mt) in 2024, up from 38.3Mt in 2023, reflecting strong domestic demand and capacity expansions. Globally, stainless steel production rose from 60.4Mt in 2023 to 63.3Mt in 2024, marking steady year-on-year growth. This expansion directly supports ferrochrome consumption, as chromium enhances corrosion resistance, strength, and durability in stainless steel applications across construction, automotive, and industrial sectors.

Factors Influencing Global Ferrochrome Demand and Pricing:

• Global stainless-steel production is the main driver of ferrochrome demand.

• China is the largest ferrochrome-producing region and is expanding cost-efficient production capacity.

• South African ferrochrome output has declined due to rising electricity costs.

• European Union regulations, such as the carbon border adjustment mechanism, are affecting production by targeting greenhouse gas emission reductions.

Technological Advancements in Ferrochrome Production

Advancements in production technologies are enhancing the efficiency and cost-effectiveness of ferrochrome manufacturing. Methods such as electric arc furnaces (EAF) and submerged arc furnaces have led to a 10-15% reduction in energy consumption per ton of ferrochrome produced. The new technologies are enabling the production of ferrochrome with significantly lower carbon emissions. In 2025, carbon-neutral ferrochrome technologies reduced CO₂ emissions by up to 67% compared to traditional smelting processes. This is a crucial step for companies aiming to comply with global environmental regulations and reach sustainability goals. Outokumpu, for example, invested USD 45 million in a pilot plant to scale up carbon-free ferrochrome production.

Market Drivers

Sustainability Efforts in Production

Ferrochrome manufacturers are increasingly focusing on sustainability. With global pressure to reduce carbon emissions, companies are adopting cleaner technologies to produce ferrochrome.

• For instance, Outokumpu, a key player in the market, has committed to achieving carbon neutrality at its Kemi mine by 2025. The transition to renewable fuels and the electrification of mining operations are contributing factors to this shift, further enhancing the attractiveness of low-carbon ferrochrome in the market.

High Energy Consumption in Production to Hamper Ferrochrome Market Growth

Ferrochrome production is an energy-intensive process. The carbothermic reduction of chromite requires extremely high temperatures, exceeding 2,800°C. This results in significant electricity consumption, making ferrochrome production costly, especially in regions with high energy prices. The rising cost of energy poses a challenge to the profitability of ferrochrome producers and affects the market dynamics.

Ferrochrome Market Segment Analysis

Based on Product Type, the market is segmented into High Carbon, Medium Carbon and Low Carbon. High carbon ferrochrome (HC FeCr) was the dominant product Type for the ferrochrome market in 2025, accounting for over 70% of global production. With a carbon content between 4% and 9%, it is primarily used in the production of stainless steel, especially for applications requiring high-strength materials, such as in the automotive and construction industries.

The demand for HC FeCr is directly correlated to the global stainless-steel production. South Africa, Kazakhstan, and India are the major producers of HC FeCr, with South Africa leading the market, contributing over 40% of global production. The segment’s growth is driven by the rising demand for high-quality stainless steel and increasing industrialisation in emerging economies.

Ferrochrome Market Regional Insights

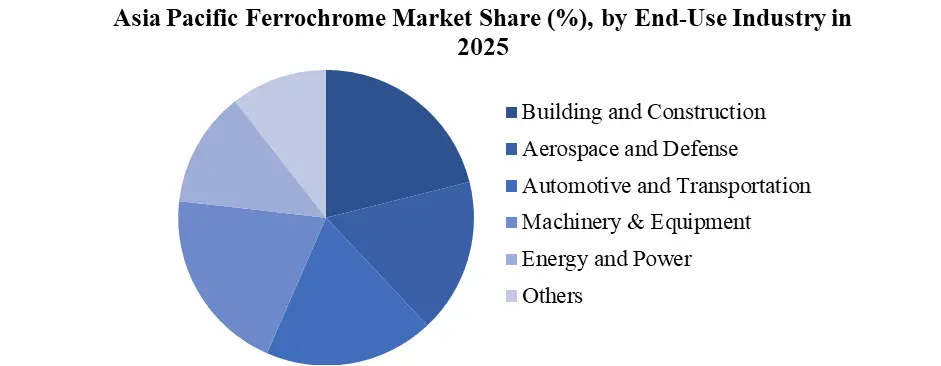

Asia Pacific dominated the Ferrochrome Market in 2025. The Asia-Pacific region is a significant player in the global ferrochrome market, driven by its extensive steel production and large-scale manufacturing industries. Countries like China, India, and Japan are the leading consumers and producers of ferrochrome in the region. China, in particular, accounts for the largest share of ferrochrome consumption, primarily due to its dominance in the steel industry. The demand for ferrochrome in the Asia-Pacific is strongly influenced by the region’s infrastructure development, automotive growth, and expanding consumer goods sectors.

India is another major consumer, with ferrochrome consumption increasing by 4-5% annually in recent years, particularly in the automotive and construction sectors, which are vital for its expanding industrial base. As these economies continue to industrialise, the demand for stainless steel and, consequently, ferrochrome is expected to remain high. The region's ferrochrome production facilities are concentrated in countries with abundant chromite reserves, ensuring a steady supply of this critical alloy.

Ferrochrome Market Competitive Landscape

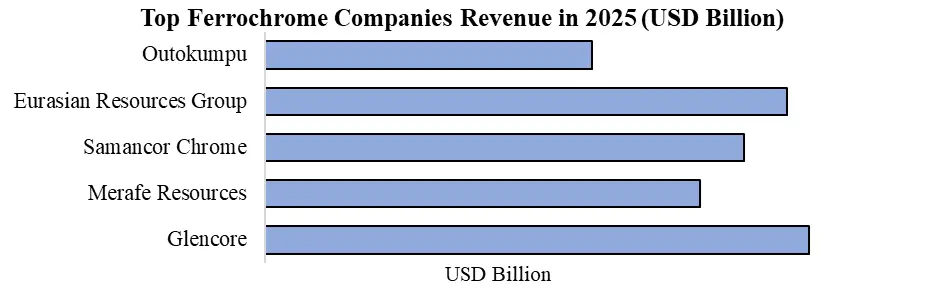

The Ferrochrome Market is moderately consolidated, with several major global producers shaping industry dynamics through capacity, geography, and strategic initiatives. Key players include Glencore International AG, Eurasian Resources Group (ERG), Samancor Chrome Ltd., Merafe Resources, Tata Steel Limited, Outokumpu Oyj, Indian Metals & Ferro Alloys Ltd (IMFA), Hernic Ferrochrome Pty Ltd., Afarak Group, and Assmang each with substantial production, diverse product portfolios, and regional strengths.

Ferrochrome Market Recent Developments

• October 29, 2025 – Outokumpu Invests USD 45 Million in Chromium Metal and Enriched Ferrochrome Pilot Plant.

Outokumpu has announced a USD 45 million investment in a new pilot plant in New Hampshire, U.S., to produce enriched ferrochrome and chromium metal. The plant, set to be operational by H1 2027, will scale production from lab-scale (1g) to industrial-scale (1 ton) and is a key part of Outokumpu’s EVOLVE strategy to produce low-carbon, high-purity materials. This pilot project aims to advance the company’s speciality metals business, with the potential to build an industrial plant by 2029–2030.

Ferrochrome Market Scope: Inquire before buying

| Ferrochrome Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 22.83 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.28% | Market Size in 2032: | USD 30.61 Bn. |

| Segments Covered: | by Product Type | High Carbon Medium Carbon Low Carbon Others |

|

| by Application | Stainless Steel Alloy Steel Others |

||

| by End-Use Industry | Building and Construction Aerospace and Defense Automotive and Transportation Machinery & Equipment Energy and Power Others |

||

Ferrochrome Key Players

1. Glencore

2. Merafe Resources

3. Samancor Chrome

4. Eurasian Resources Group

5. Outokumpu

6. Tata Steel

7. IMFA (Indian Metals & Ferro Alloys)

8. Assmang Proprietary Limited

9. Tharisa

10. Afarak Group

11. (FACOR)

12. Yildirim Group

13. Mintal Group

14. Zimasco

15. Jindal Steel & Power

16. Balasore Alloys

17. VISA Steel

18. Sichuan Mingda Group

19. Ehui Group

20. Sinosteel Corporation

21. China Minmetals Corporation

Frequently Asked Questions:

1. What are the growth drivers for the Ferrochrome Market?

Answer: The ferrochrome market is driven primarily by the increasing demand for stainless steel across industries such as automotive, construction, and consumer goods. The rise in infrastructure development, automotive growth, and consumer goods sectors in emerging economies, particularly in the Asia-Pacific, is expected to continue fueling the demand for ferrochrome.

2. What are the major restraints for the growth of the Ferrochrome Market?

Answer: Key restraints include high energy consumption in ferrochrome production, which requires extremely high temperatures (~2,800°C), leading to increased electricity costs. Additionally, carbon emission regulations and environmental concerns are pushing manufacturers to invest in cleaner technologies, which could affect profitability in the short term.

3. Which region dominated the global Ferrochrome Market in 2025?

Answer: Asia-Pacific dominated the ferrochrome market in 2025, with China, India, and Japan being the leading consumers and producers. The region's dominance is attributed to its high steel production, industrial growth, and abundant chromite reserves in countries like India and Kazakhstan, ensuring a stable supply of ferrochrome.

4. What was market size in 2025 and growth rate of the Ferrochrome Market?

Answer: The global ferrochrome market was valued at USD 22.83 billion in 2025 and is projected to grow at a CAGR of 4.28%, reaching USD 30.61 billion by 2032. This growth is primarily supported by the rising demand for stainless steel, increased technological innovations, and sustainability initiatives across the industry.

5. What segments are covered in the Ferrochrome Market report?

Answer: The report covers segmentation by Product Type, Application and End-Use Industry and Region.